Currencies

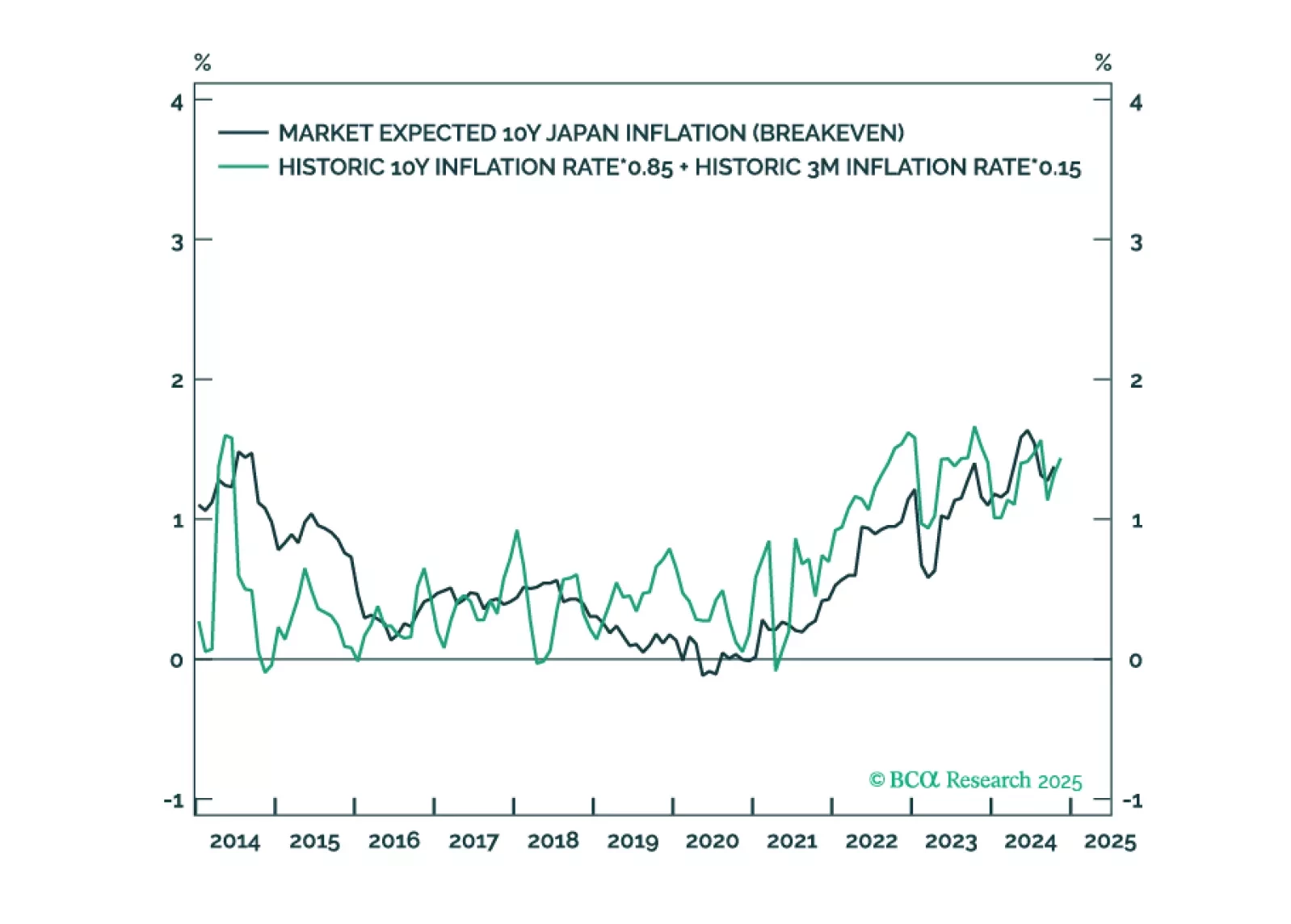

In most developed economies, rising inflation expectations will lift them further above the 2 percent target, limiting the scope for further interest rate cuts. But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target, removing the BoJ’s justification for its zero-interest rate policy. The normalisation of Japan’s monetary policy poses a big structural risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations. From a timing perspective though, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have collapsed. Plus: go tactically long copper.

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.