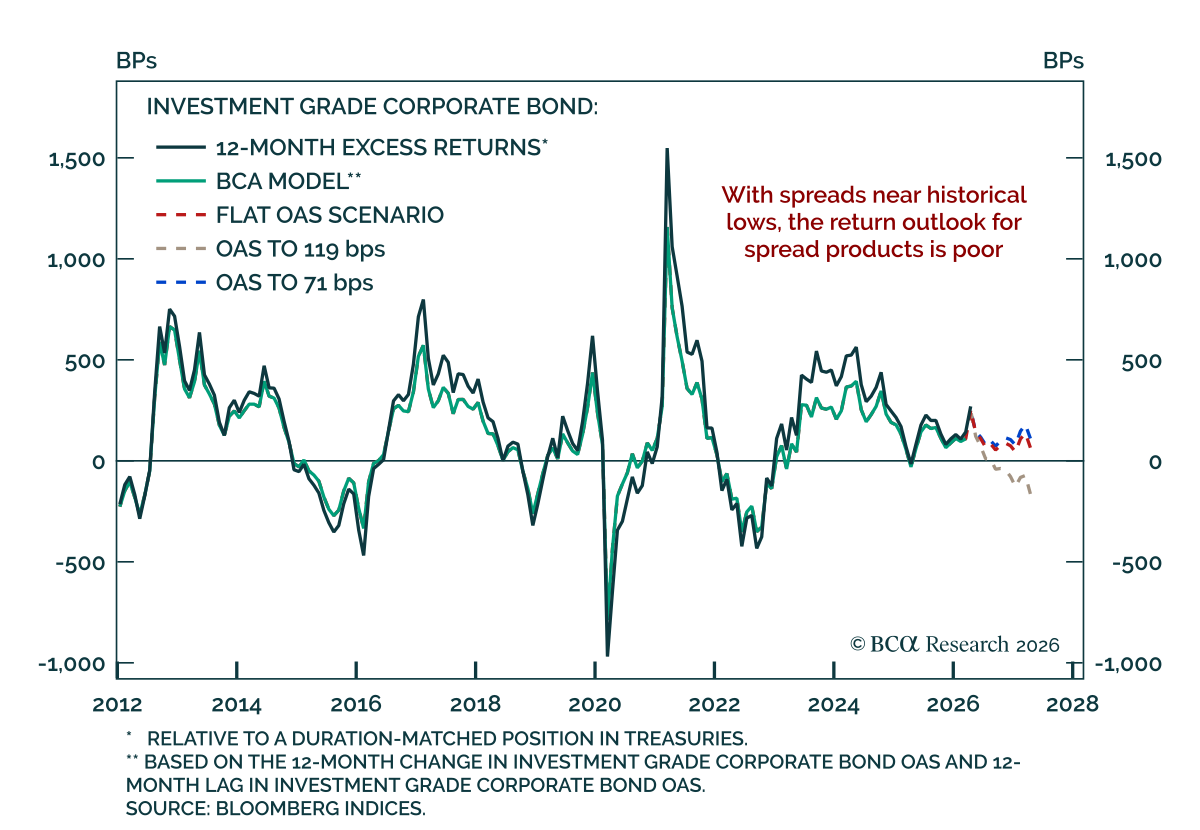

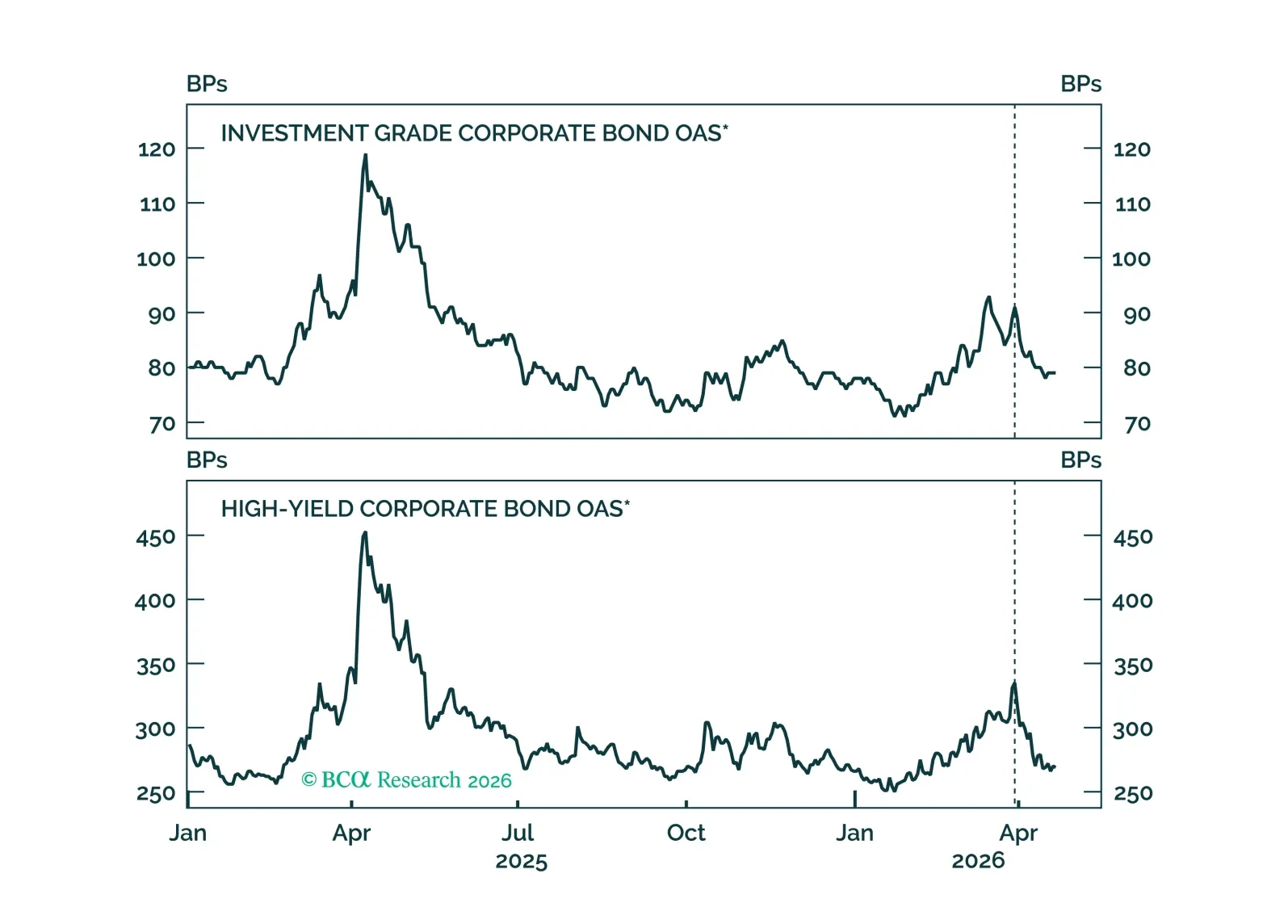

Corporate Bonds

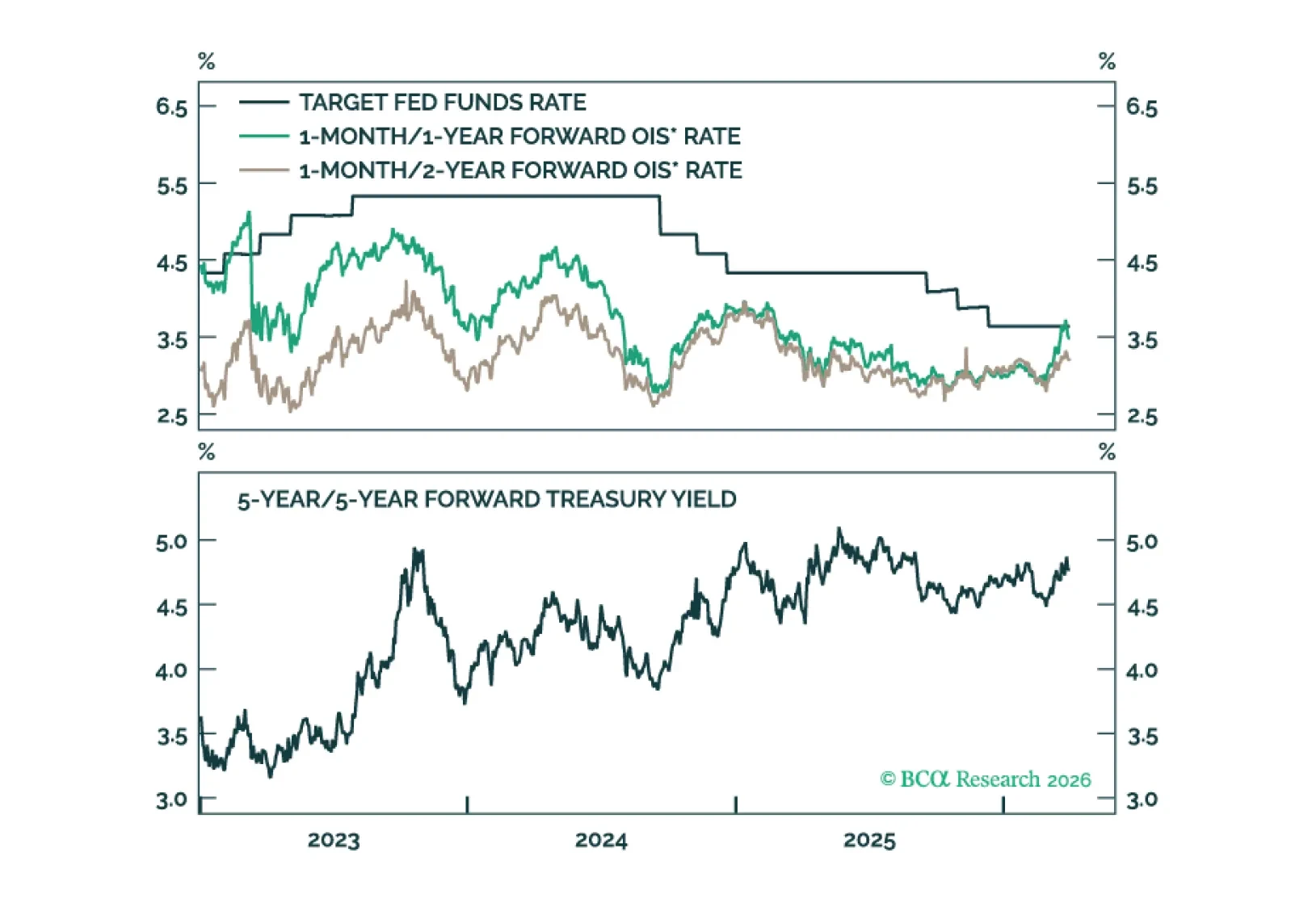

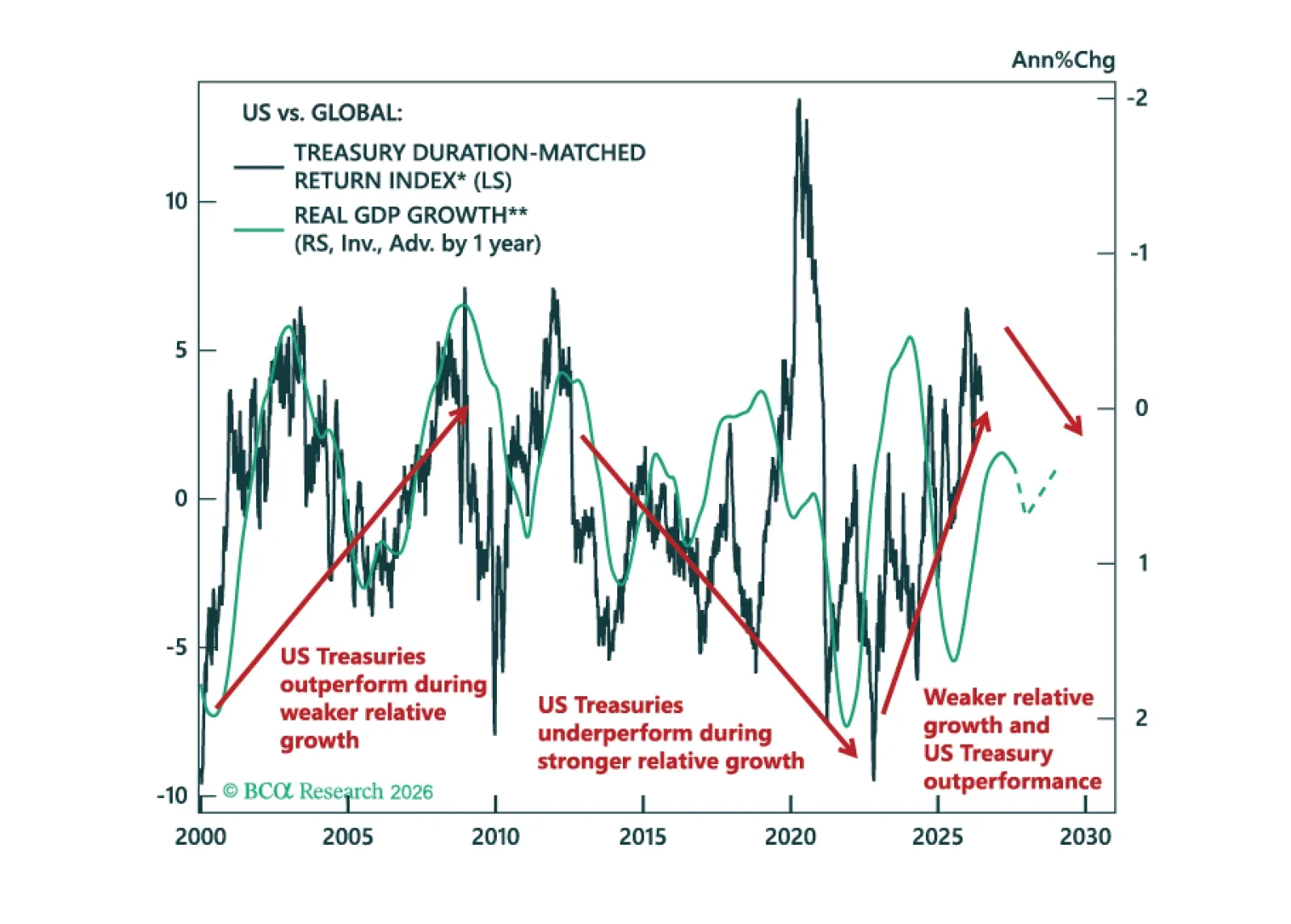

We review our Model Bond Portfolio performance for Q2 and look ahead as fixed income markets move beyond the US-Iran conflict, which is finding its kinetic equilibrium. Valuations and growth differentials are moving against continued US Treasury outperformance.

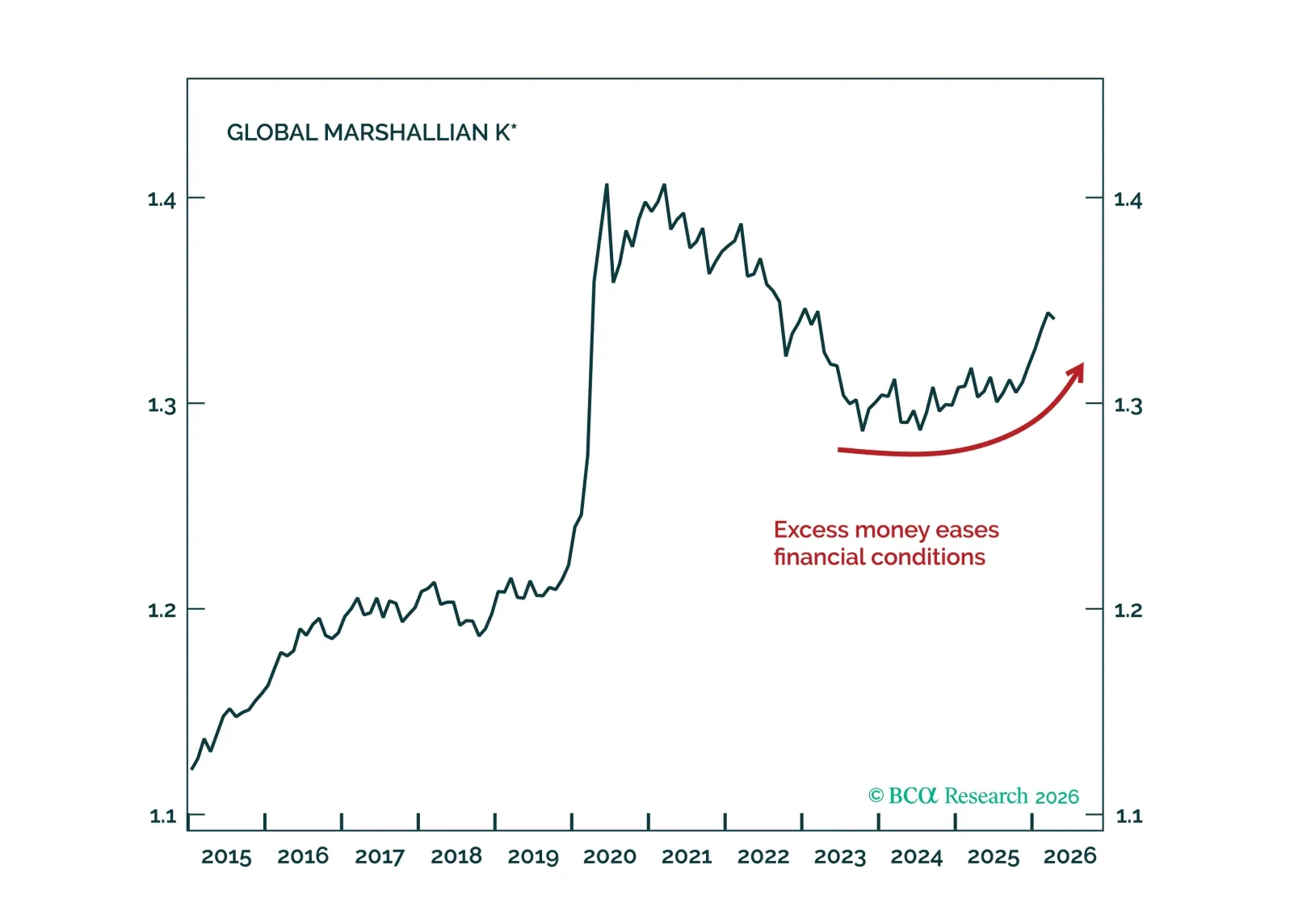

Markets keep buying the dip because liquidity remains plentiful. That buffer lasts through 2026; the bigger question is what happens when it thins in 2027.

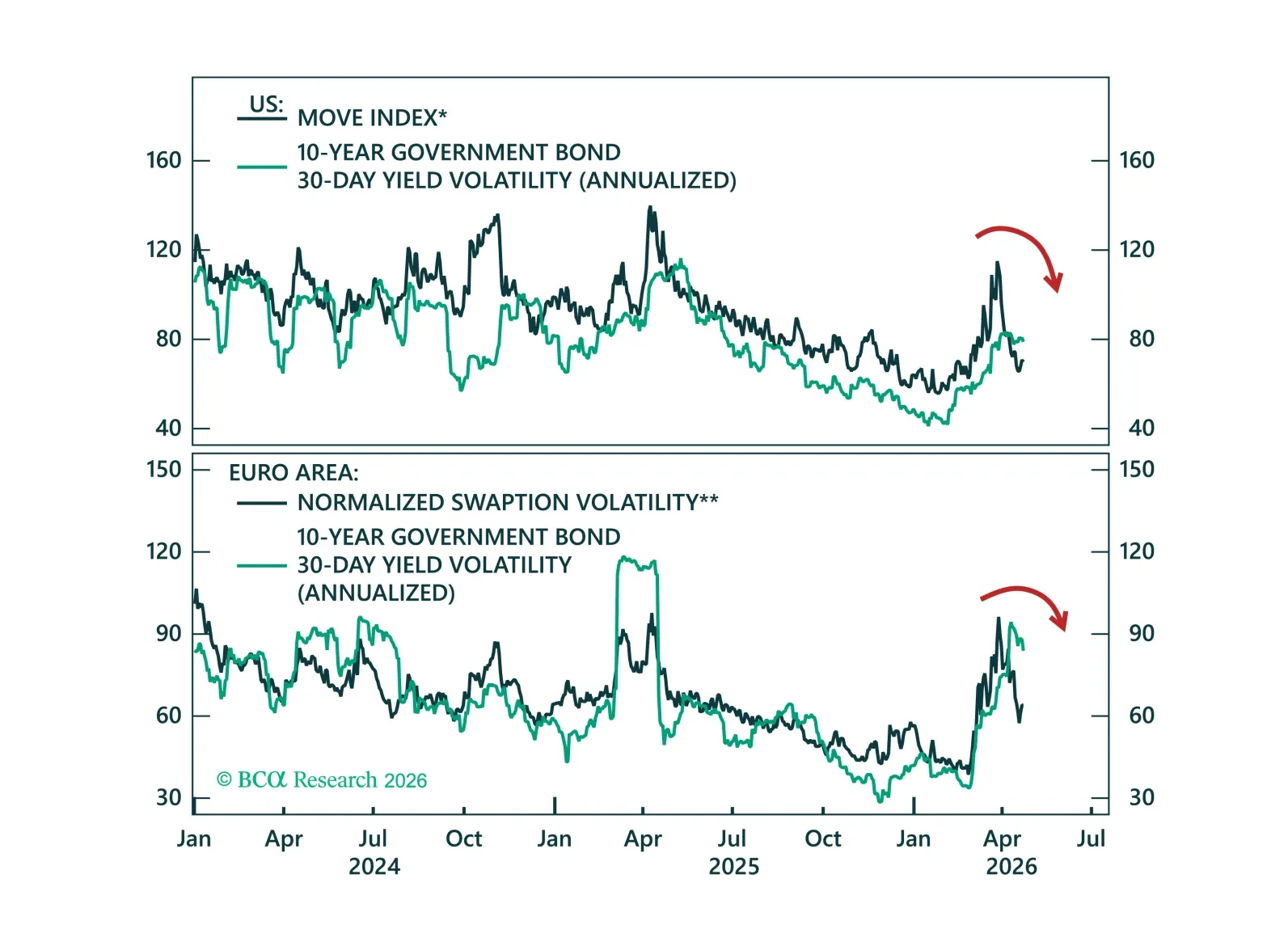

With central banks largely on hold, the return of a lower volatility environment is bringing carry trades back into focus. We outline the most attractive carry opportunities across global fixed income markets.

We recommend increasing exposure to spread product as the US economy transitions back into a low rate vol regime.

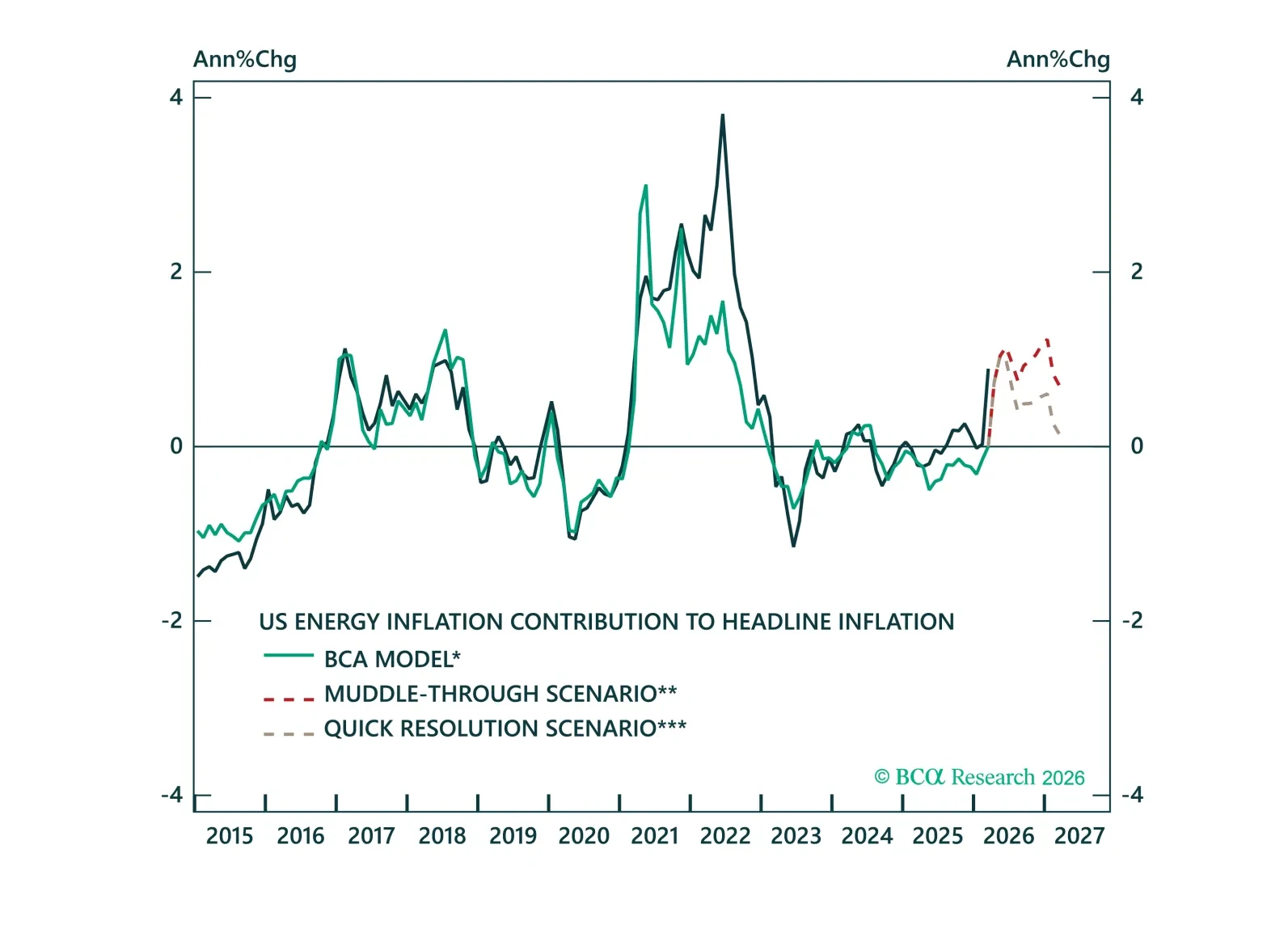

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.