Currencies

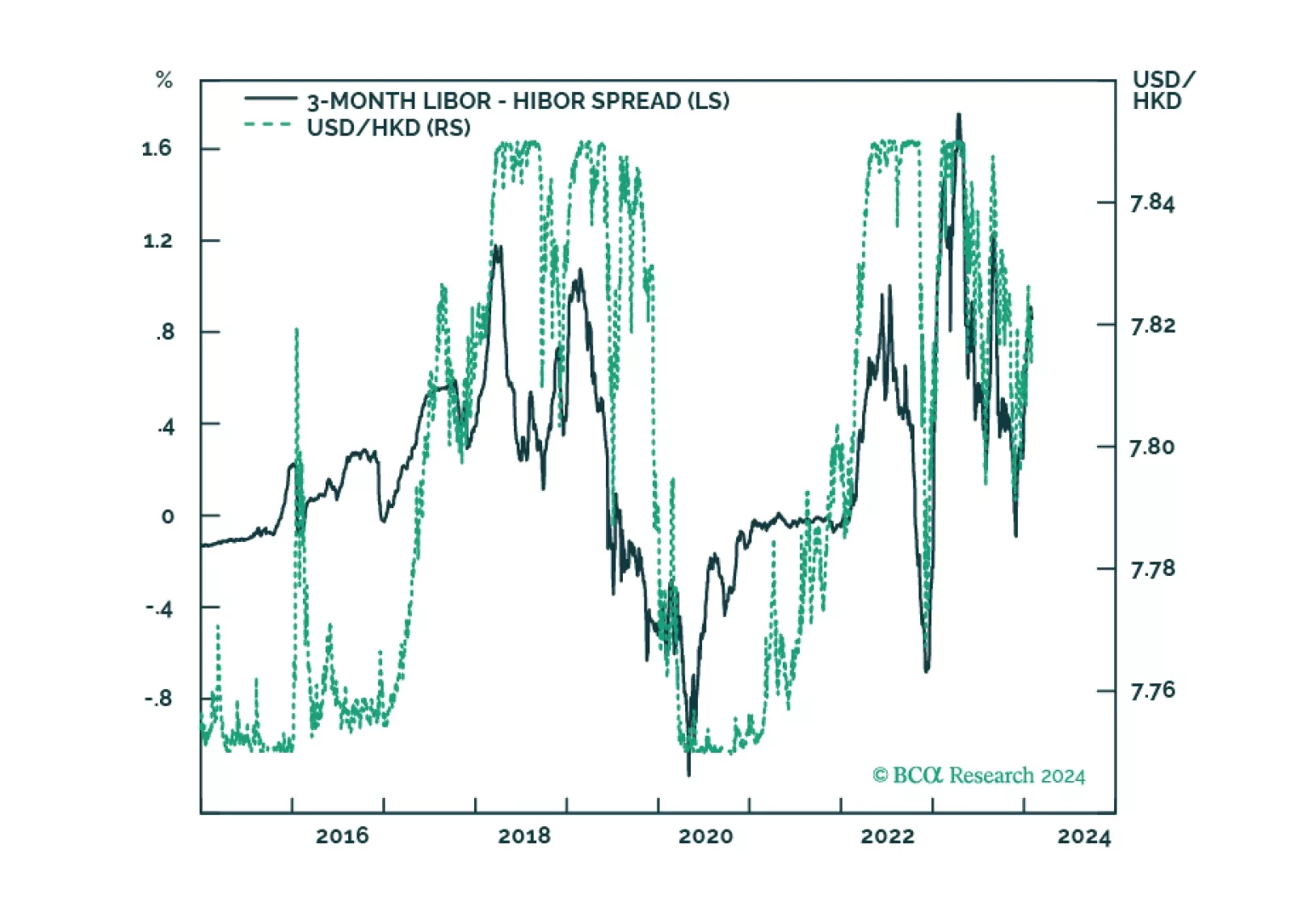

In this Special Report, we update our thinking on the Hong Kong SAR dollar peg, with implications for domestic asset markets.

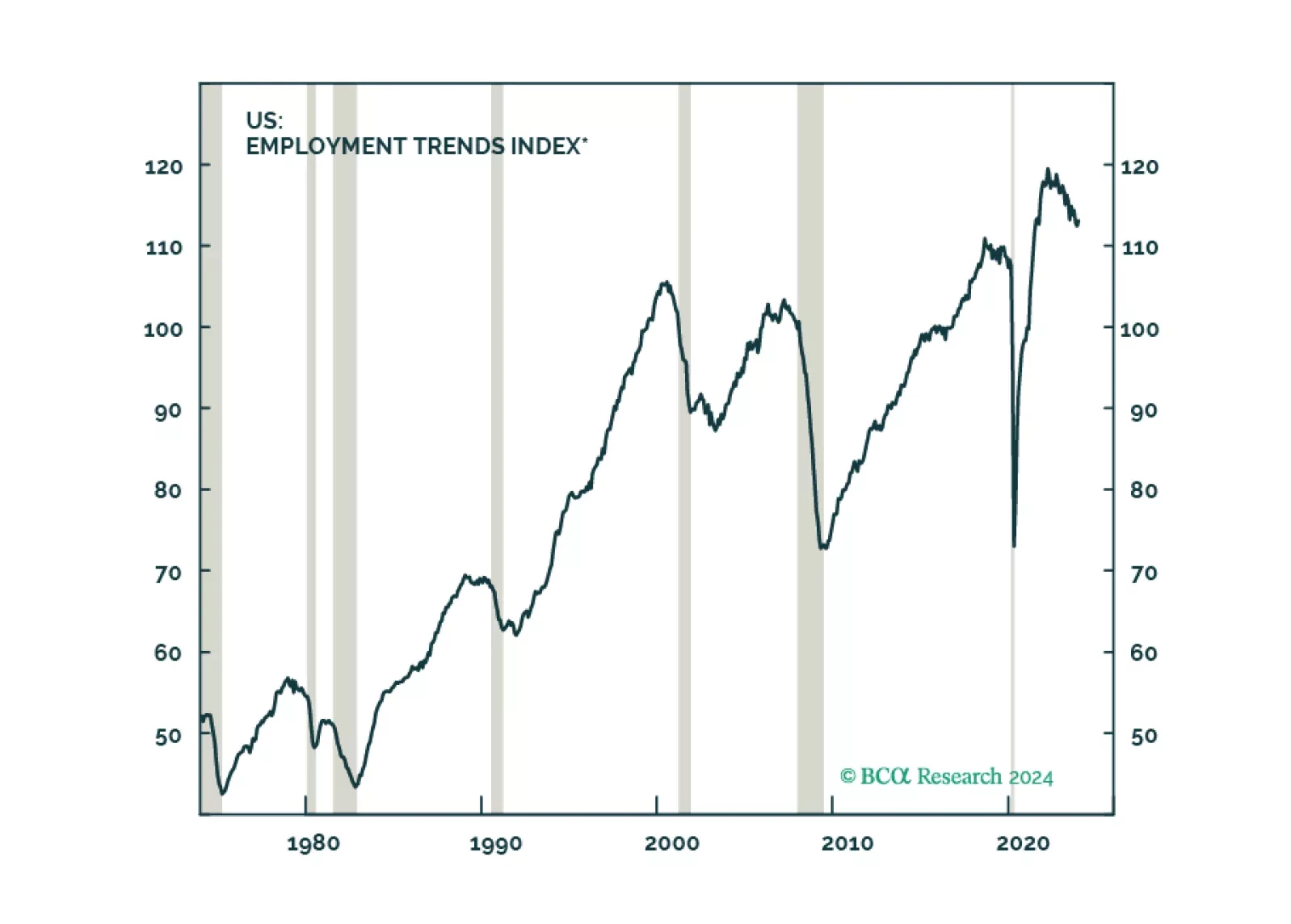

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

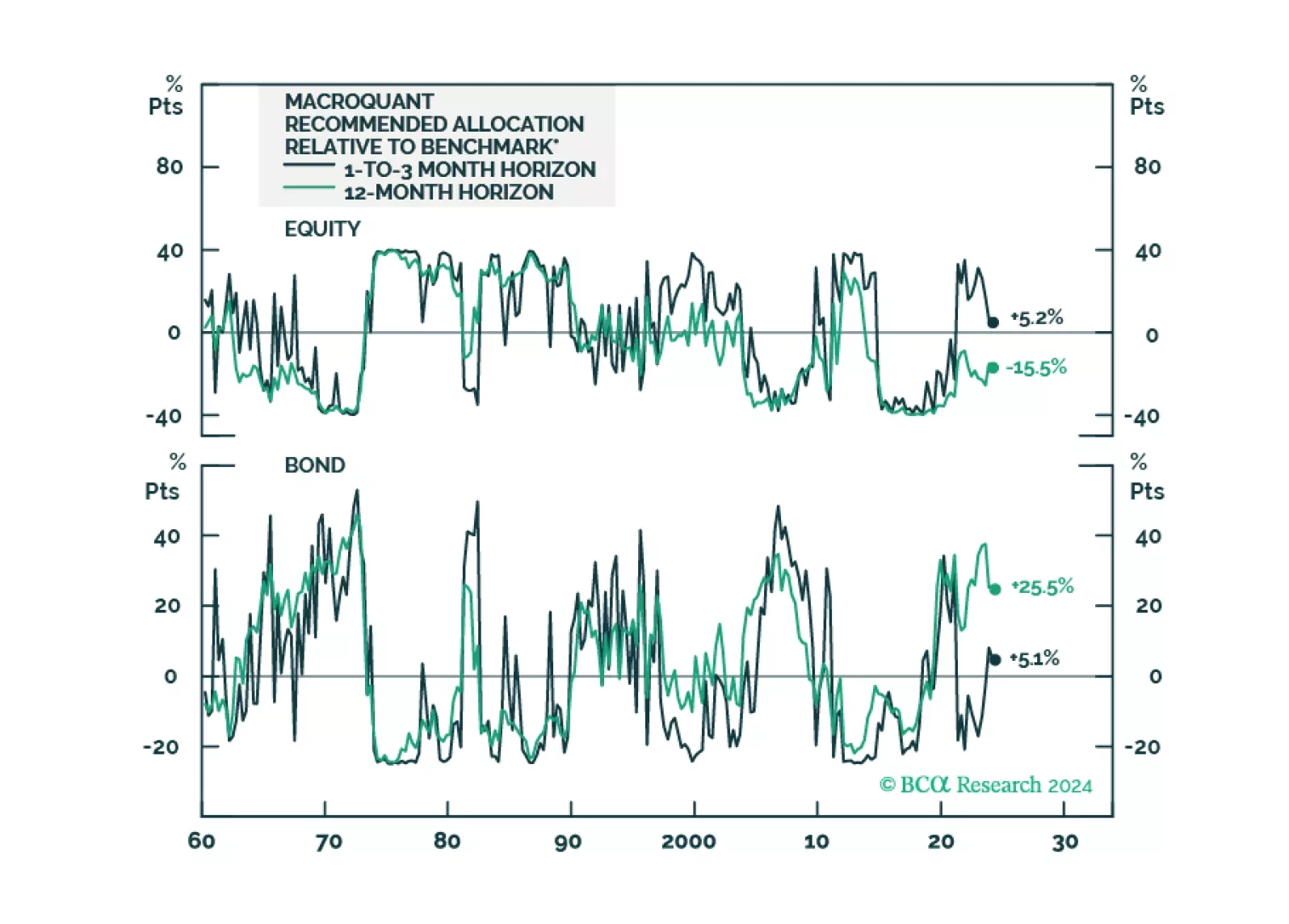

Following the release of the white paper yesterday, today we are sending you the inaugural issue of the MacroQuant Monthly, a report summarizing the output of our next-generation MacroQuant 2.0 model.

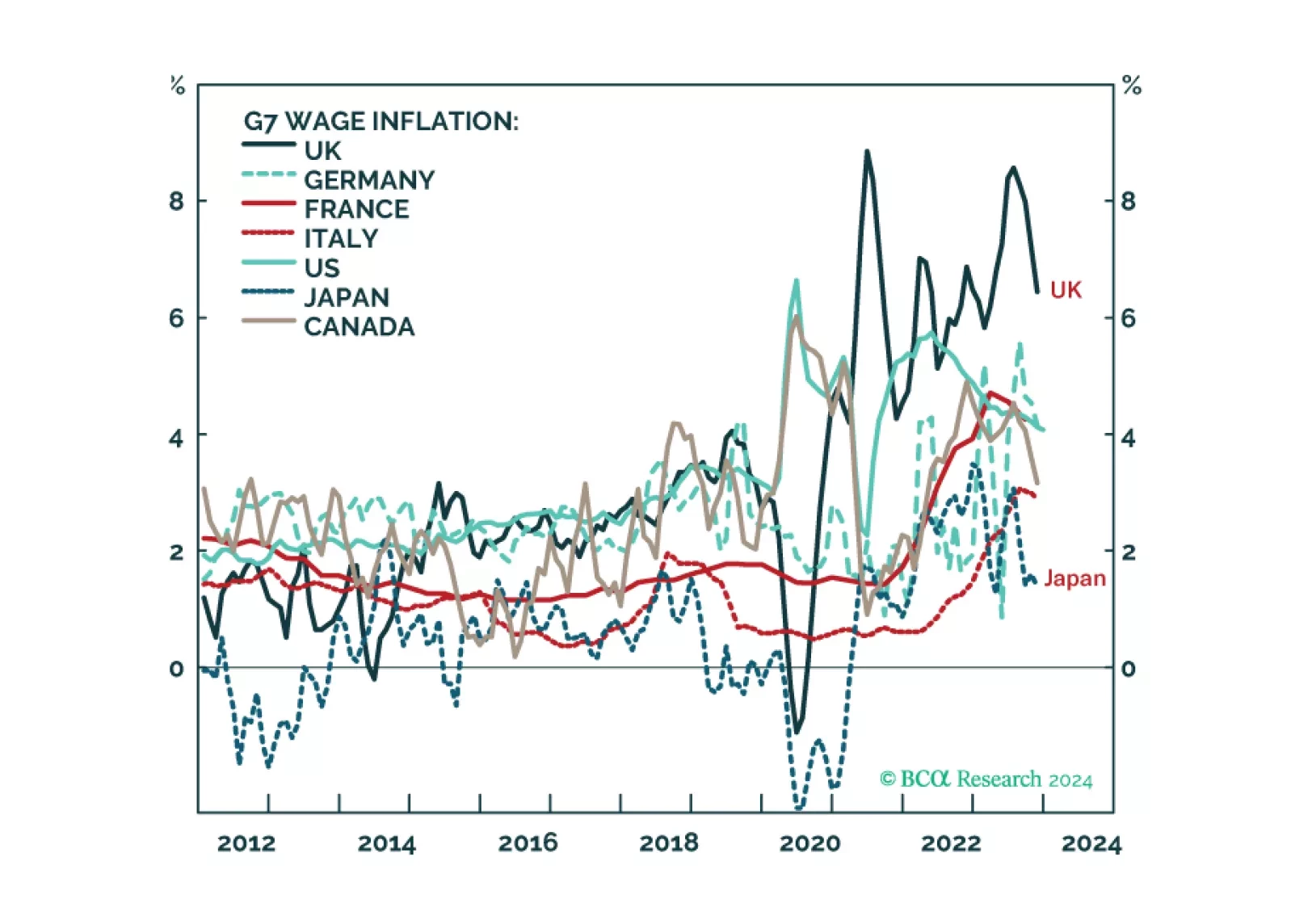

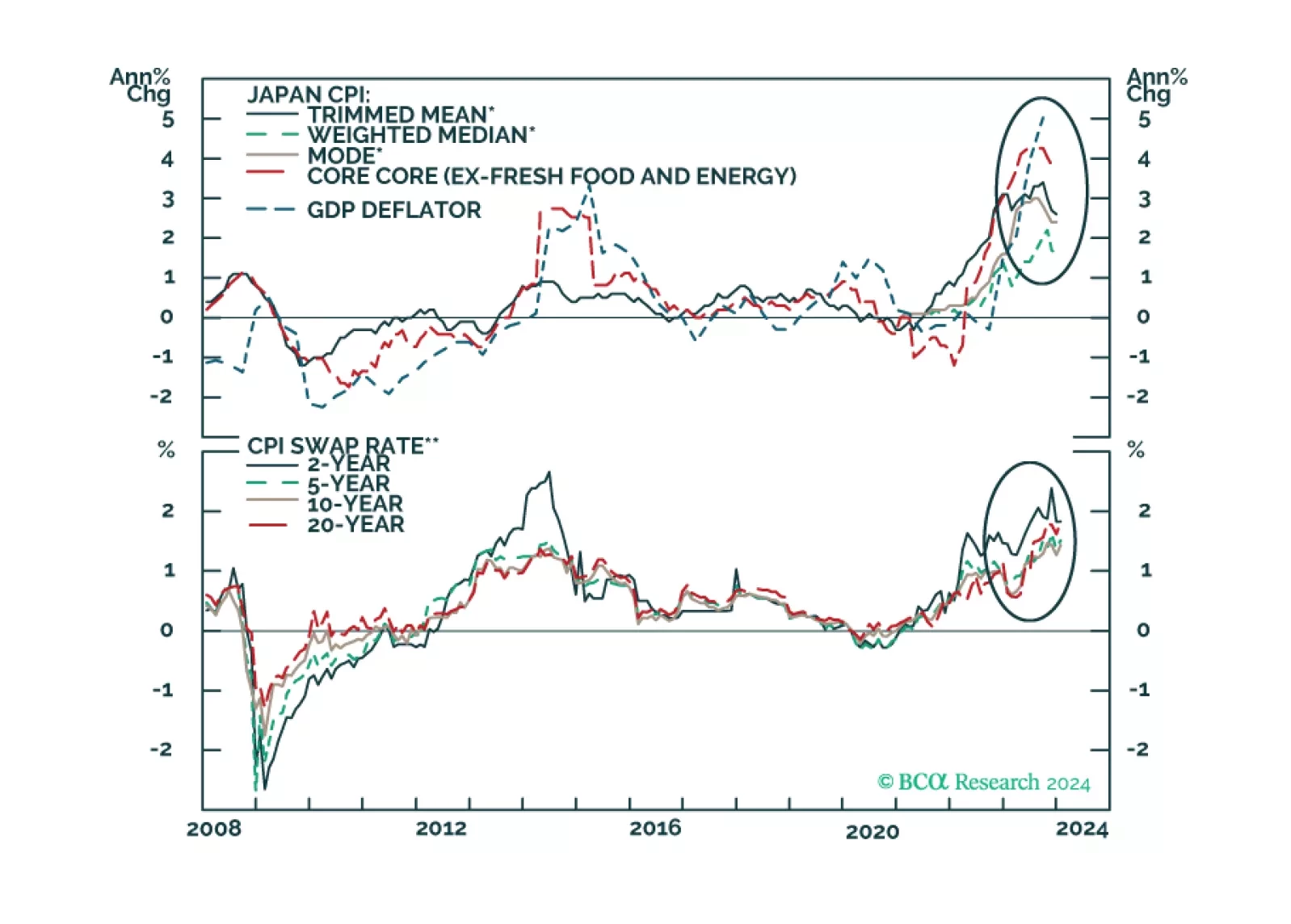

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.

We look at the implications for FX from the slew of central bank meetings this week.

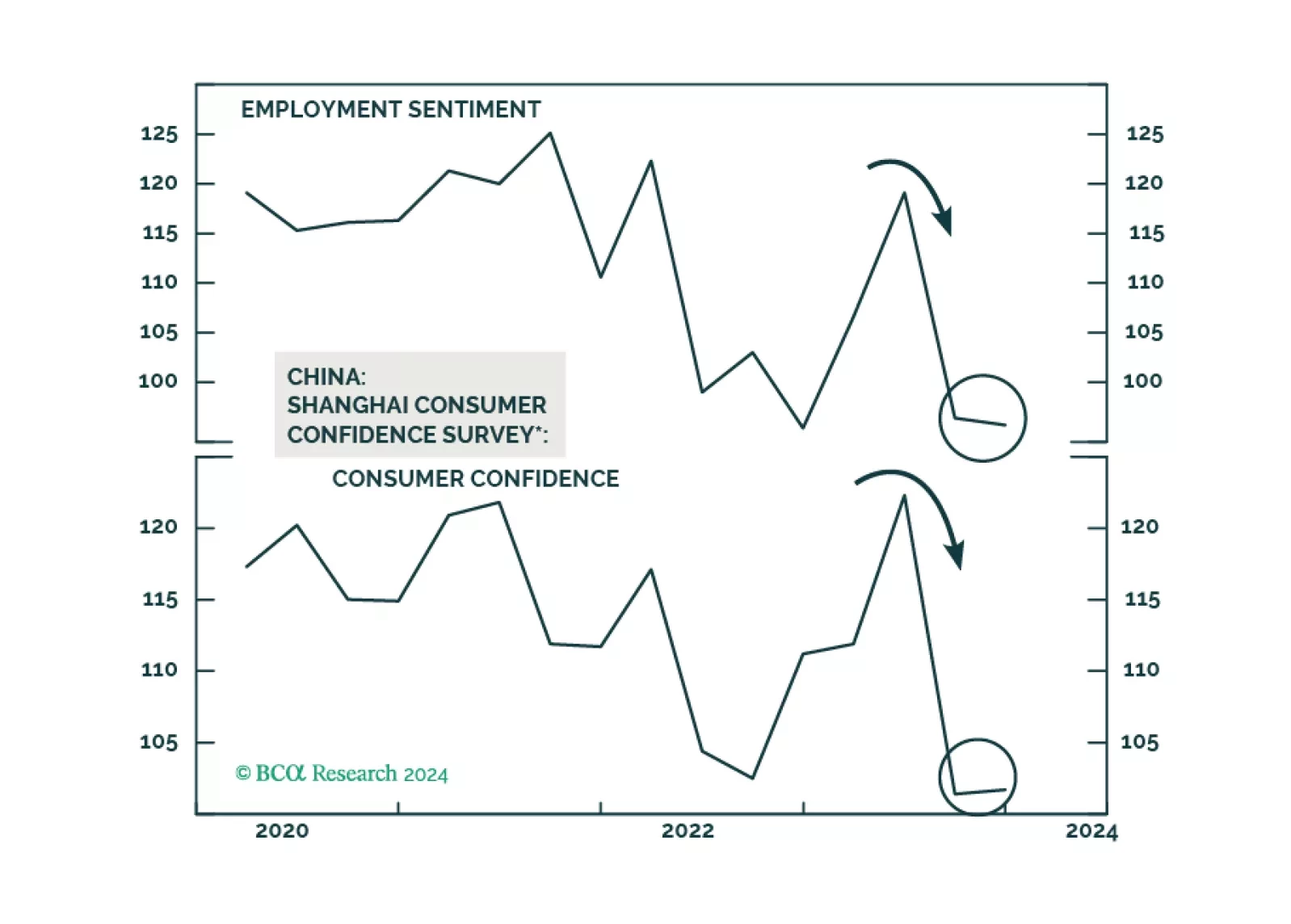

There is no easy way for China to forestall deflation. Provided policymakers are still reluctant to unleash large-size stimulus, more economic disappointments are likely in the coming months, and Chinese stocks will continue to sell off. The yuan is at risk of further depreciation versus the US dollar.

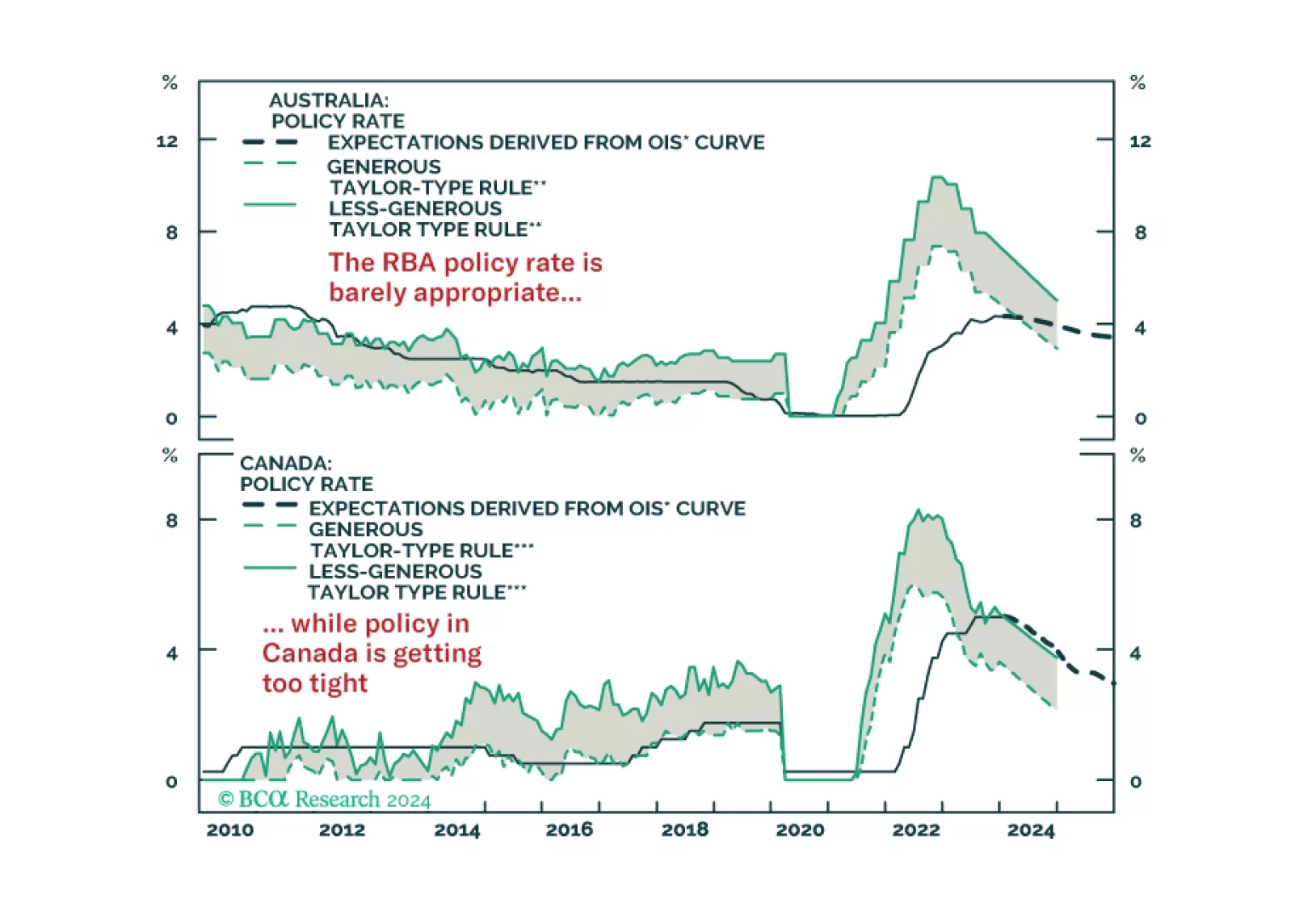

In this Strategy Insight, we assess the monetary policy path for Australia and Canada in 2024 and we discuss how to profit from a growing divergence between the two economies.