Developed Countries

The November CPI came in line with expectations, accelerating to 0.3% m/m (2.7% y/y) from 0.2% (2.6% y/y) in October. Core also printed at 0.3% m/m, the same as October and remaining at 3.3% y/y. The acceleration was mainly driven by food and used cars. …

Our US equity strategists just published their annual outlook, where they discuss the environment and rotation they foresee in 2025, which is more bullish than our House View. Our colleagues see Trump 2.0 policies driving economic growth and…

We offer 5 key investment views for US fixed income markets in 2025.

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

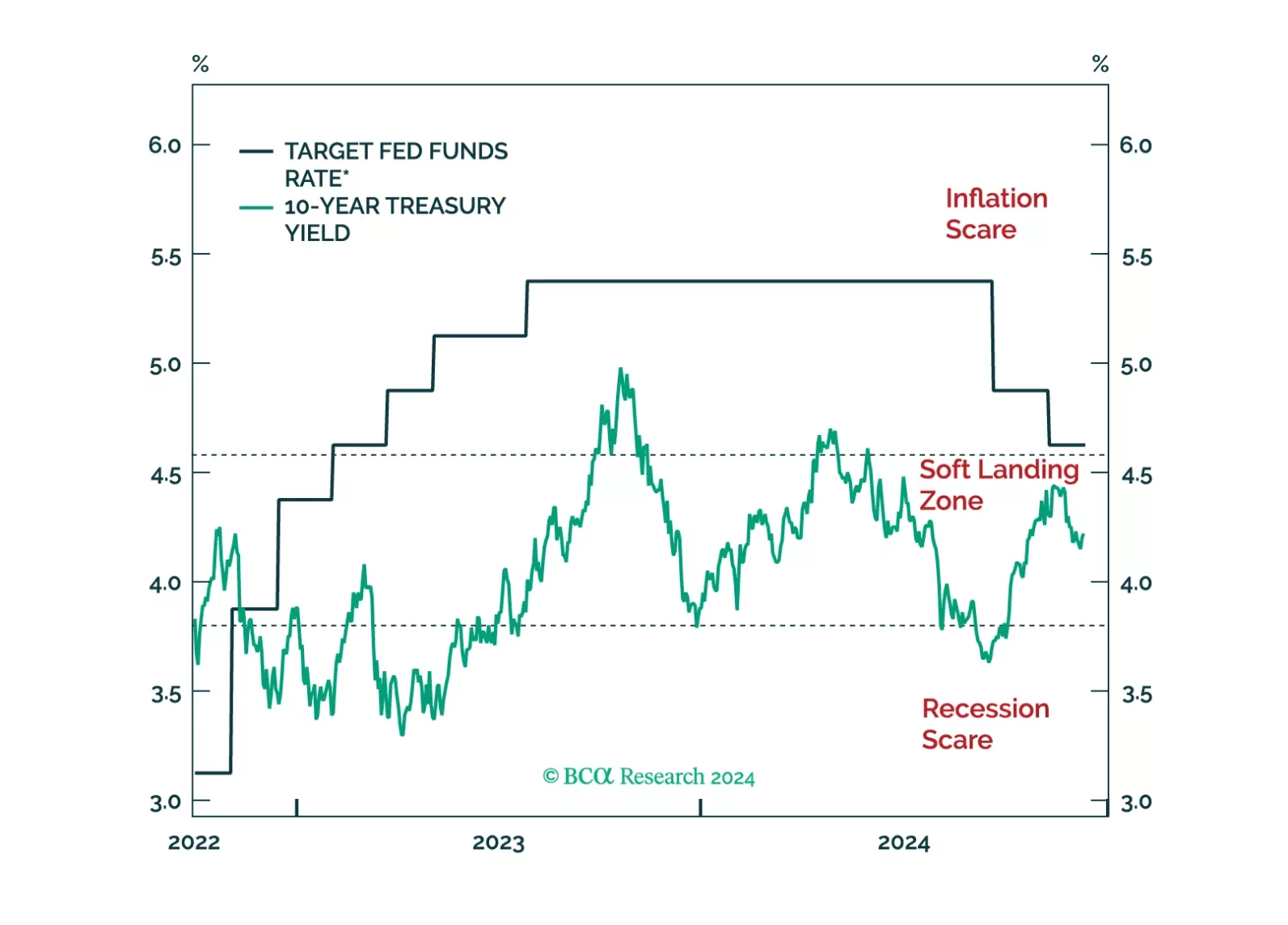

US economic data have generally surprised to the upside for the last few months, further swelling the bulls’ ranks. BCA is skeptical of the optimism, however, and recommends that investors pull in their horns ahead of the new year.

The November NFIB Small Business Optimism index beat expectations, jumping to 101.7 from 93.7 in October. Outside of inventory satisfaction, which was flat, all index subcomponents increased, led by measures of expectations. The outlook for general business…

Our Geopolitical Strategy team published their annual outlook, and see three trends shaping 2025. First, Congress is expected to pass tax cuts by the end of 2025, providing a fiscal thrust of 0.9% of GDP in 2026. This stimulus will likely…

The December Sentix Economic Index for the Euro Area missed expectations, declining to -17.5 vs. -12.8 in November. Both the current situation and expectations components declined. As the first sentiment indicator for December, the Sentix confirms…

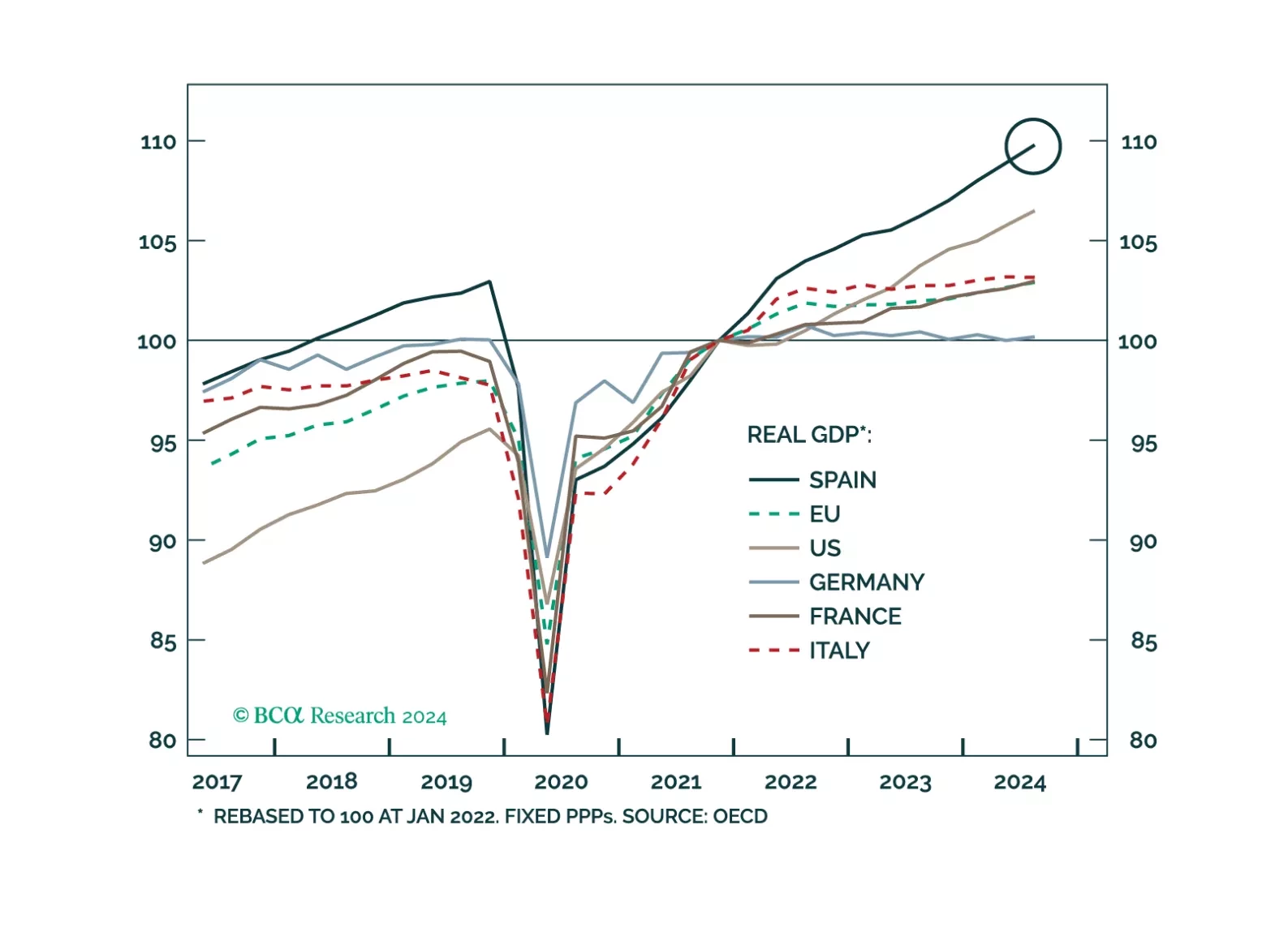

In the final installment of their “PIGS Have Wings” special series, our European investment strategists took a deep dive into the Spanish economy and financial assets. Spain outperformed most developed markets since 2022, with strong gains in both…

Spain has outperformed most developed markets since 2022 – real economic output and risk assets alike. Can it last?