Developed Countries

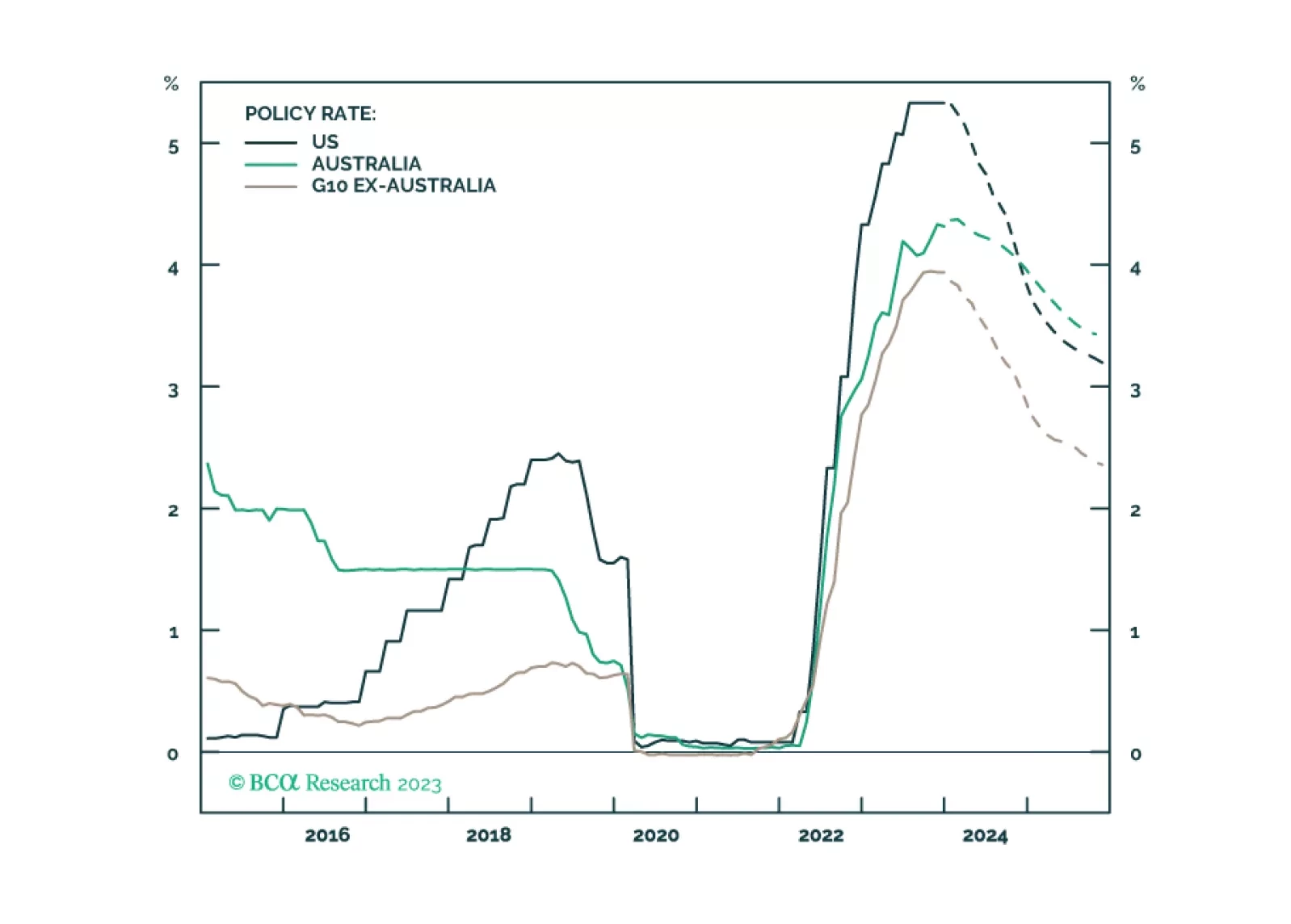

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.

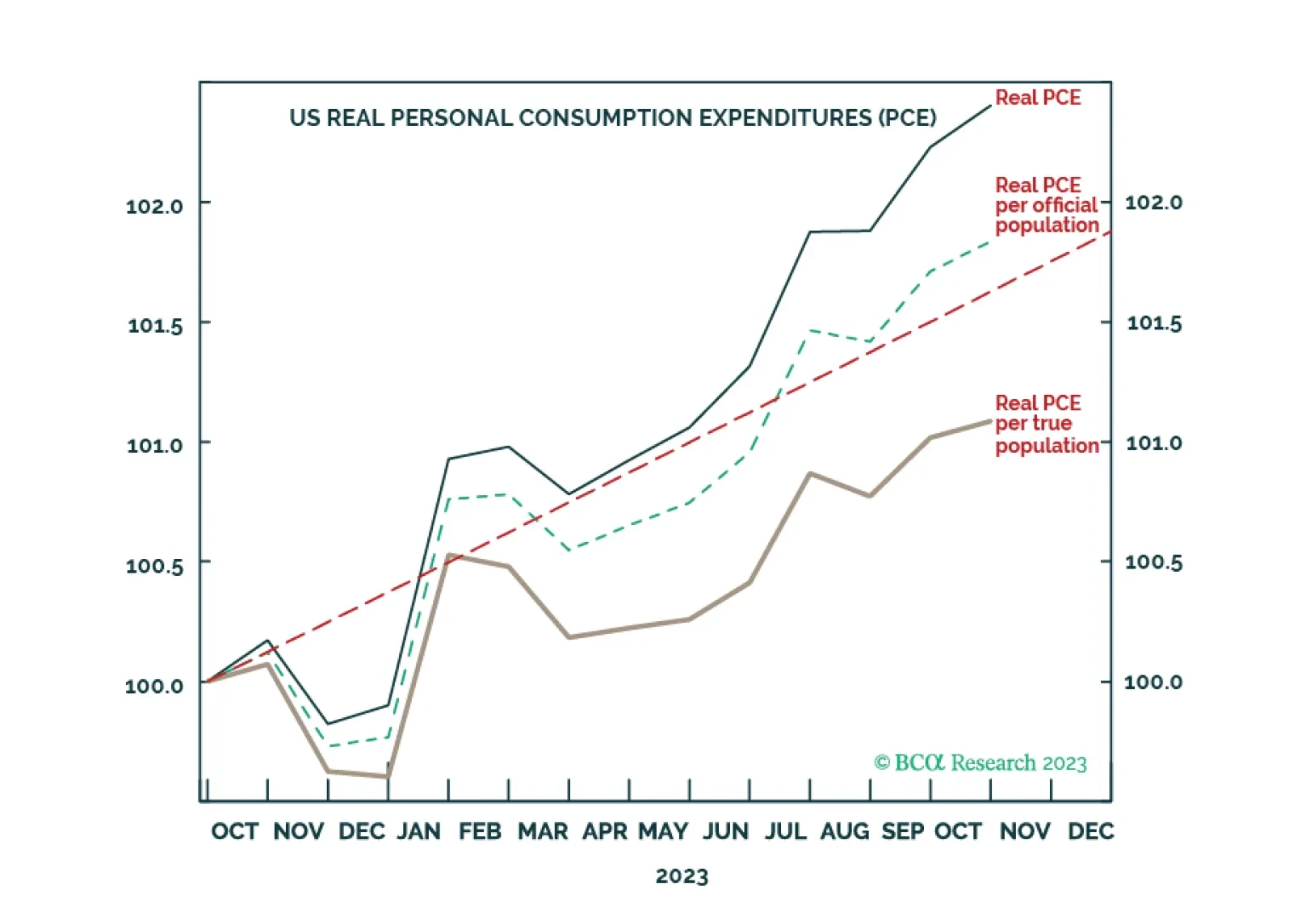

Illegal immigration into the US has skyrocketed to record levels. Correctly accounting for this, US real consumption growth on a per head basis is already fragile. Meanwhile, the real bond yield is only now approaching the pain point that typically triggers a recession. Ahead of the upcoming US jobs report, we point out what it would take for the Joshi rule real-time US recession indicator to breach its event horizon. And how to position in stocks and bonds, both tactically and cyclically. Plus: potential turning points in Biotech and Genome, ADBE, and Taiwan versus China.