Consumer

The Conference Board’s gauge of US consumer confidence came in at 104.7 in March – broadly unchanged from a downwardly revised 104.8 in February and below expectations of an improvement to 107. The Expectations Index deteriorated from 76.3 to 73.8, while…

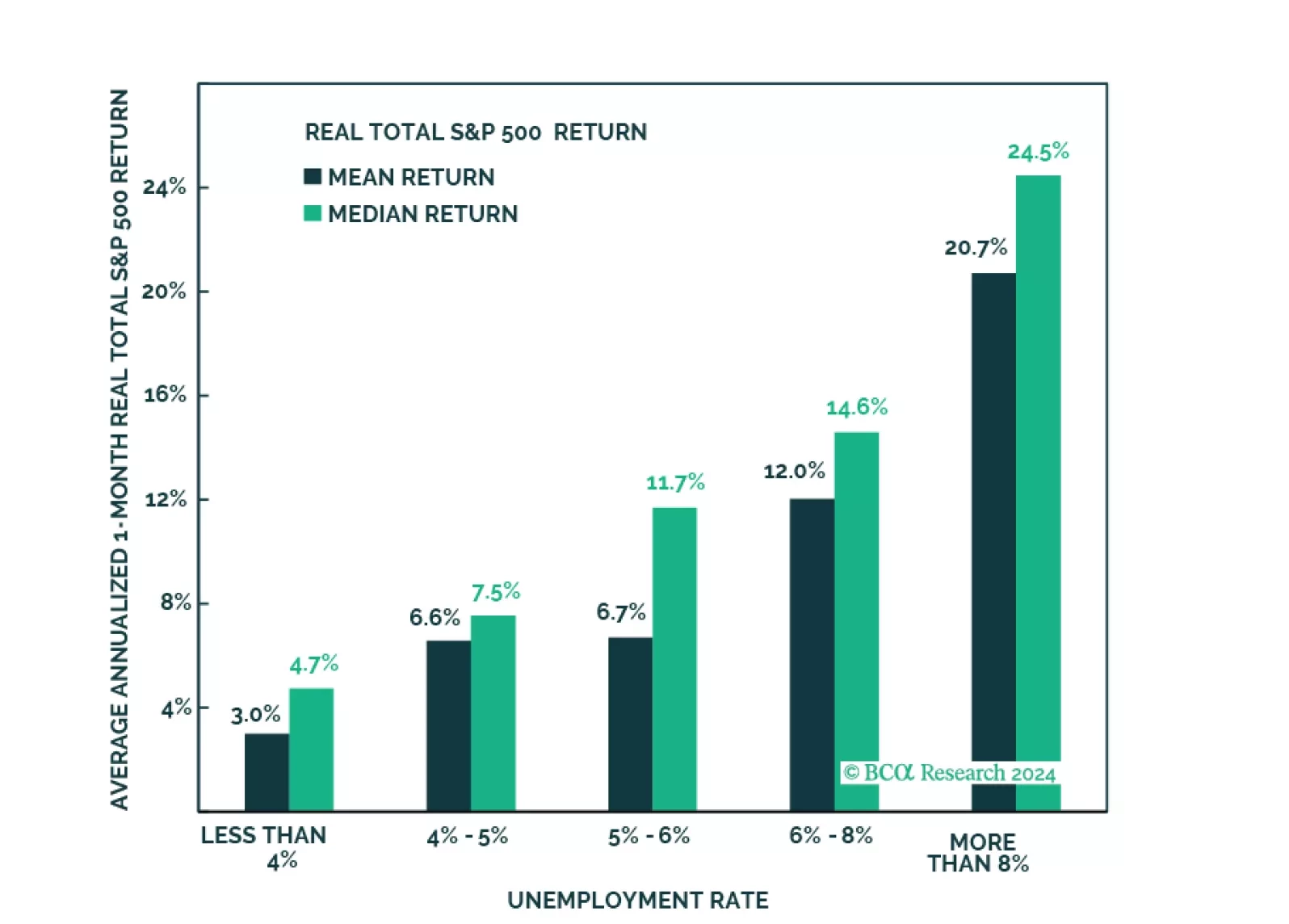

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

The latest batch of economic data out of the UK suggests that economic conditions have recently stabilized. The flash Manufacturing PMI rose by a stronger-than-anticipated 2.4 points to a 20-month high of 49.9 in March – only a hair below the 50 boom-bust…

The 2.1-point increase in Germany’s Ifo Business Climate index in March brought it to a 9-month high of 87.8 and beat expectations of a more muted rise to 86.0. Both current economic conditions (+1.2 to 88.1) as well as expectations for the next six months…

The steepening of the yield-curve powered the outperformance of the S&P 500 Financials relative to the overall market since the spring of 2023 banking crisis. This sector returned 30.1% over this period, against 27.3% for the S&P 500. Our US Equity…

According to BCA Research’s Emerging Markets Strategy service, although certain Chinese industries and individual EM economies are growing briskly, overall EM growth will remain tepid, with risks skewed to the downside. The fiscal stimulus announced during…

According to BCA Research’s China Investment Strategy service, the adjustment in China’s real estate sector is not over. Odds are that the property market will contract for the fourth year in a row. The property market indicators continue to paint a grim…

Indicators continue to point to resilient US housing market dynamics. The NAHB Housing Market Index increased for the fourth consecutive month to an 8-month high of 51 in March, beating expectations it would remain unchanged at 48. Increases across all three…

According to BCA Research’s Global Asset Allocation service, the impact of the global savings glut is among the four structural trends that will drive EM debt going forward. As an asset traditionally further out on the risk curve, EMD is sensitive to…

In a recent Insight we highlighted that the selloff in the price of iron ore – which is down 25.4% year-to-date – is sending a pessimistic signal on China’s economy, suggesting that the current rally in Chinese stocks is unlikely to persist over a cyclical…