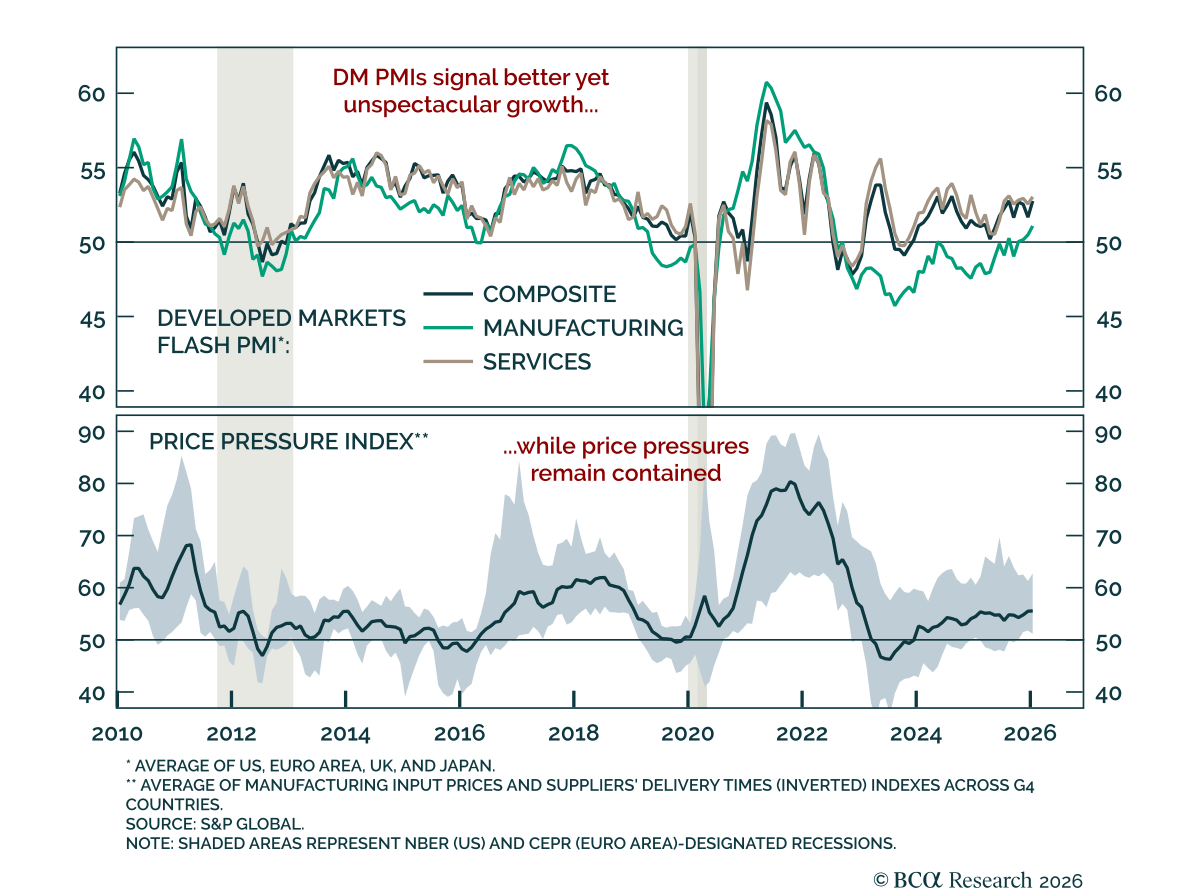

Developed Countries

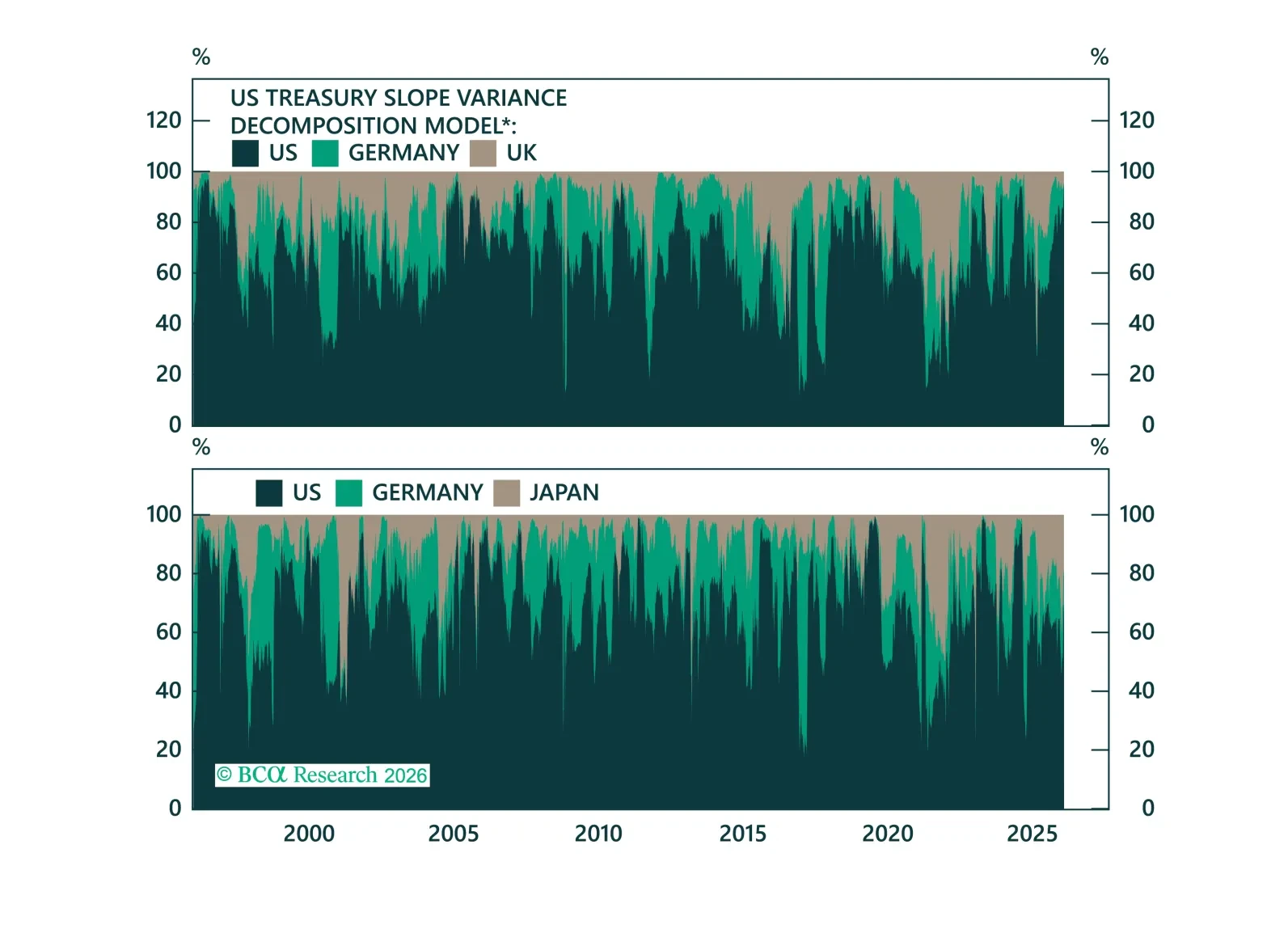

What’s driving government bond yields, and how do different bond markets impact each other? In today's Strategy Insight, we decompose yield moves into global drivers and idiosyncratic local drivers.

Our Portfolio Allocation Summary for February 2026.

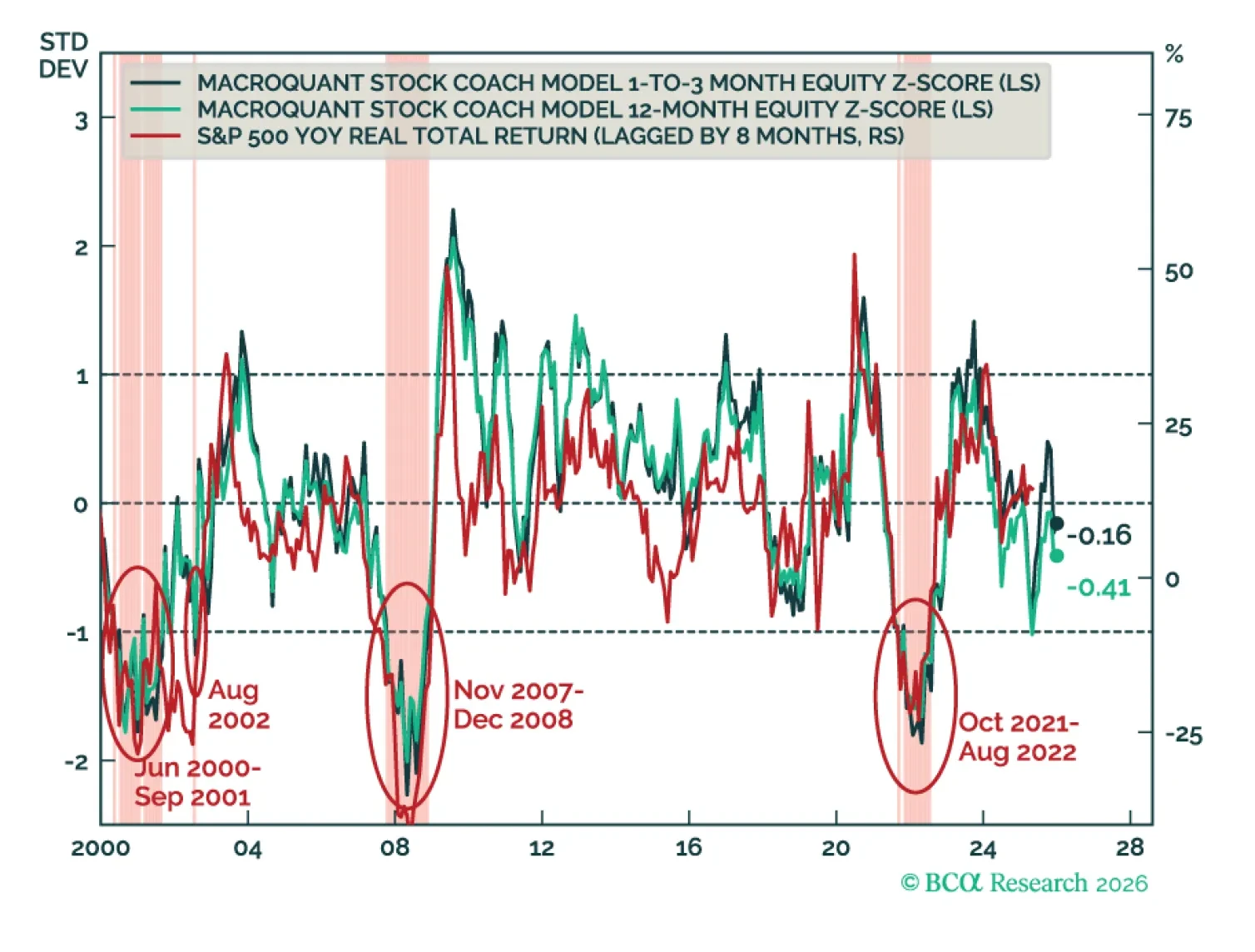

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

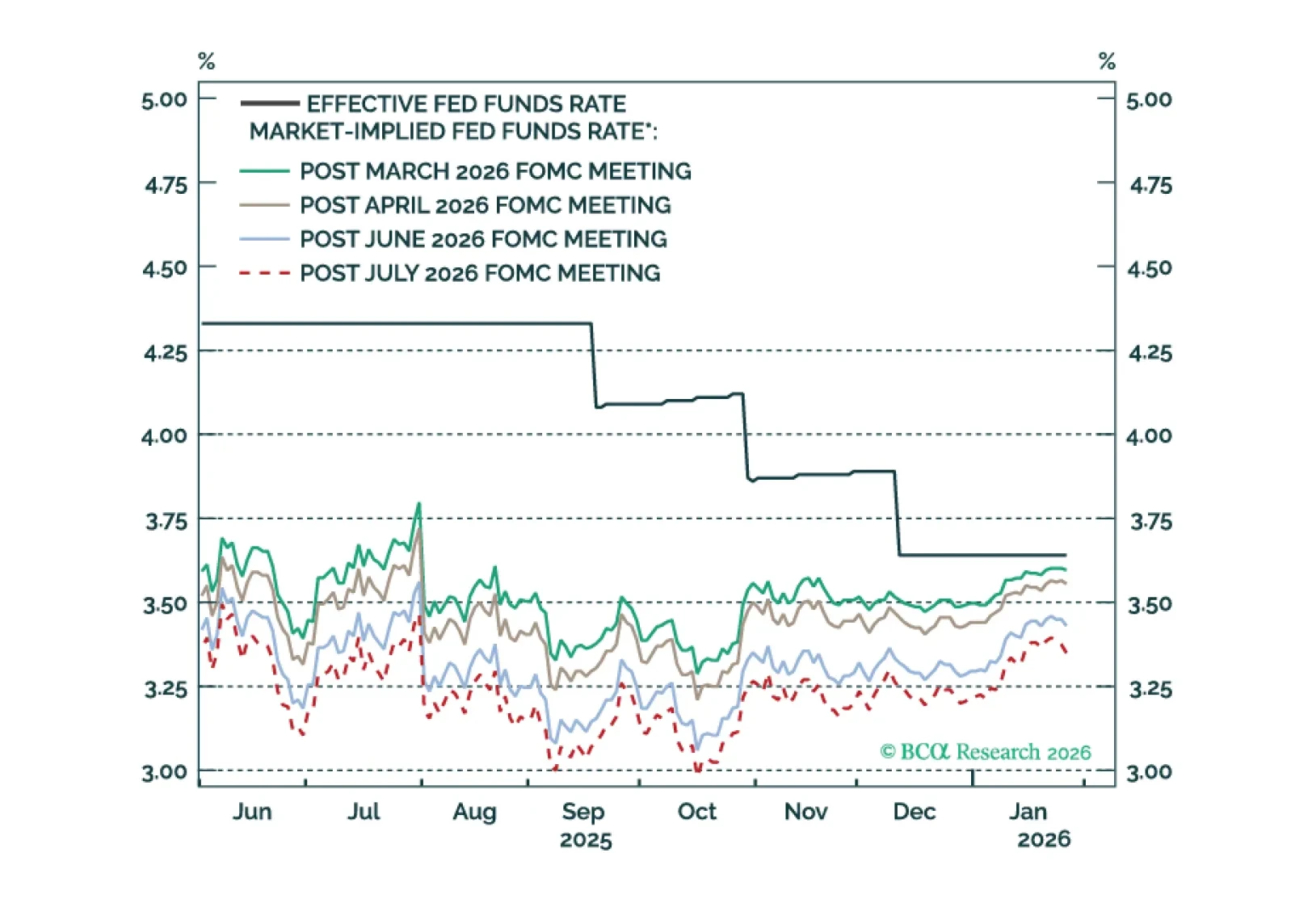

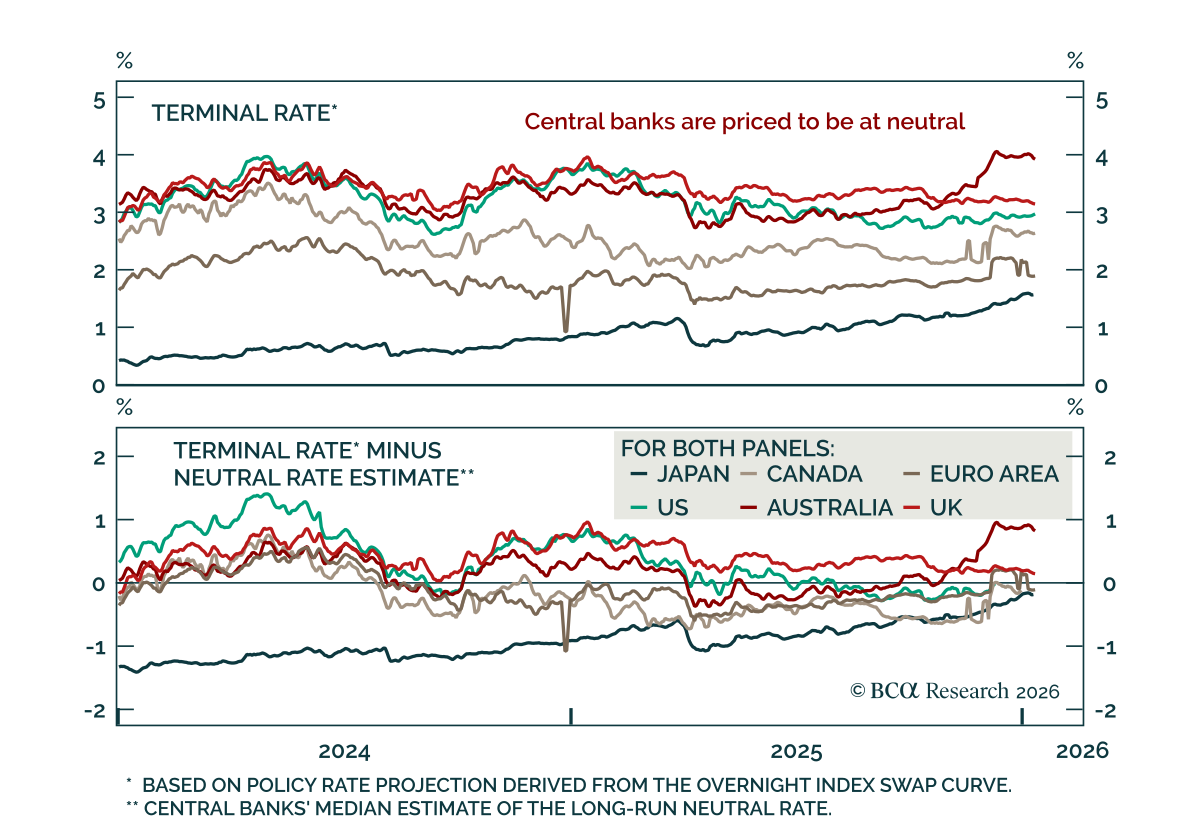

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

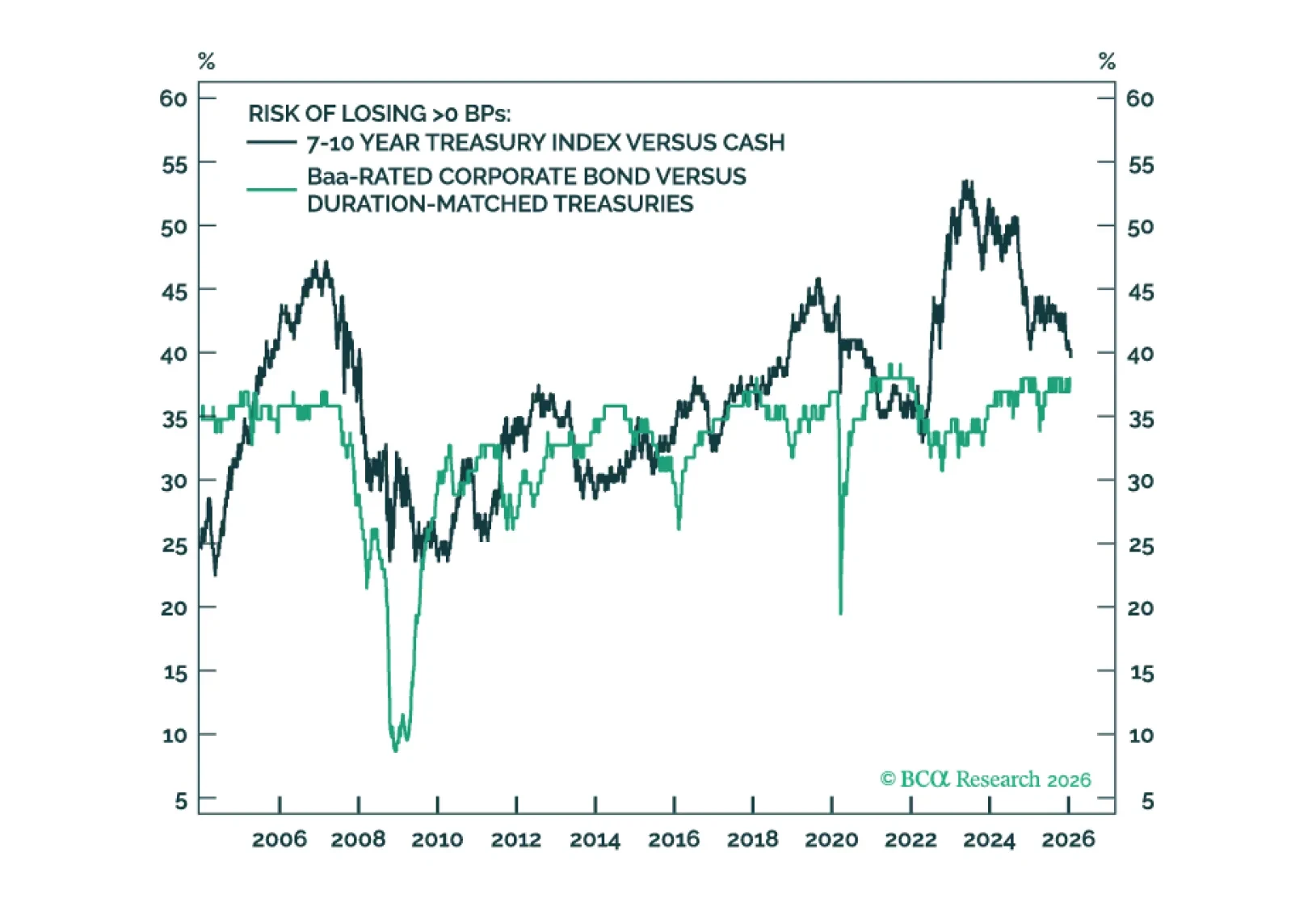

The 10-year Treasury term premium is now competitive with Baa- and Ba-rated credit spreads. Even without term premium compression, duration carry trades could outperform credit carry trades in a low rate vol environment.

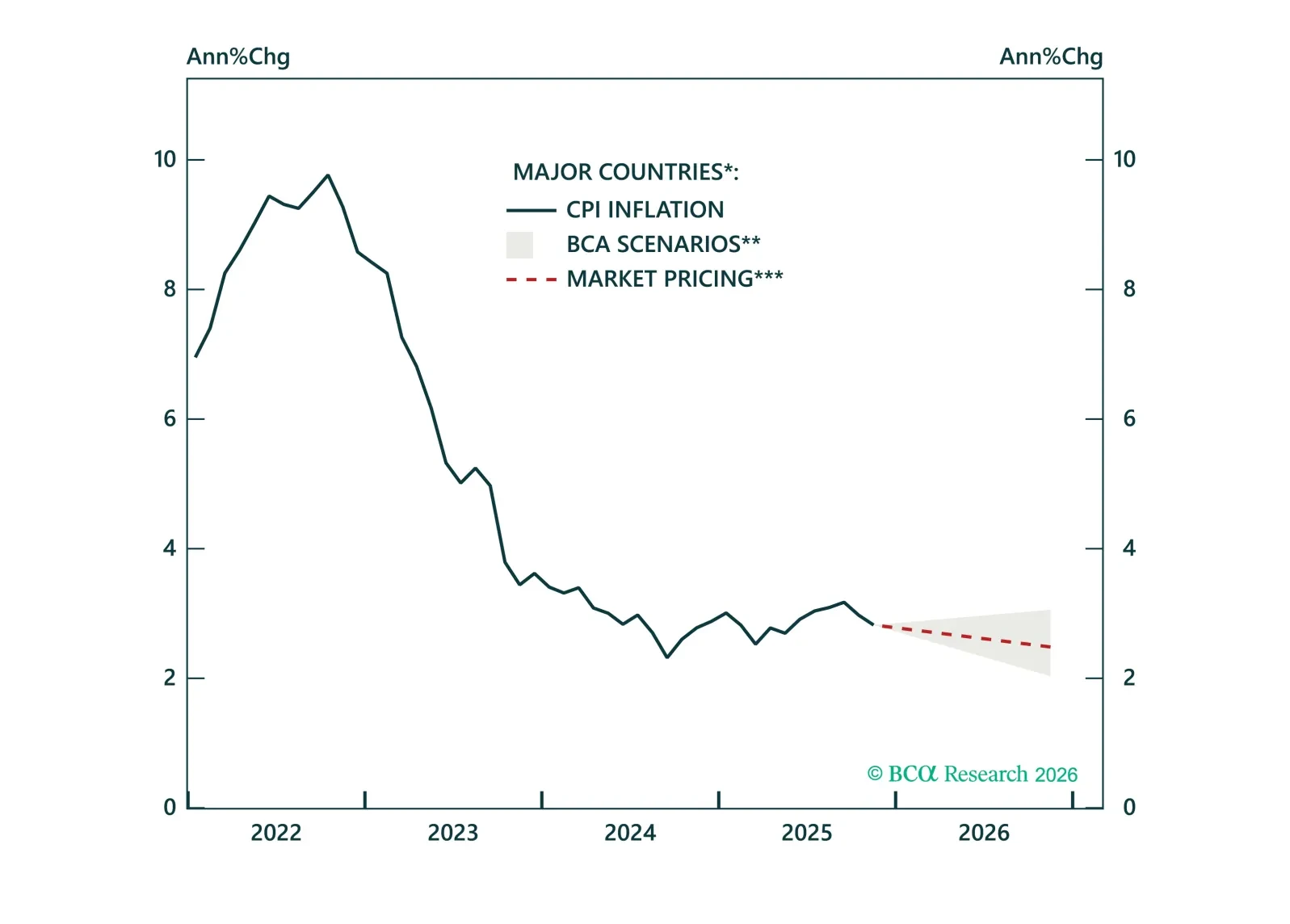

In our 2026 inflation outlook, we explain why 2026 will bring more disinflation, upside risks remain contained, and how to position in ILBs across major markets.

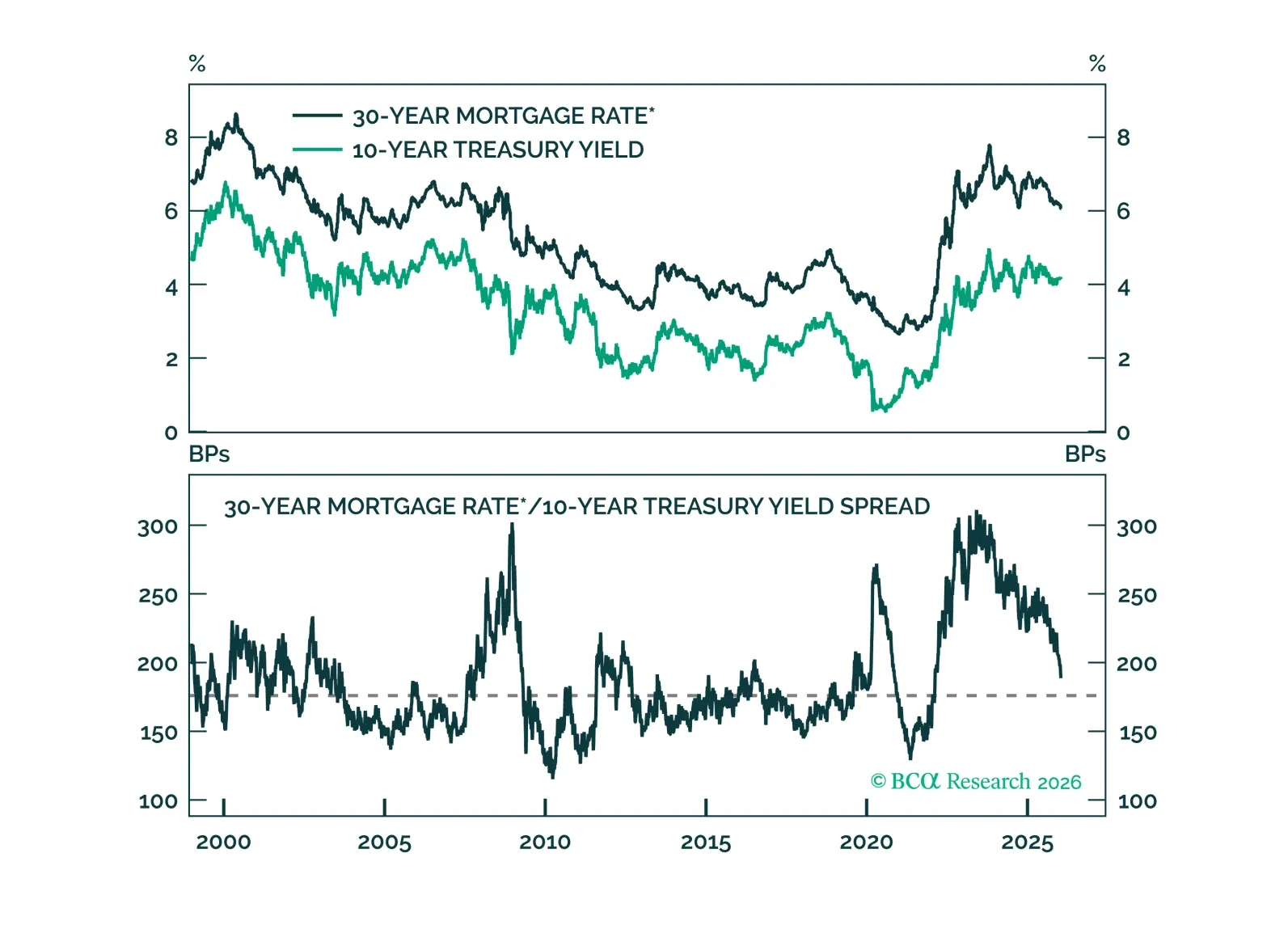

Mortgage spread tightening has run its course. Any further drop in mortgage rates will necessitate lower Treasury yields.

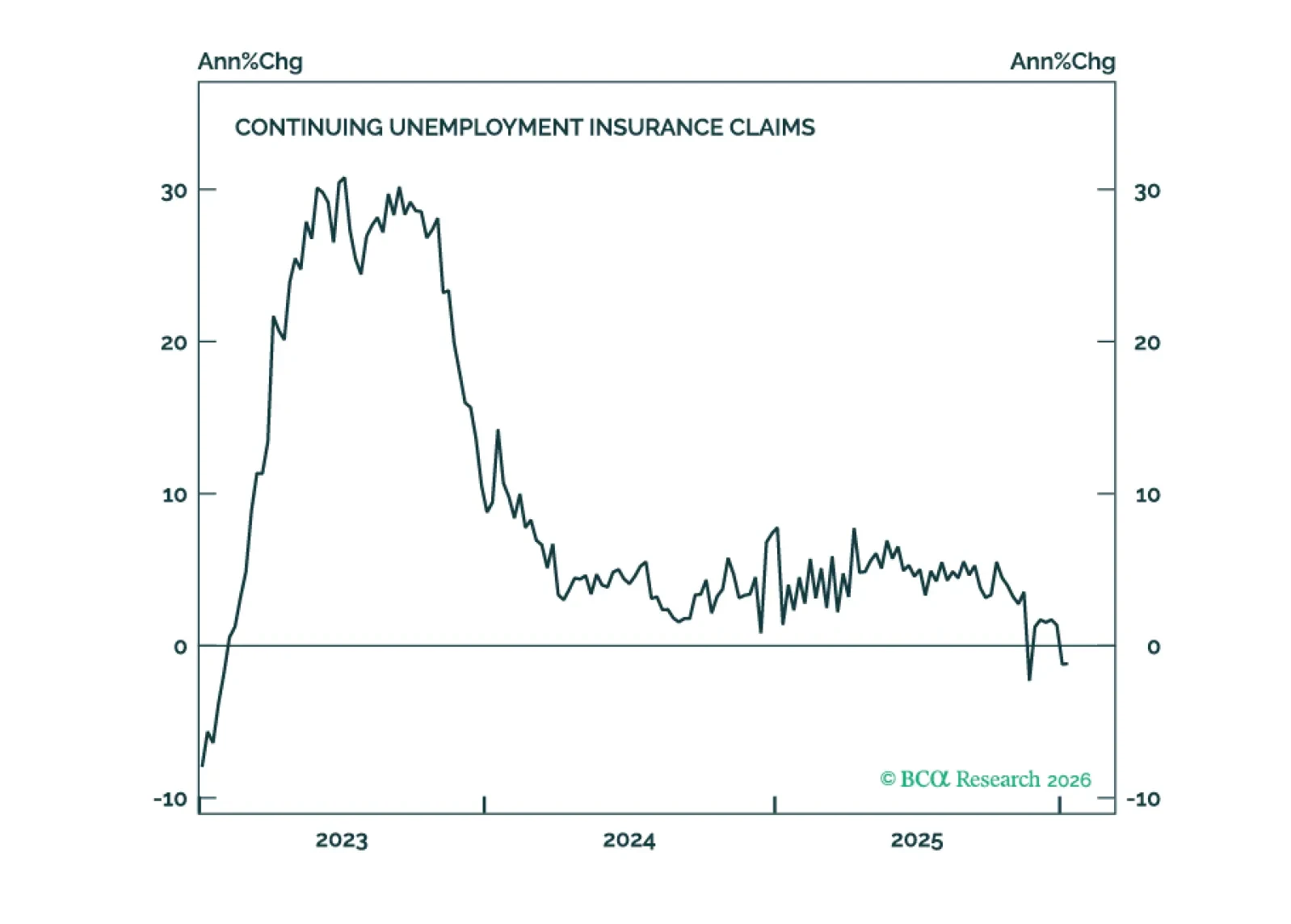

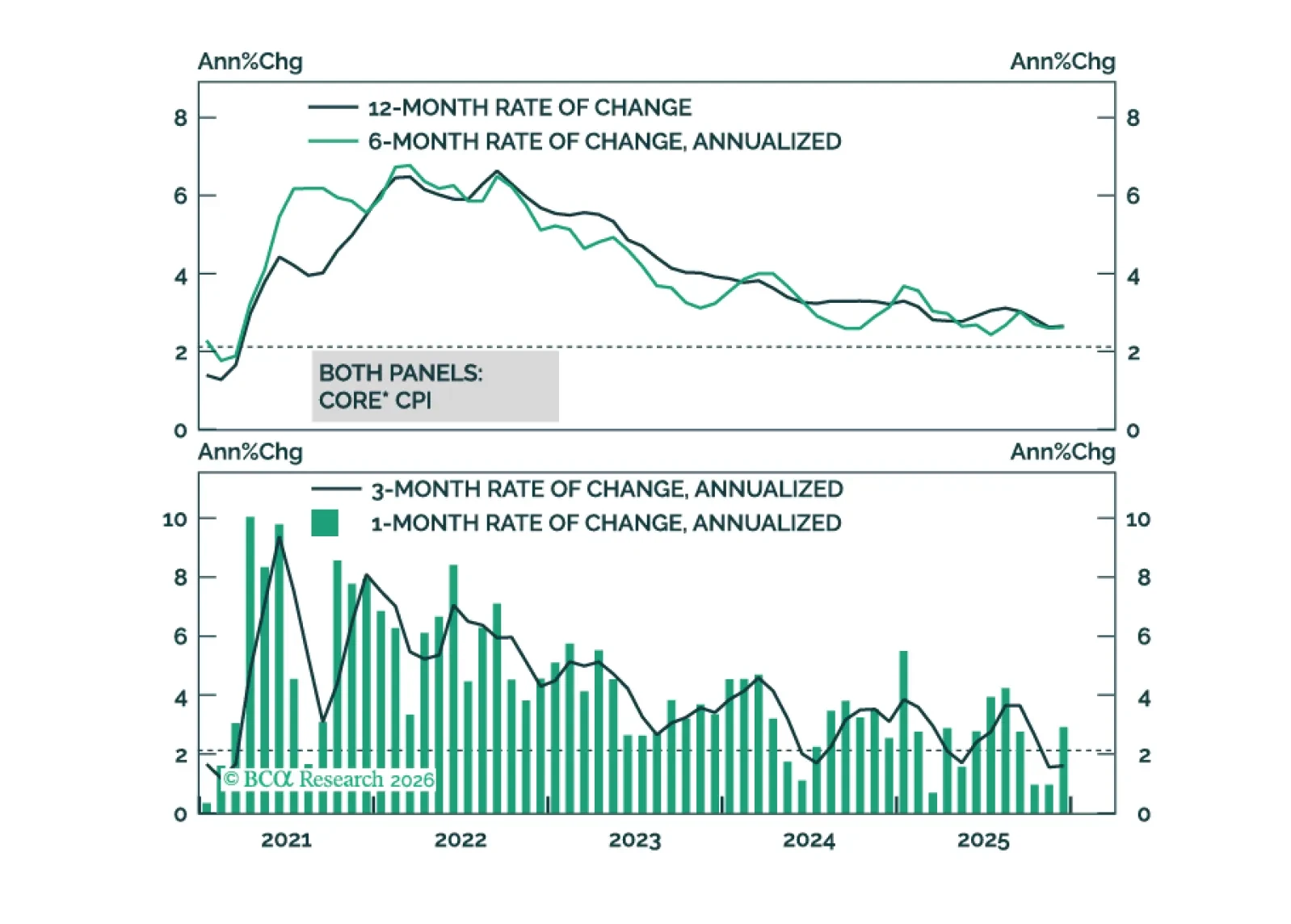

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.