Developed Countries

Our GeoMacro strategists recommend positioning for an exodus out of US assets, with long exposure to gold, the yen, and the Canadian dollar. April 2, “Liberation Day,” is likely to mark the peak in de-globalization hysteria, as the trade war acts as a…

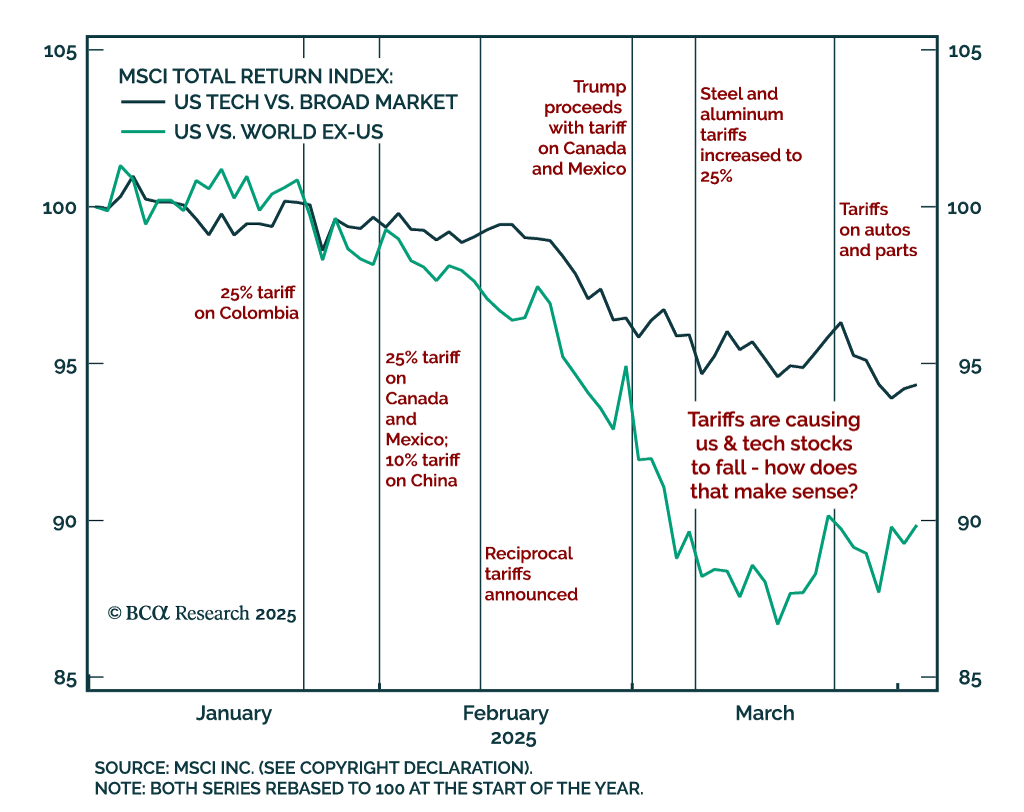

Markets had a risk-off reaction to the Trump administration’s announcement of reciprocal tariffs, reinforcing the case for defensive portfolio positioning. The proposal includes a 10% baseline tariff on all imports, a 25% tariff on foreign-made vehicles, and…

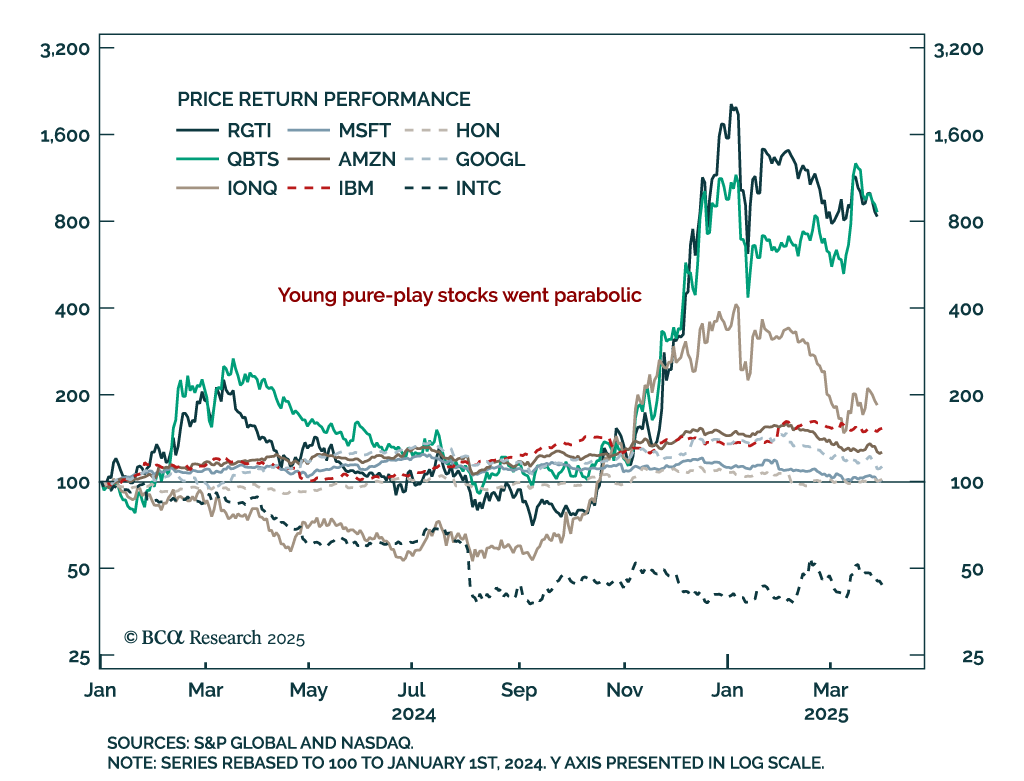

Our US Equity strategists recommend caution on quantum computing, as the industry is still too early-stage for reliable investment exposure. Although quantum computing (QC) is on the verge of major breakthroughs, pure-play QC stocks remain unprofitable and…

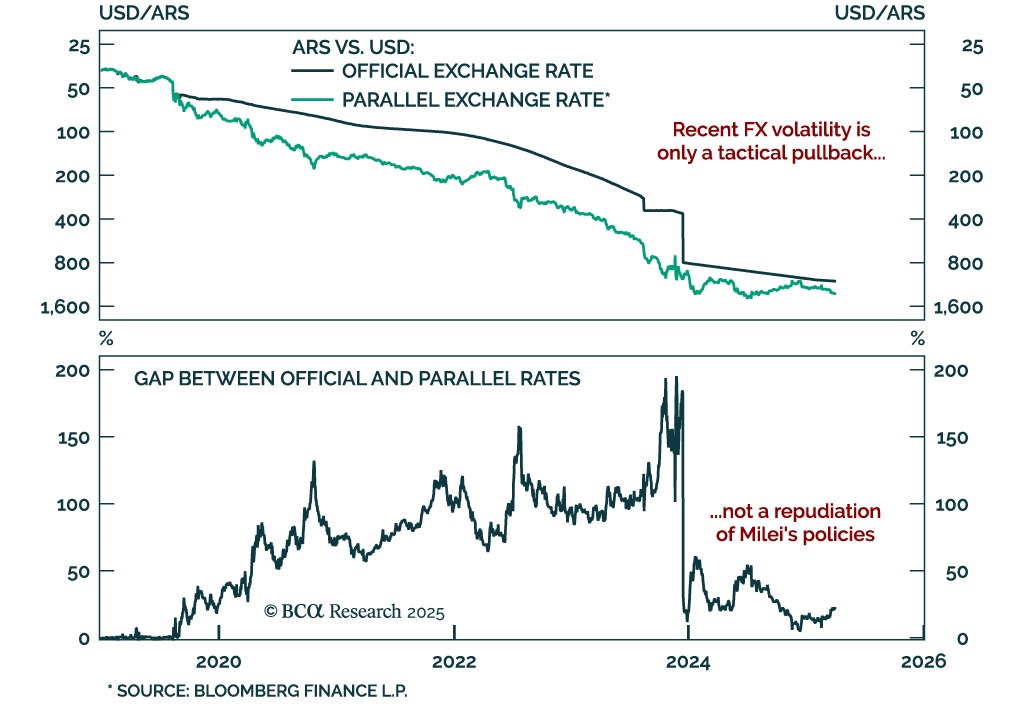

Remain constructive on Argentine assets as recent market moves are a tactical pullback, not a loss of confidence. The gap between official and parallel exchange rates has widened, prompting concerns that markets are questioning President Milei’s liberalizing…

Low correlations and regional dispersion are shaping market dynamics, creating selective opportunities outside the US even as near-term risks remain. Asset classes tend to become highly correlated during crisis episodes, limiting diversification when it is…

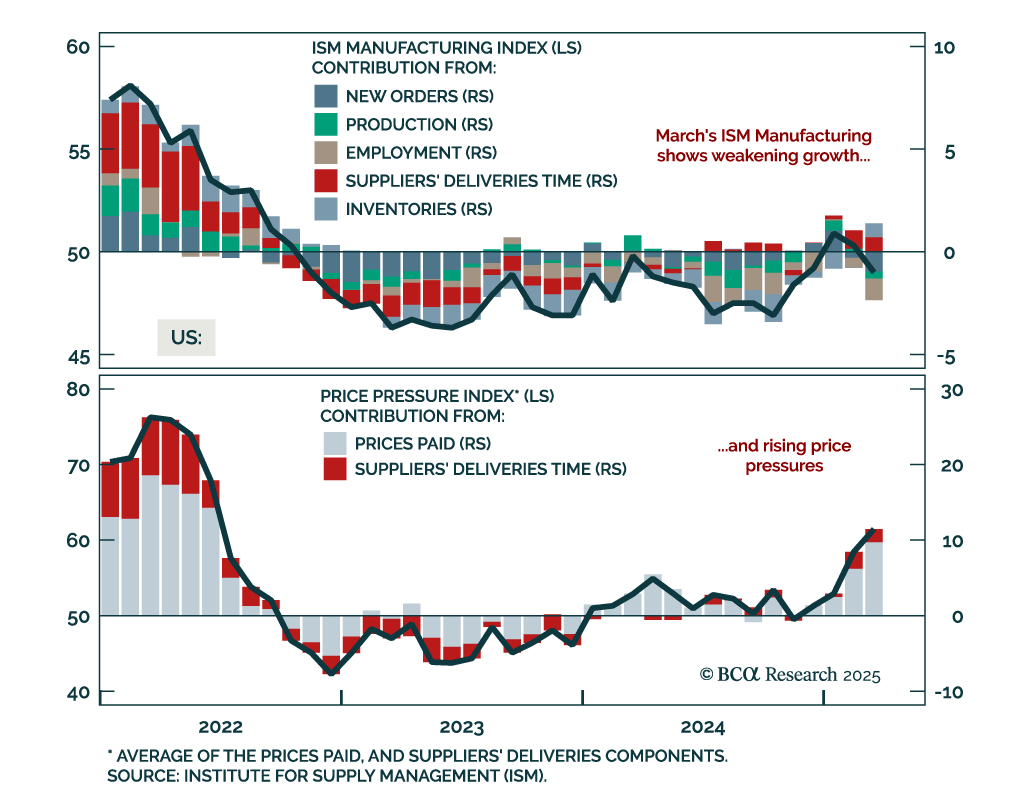

The March ISM Manufacturing adds to the recent stagflationary impulse, but markets remain focused on the growth drag, reinforcing our defensive asset allocation. The headline index fell more than expected to 49.0 from 50.3, with new orders and employment…

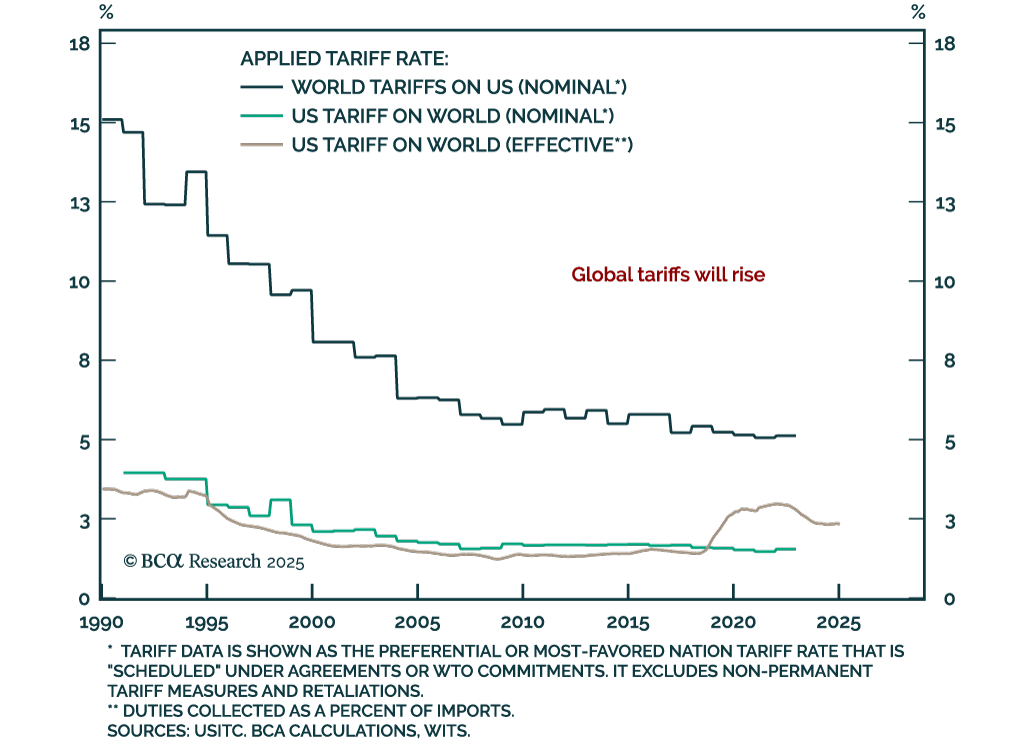

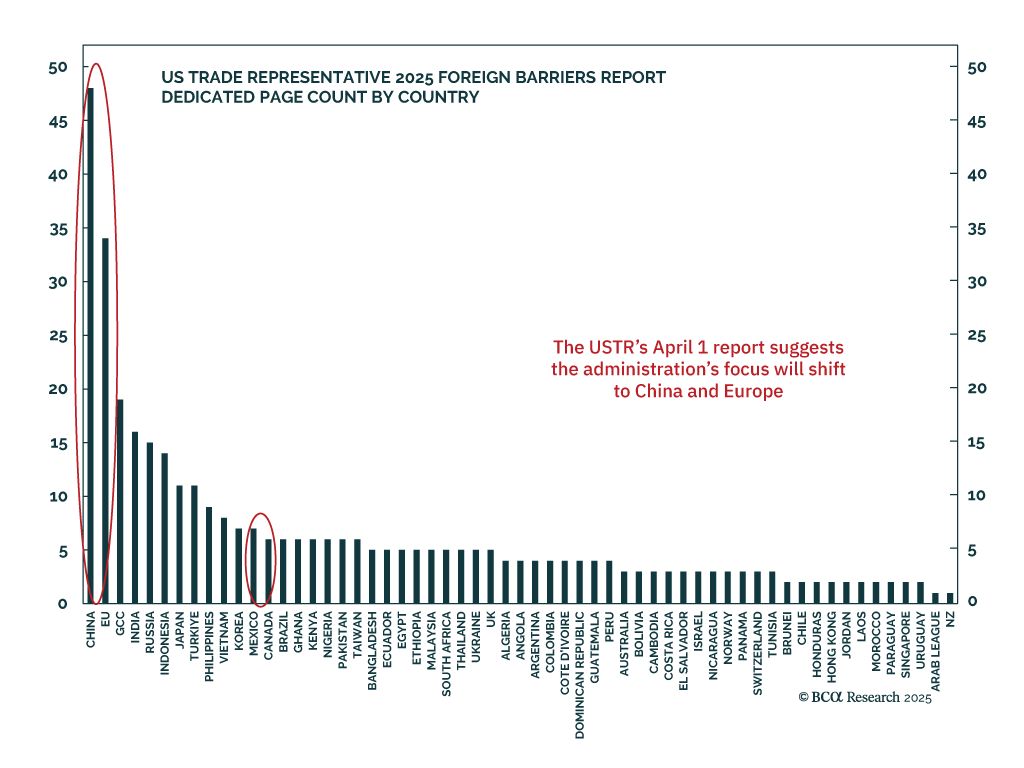

April 2 may mark peak trade tensions, but the path forward remains highly uncertain, supporting our underweight on risk assets and industrial commodities. The USTR’s long-awaited report on trade barriers will guide the next phase of US trade policy. While the…

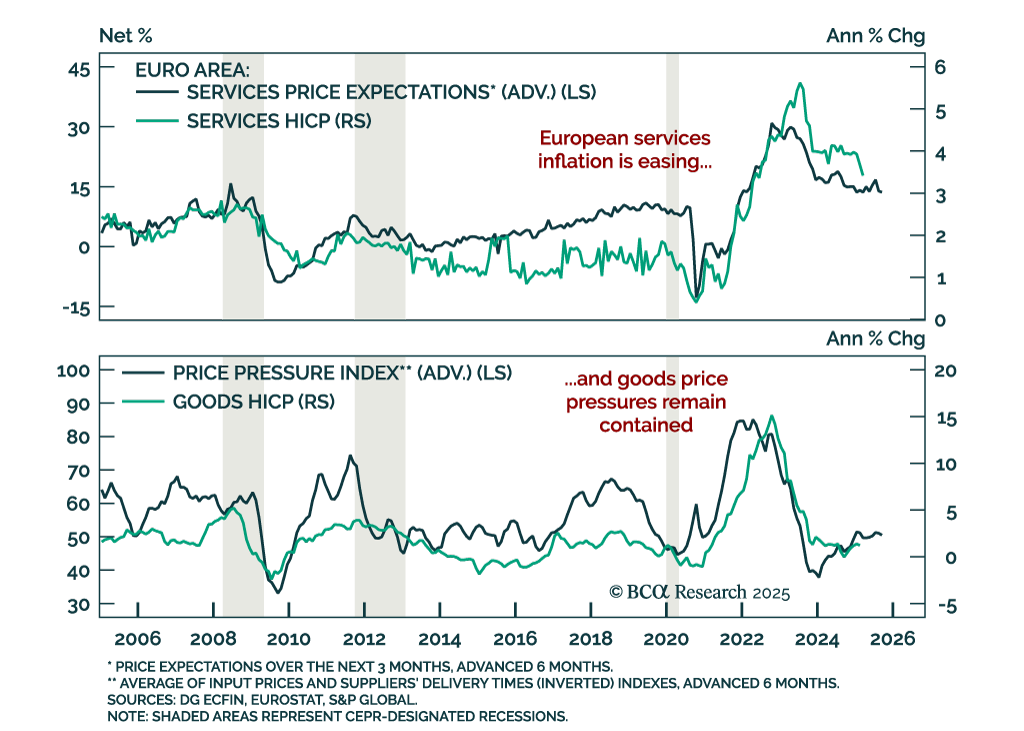

Eurozone inflation is cooling steadily, supporting our tactical overweight in German bunds versus European equities and increasing the odds of an April ECB cut. Headline HICP eased to 2.2% y/y in March from 2.3%, while core came in cooler than expected at…

Our Global Fixed Income strategists recommend maintaining an underweight allocation to corporate credit versus government bonds in global fixed income portfolios. Within corporates, they are neutral on the US, UK, Japan, and Australia, and underweight on…

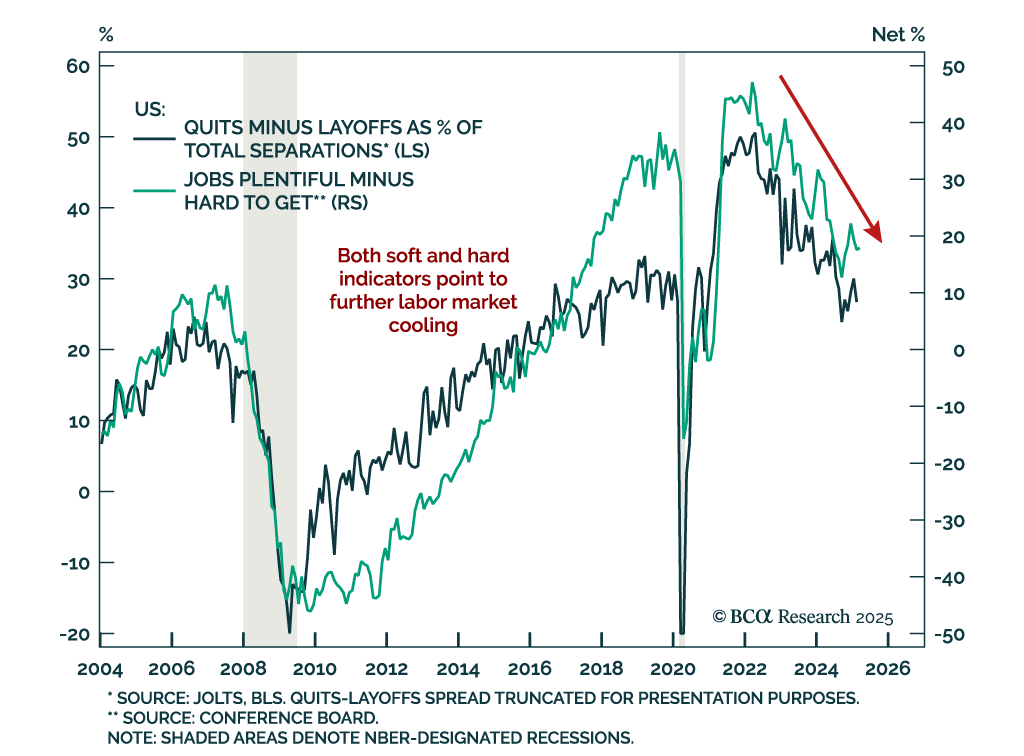

Labor market data continues to cool, reinforcing our overweight in government bonds and above-benchmark duration stance. February job openings fell to 7.6m, below expectations. Declining quits and rising layoffs signal that labor market slack is increasing.…