Currencies

The four ASEAN stock markets (Indonesia, Malaysia, Thailand, and the Philippines) have fallen in absolute terms over the past year despite the powerful rally in the developed markets. They have also underperformed their EM benchmark. Our Emerging Markets…

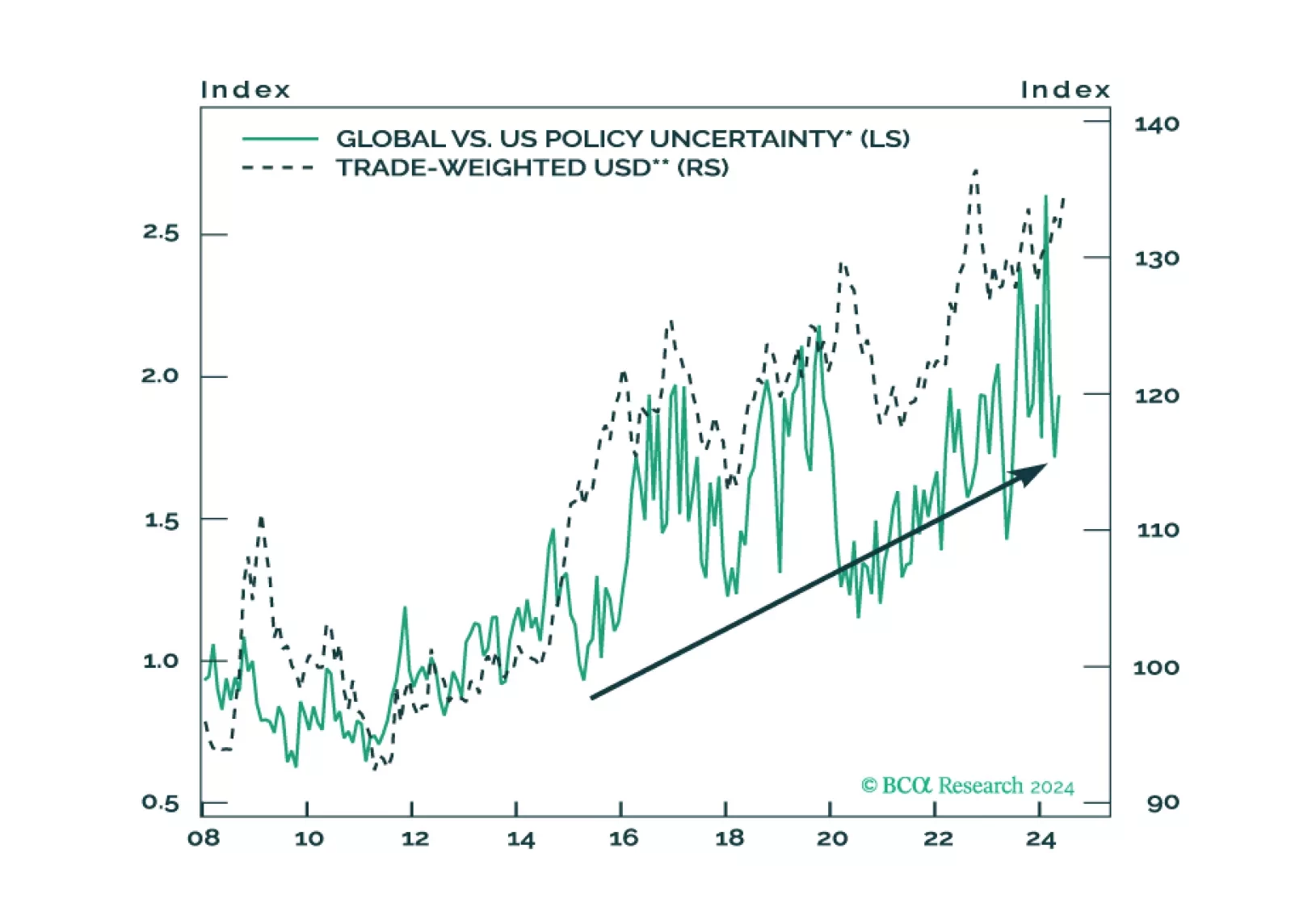

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

Two of Brazil’s ever-recurring demons have come back to haunt investors: public debt sustainability and persistent inflation. According to the latest report from our Emerging Markets Strategy (EMS) team, these troubles are set to worsen in the next six to…

According to BCA Research’s Foreign Exchange Strategy service, shrinking dollar liquidity often coincides with financial market crises and also leads to an appreciation in the currency, as the premium foreigners are willing to pay to get USD cash increases. …

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?

US dollar liquidity has been shrinking, which has important ramifications for global asset prices, including currencies. In this report, we delve into the process of dollar liquidity creation and the outlook for currencies over the next six-to-twelve months.

Since early 2023, the Philippine peso has depreciated by 8% versus the US dollar despite the country’s central bank pushing up real policy rates by 500 basis points. BCA’s Emerging Markets Strategy argues that raising policy rates has not helped the currency…

South African stocks, domestic bonds, and currency have all rallied since BCA’s Emerging Markets Strategy team upgraded South African assets last month following the formation of the new national unity government. The rally's persistence, however, will depend…

Japanese wage growth fell below expectations in May, expanding by 1.9% y/y versus consensus estimates calling for a 2.1% y/y increase. Although this marks an acceleration from April’s 1.6% y/y, that figure was revised down meaningfully from 2.1% y/y.…

The Chinese currency has been under considerable depreciation pressure due to capital outflows. Additionally, the economy is grappling with debt deflation and a balance sheet recession, conditions that typically call for lower interest rates and a weaker…