Developed Countries

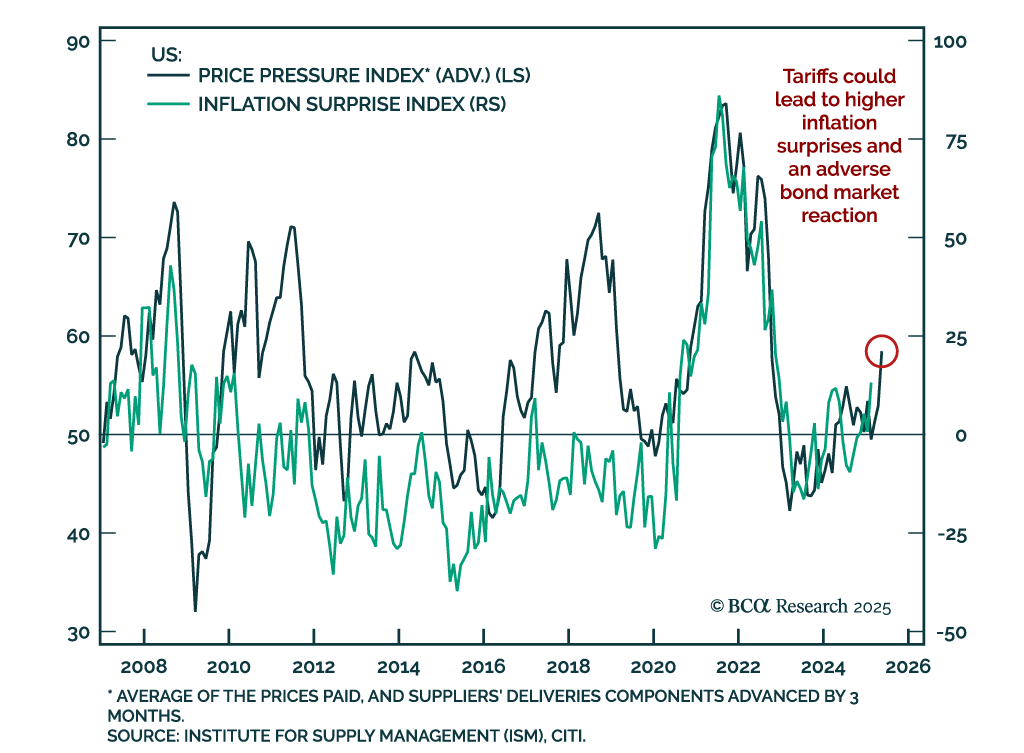

Leading US growth indicators have slowed, with economic surprises now in negative territory. However, Monday’s ISM Manufacturing showed that while activity is slowing due to tariffs uncertainty, supply-side price pressures are increasing. Our Price…

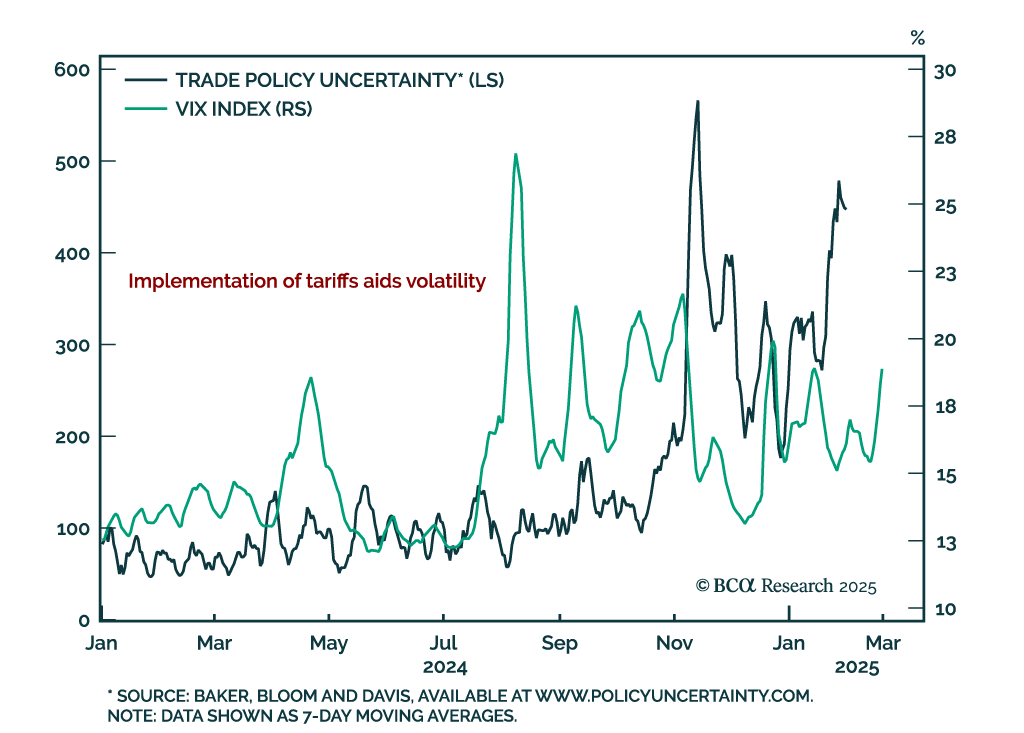

Our Geopolitical strategists received a lot of client questions following rapid US political developments, and addressed them in their latest report. US policy uncertainty is spiking, driving global uncertainty higher. Tariff implementation in March and…

February flash inflation for the Eurozone was slightly hotter than expected but nonetheless declined, with both headline and core inflation falling 0.1% to 2.4% y/y and 2.6%, respectively. Services inflation also declined to 3.7% from 3.9%. While Europe…

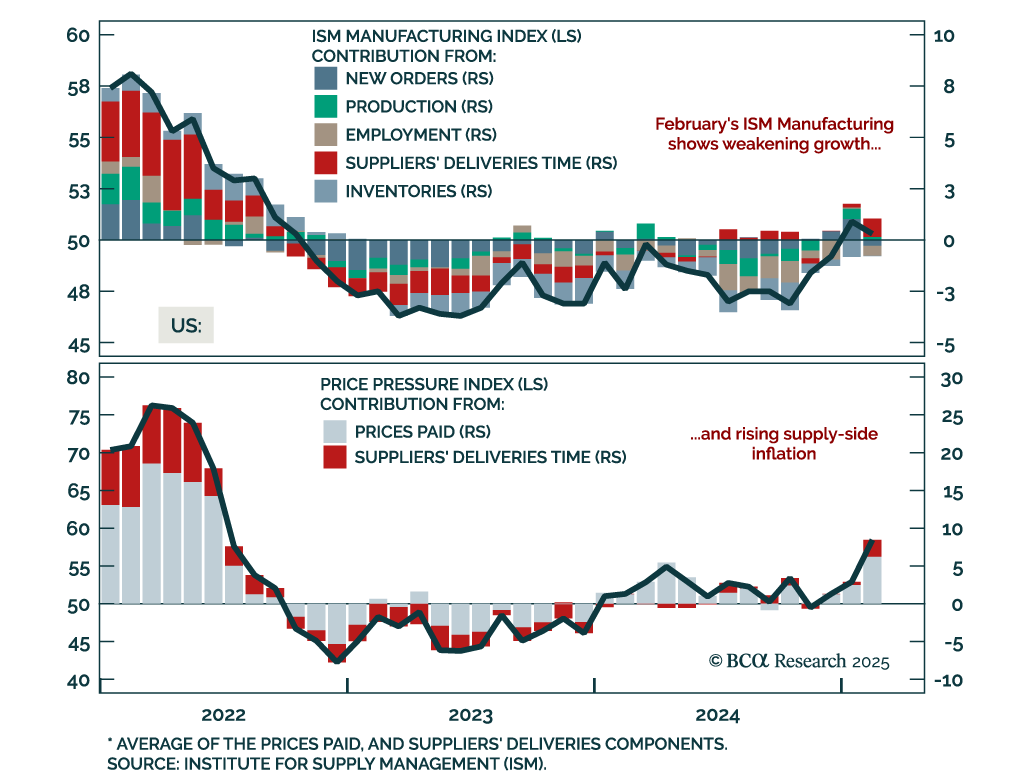

The February ISM Manufacturing index was weaker than expected, declining to 50.3 from 50.9. New orders plunged to 48.6 from 55.1, with employment also contracting. Price pressures however increased. Prices paid and suppliers’ delivery times jumped to their…

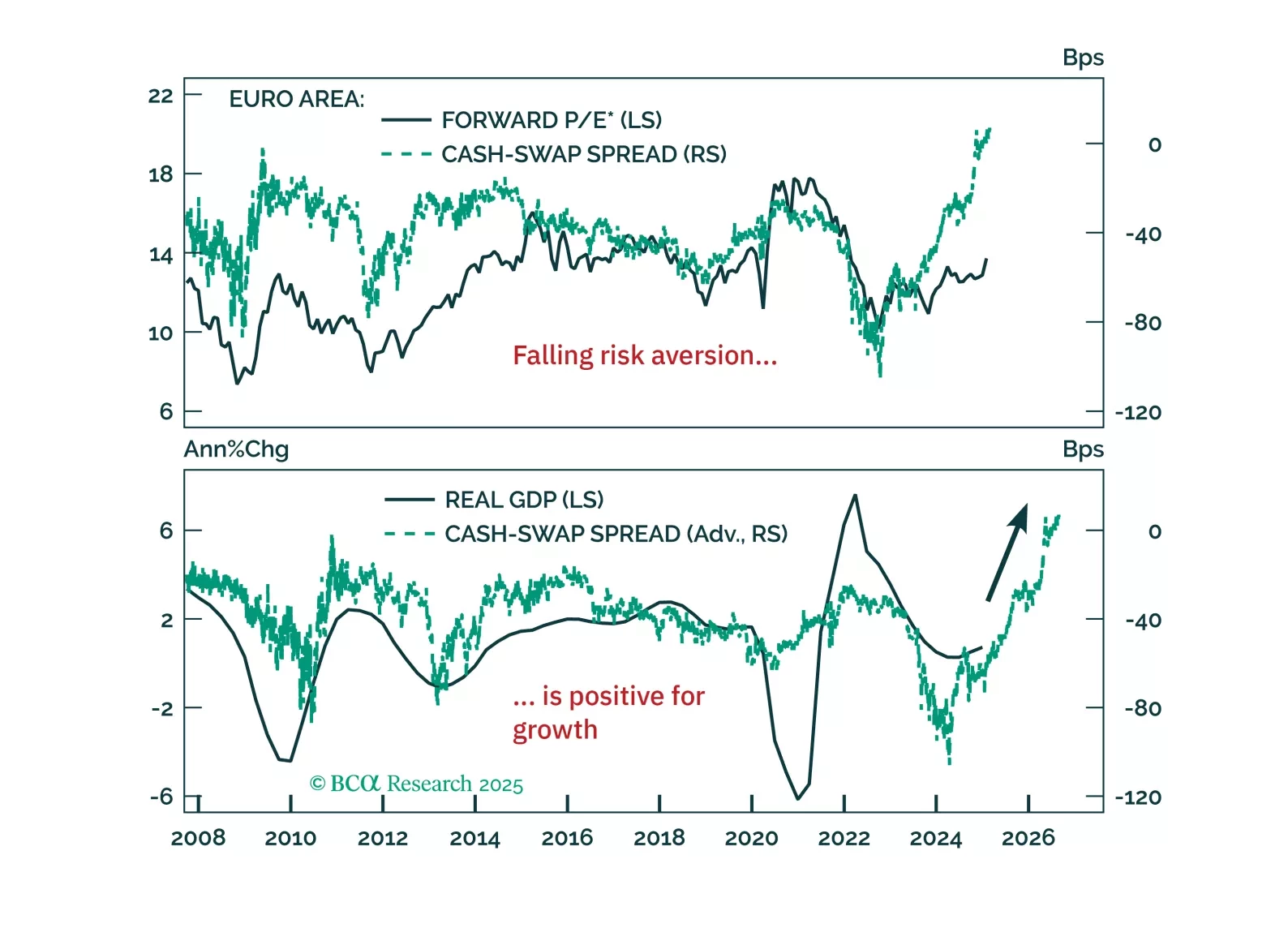

Europe’s resilience to global liquidity deterioration isn’t a fluke—it signals a structural shift. Our latest report explains why the decline in precautionary money demand marks the end of Europe’s liquidity trap and what it means for investors.

Our Bank Credit Analyst strategists published their latest monthly report, and Section II aims to assess whether AI is leading to a productivity increase. Our colleagues remain unconvinced that Generative AI is a true productivity revolution, though it…

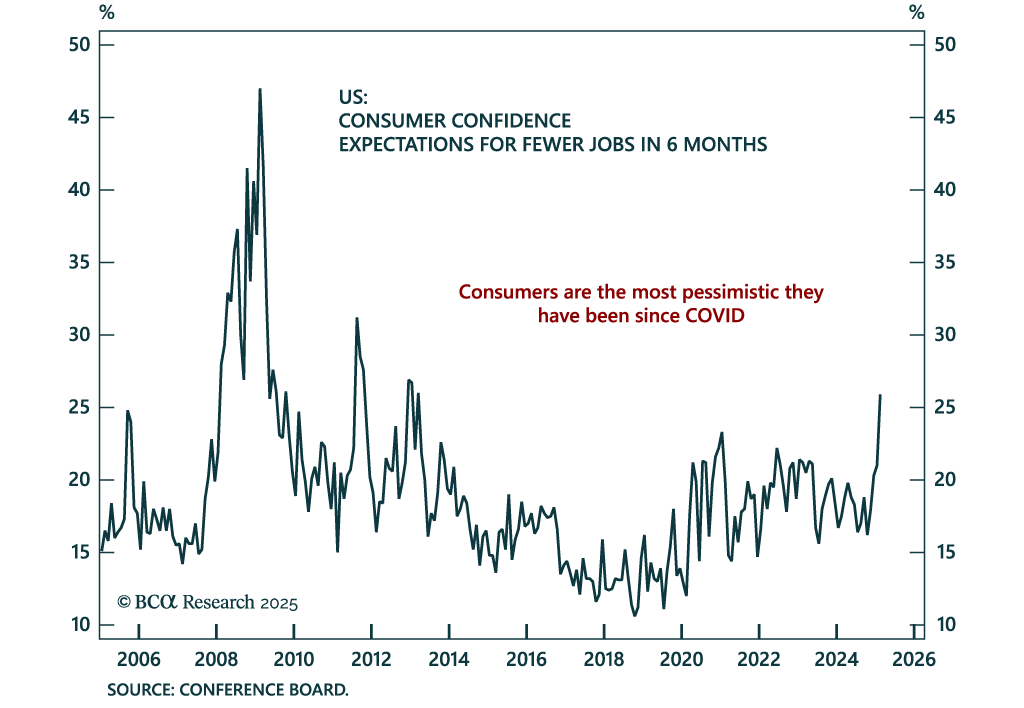

Our Chart Of The Week comes from Juan Correa, from our Global Asset Allocation (GAA) strategy service. Juan highlights weakening US growth observed in the data lately. We have seen a few growth slowdown episodes since 2022. Why is this time…

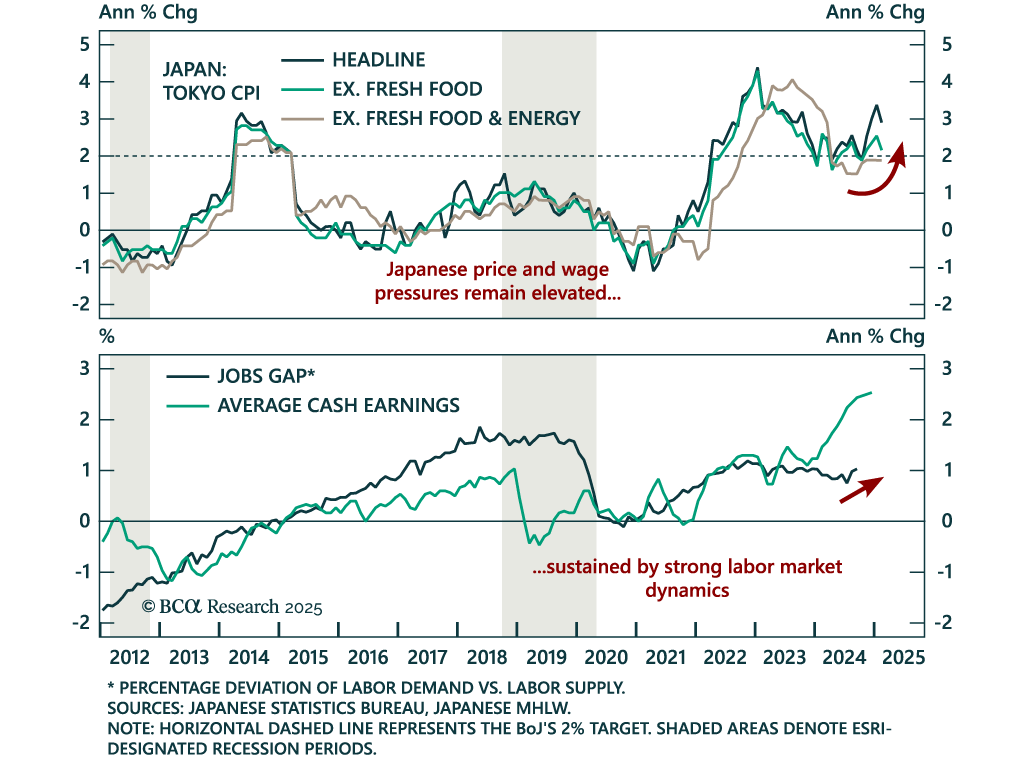

The February Tokyo CPI print came in slightly cooler than expected. Headline inflation moderated to 2.9% y/y from 3.4%, while “core core” was steady at 1.9%. The Tokyo CPI gives an advance reading on national price pressures, and the data suggests…

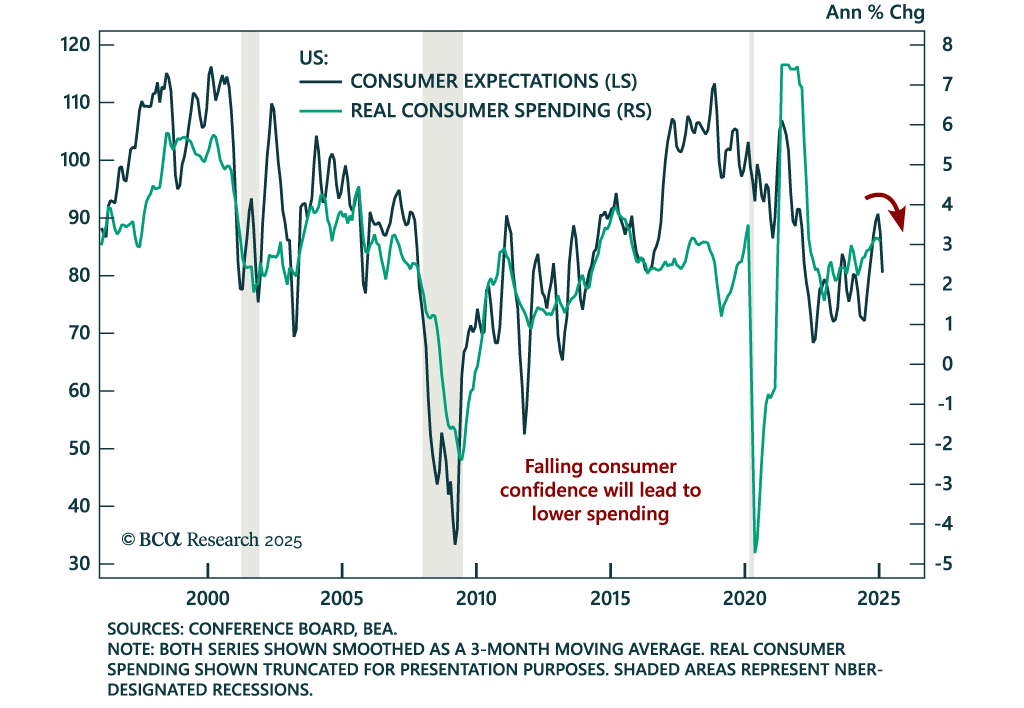

January PCE inflation was in line with expectations, with headline and core inflation rising 0.3% m/m, leaving the respective annual growth rates at 2.5% and 2.6%, near the Fed’s projection for 2025. Consumer spending missed expectations and was weak in both…

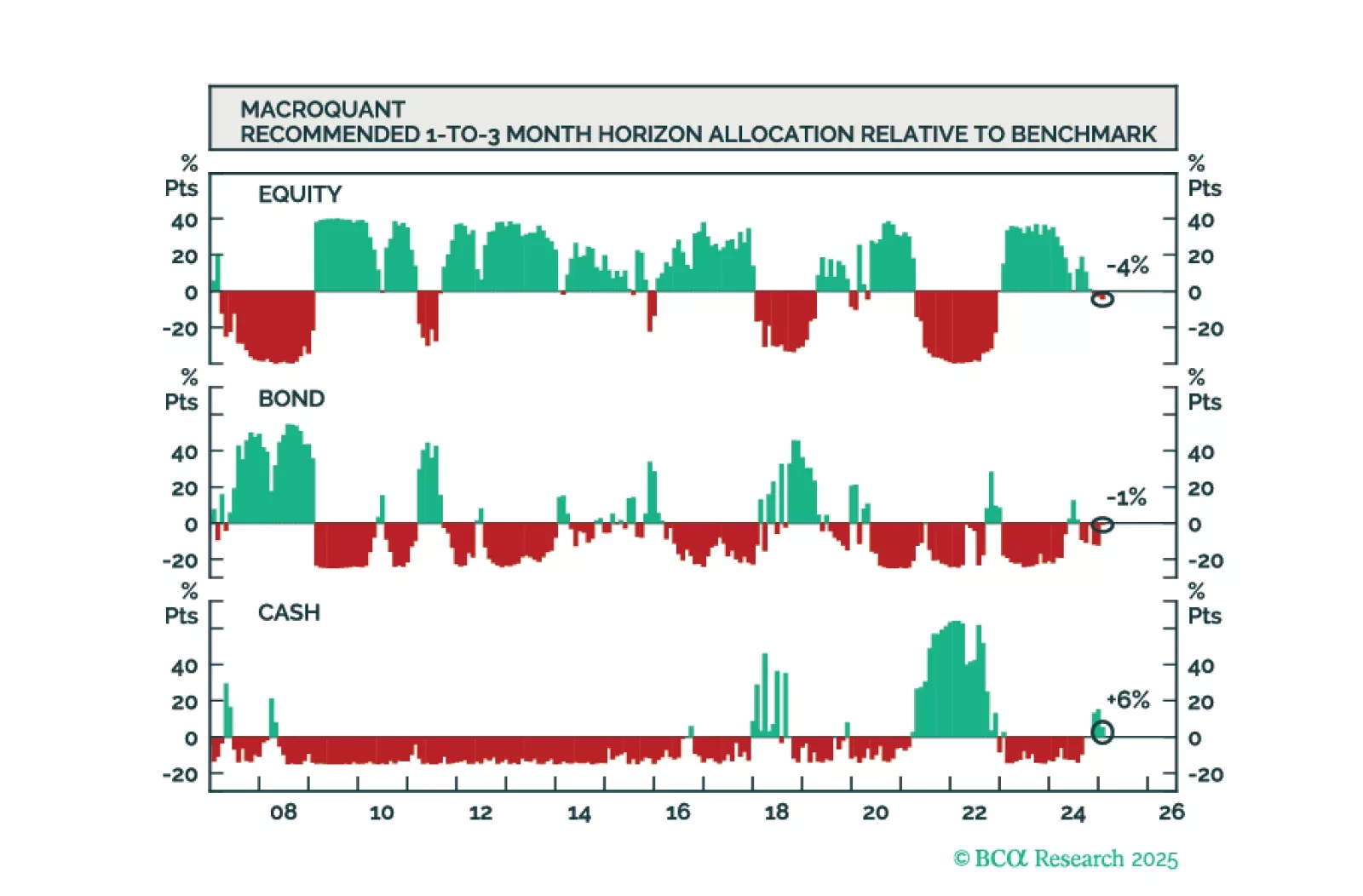

The MacroQuant model is no longer bullish on stocks but is not yet prepared to turn underweight. Subjectively, the Global Investment Strategy team is more bearish on equities than the model.