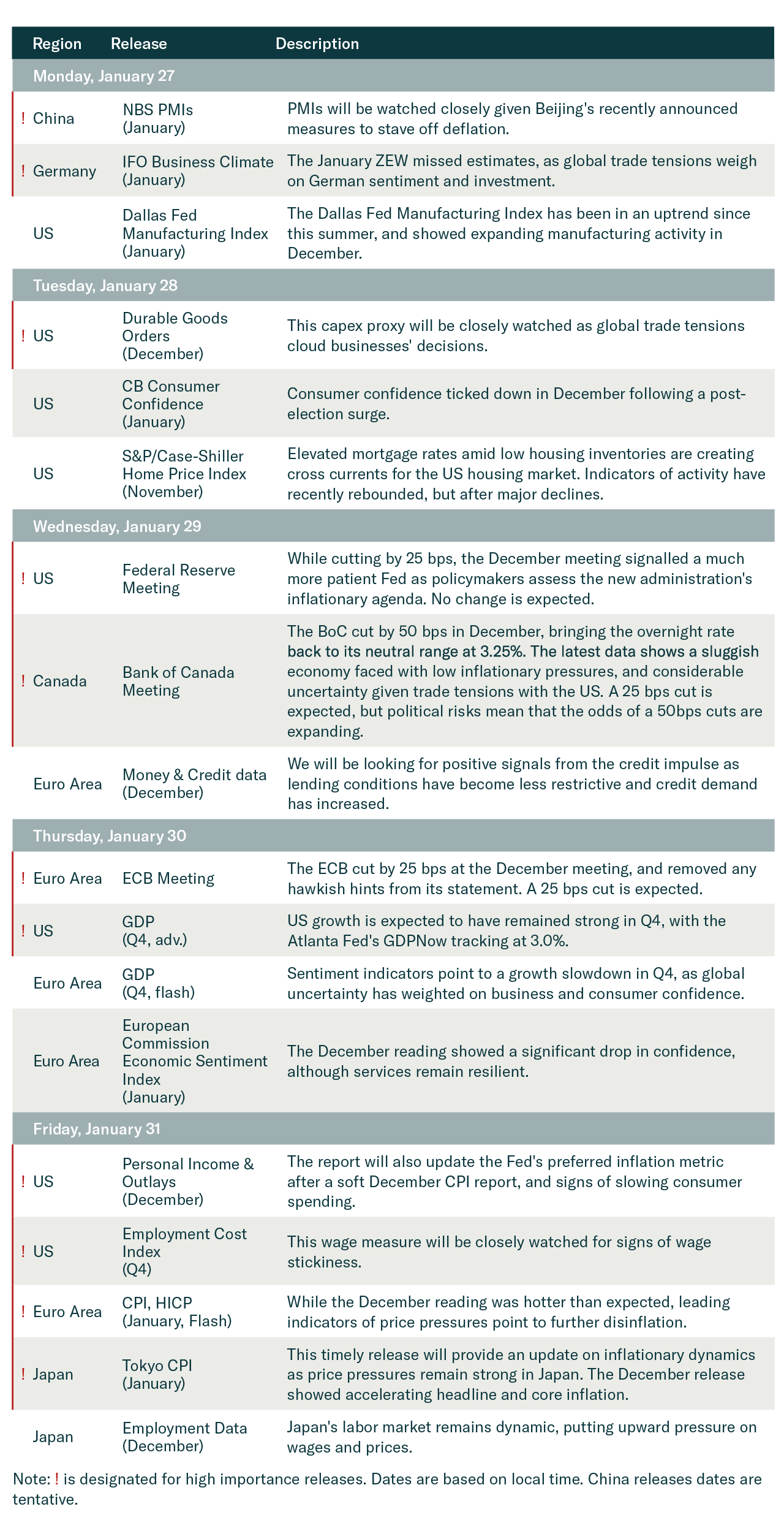

Developed Countries

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

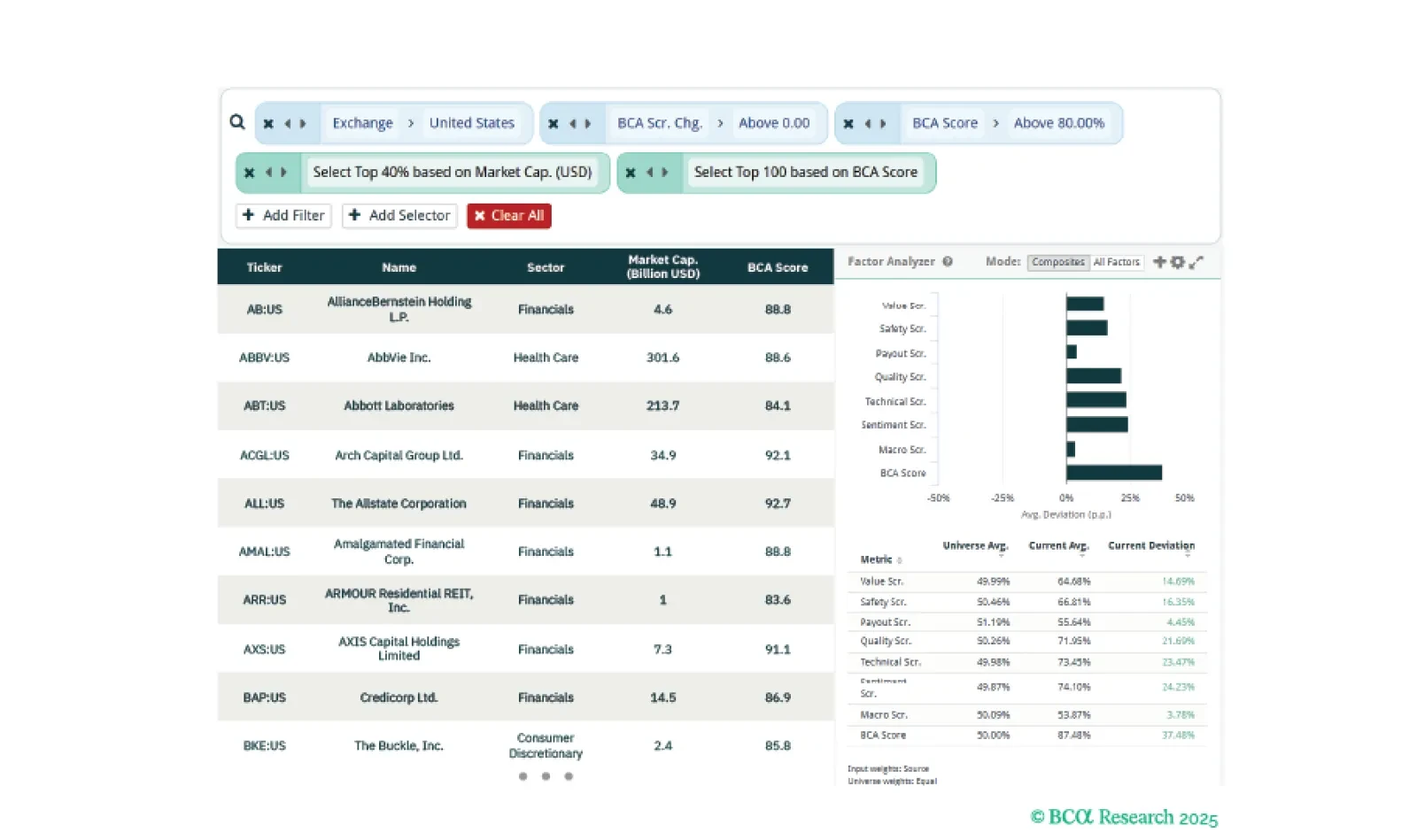

This week, our three screeners show you how to setup easy monitoring of the BCA Score, take advantage of earnings season in the US, and seek out global stocks that are cheap and high quality.

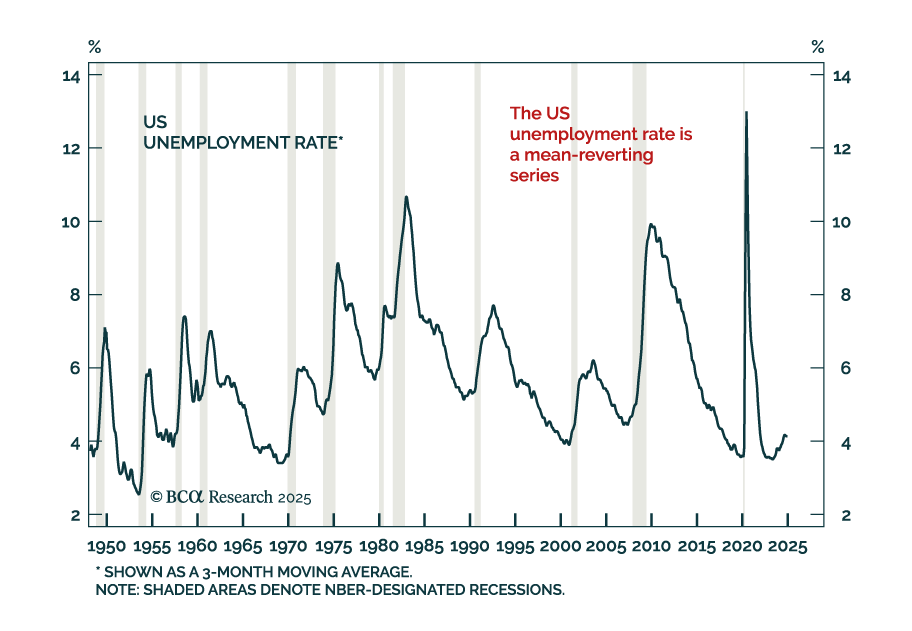

Our Global Investment strategists believe the US economy is in a more precarious position than investors realize. A slowdown in growth could raise unemployment, while stronger activity may heighten inflation worries. The economic momentum seen in late…

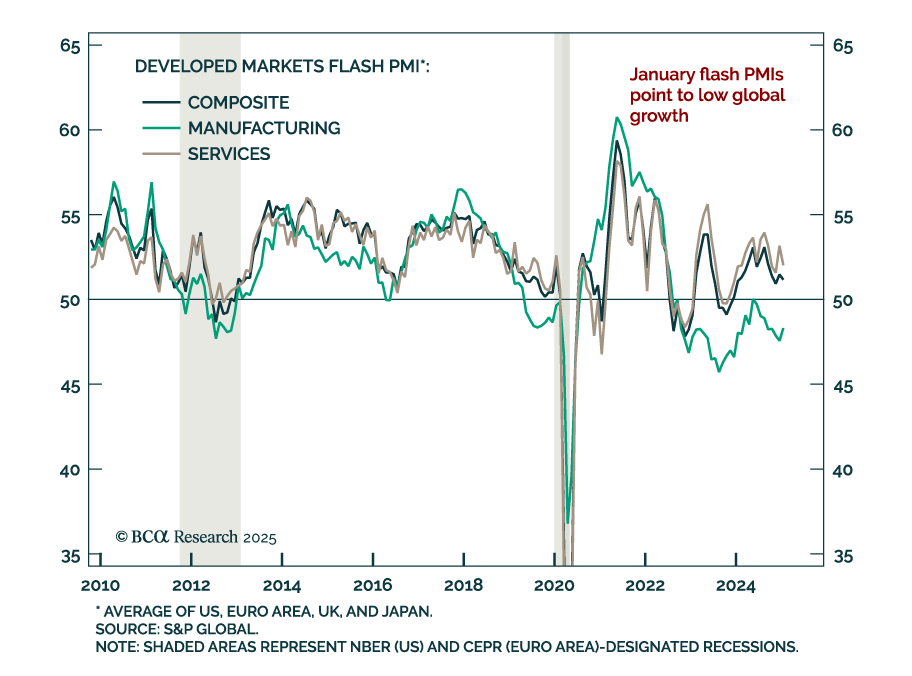

January’s flash PMIs for the major developed markets showed that manufacturing contracted at a slower pace and service activity continues to display significant regional differences. Moreover, the performance gap between the US and its DM peers…

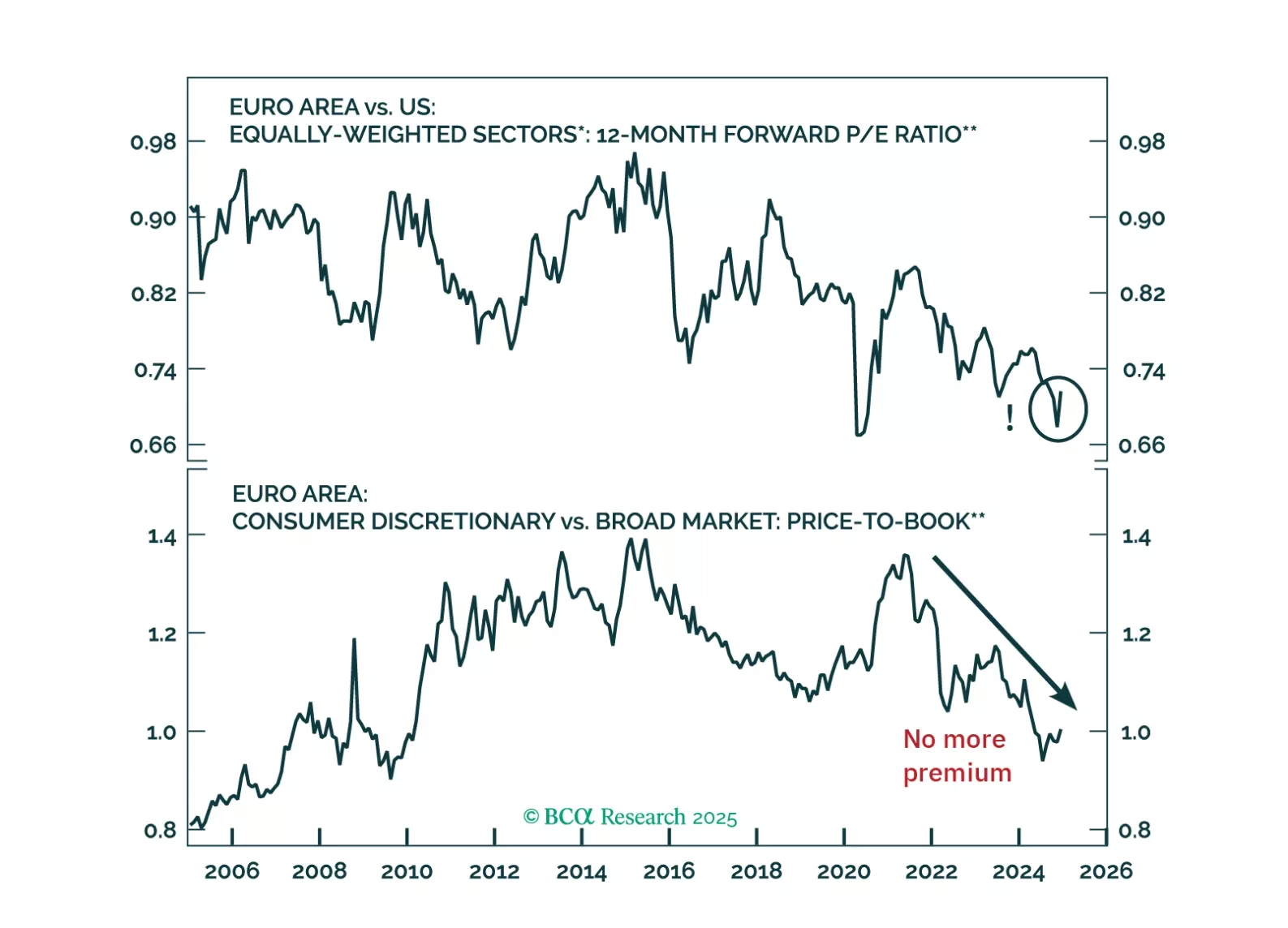

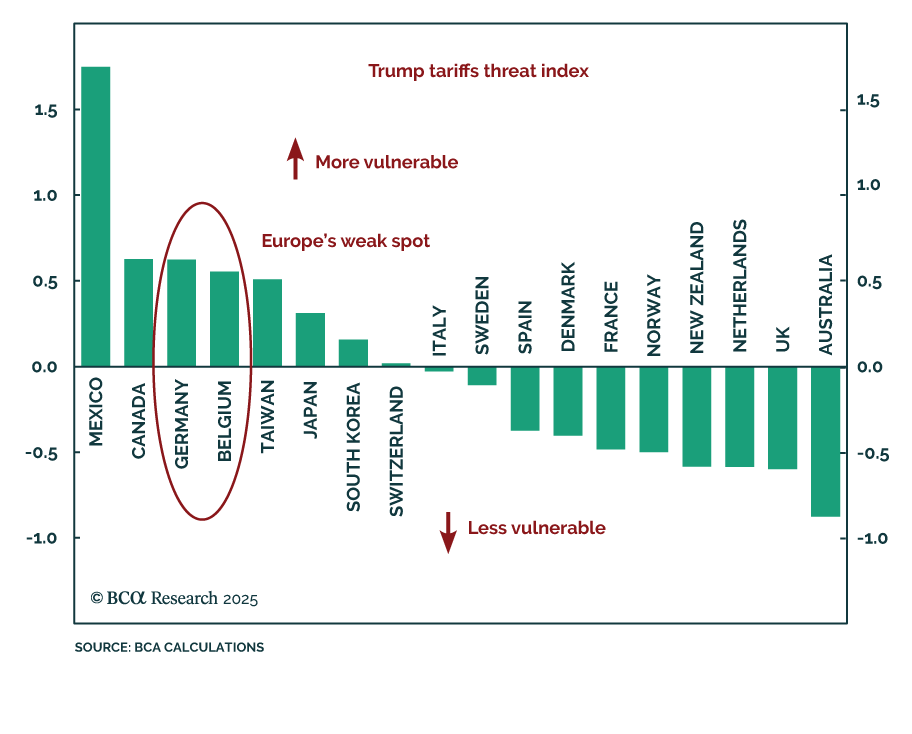

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu investigates why President Trump started his global trade offensive with an attack on Canada and Mexico, the US’ two closest…

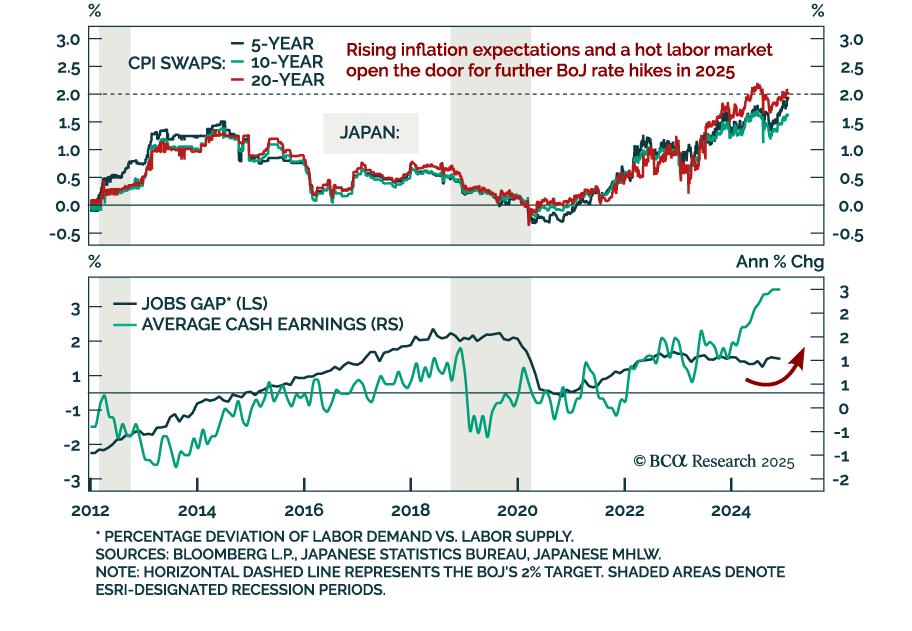

The Bank of Japan hiked rates by 25 bps as expected to 0.50%, or a 17-year high. The BoJ is currently the only G10 central bank in a hiking cycle, as the hot labor market creates sustained domestic price pressures. Additionally, the BoJ signaled a…

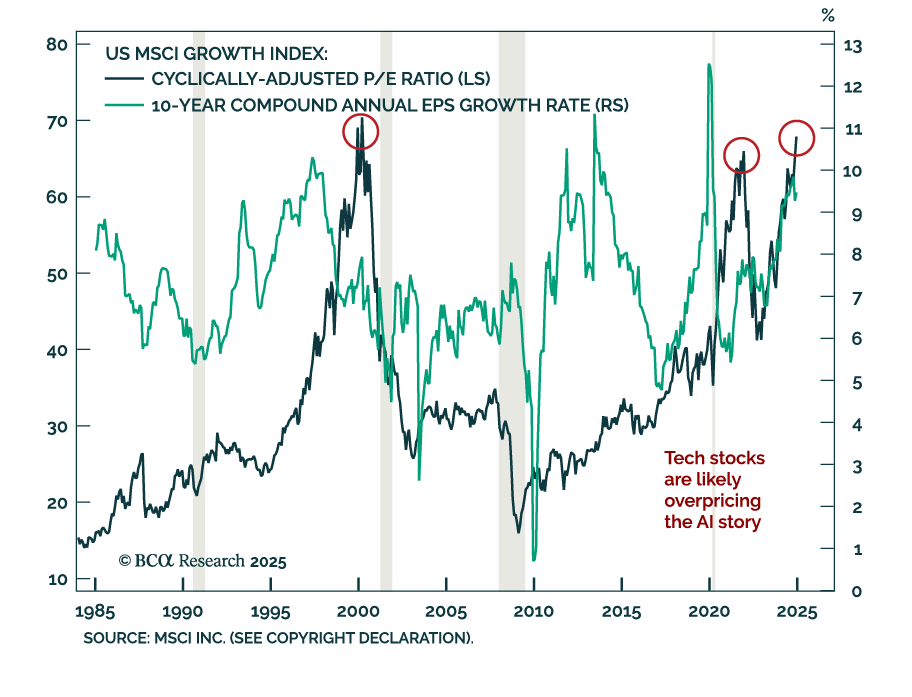

The Magnificent 7 have a leg up on AI investments over the rest of the market. Although the future impact of AI on productivity and profits is still debated, current tech stocks valuations reflect great optimism that AI indeed will be massively accretive to…

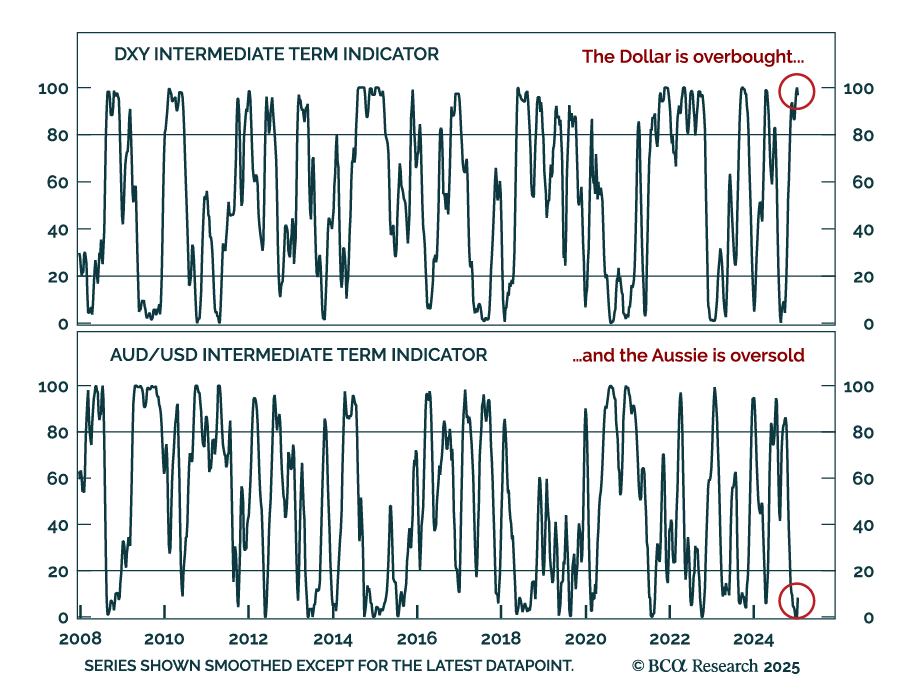

Our Foreign Exchange strategists recently provided an update on their US and Australian dollar views. The US dollar remains overbought and may continue rising as a momentum currency, but cyclical indicators suggest a capitulation phase. Our FX team…

Despite the choppy price action of the last few weeks, equity sentiment remains elevated. Surveys of investor sentiment remain at the top end of the bullish spectrum, and the S&P 500 is trading over 22x forward earnings, levels only seen in the…