Corporate Bonds

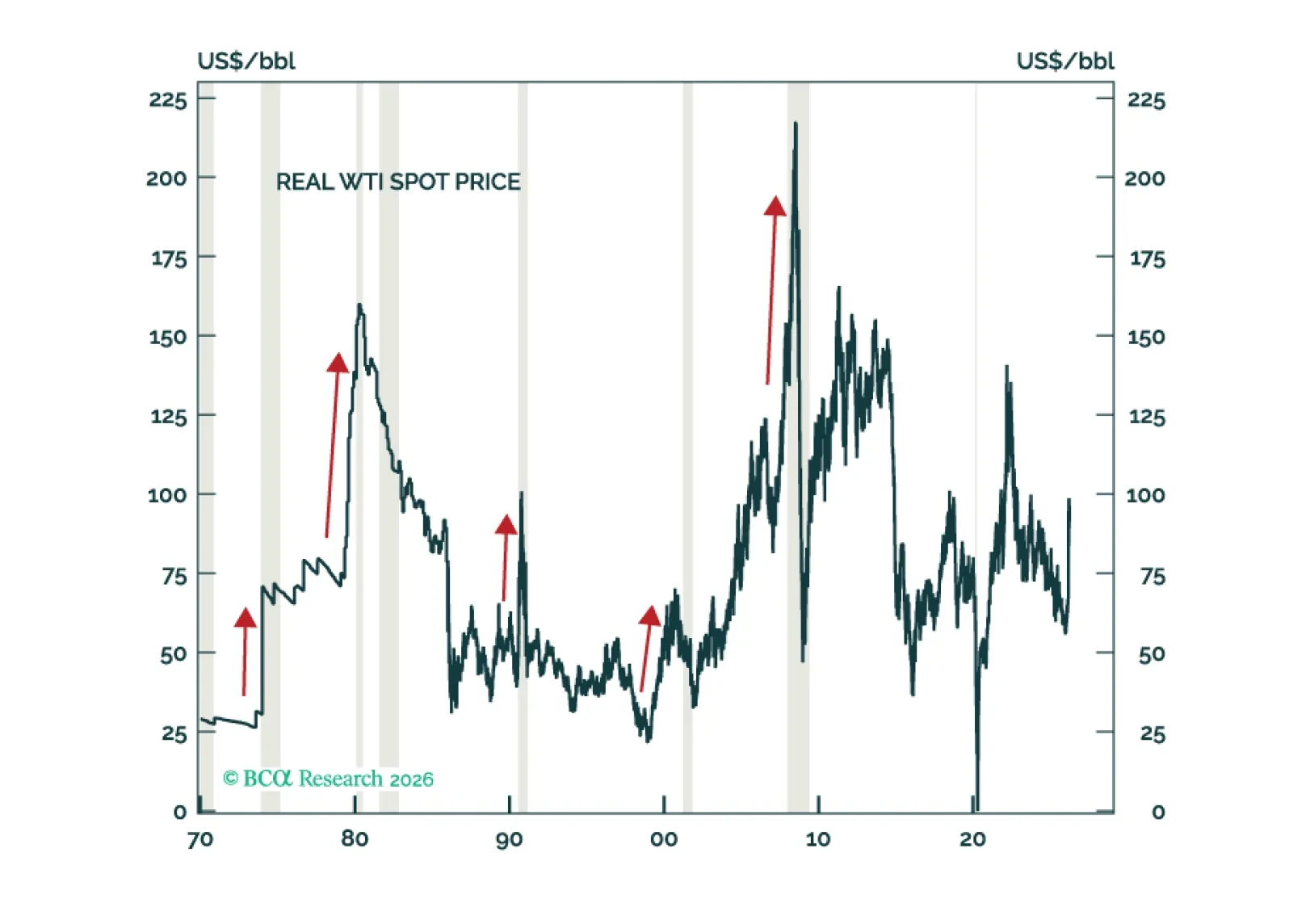

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

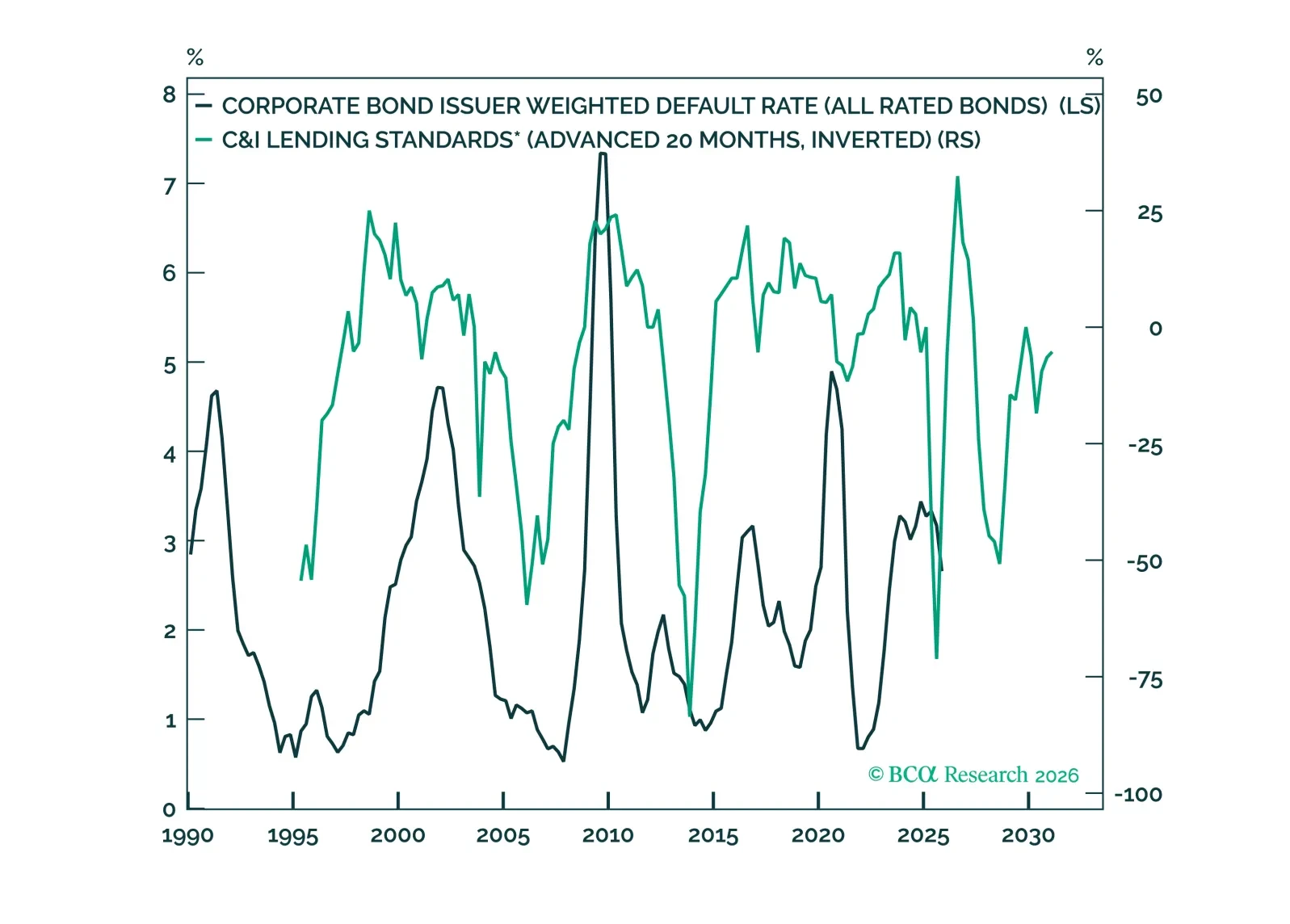

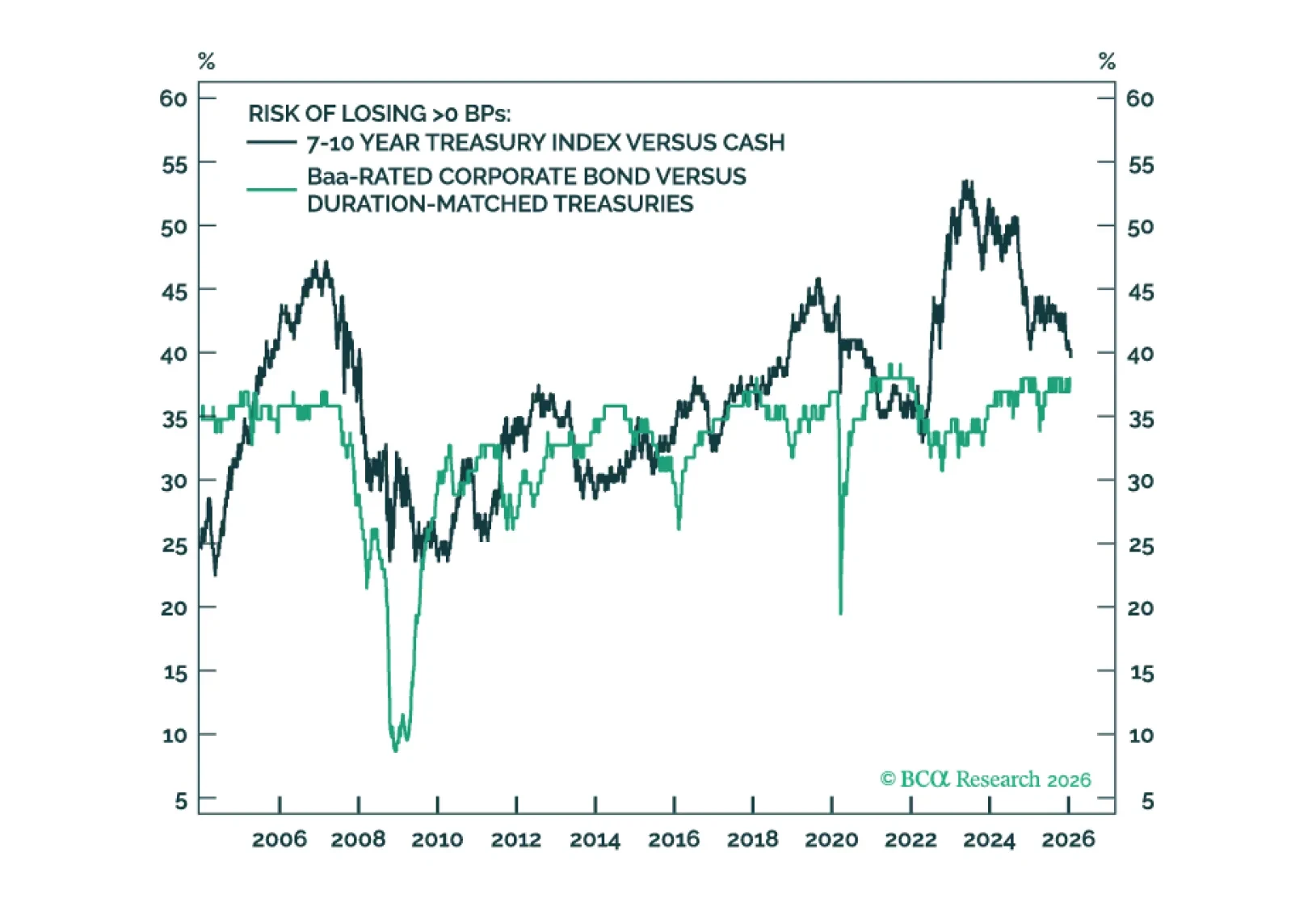

The turmoil in private credit is a wild card, but our traditional suite of credit cycle indicators does not point to an imminent spread-widening episode. We reiterate our benchmark weightings on Treasuries, investment-grade and high-yield corporate bonds.

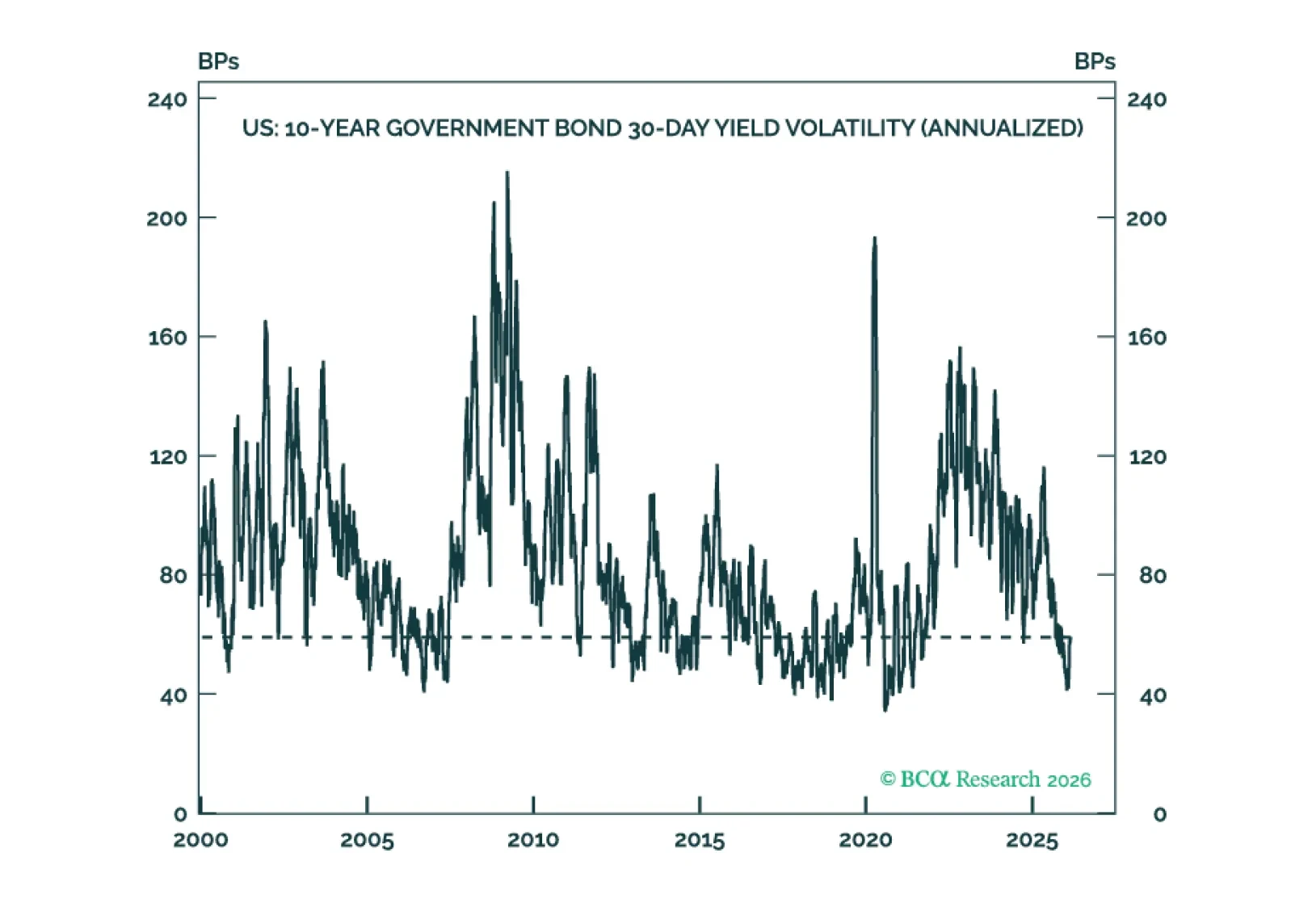

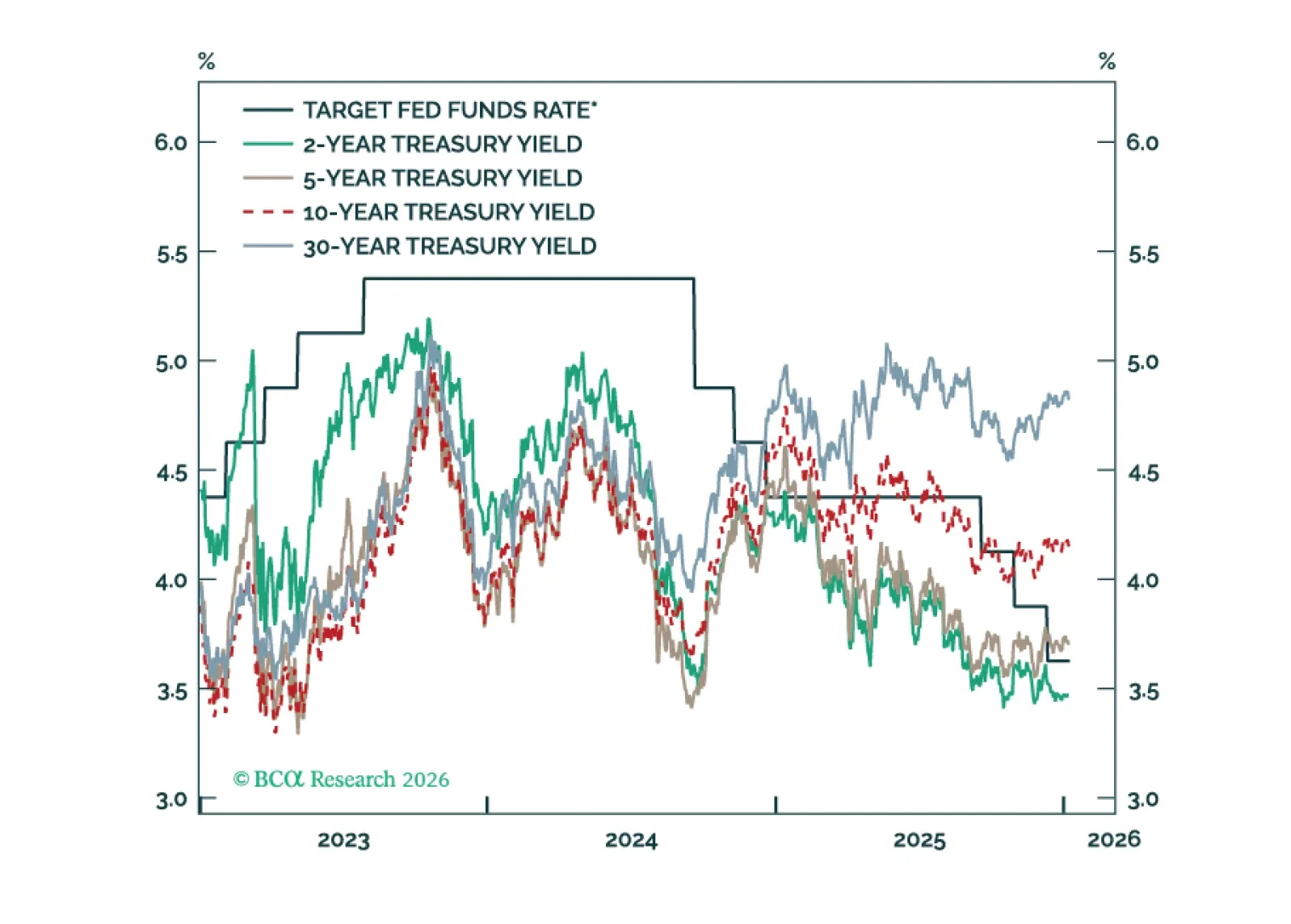

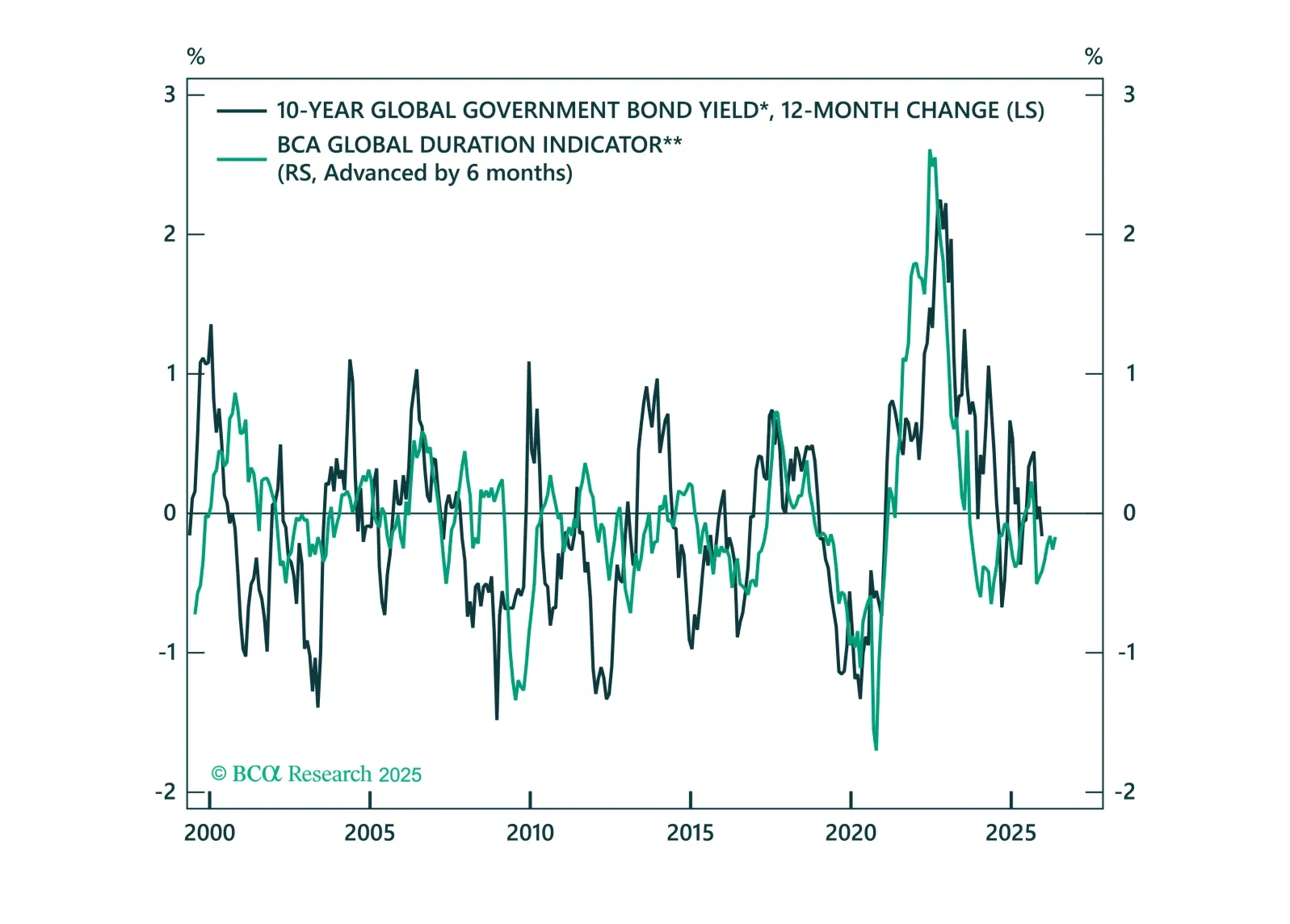

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

The 10-year Treasury term premium is now competitive with Baa- and Ba-rated credit spreads. Even without term premium compression, duration carry trades could outperform credit carry trades in a low rate vol environment.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.