DM Europe

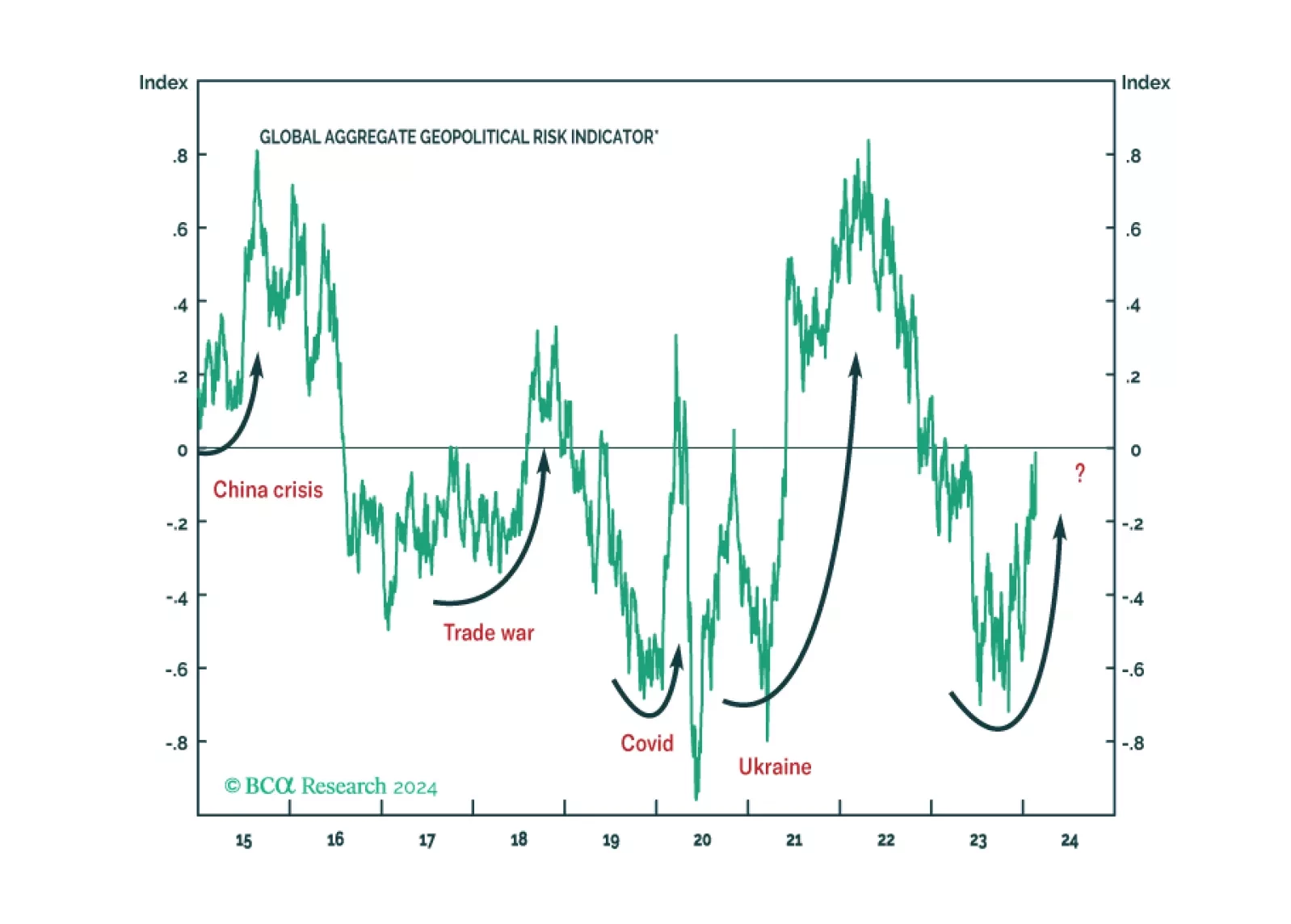

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

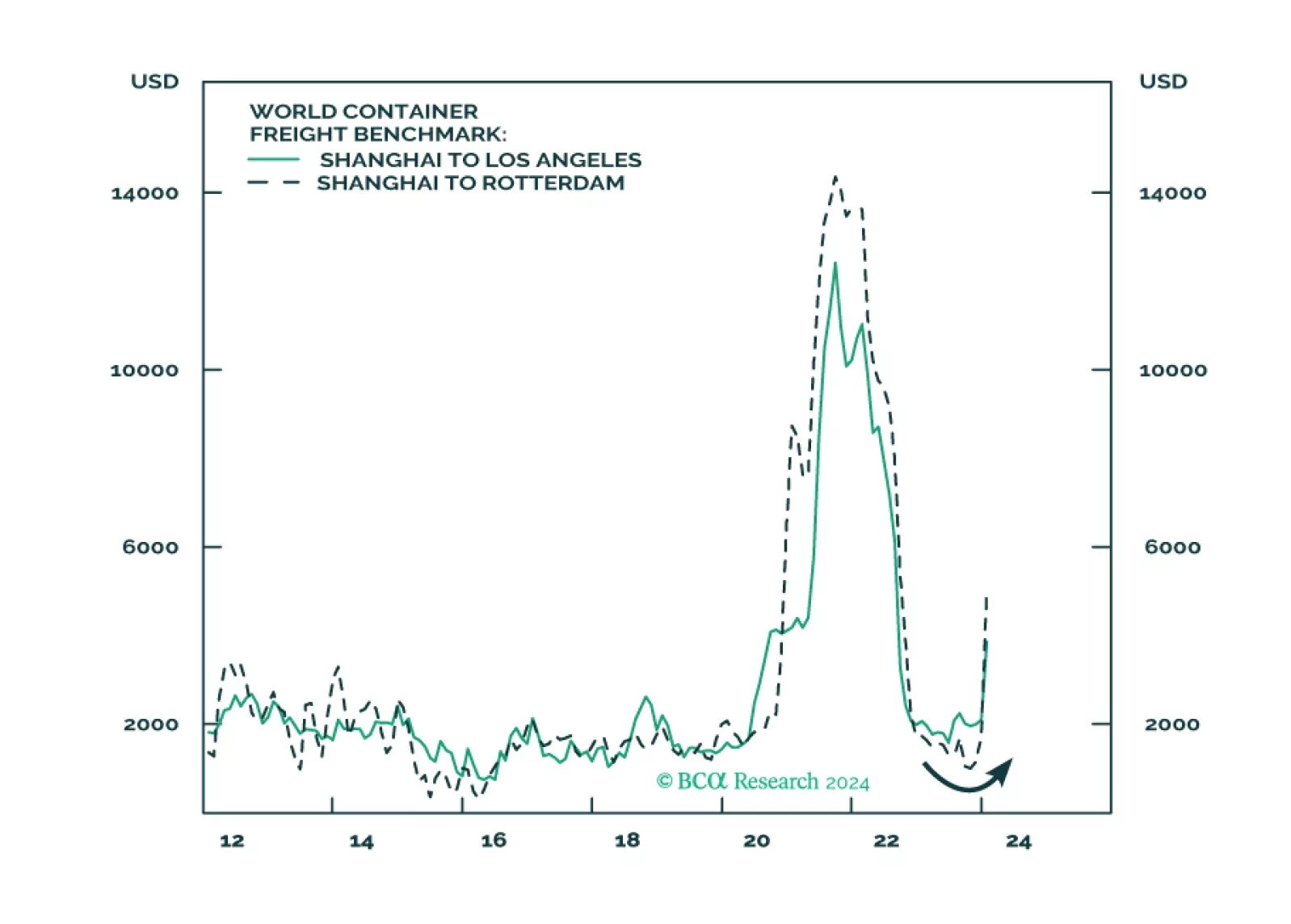

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

We share the edited transcript of a webinar we participated in discussing global trade, trade wars and tariffs, as well as de-risking strategies.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

A series of notable events took place over the Thanksgiving holiday but none of them force us to change our fundamental assessments. The conflict in the Middle East is likely to escalate rather than de-escalate, while the Taiwan Strait has at least a 50/50 chance of seeing tensions escalate next year.

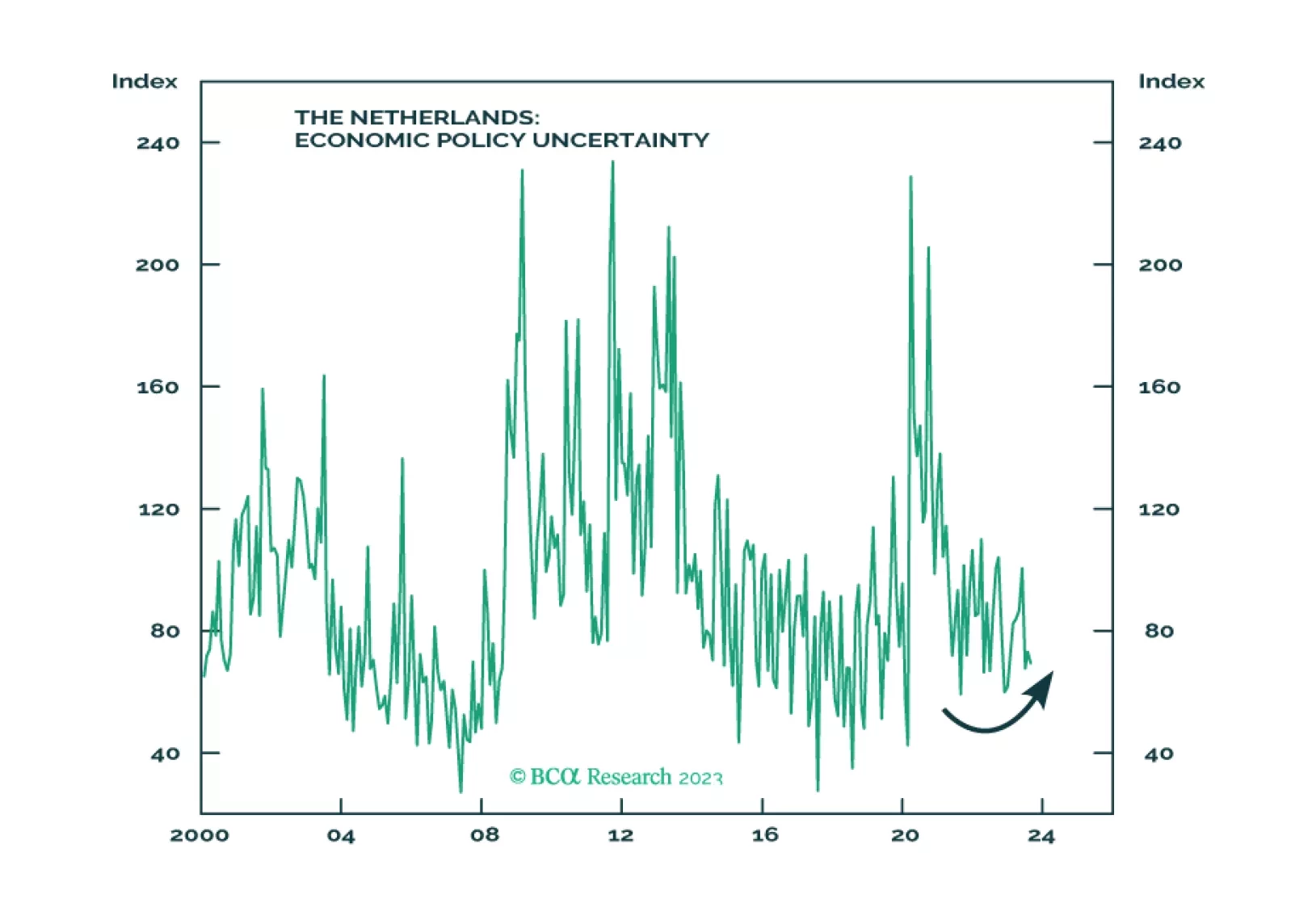

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.