Developed Countries

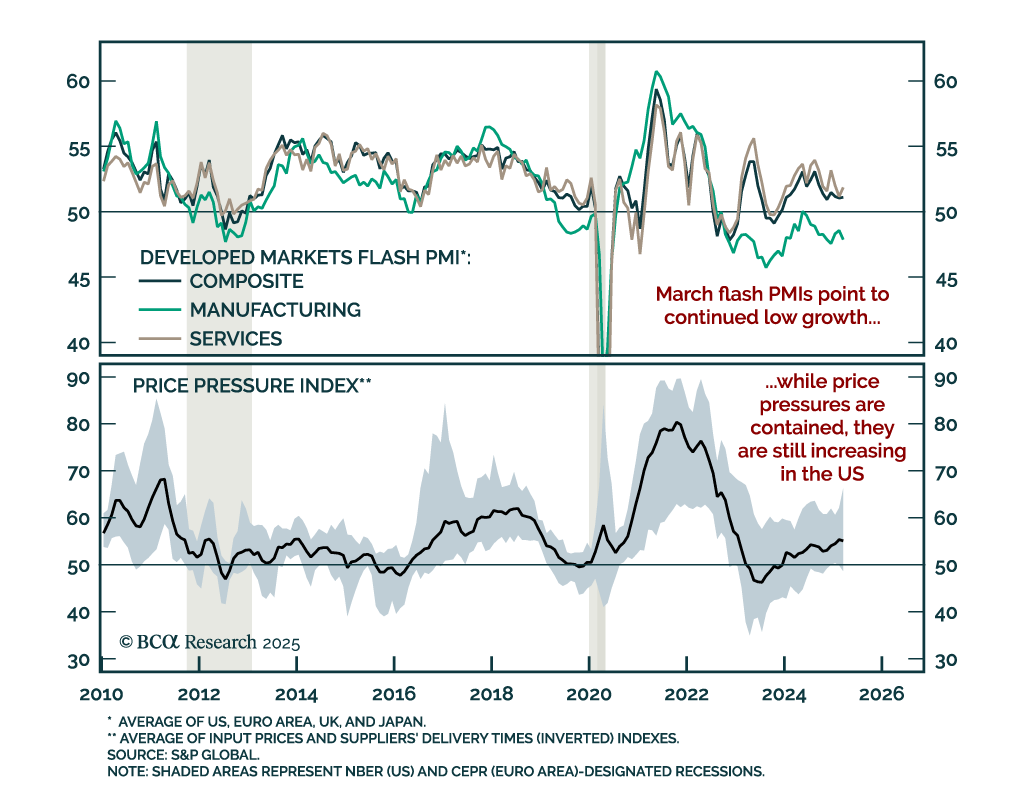

The March PMIs point to a low growth buffer outside the US as uncertainty engulfs the global economy. Aggregate price pressures were contained in March, but input prices still increased in the US. While the market reaction was risk-on, with the S&P 500…

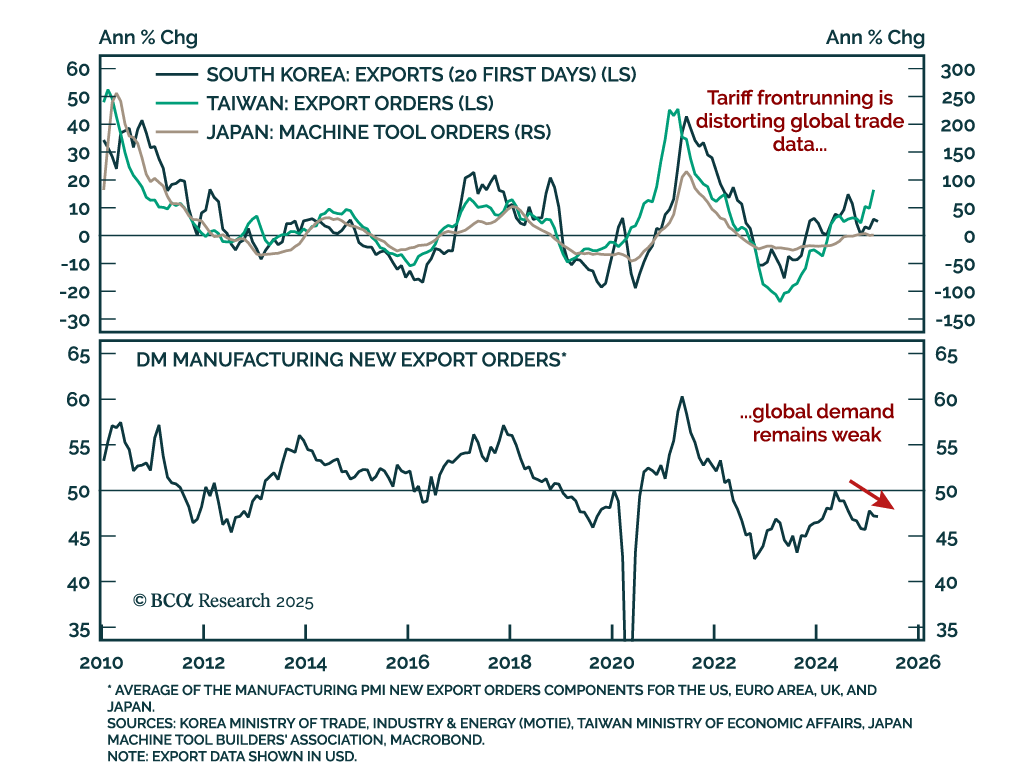

East Asian trade data has been disappointing. Preliminary February data for Japanese machine tool orders showed a slowdown to 3.5% y/y from 4.7% in January. Broader machinery orders were down 3.5% m/m in January. Taiwanese exports orders were up an abnormal…

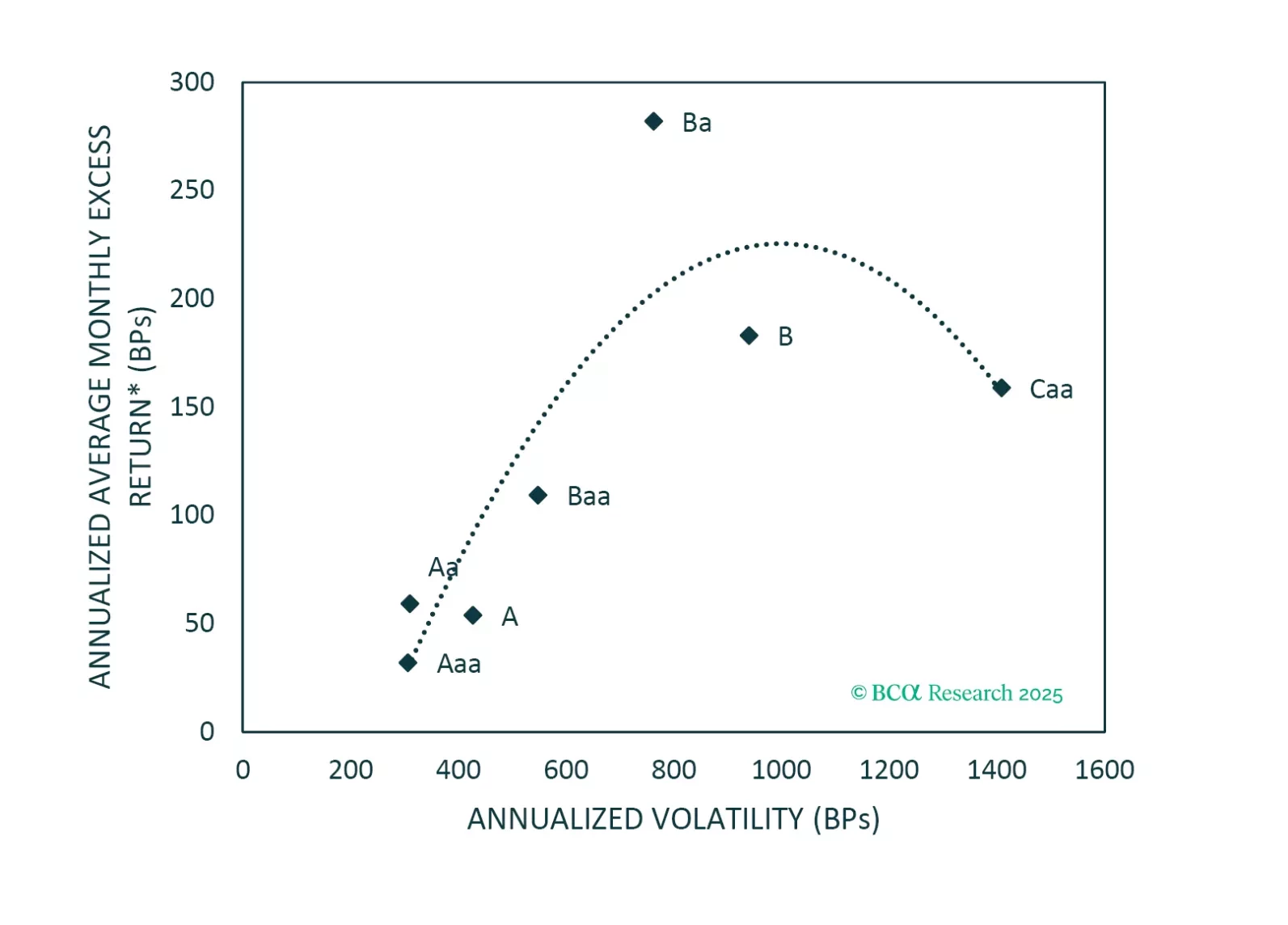

An analysis of historical data shows that Ba-rated bonds outperform other corporate credit tiers in the long-run on a risk-adjusted basis. That said, today’s fragile macro environment warrants a more cautious allocation.

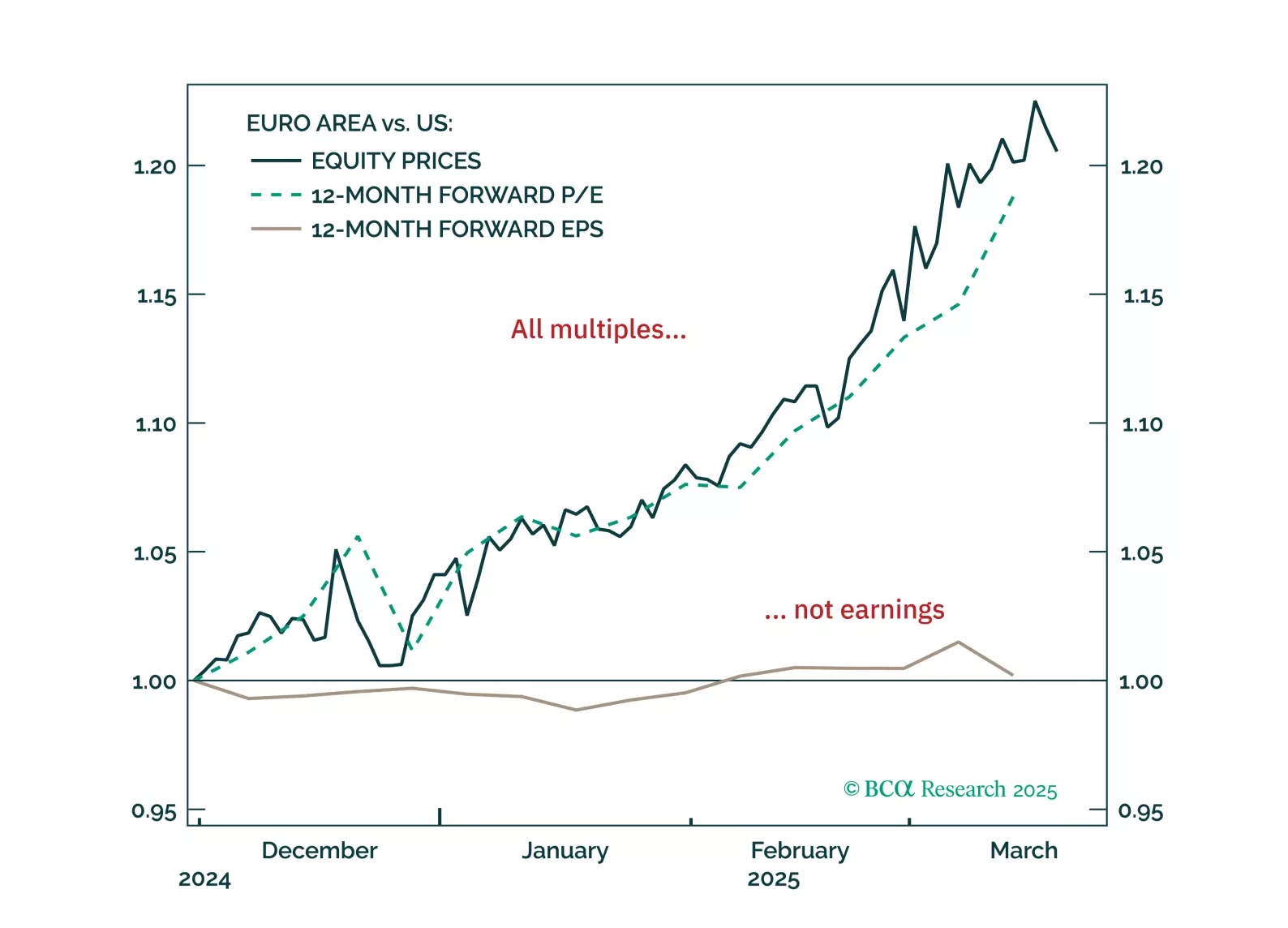

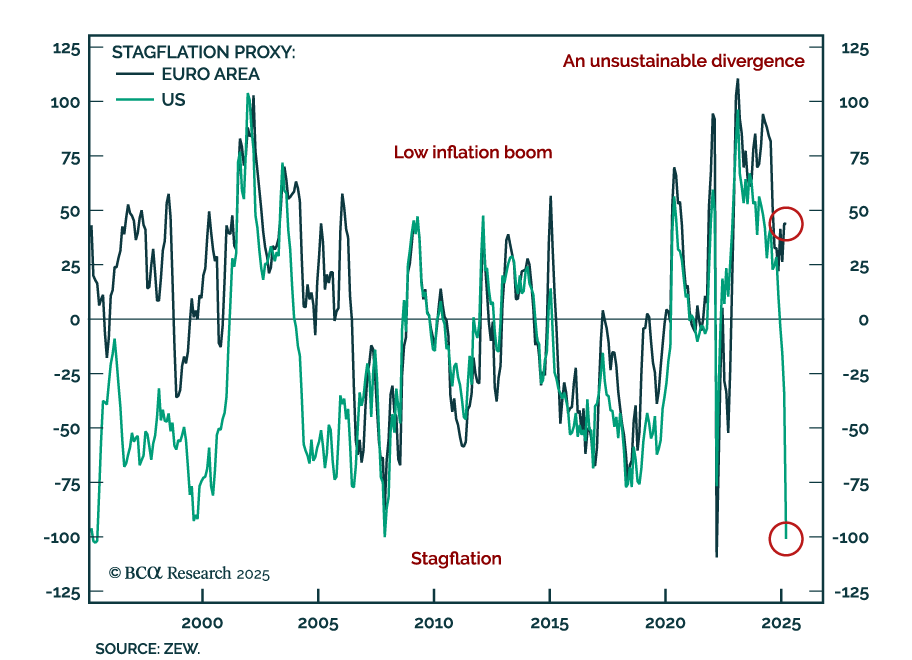

European equities have surged on hopes of a low-inflation boom—but the rally has likely gone too far, too fast. With a pullback now likely, how should investors position themselves over the next 3–6 months?

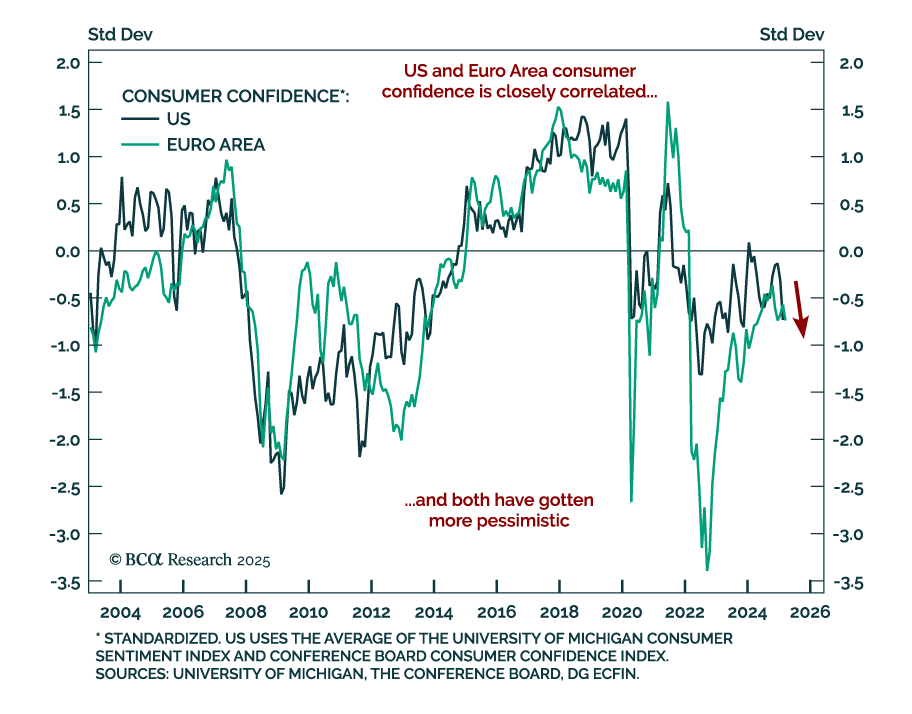

The March flash estimate for European Consumer Confidence missed estimates, and fell to -14.5 from -13.6 in February. This negative reading is the first European sentiment number missing expectations since January. The sentiment shift between the US and…

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu believes the recent outperformance of European over US risk assets is unlikely to last over the next 3-6 months. Markets are…

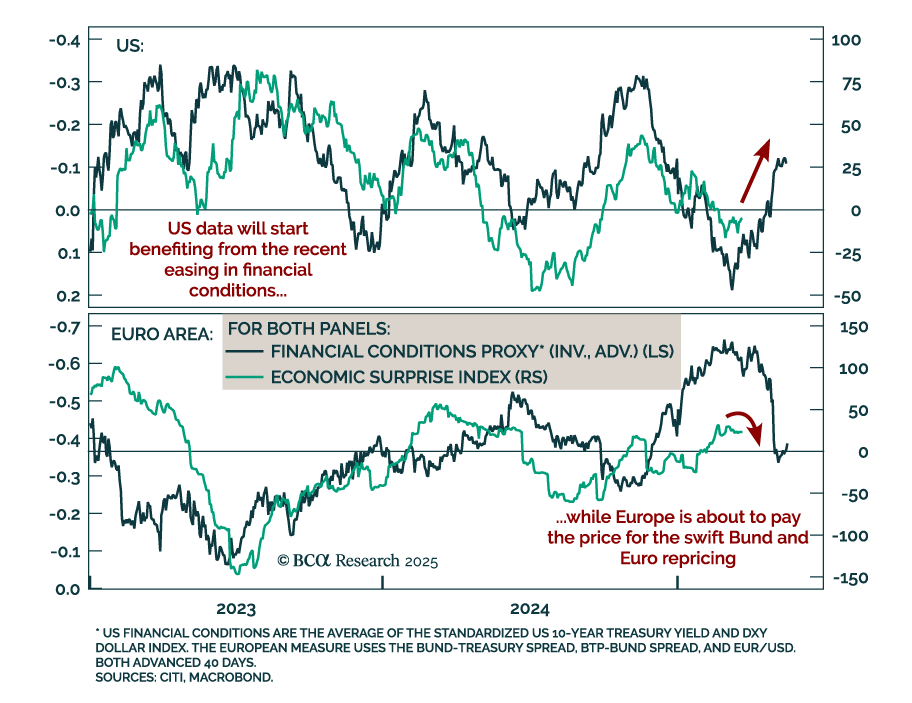

Our tactical framework highlights how financial conditions and economic surprises interact, where growth often sows the seeds of its own demise. Markets price expectations efficiently but lack perfect foresight, making data surprises key to price action.…

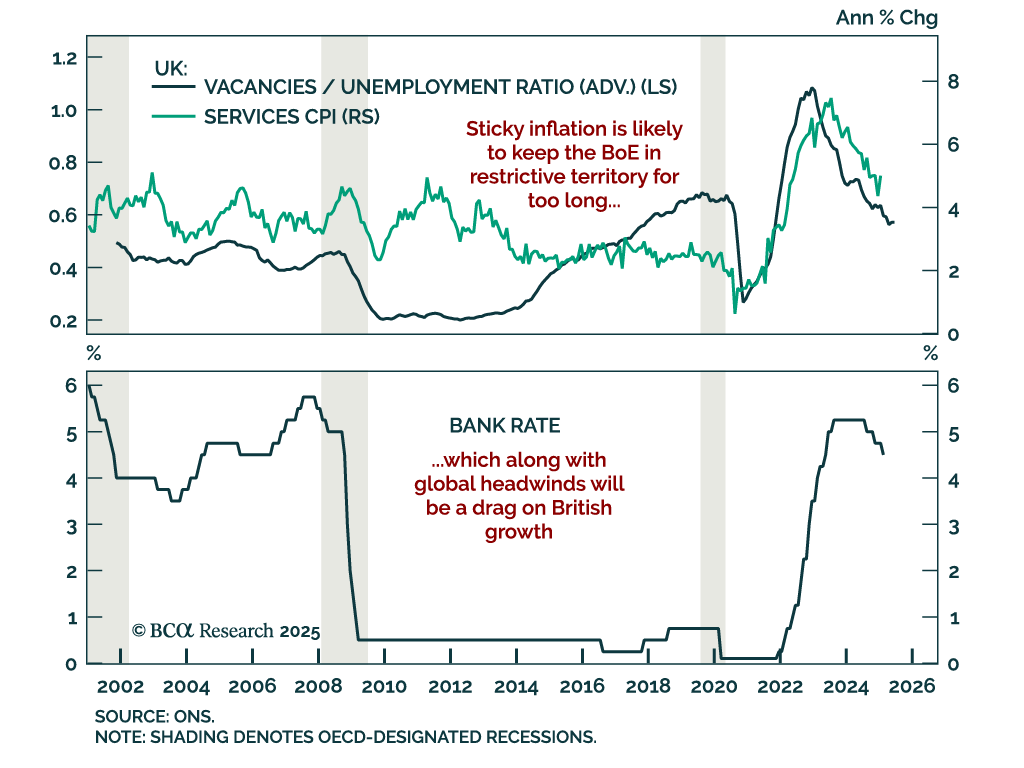

The Bank of England held its policy rate at 4.5%, with only one MPC member dissenting to cut 25 bps. The BoE signaled a slower pace of easing, as inflation remains elevated while global growth becomes increasingly uncertain. Like other DM central banks,…

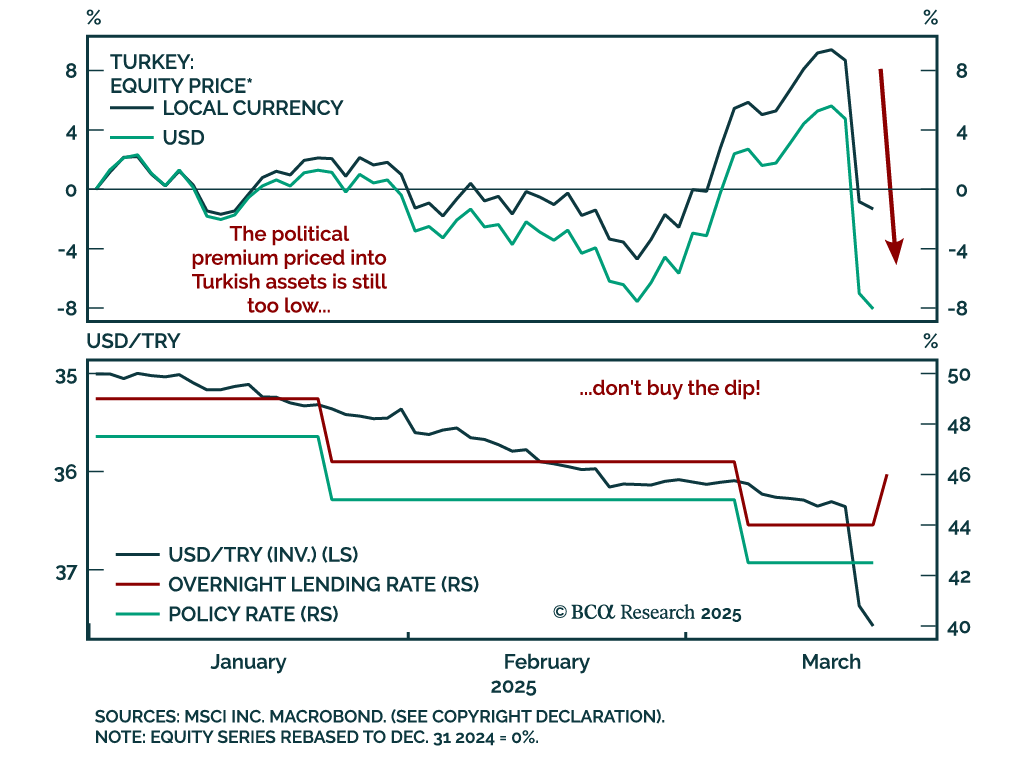

After a period of relative stability and progress towards policy orthodoxy, politics are again haunting Turkish assets. President Erdogan jailed Istanbul mayor Ekrem Imamoglu, a political rival from the opposition party gaining ground at the municipal level.…

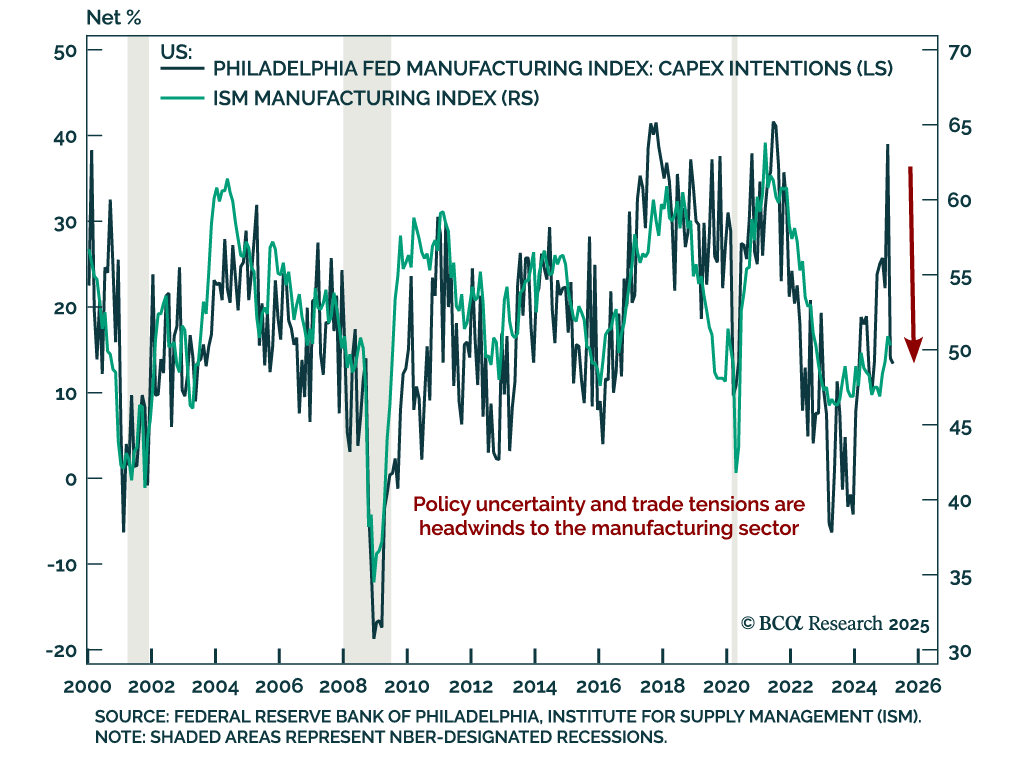

The March Philadelphia Fed Manufacturing index beat expectations, but still fell from 18.1 to 12.5, significantly down from January’s lofty 44.3 reading. Most activity components slowed except for current employment and work hours. Price pressure indicators…