Corporate Bonds

Our Portfolio Allocation Summary for January 2025.

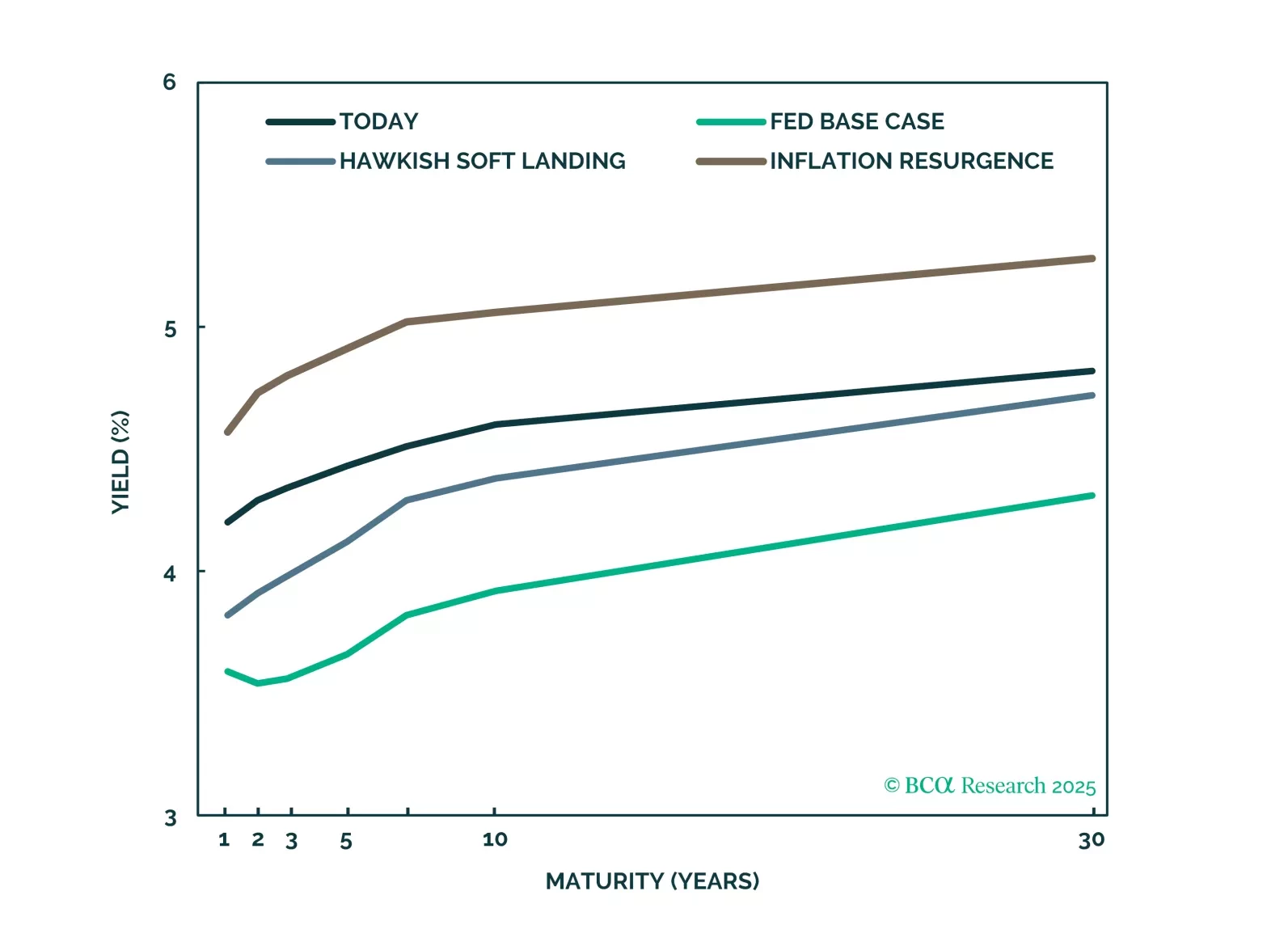

We forecast Treasury and corporate bond returns in three different economic scenarios. This report focuses on what returns might look like in a scenario where inflation is sticky and the Fed makes a hawkish pivot.

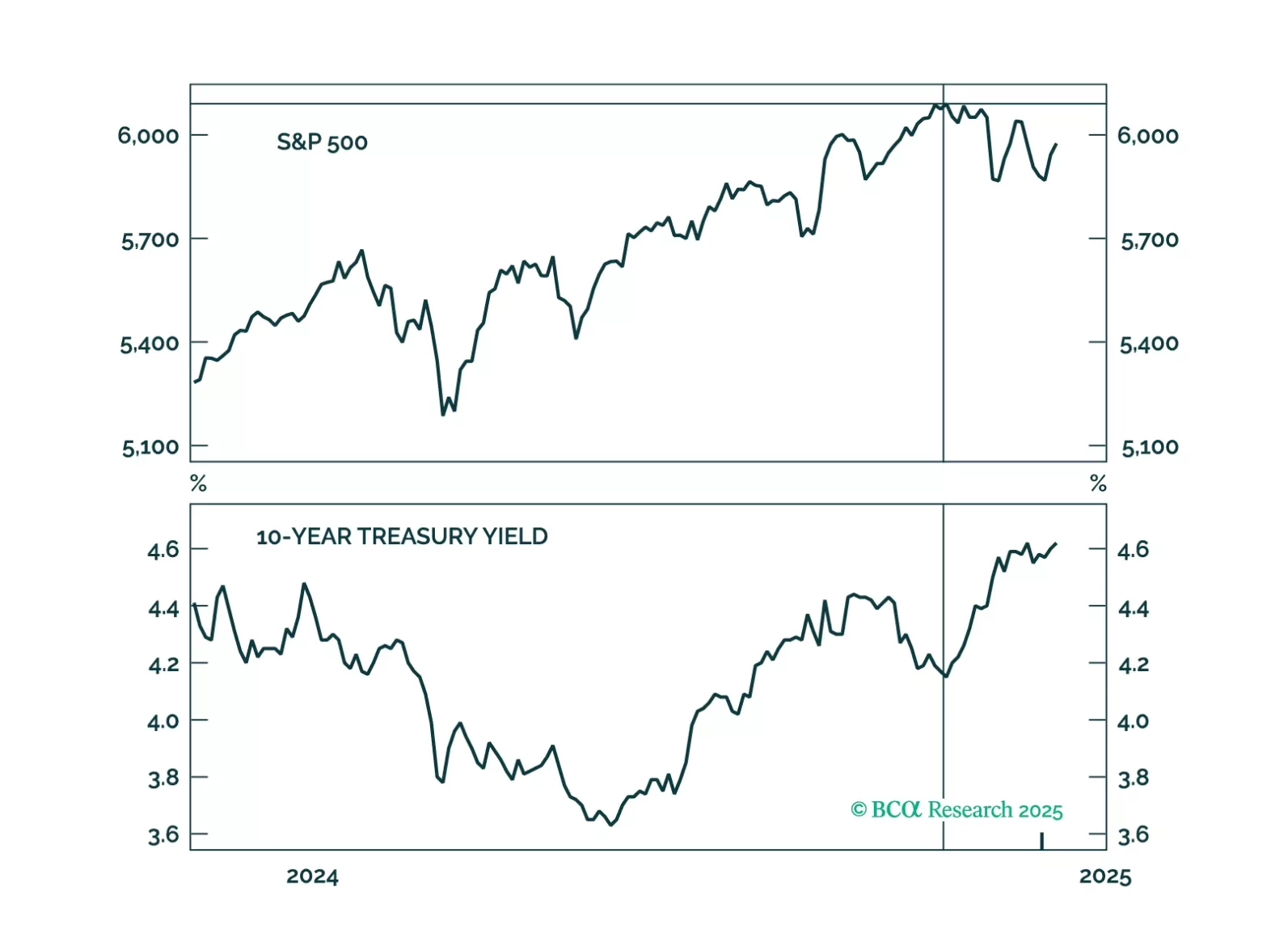

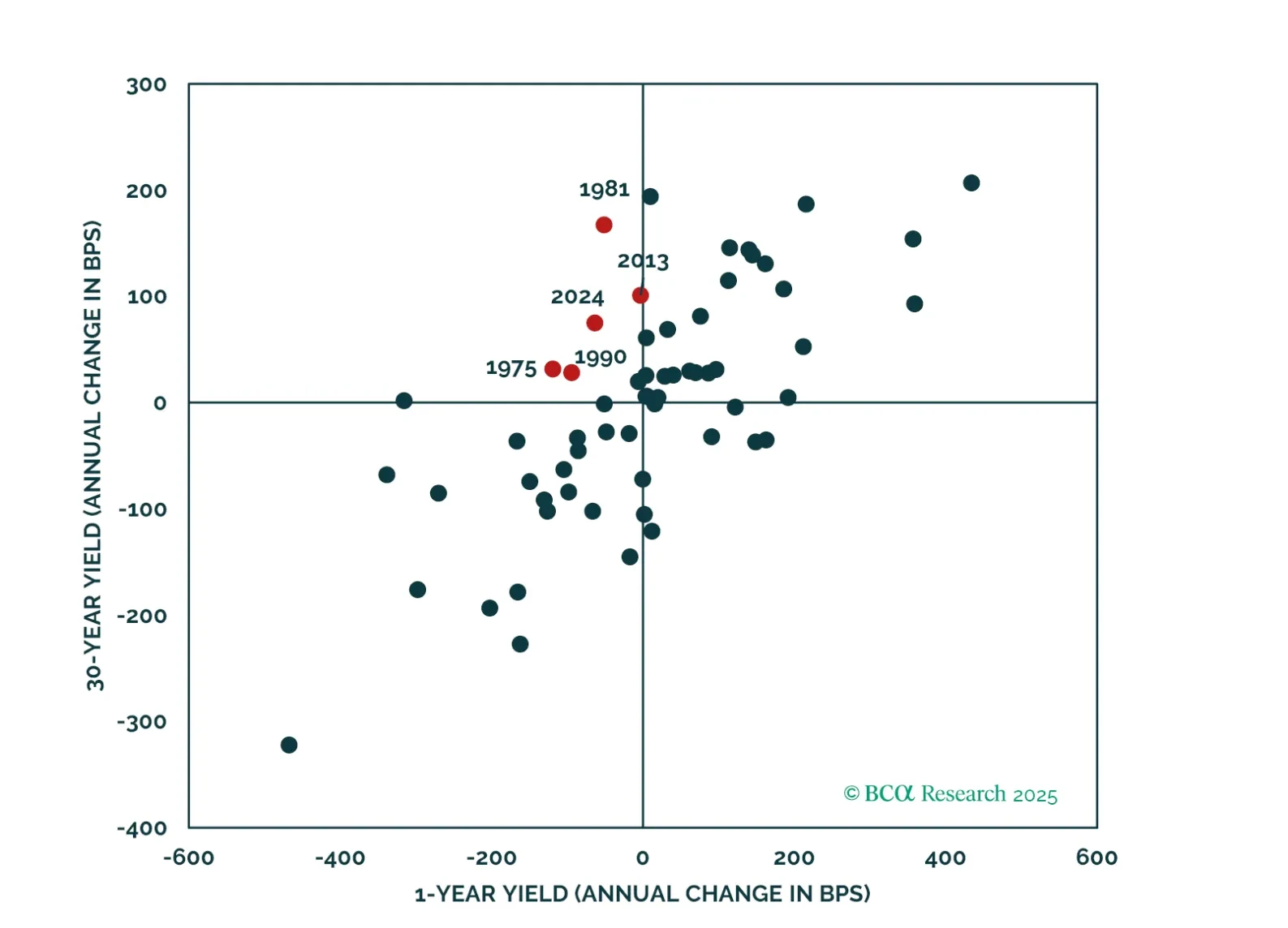

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.

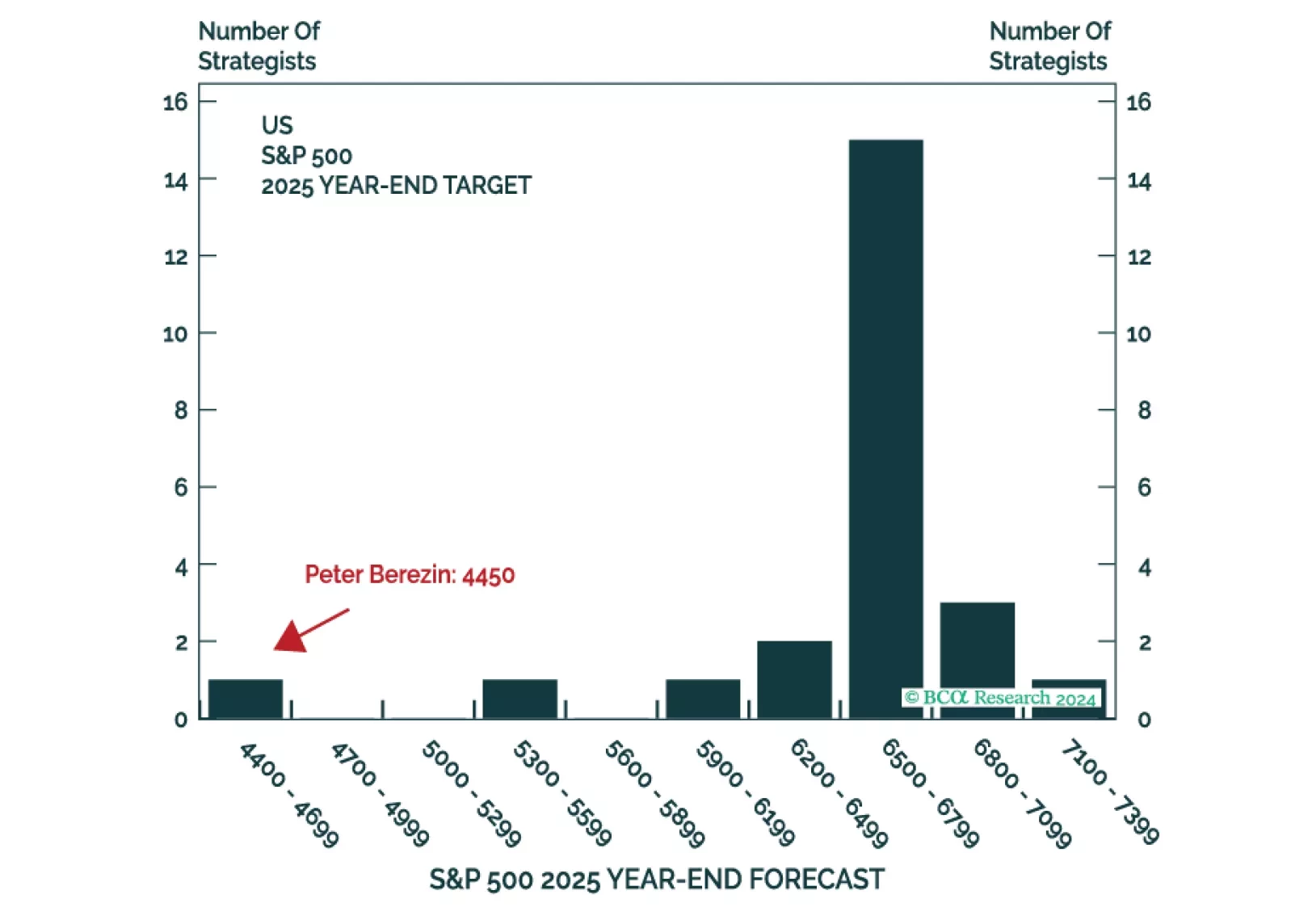

This is the time of the year when strategists are busy sending out their annual outlooks. Here on the Global Investment Strategy team, we decided to go one step further. Rather than pontificating about what could happen in 2025, we decided to harness the power of the multiverse to tell you what did happen (in at least one highly representative timeline).

Next week, please join me for a Webcast on Tuesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets.

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2025. We will be back in the first week of January with our MacroQuant Model Update.

We offer 5 key investment views for US fixed income markets in 2025.

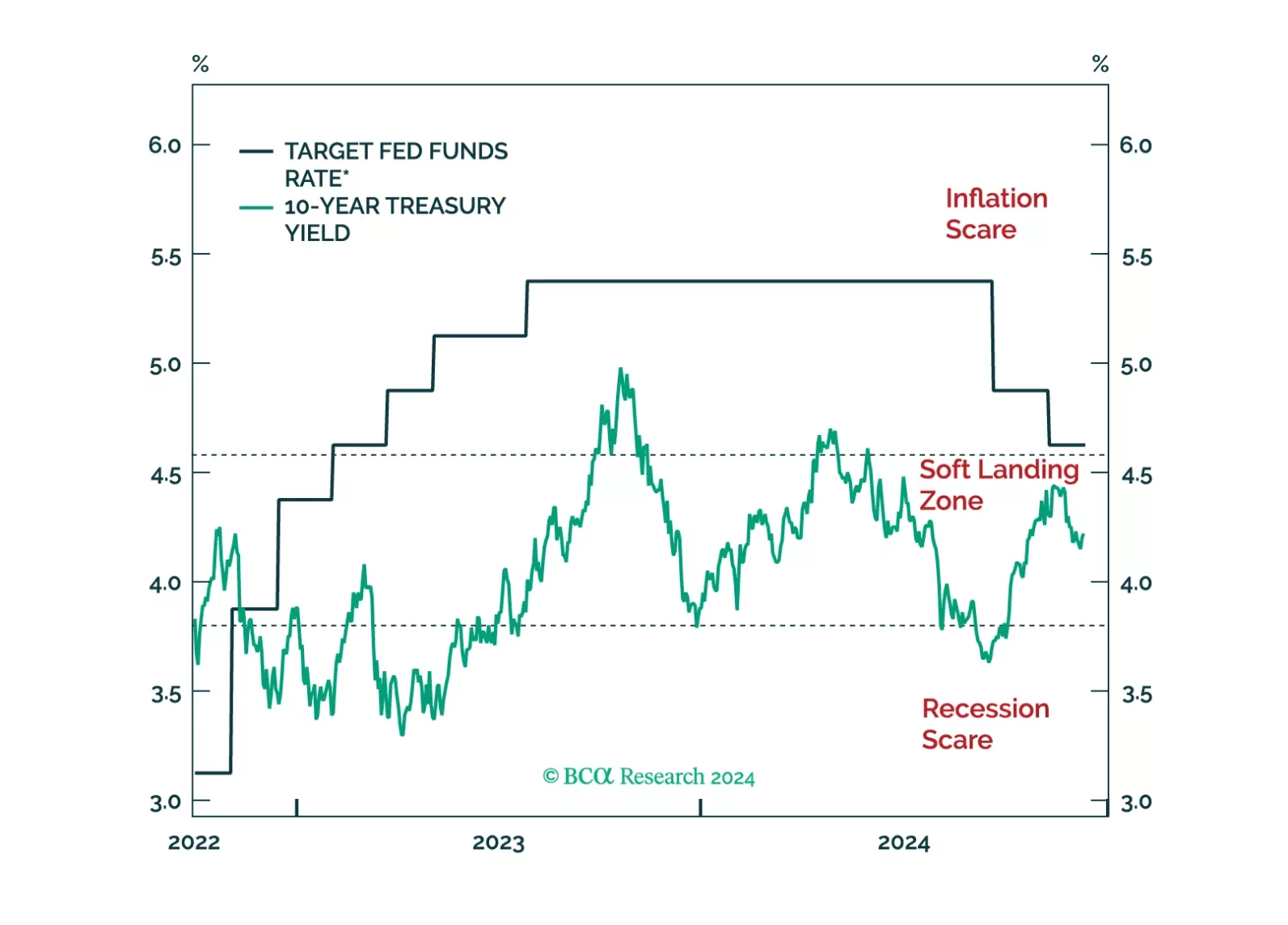

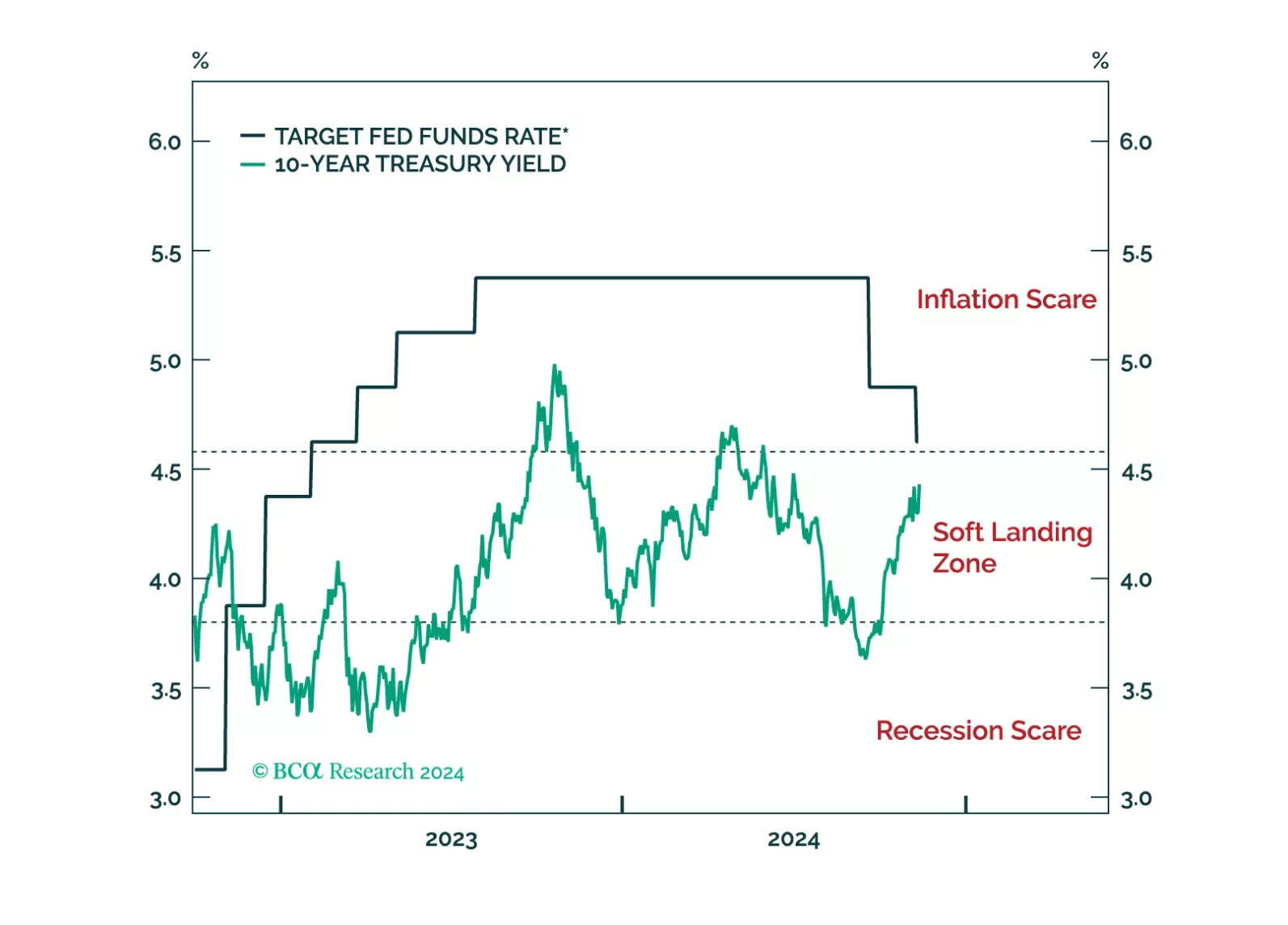

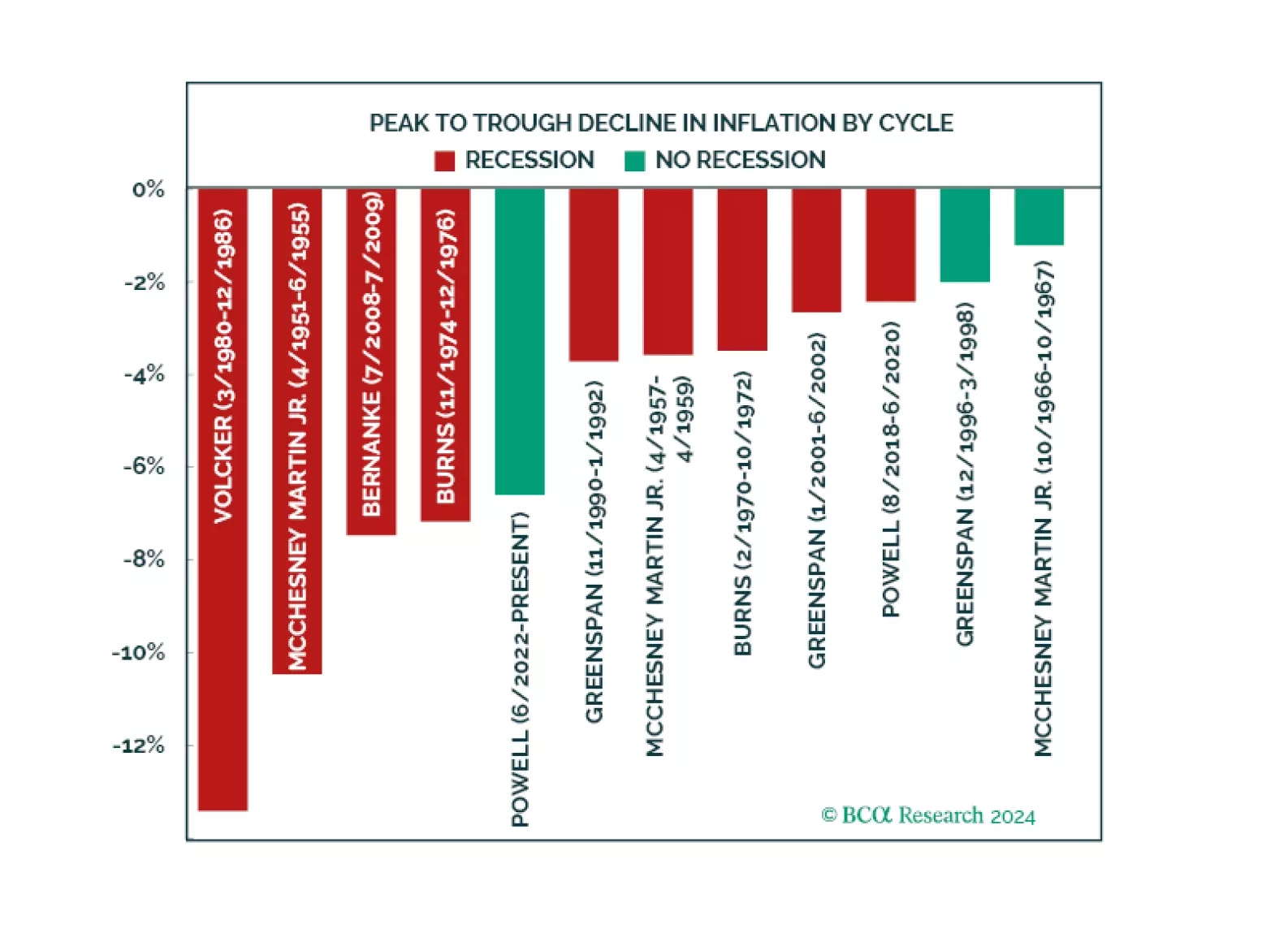

Can Powell achieve a soft landing? There are some indications he is doing it. We examine why our negative stance was wrong and analyze the four growth engines that kept recession at bay. Half of these forces remain while the other half have run out of juice. While this might be enough to keep the economy going, we maintain our defensive positioning. Equities have priced a very benign outcome. Meanwhile, rising rates in anticipation of a Trump win are pushing the economy away from the soft-landing path. We hedge the possibility of further upside in yields in case Trump gets elected by downgrading duration to neutral.