Developed Countries

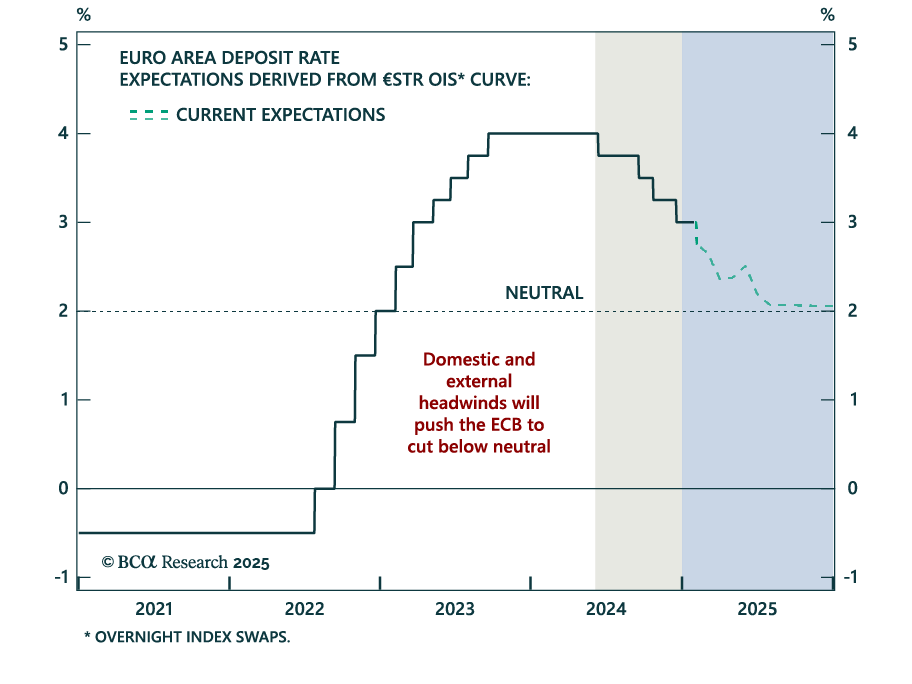

The ECB cut its deposit rate to 2.75%, as was widely anticipated. President Christine Lagarde did not provide any fireworks, but the Governing Council’s message was clear: Policy is restrictive, and inflation will fall further. As a result, if we combine our economic forecasts for the Eurozone with Frankfurt’s data dependency, we continue to expect the ECB’s deposit rate to settle below 2%. Consequently, German bond yields have downside, and the euro has yet to bottomed.

The ECB cut by 25 bps as expected, bringing the deposit facility rate to 2.75%. Despite avoiding committing to a path for policy, President Lagarde reiterated the disinflationary process is “well on track”, and did not push against current market pricing,…

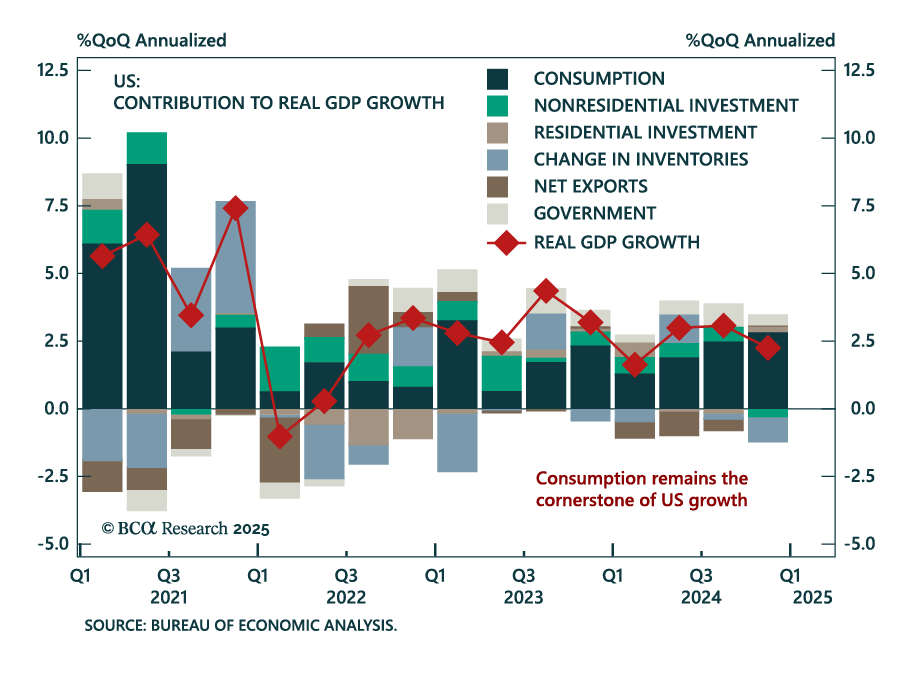

Advanced Q4 US GDP missed estimates, slowing down to 2.3% quarterly annualized growth from 3.1%. The weakness was however driven by inventories. Consumer spending beat estimates and accelerated to 4.2% from 3.7% in Q3. Growth is still above trend as the US…

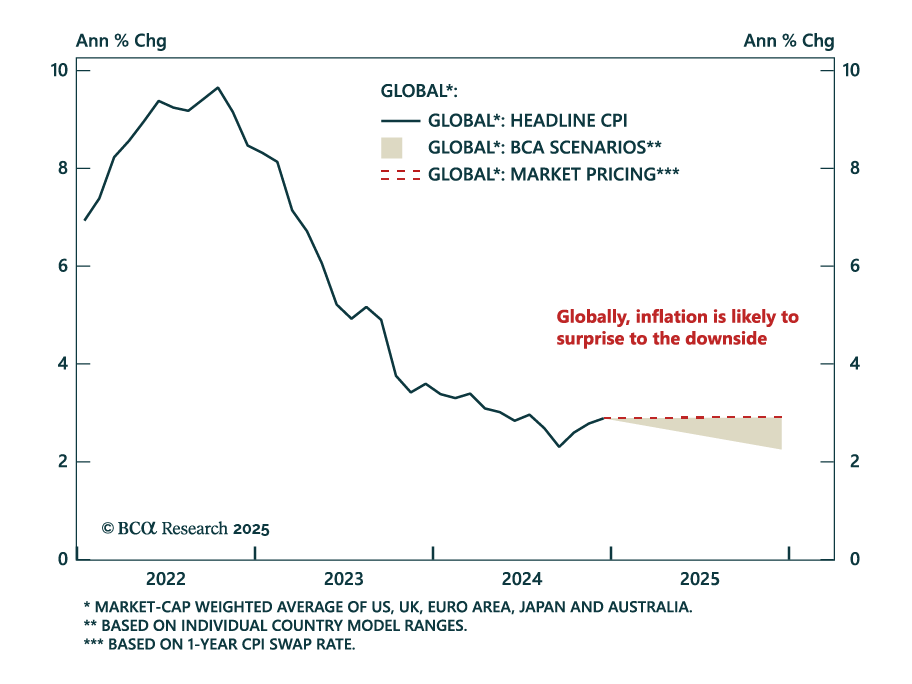

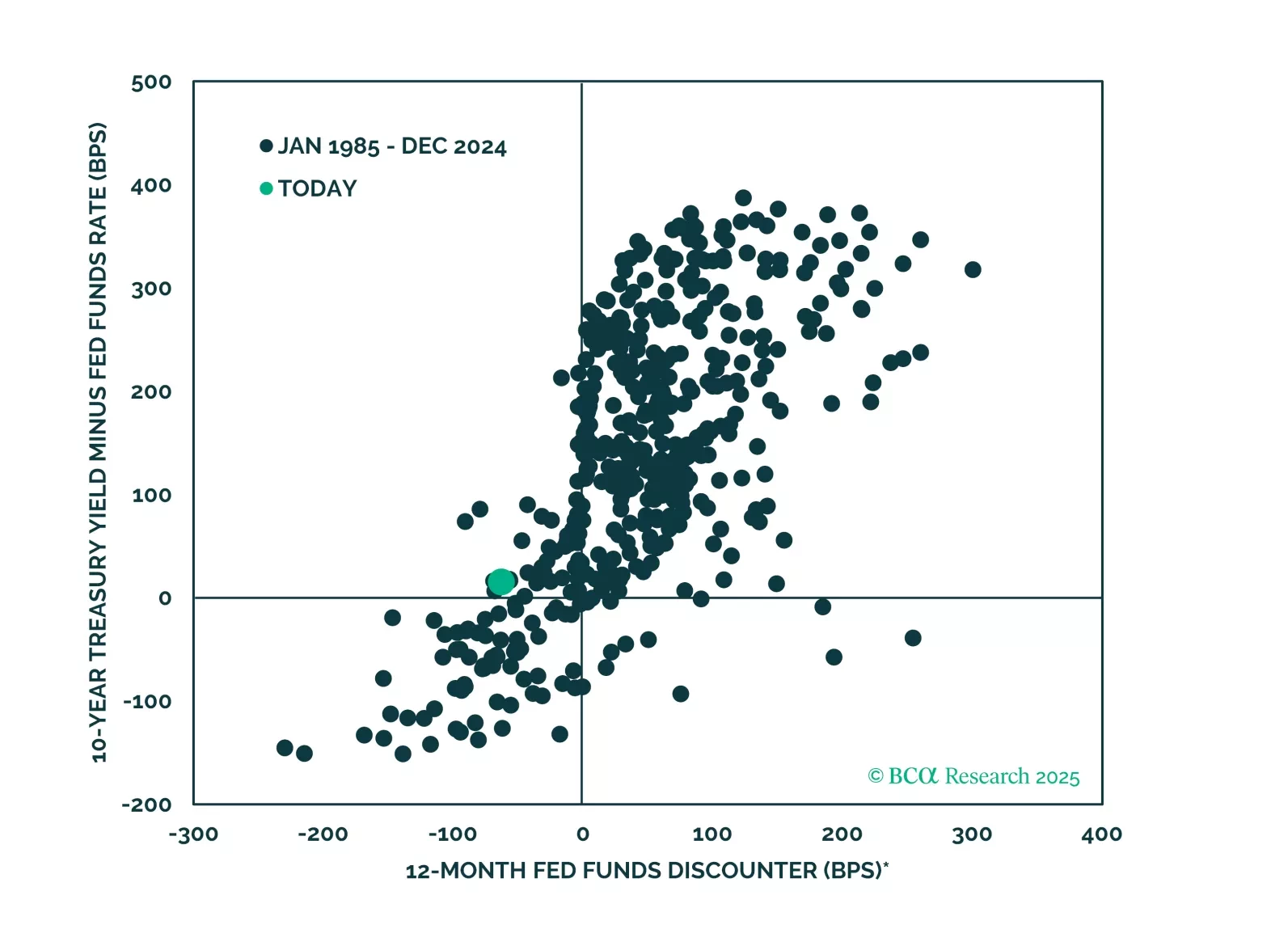

Our Global Fixed Income strategists assessed the risk of a second wave of inflation, and discussed the opportunities within the inflation-linked bond (ILB) market. Global disinflation remains on track, though energy prices and tariffs pose upside risks.…

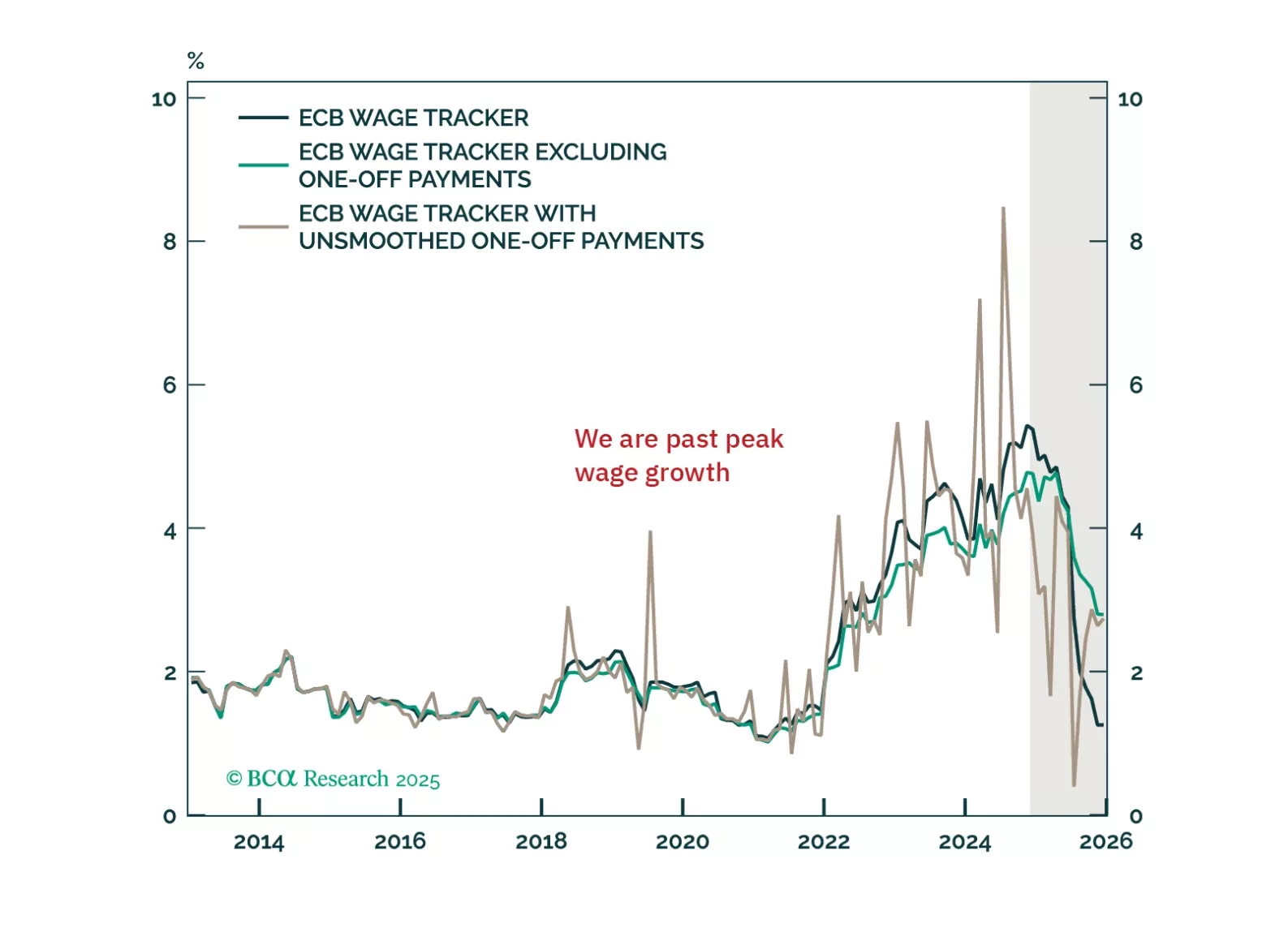

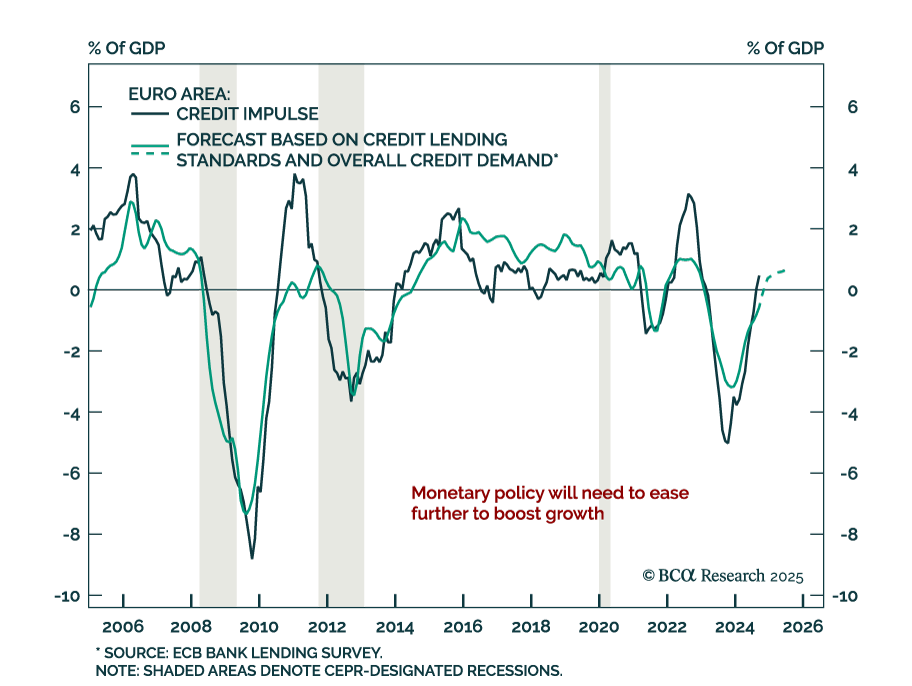

The January 2025 ECB bank lending survey saw a net tightening of credit standards in Q4 2024. Credit standards were tightened for business and consumer lending, and were roughly unchanged for home mortgage loans. Banks expect further tightening across all…

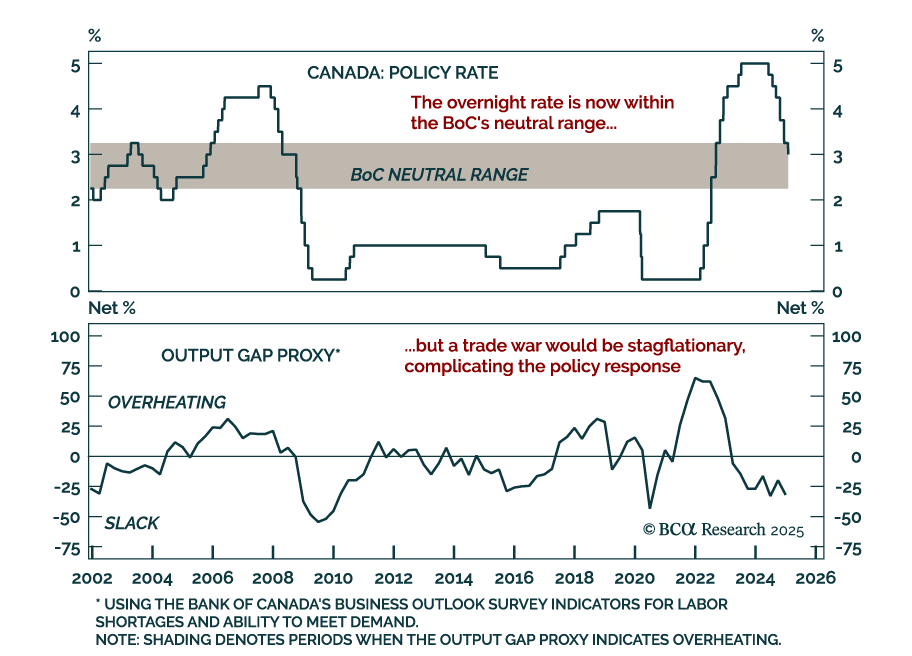

The Bank of Canada cut by 25 bps to 3% as expected, and announced the end of quantitative tightening. This sixth consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC assessed…

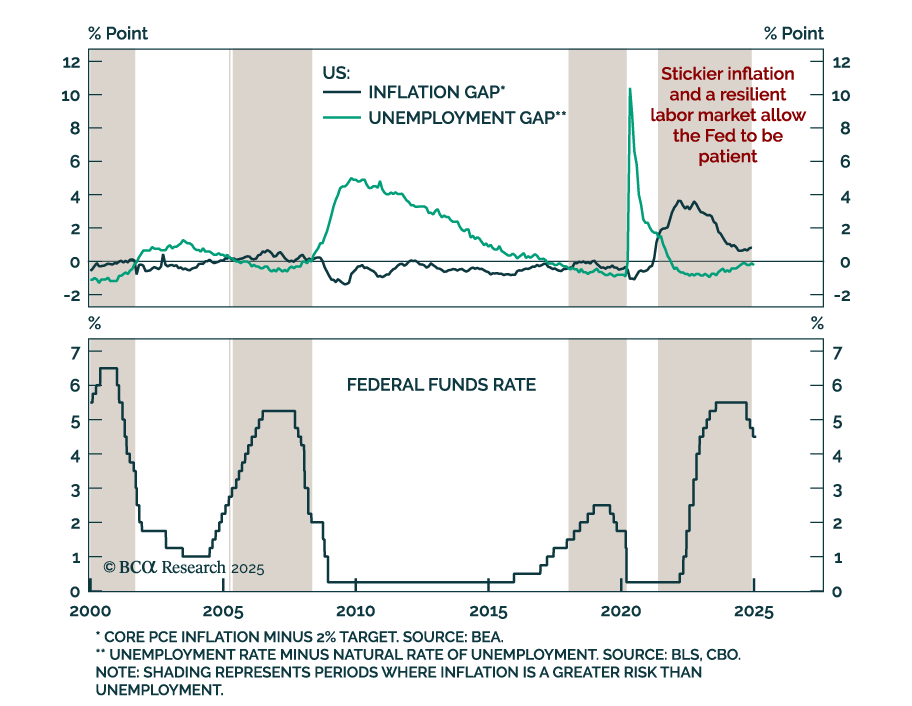

The Federal Reserve kept rates on hold in its 4.25%-to-4.5% range, as expected. The main change in the statement was the removal of the reference to progress towards the Fed’s 2% target, leaving instead a simple mention that inflation “remains somewhat…

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

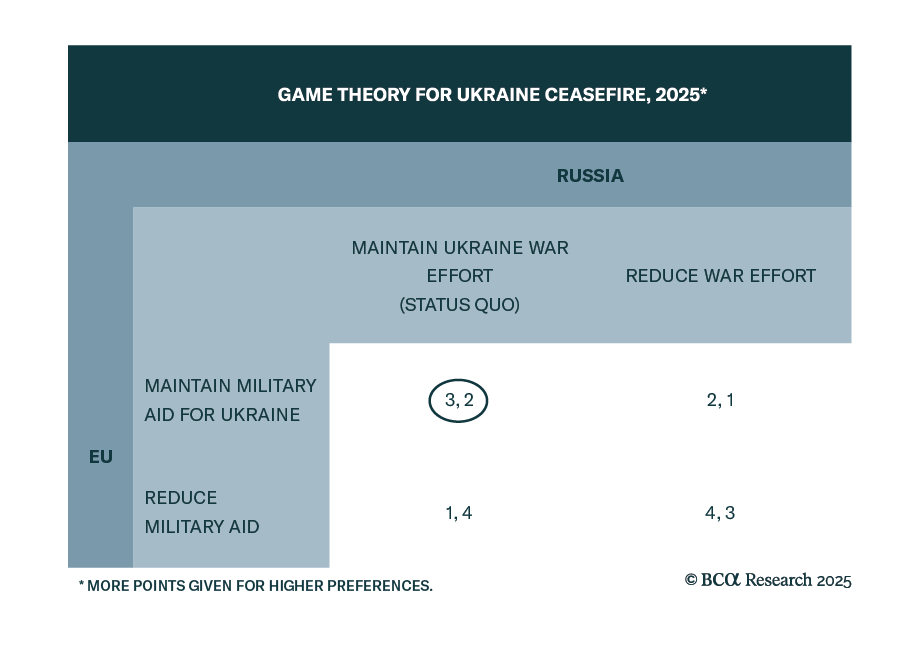

Our Geopolitical Strategy team modeled several of the Trump administration’s most disruptive policies in a simple game theory framework. The Trump administration’s policies have created a complex web of trade and foreign negotiations, increasing…

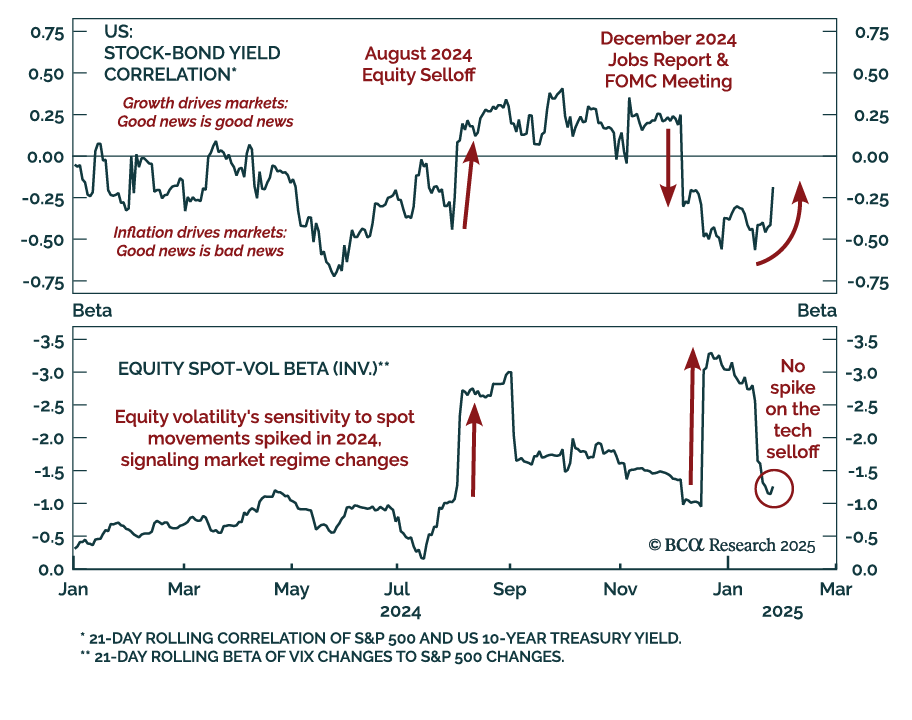

Monday’s selloff was orderly and concentrated in the tech sector. The price action was a classic risk-off response, where both stock prices and bond yields decreased. While the VIX increased, the equity spot-vol beta, volatility’s sensitivity to spot price…