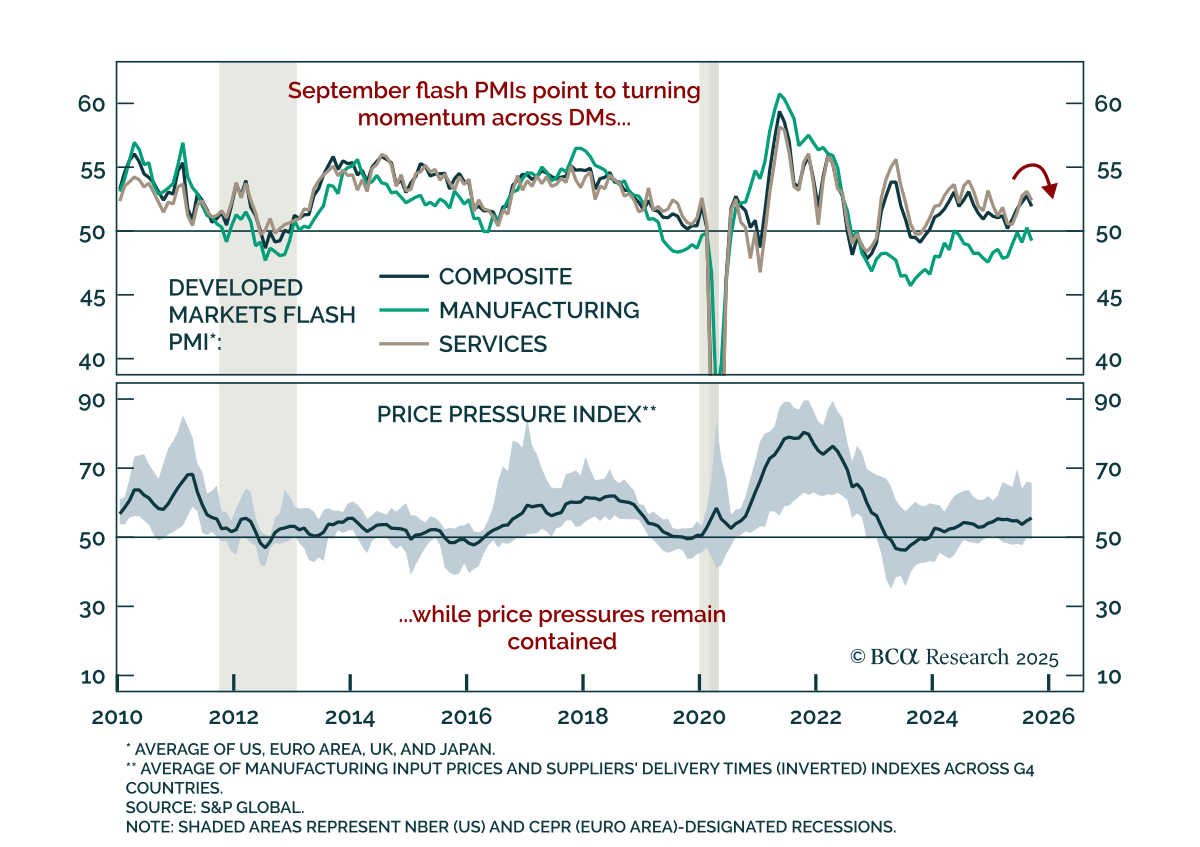

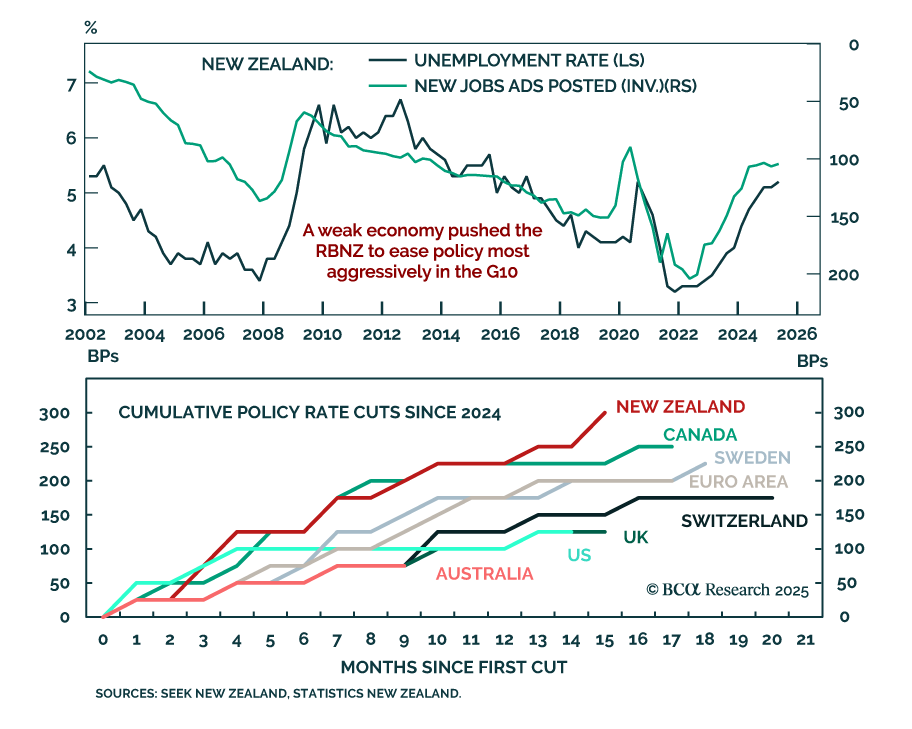

Developed Countries

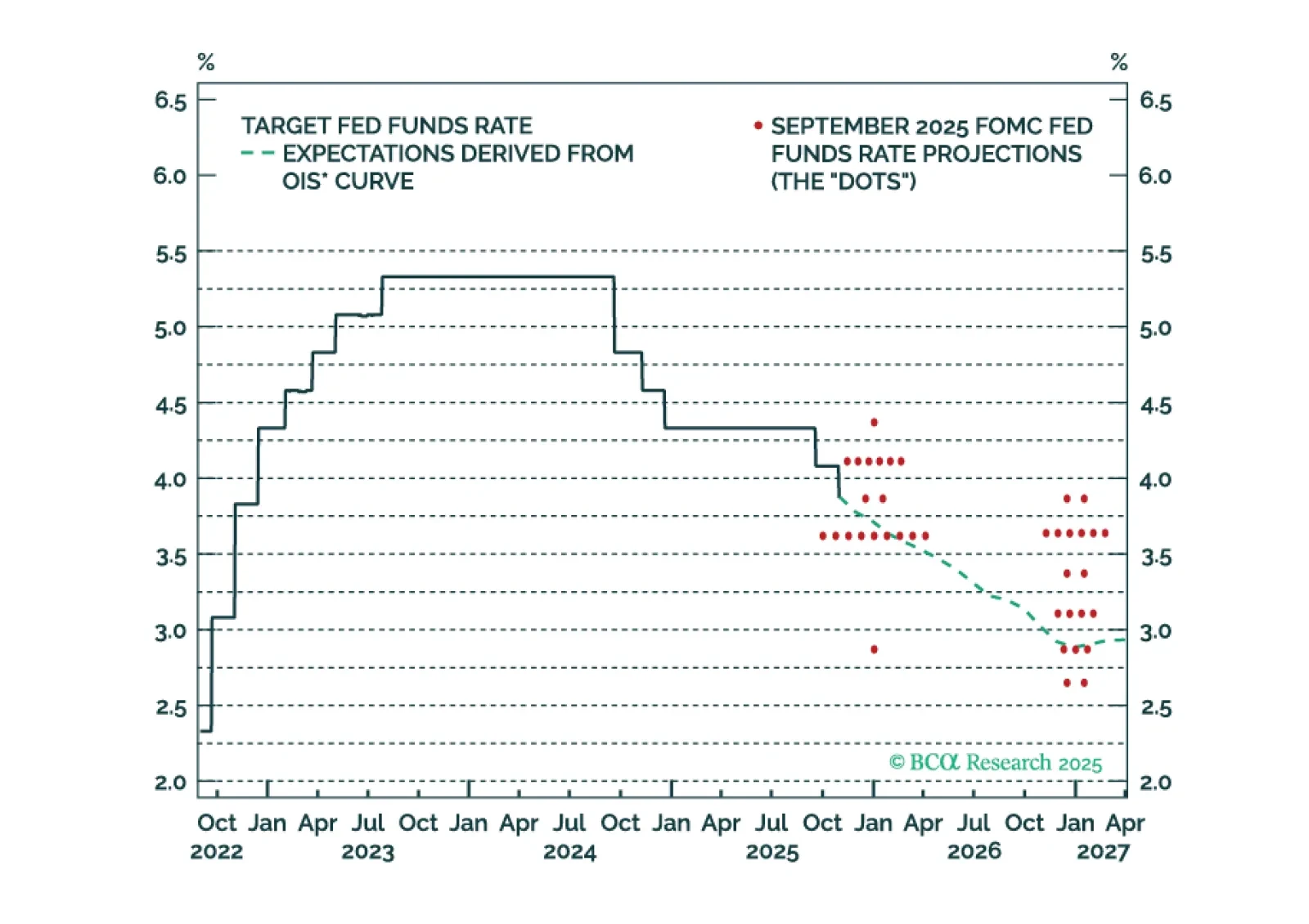

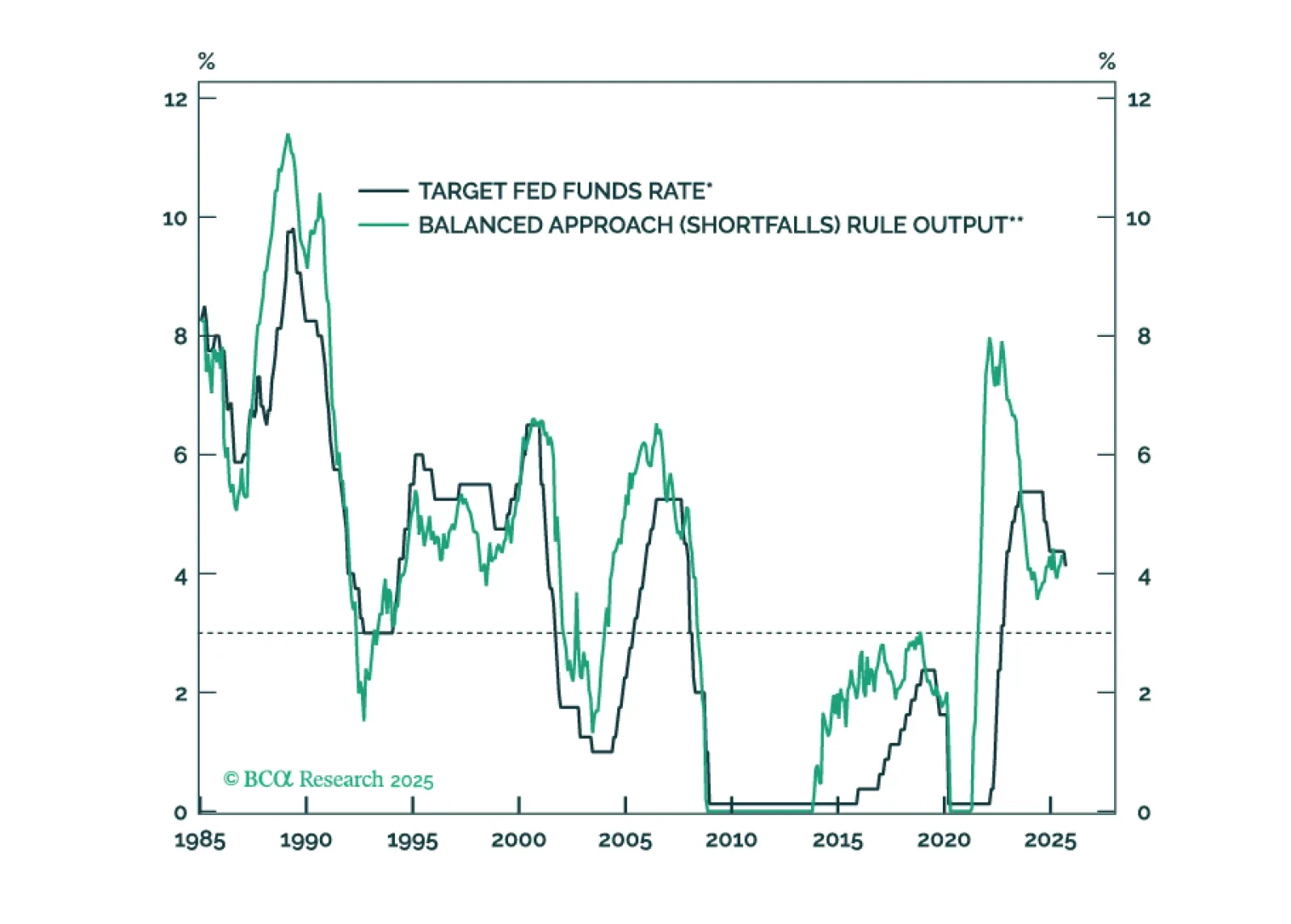

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

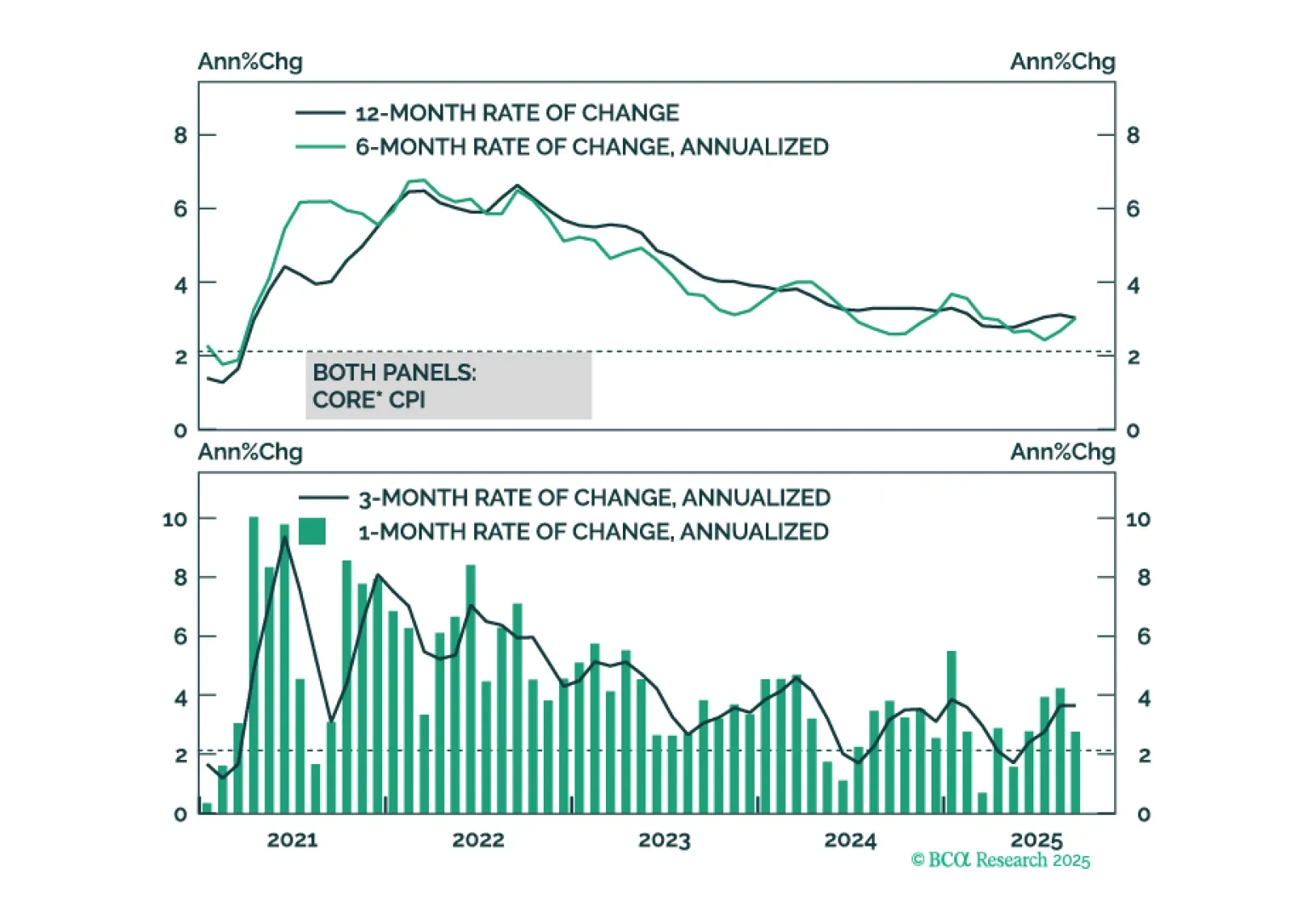

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

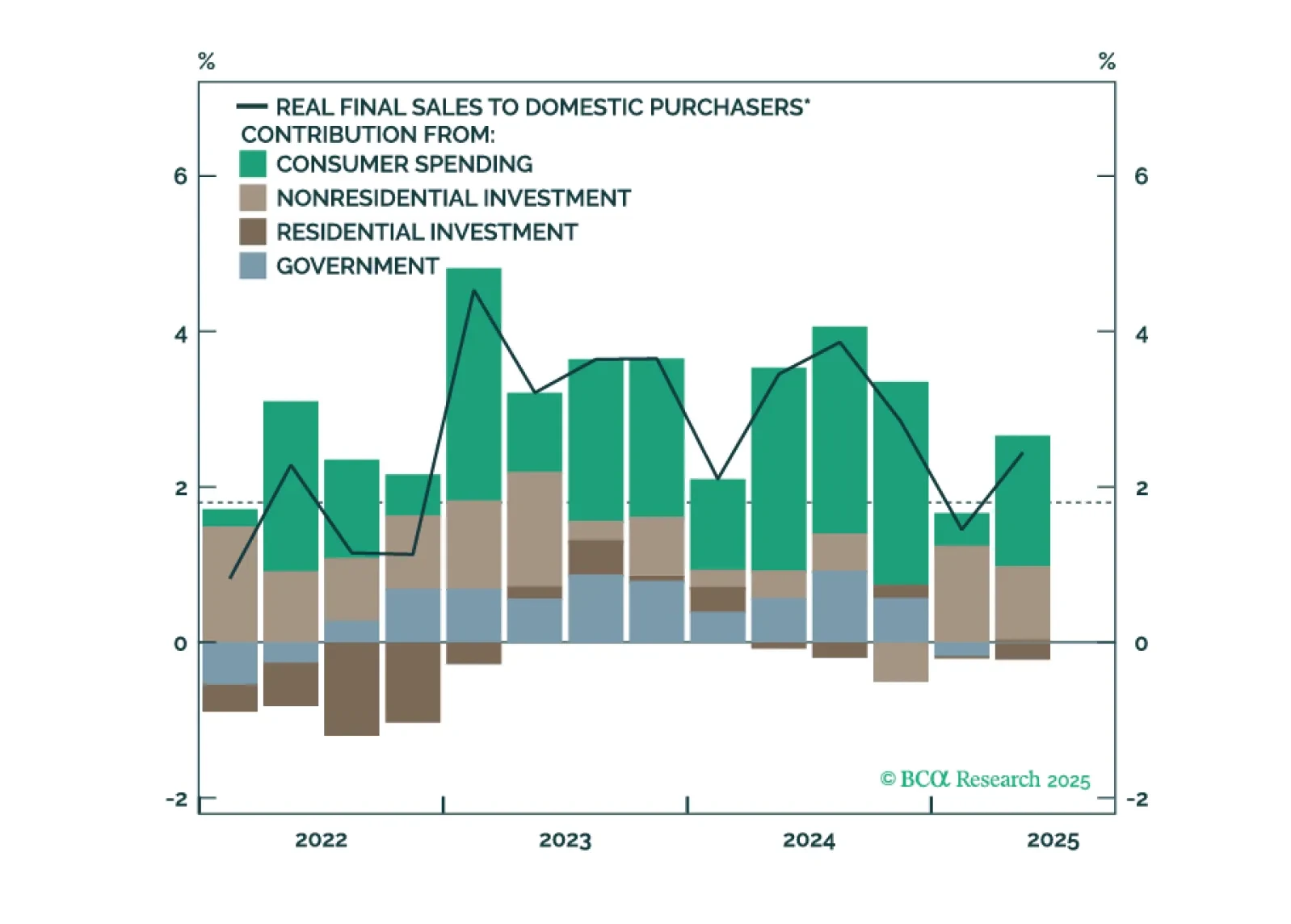

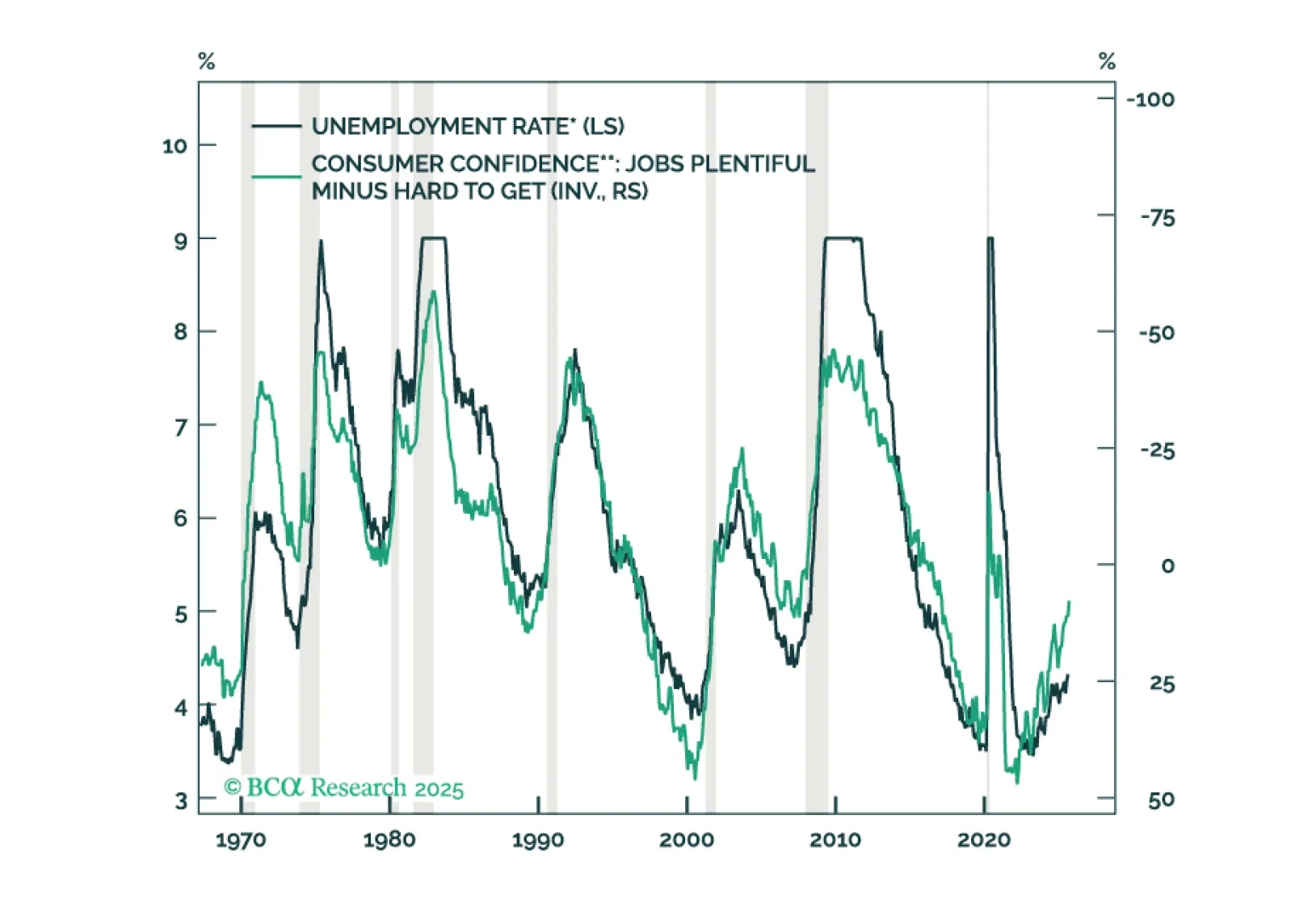

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

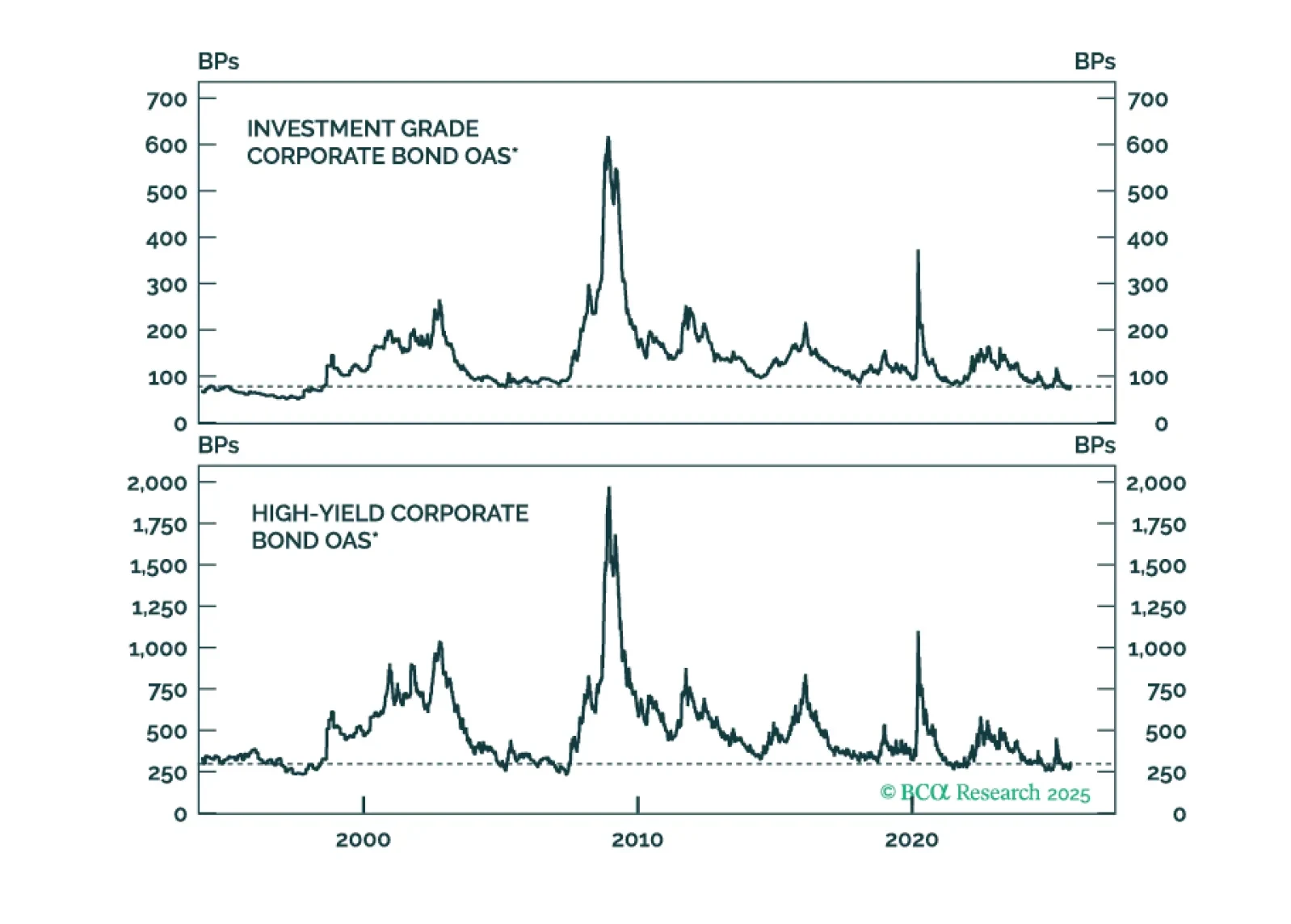

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.

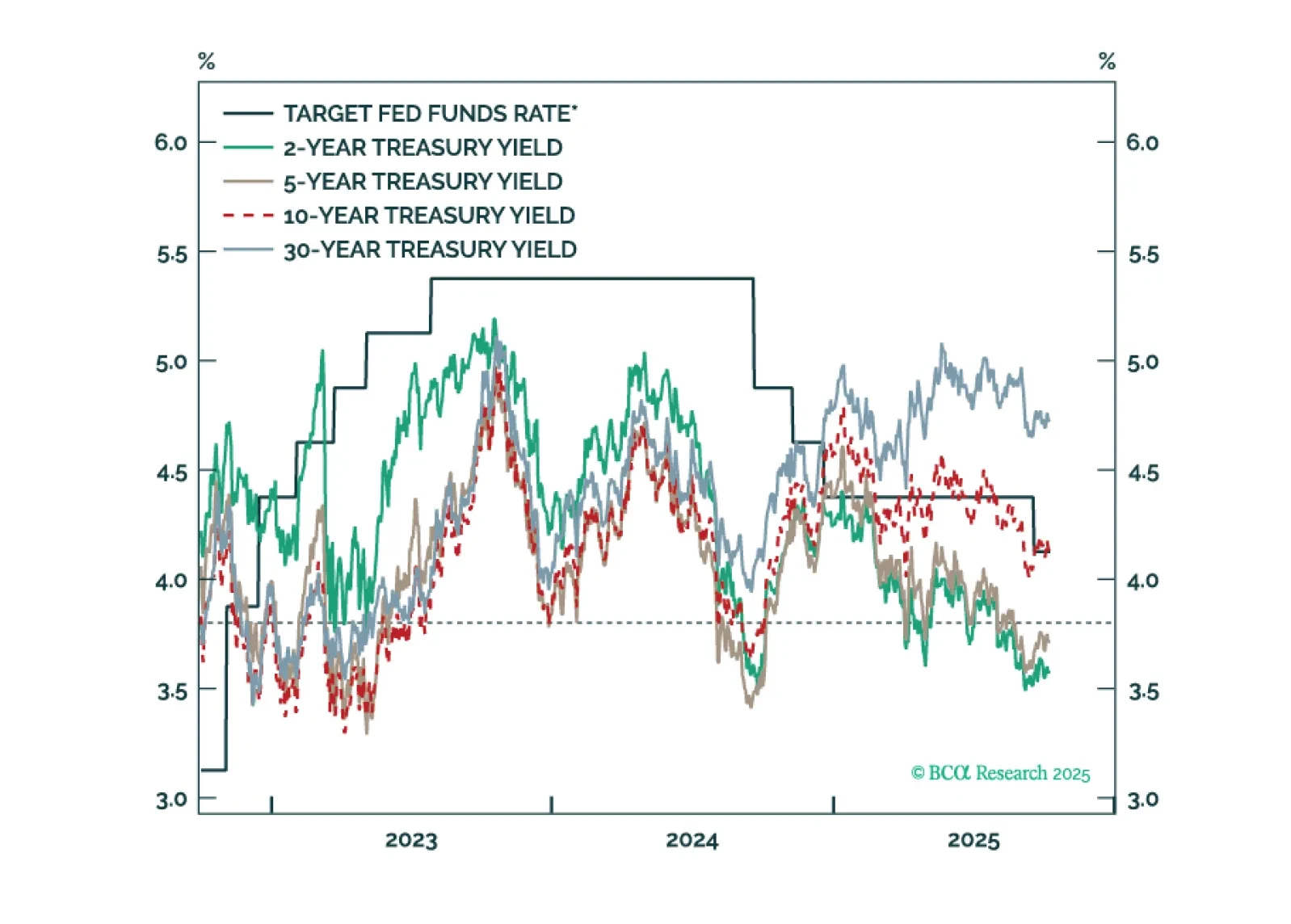

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Our Portfolio Allocation Summary for October 2025.

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.