Currencies In-Depth

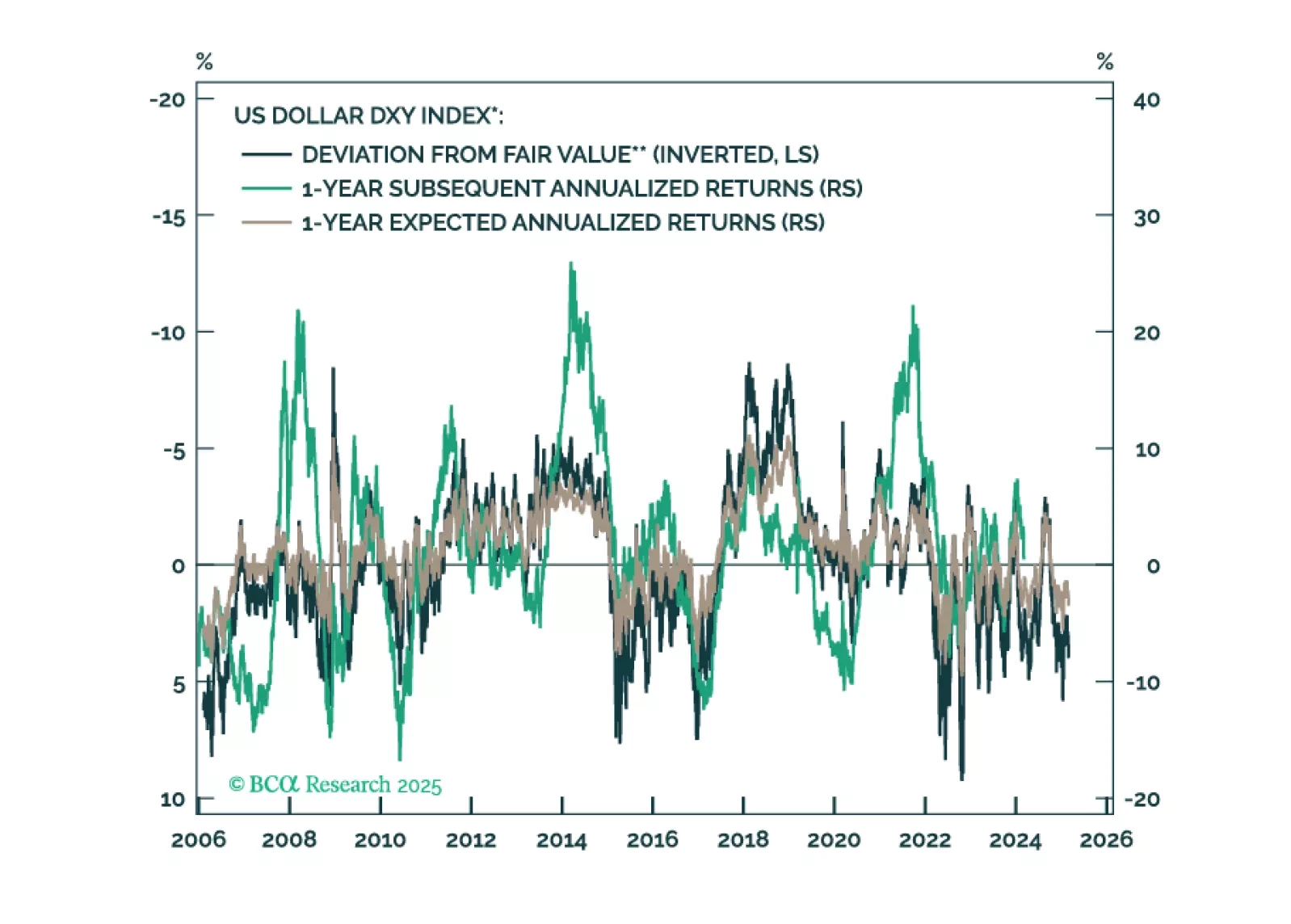

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

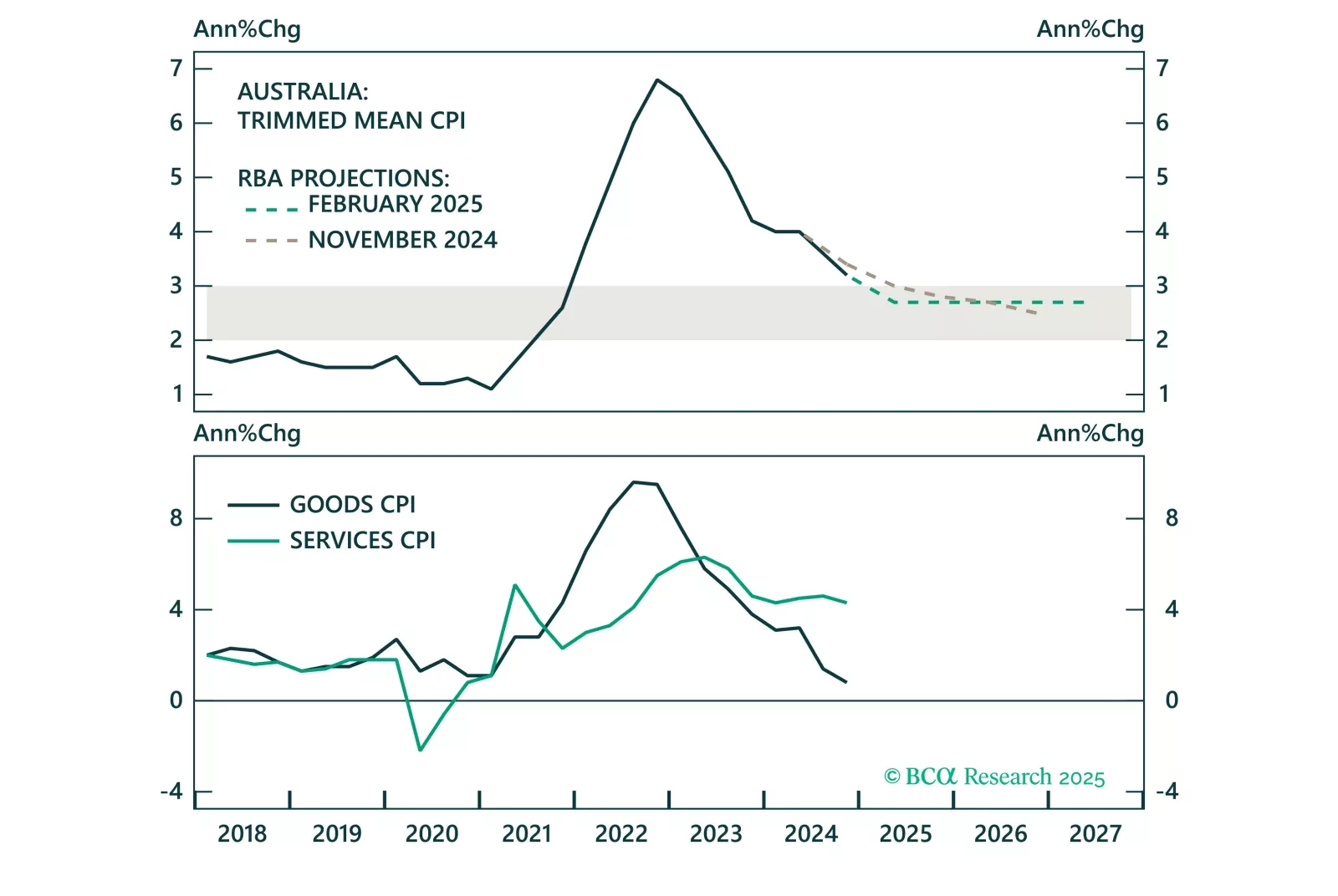

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

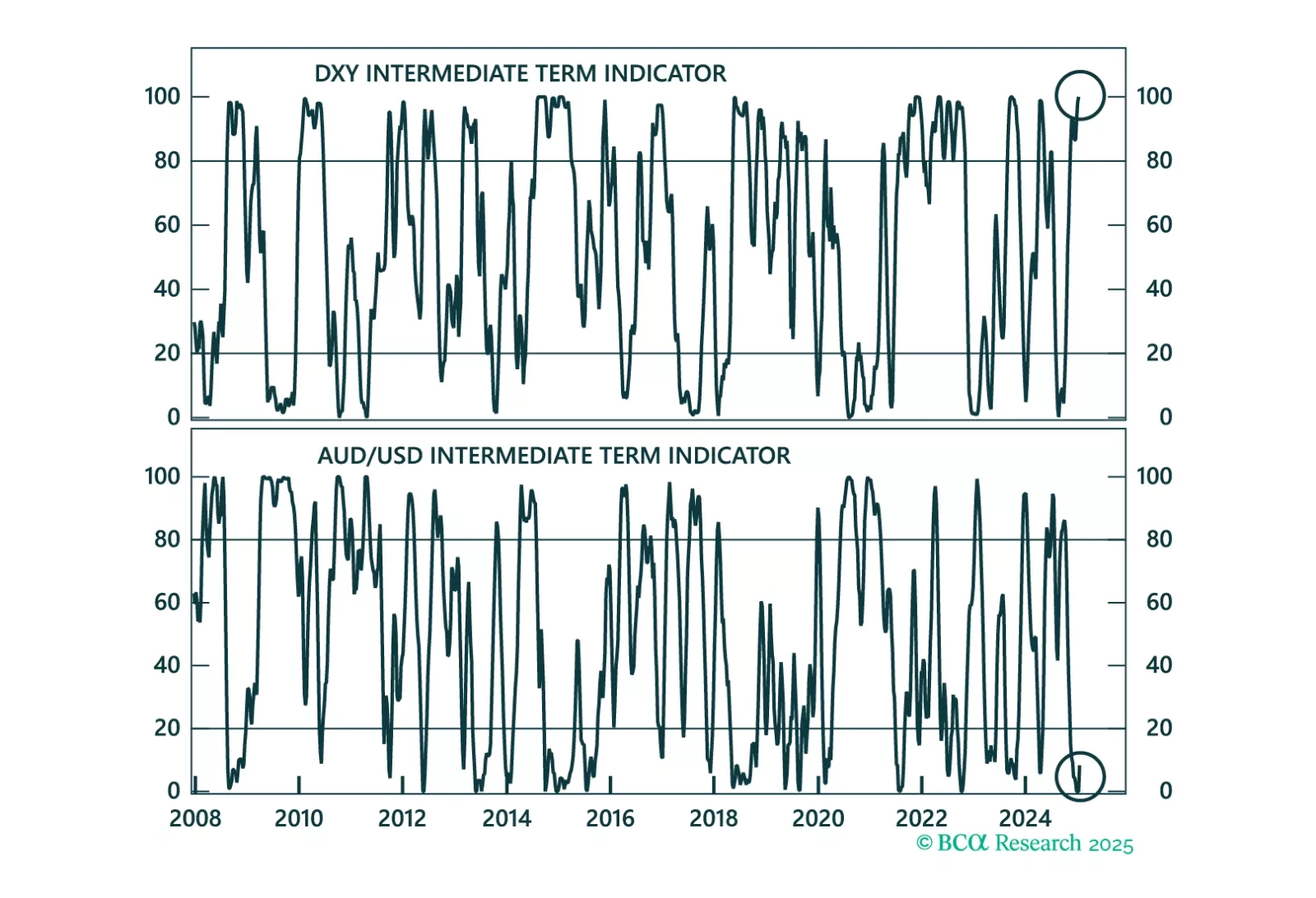

In lieu of all the geopolitical and economic news in media, this report looks at where next the dollar is likely to trend in the next one-to-three months. Our view is down, though on a cyclical horizon (six-to-twelve months), we would not be short the dollar, for now.

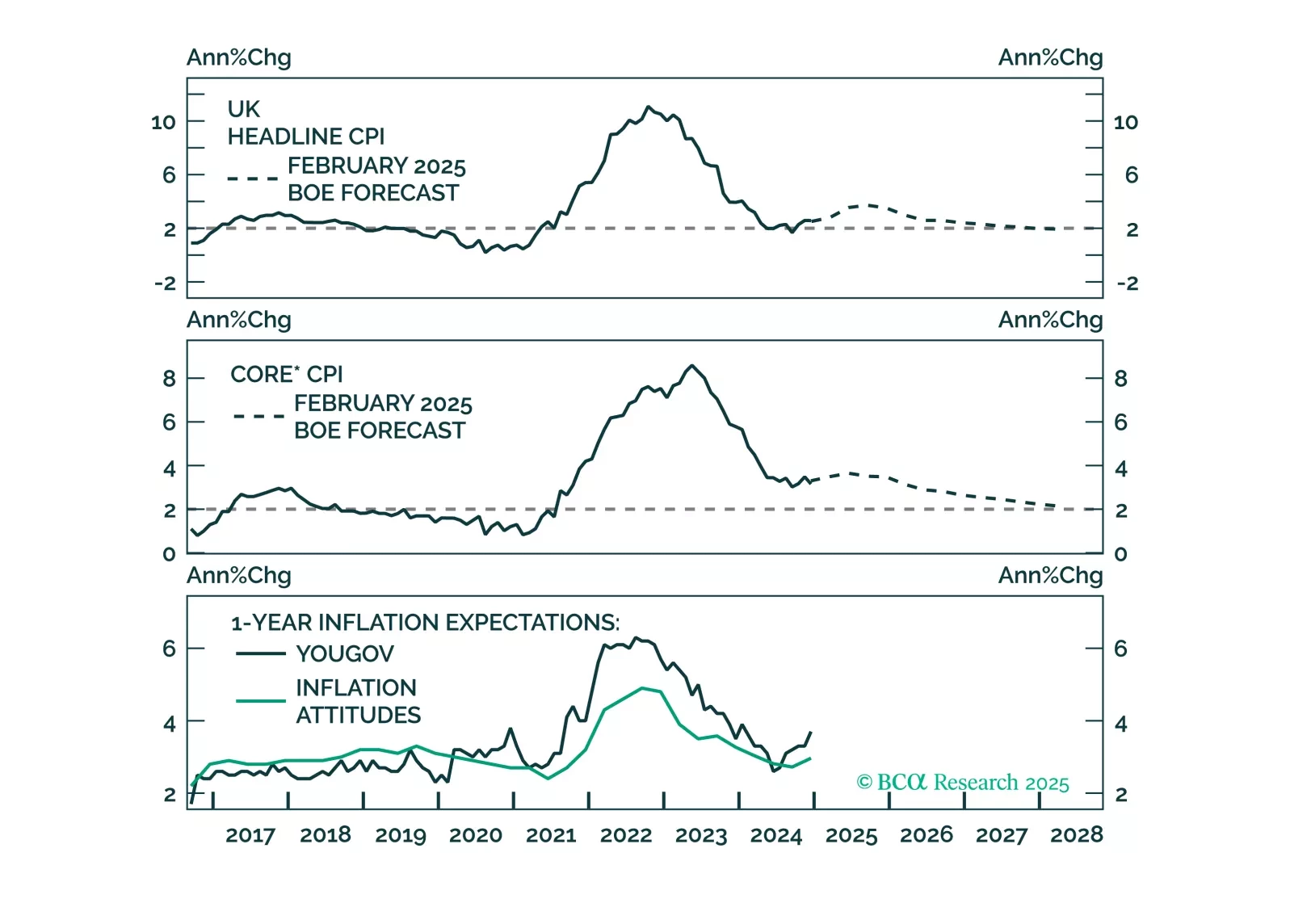

Following today’s Bank of England’s policy meeting, at which the policy rate was cut by 25 bps, we discuss our outlook for monetary policy in the UK. We expect the gradual easing to continue and discuss the investment implications for UK gilts and sterling.

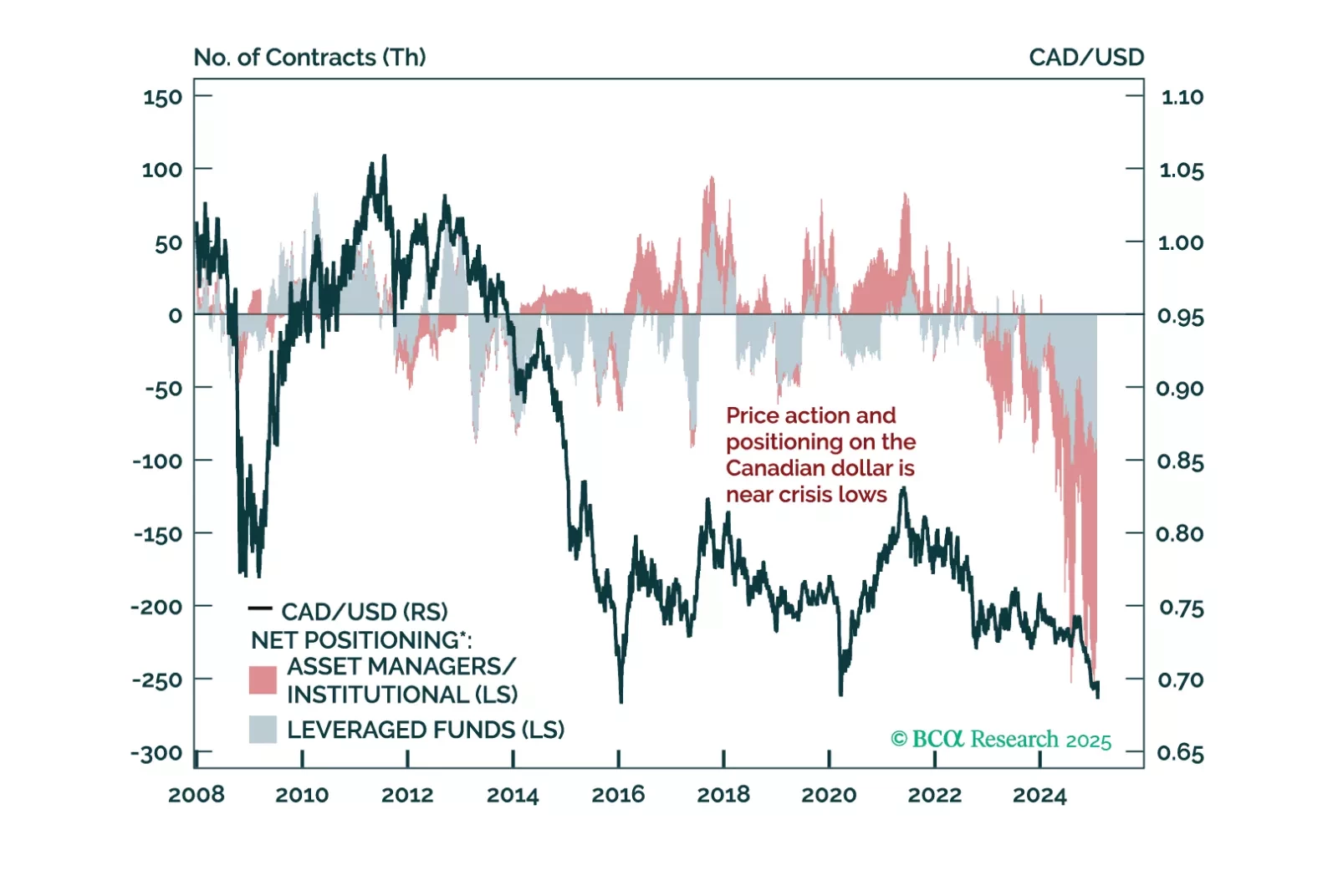

This Insight is a post mortem on Canadian assets, after the threat of tariff wars.

This Insight looks at what investors should do with CAD and fixed-income assets, given the rate cut by the Bank of Canada today.

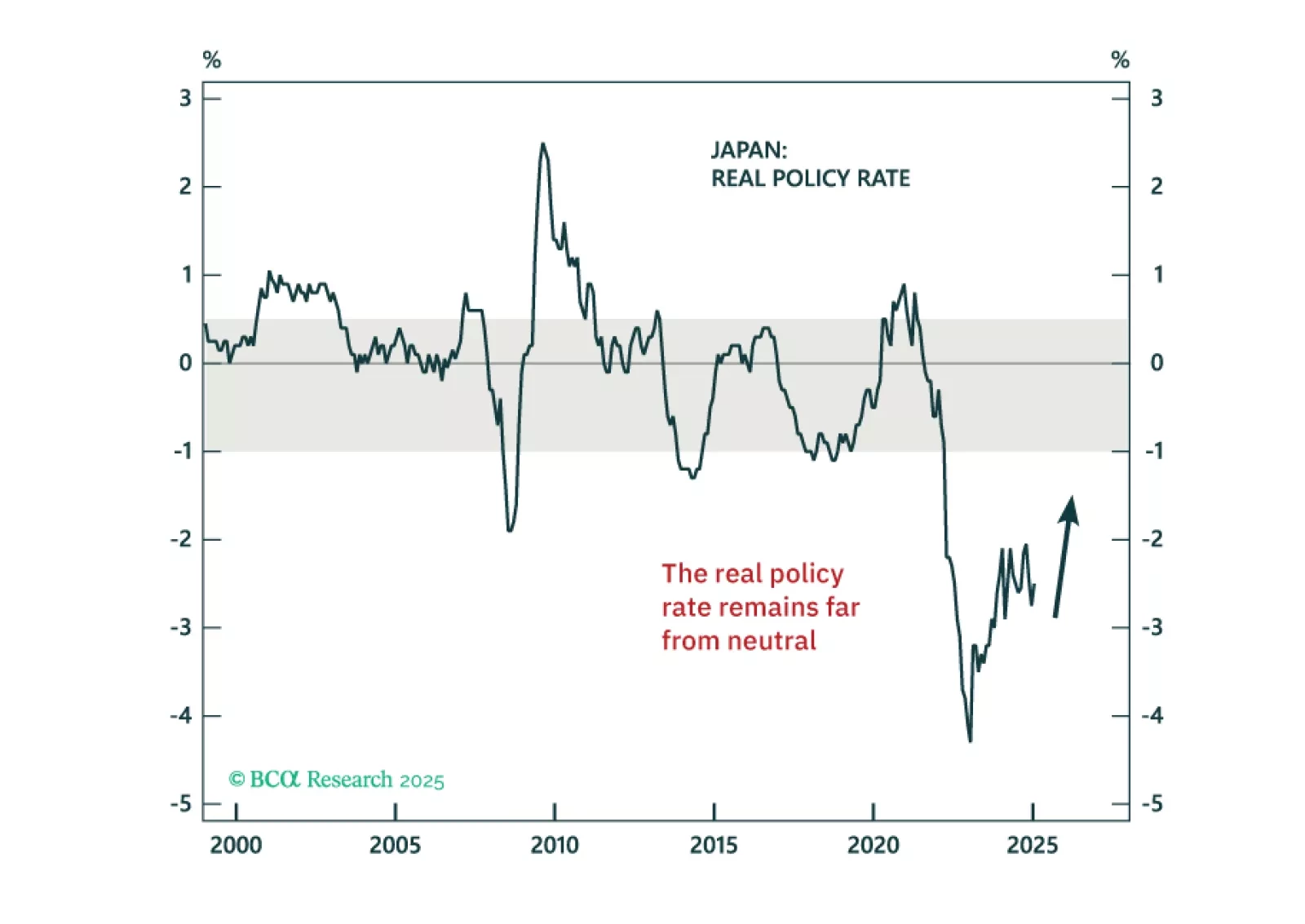

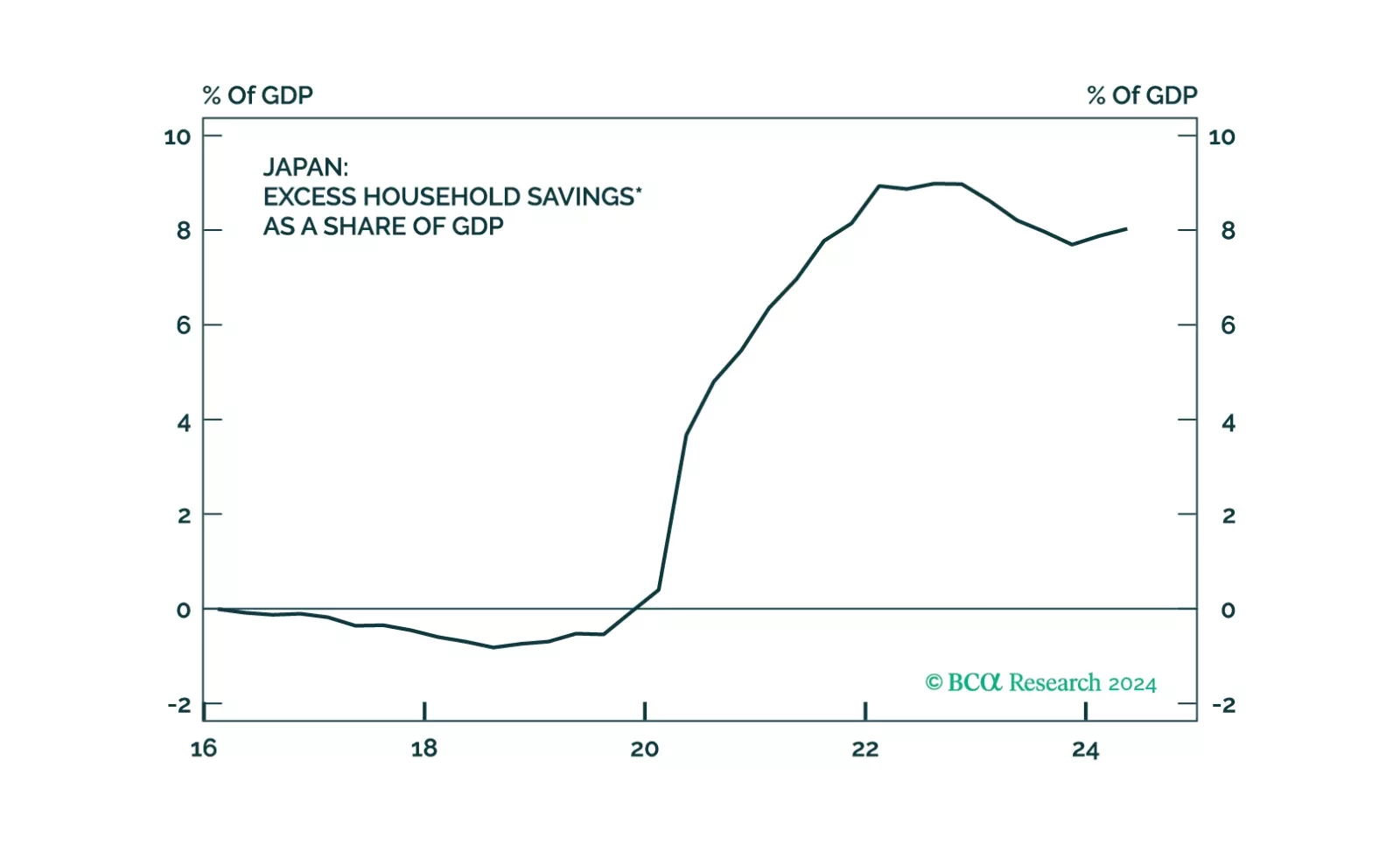

In today’s Strategy Insight, we discuss the monetary policy outlook for the Bank of Japan, following the 25-bps rate hike overnight, and what it means for JGBs and the yen.

This week’s report looks at the US dollar, from the lens of one very cyclical currency – the Australian dollar.

The latest Bank of Japan meeting did not alter our high-conviction views of being long the yen and underweight JGBs.

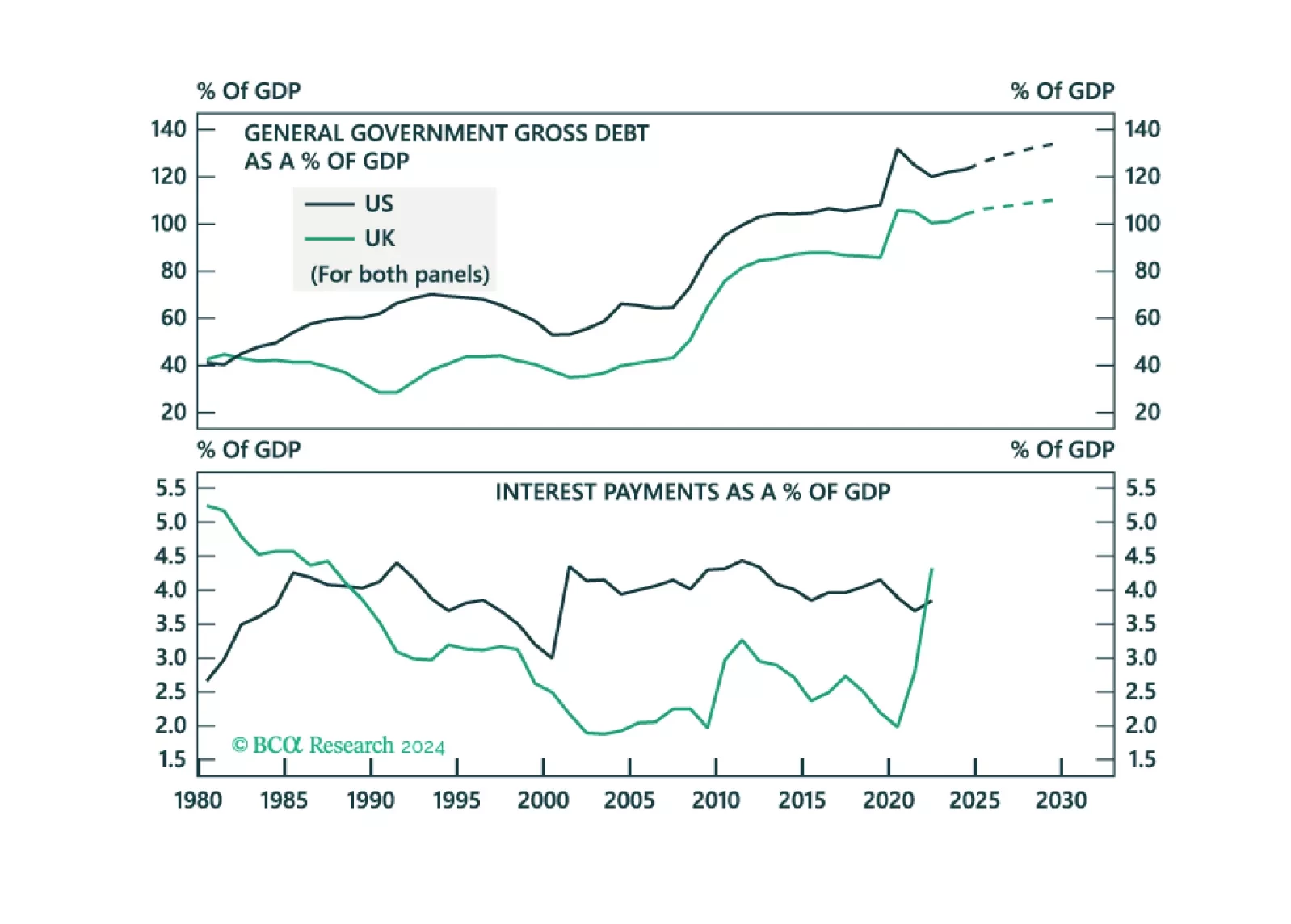

In this Insight, we assess whether investors should expect fiscal turbulence in the UK, that will drive UK yields higher and the pound lower.