Consumer

Chinese stocks are experiencing their longest rally since the country’s exit from Covid restrictions over a year ago. The MSCI Onshore and Investable indices (in USD terms) have gained 15.8% and 9.1% respectively since February 5th, with the former…

According to BCA Research’s China Investment Strategy service, a very substantial PSL financing scheme for housing, a large LG and LGFV debt swap, and considerable fiscal transfers to households—or a combination thereof— might lead them to upgrade their…

Results of the New York Fed’s Survey of Consumer Expectations showed an uptick in medium- and long-term inflation expectations in February. Specifically, the three-year ahead measure rebounded from a record low of 2.4% to 2.7% and the five-year ahead gauge…

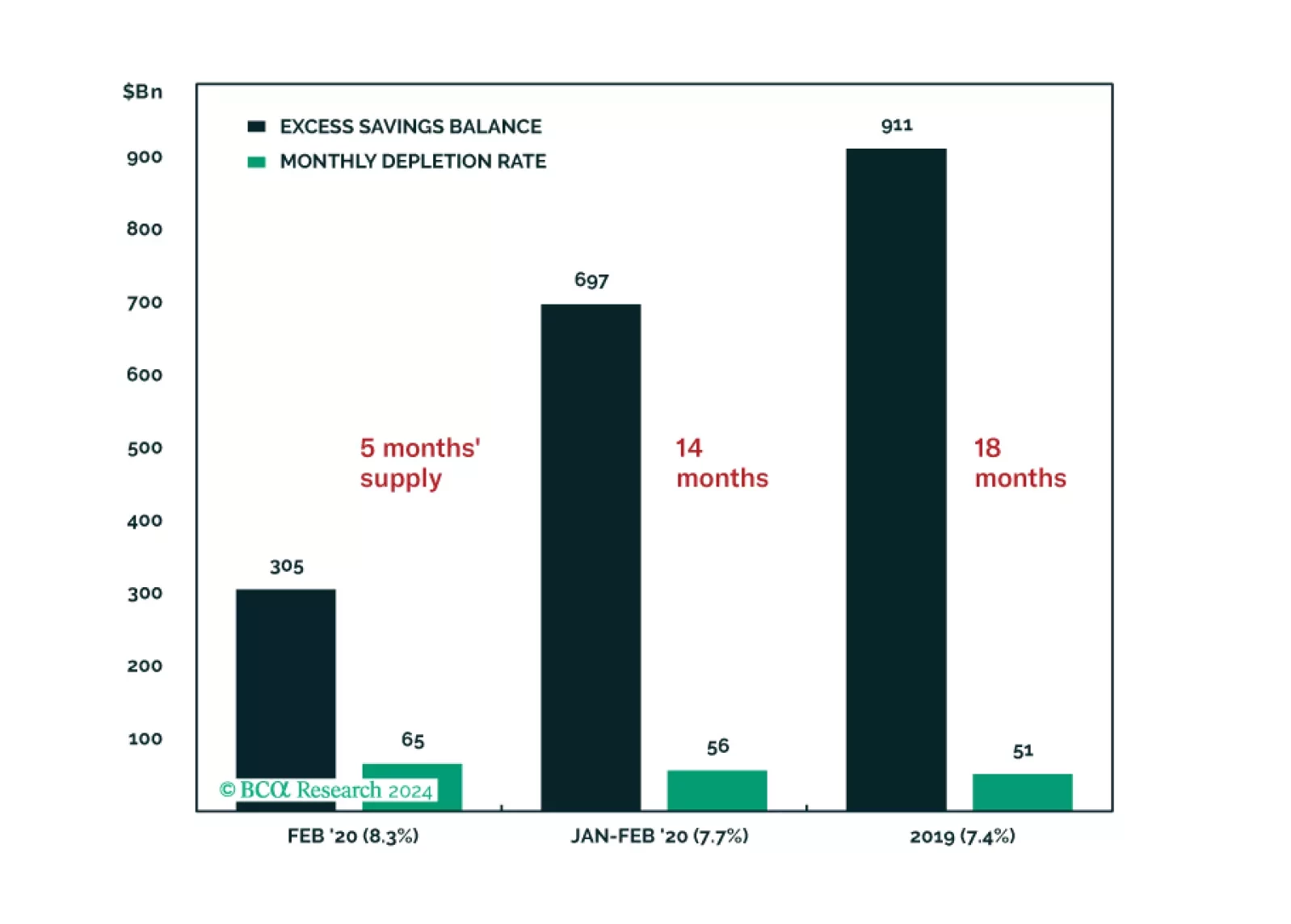

Our US Investment Strategy service examines the state of consumer finances in the context of their view that a recession will materialize this year with a double-digit peak-to-trough decline in S&P 500 earnings expectations. They expect the…

Data out of Norway is becoming increasingly positive, and there is a strong investment case to be made for the country, with bullish implications for both equities and the currency: Retail sales remain robust and are catching up to the improvement we…

China’s NBS PMI release indicates that the Chinese growth is stabilizing at a low level. The composite PMI came in at 50.9 – unchanged from January. The stabilization was led by the non-manufacturing sector though both the manufacturing and non-manufacturing…

Economic sentiment has improved since the December FOMC meeting, with positive momentum extending into February. The chart above neatly summarizes the impact that the Fed’s projected easing has had on sentiment, both on “Wall Street” and “Main Street”. The…

We feel as good about spurning the soft-landing narrative today as we did about spurning the recession narrative a year ago, but we are not giving into complacency. This week’s report looks at two key ways that we may be getting it wrong: by underestimating households’ asset support and the labor market’s durability. We remain tactically neutral but continue to look for opportunities to turn defensive.

US GDP growth for Q4 was revised lower from 3.3% to 3.2% annualized, driven by a downward revision to private inventory investments (now detracting 0.27 points from a previous 0.07 contribution to GDP). However, consumer spending grew at a faster pace than…

The US Conference Board’s February Consumer Confidence release surprised to the downside. The index decreased to 106.7 from a downwardly revised 110.9, disappointing expectations it would improve to 115.0. Consumers’ assessment of both the present situation…