DM Europe

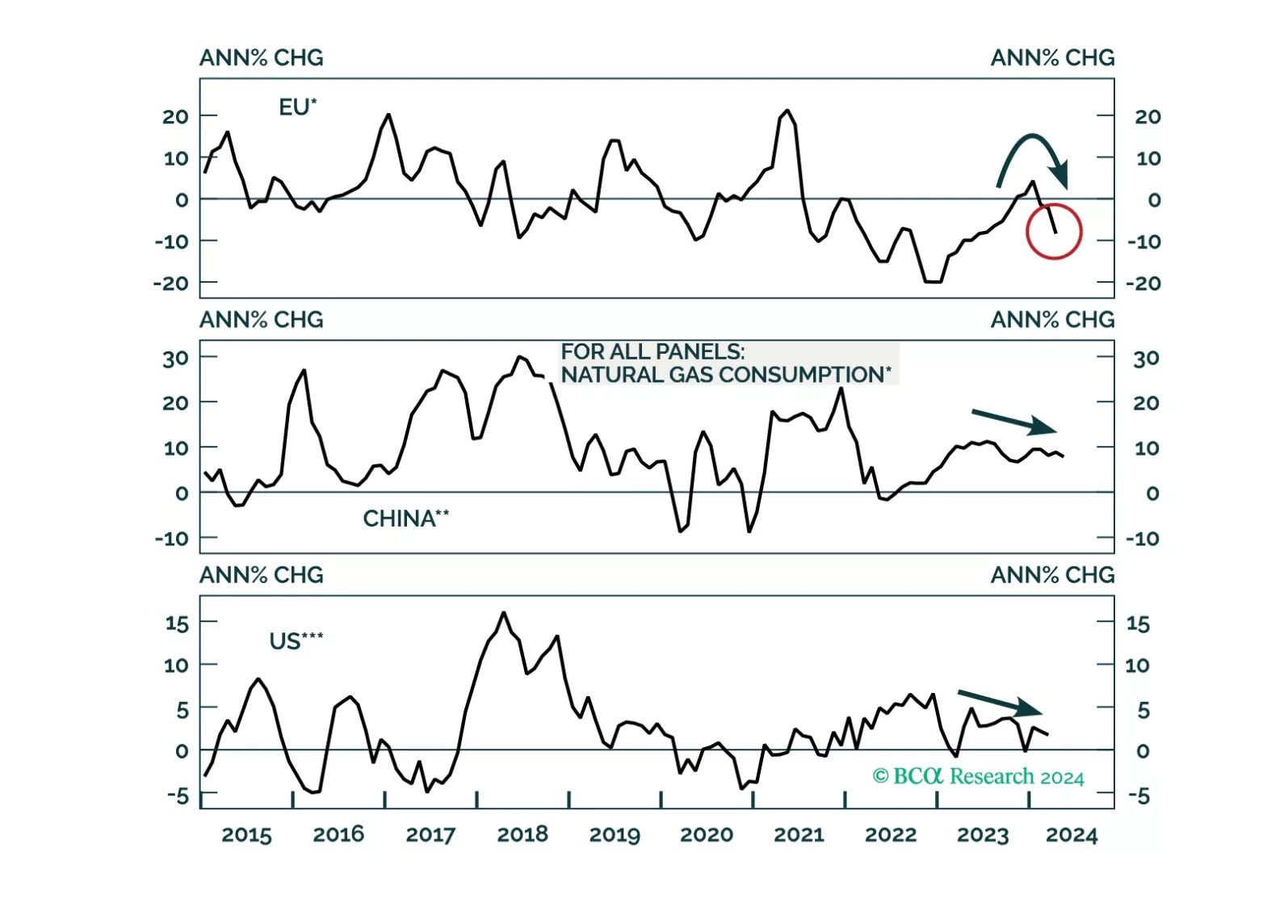

A global economic downturn will be a headwind for natgas prices over the cyclical horizon. Thereafter, LNG capacity additions will help keep the market in balance into the end of the decade. That said, Europe’s increased dependence on global LNG flows raises its exposure to market dynamics in the rest of the world. This will keep volatility elevated versus pre-Ukraine war.

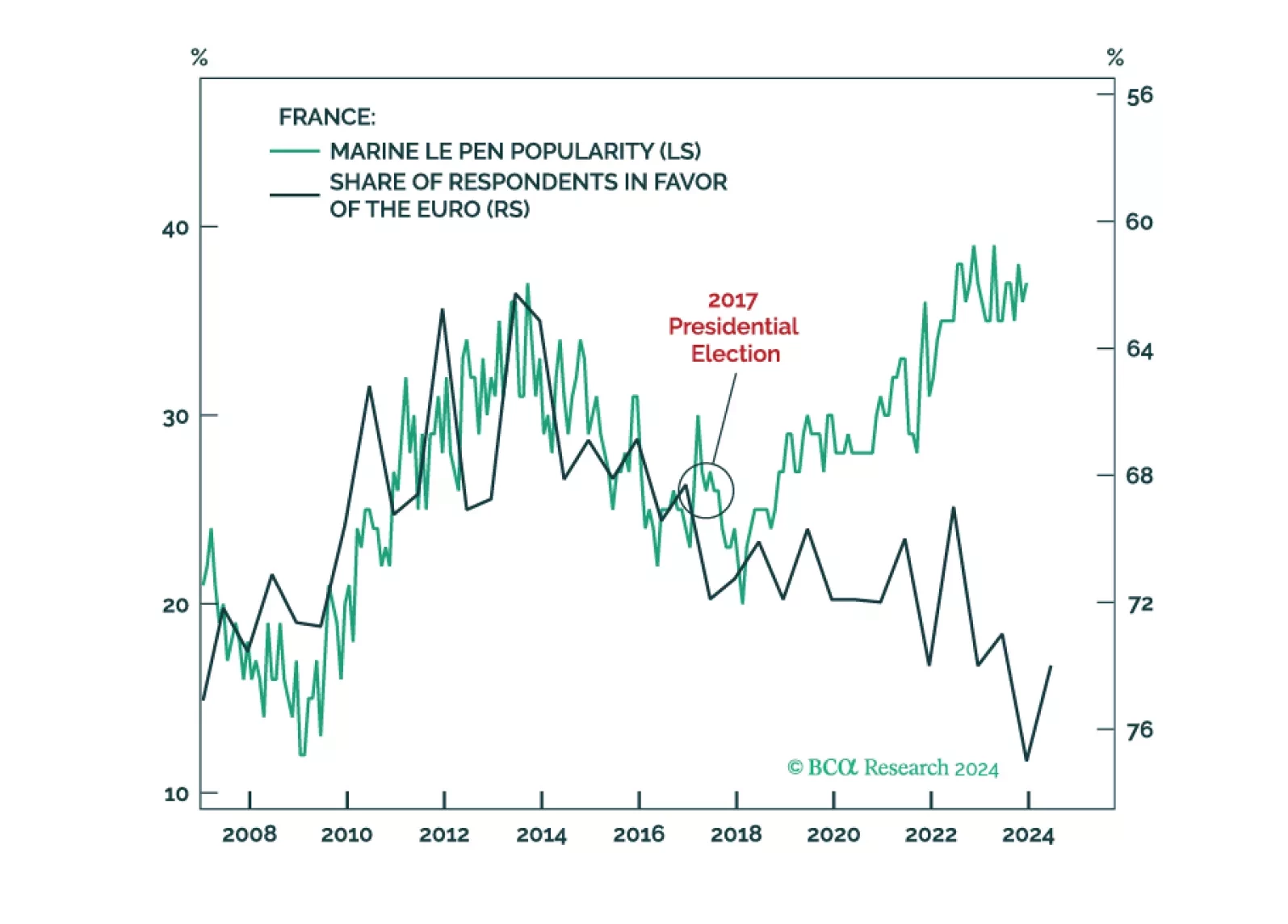

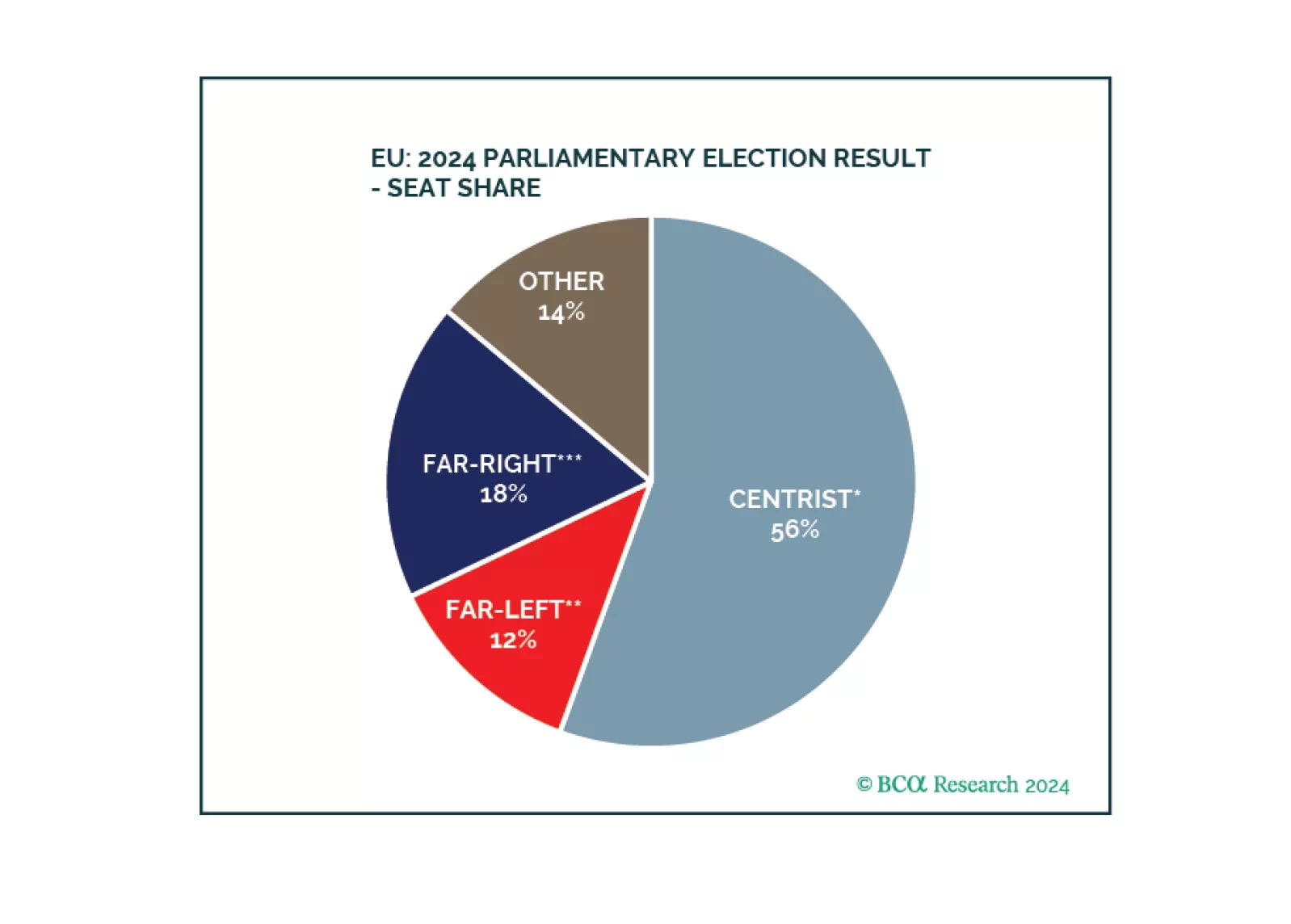

Investors in European sovereign bonds should find solace that continental voters are not turning away from support for EU integration. As such, populist parties are not really that “far” left or right. And as long as they want to maintain popular support, they will have to abide by the fiscal rules imposed by Brussels. No such supranational constraint exists in the U.S., the real risk for global bond operators.

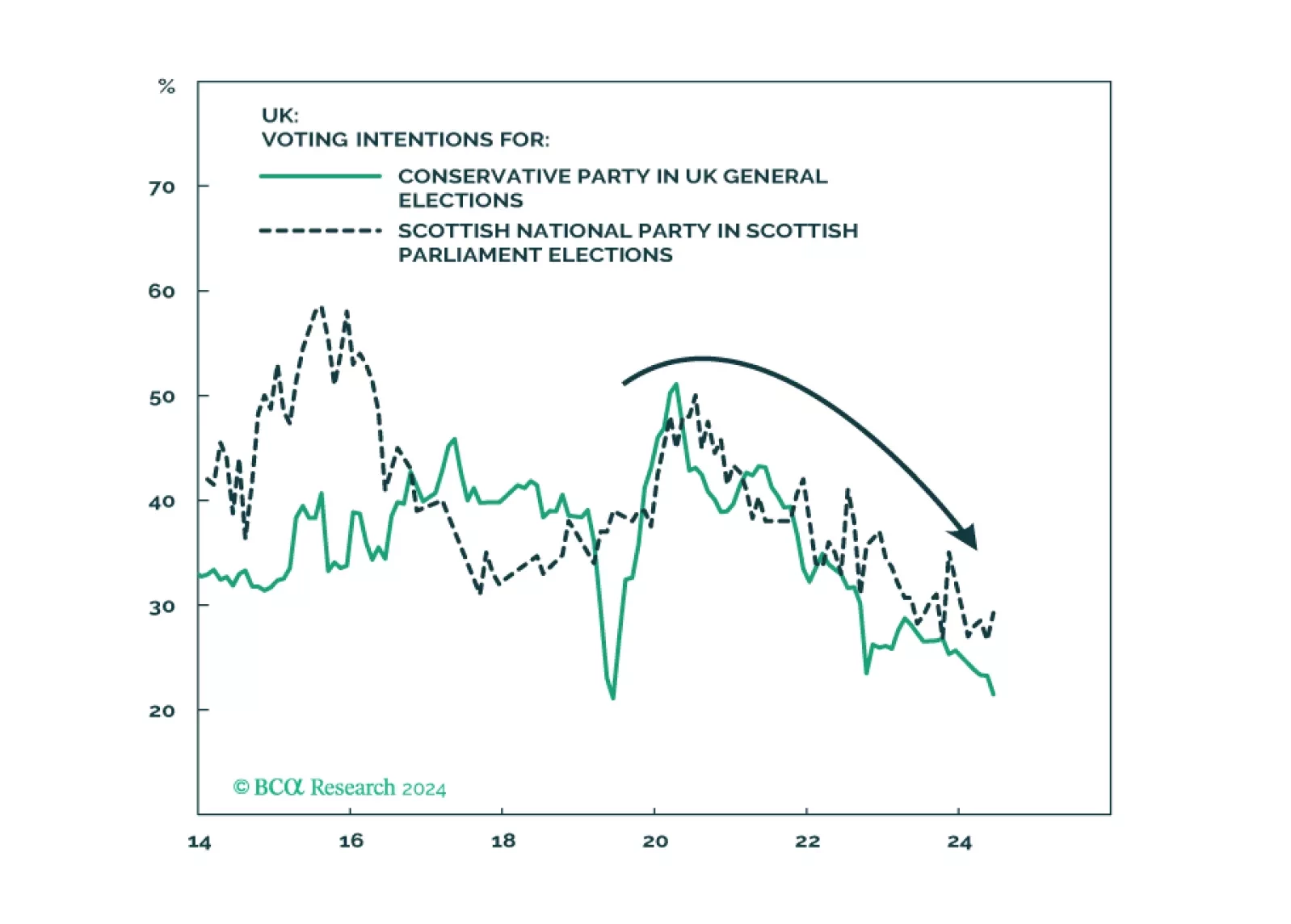

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v

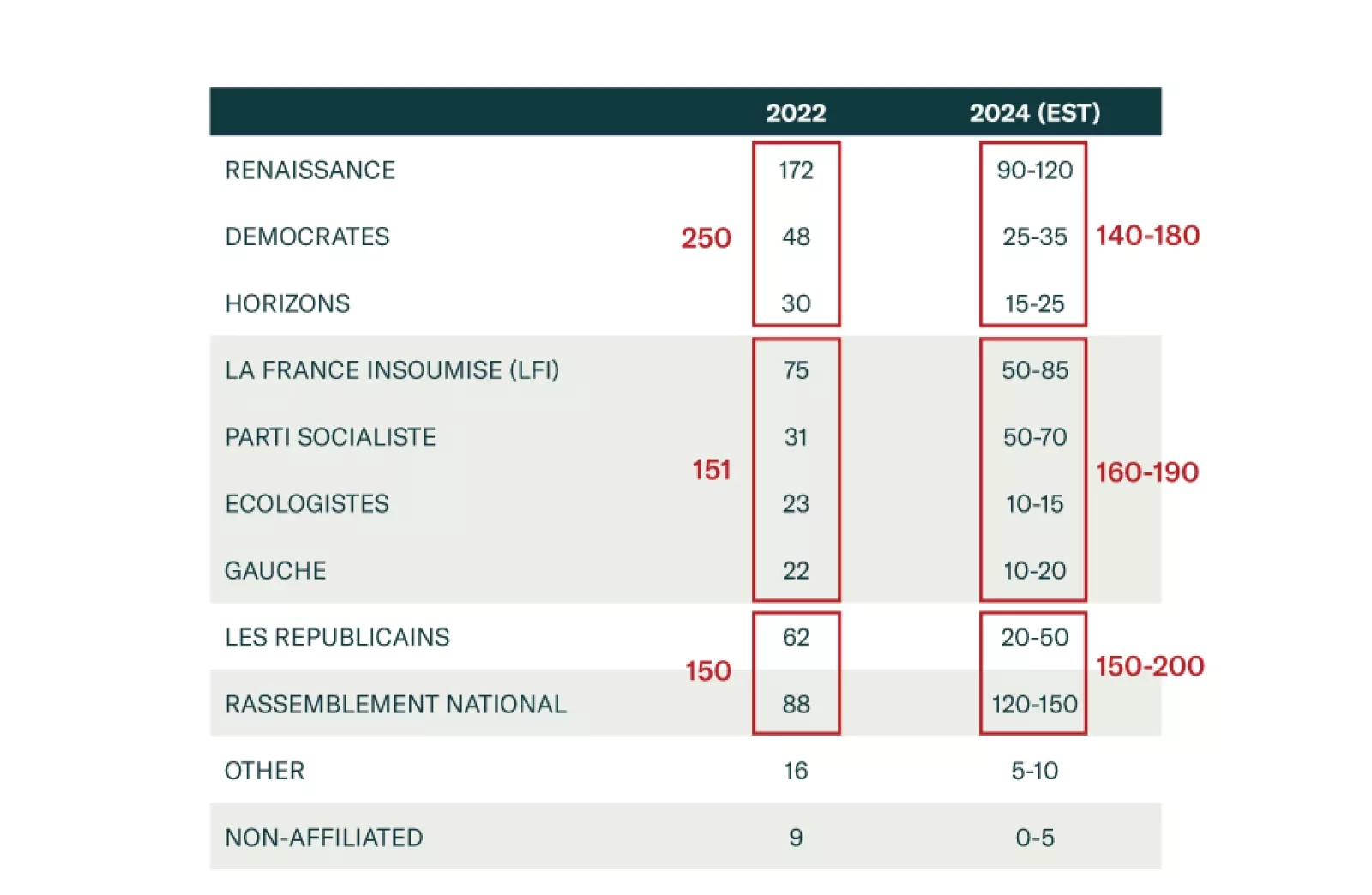

European assets are selling off as investors panic about the upcoming French election. Is this panic justified, and if so, for how long?

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.