Consumer

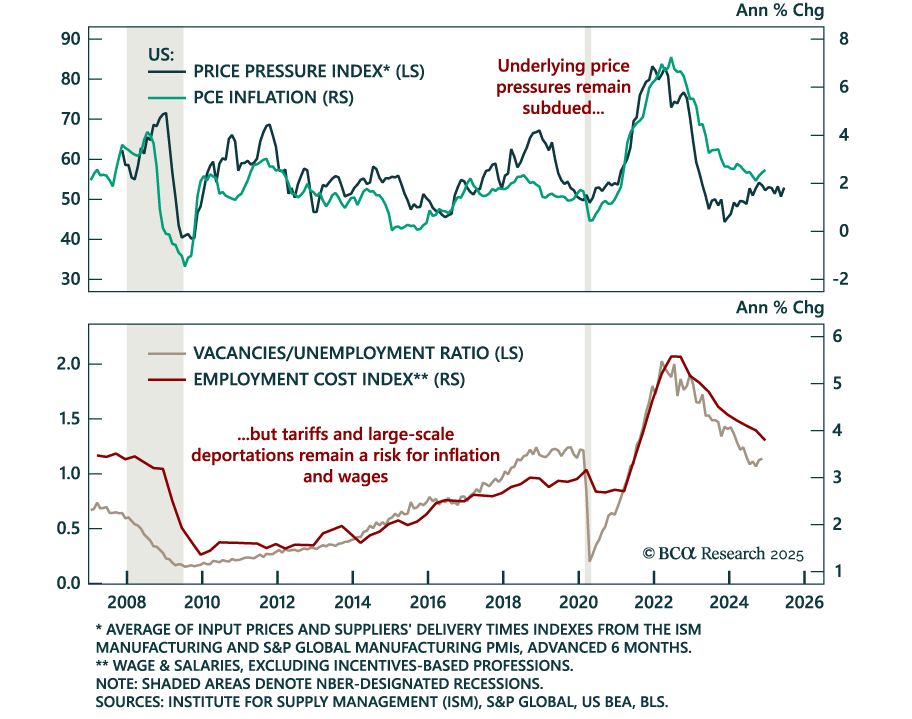

December PCE inflation was in line with expectations, with headline inflation at 0.3% m/m (2.6% y/y) and core at 0.2% m/m (2.8% y/y). The Q4 employment cost index also came in line with expectations at 0.9% q/q. Inflation is currently running below the Fed’s…

The January Tokyo CPI came in stronger than expected, with headline inflation accelerating to 3.4% y/y from 3.0%, and “core core” (ex. fresh food and energy) accelerating to 1.9% from 1.8%. The jobless rate also decreased 0.1% to 2.4% in…

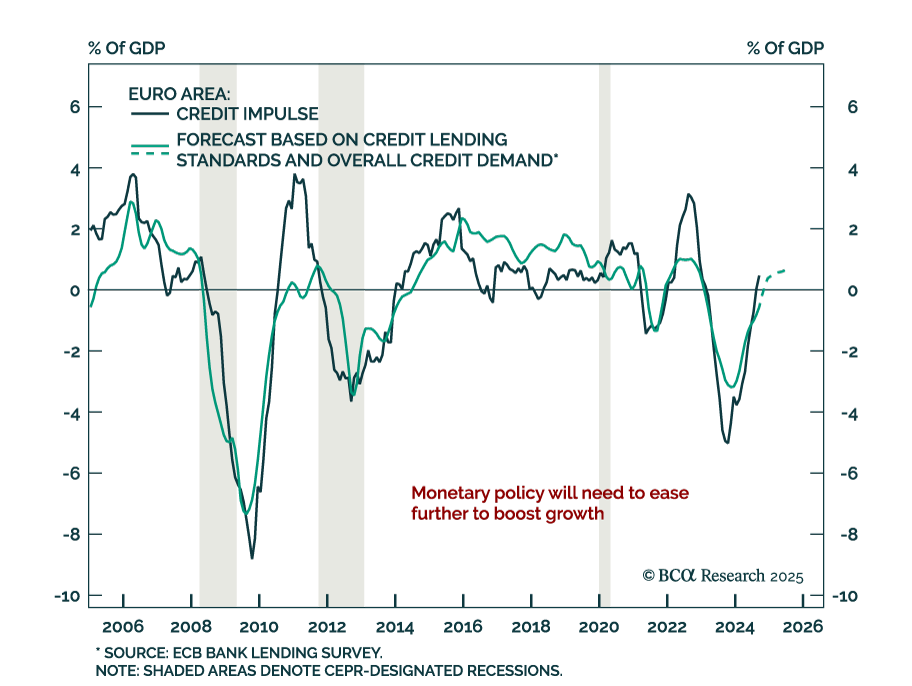

The January 2025 ECB bank lending survey saw a net tightening of credit standards in Q4 2024. Credit standards were tightened for business and consumer lending, and were roughly unchanged for home mortgage loans. Banks expect further tightening across all…

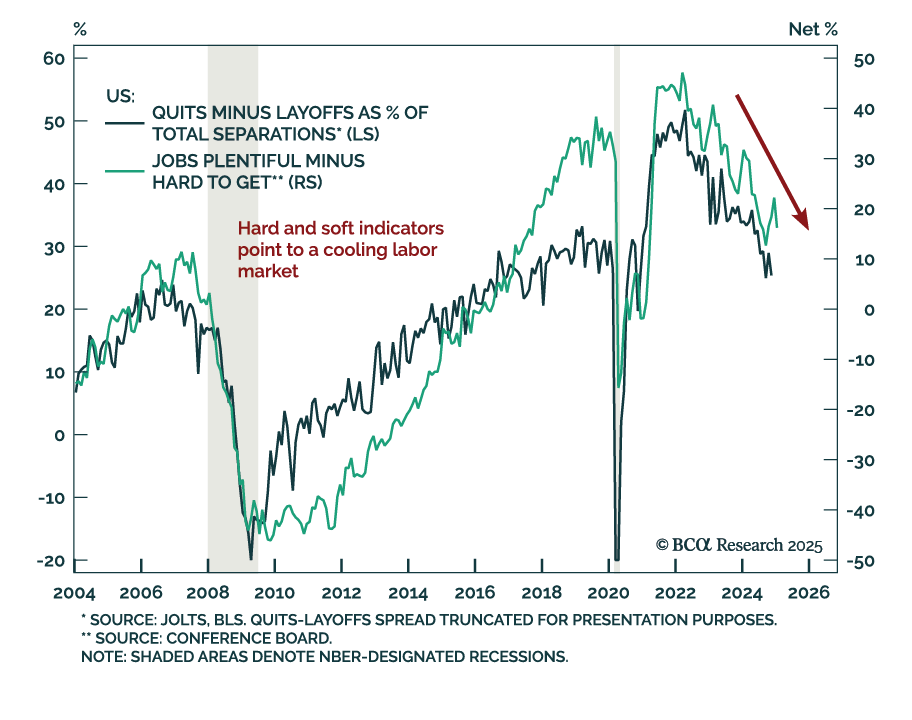

The January Conference Board Consumer Confidence index missed estimates, decreasing to 104.1 from an upwardly-revised 109.5 in December. The decrease was driven by both the present situation and expectations subcomponents. The labor differential, the…

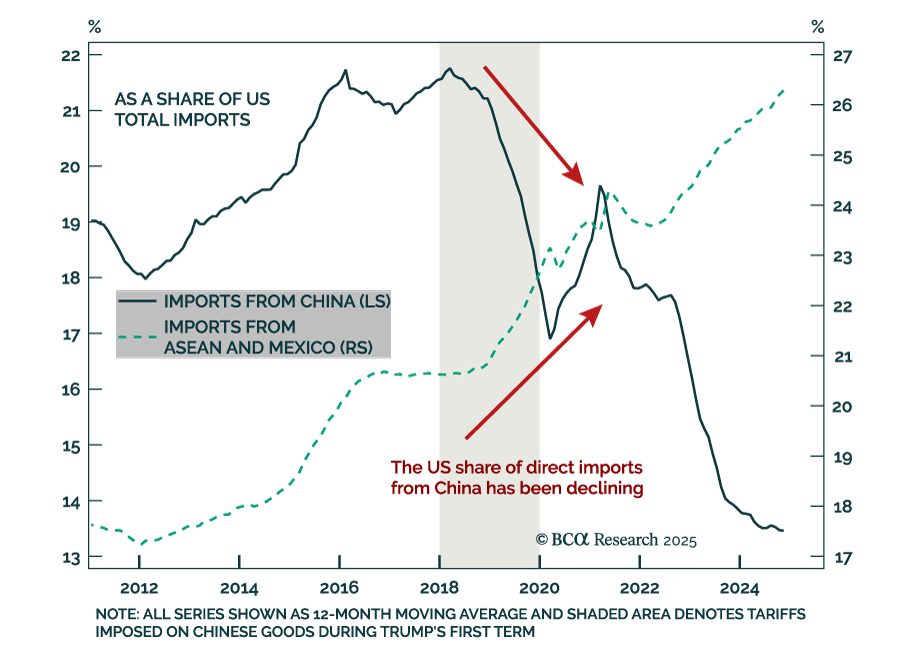

Our China Investment Strategy team explored how the costs of higher tariffs might be distributed among foreign suppliers, US importers, and consumers. The inflationary impact of new US tariffs is likely to remain modest unless President Trump imposes…

The January Ifo Business Climate index for Germany beat estimates, increasing to 85.1 vs. 84.7 in December. The increase came from the survey’s current assessment component, which increased a full point, as the expectations component missed estimates and…

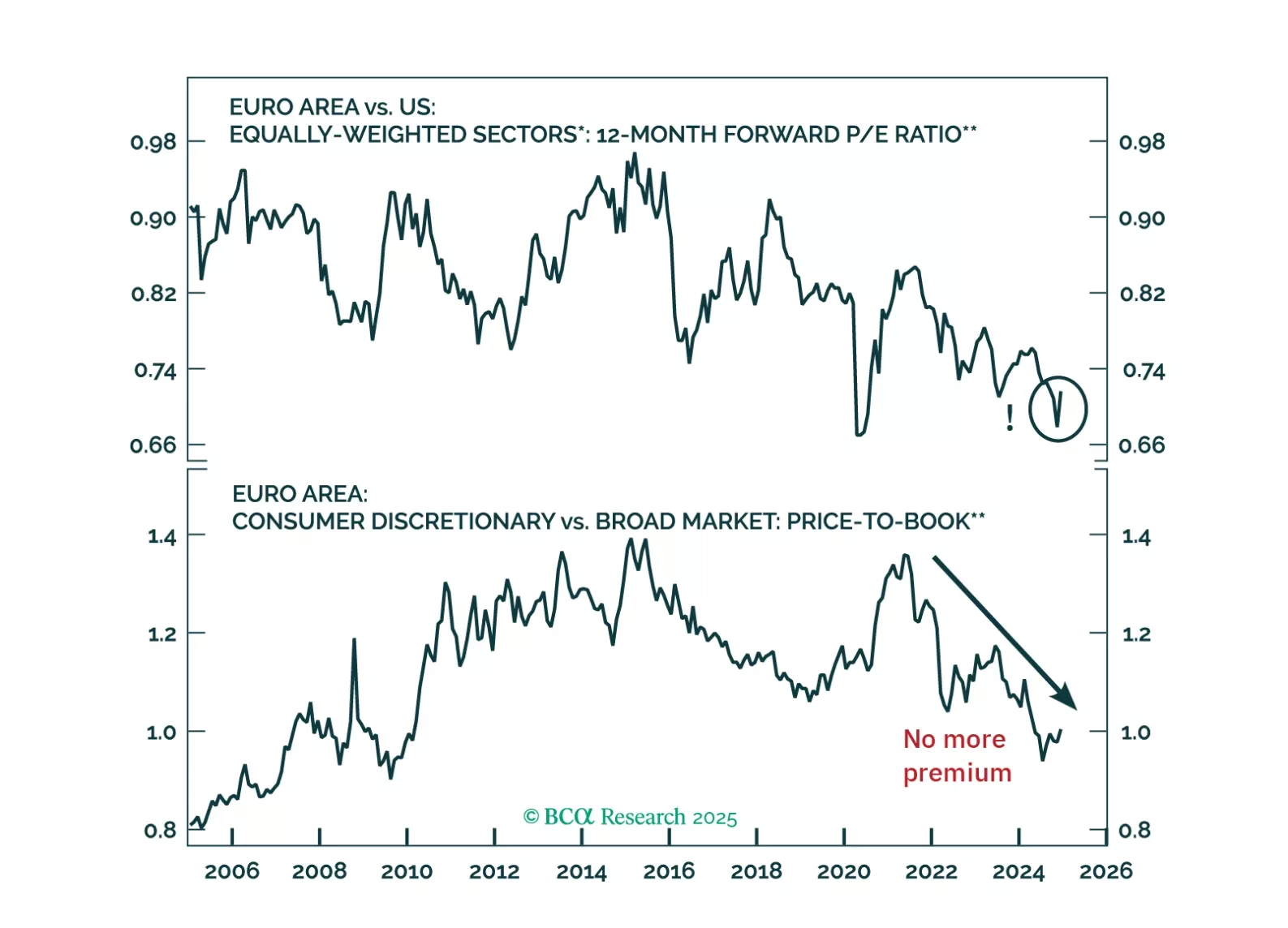

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

US December housing data was strong, with housing starts printing above estimates at 1.49m, an acceleration from an upwardly-revised 1.29m in November. Building permits also surprised positively at 1.483m, but still decreased from 1.493m a month prior. The…

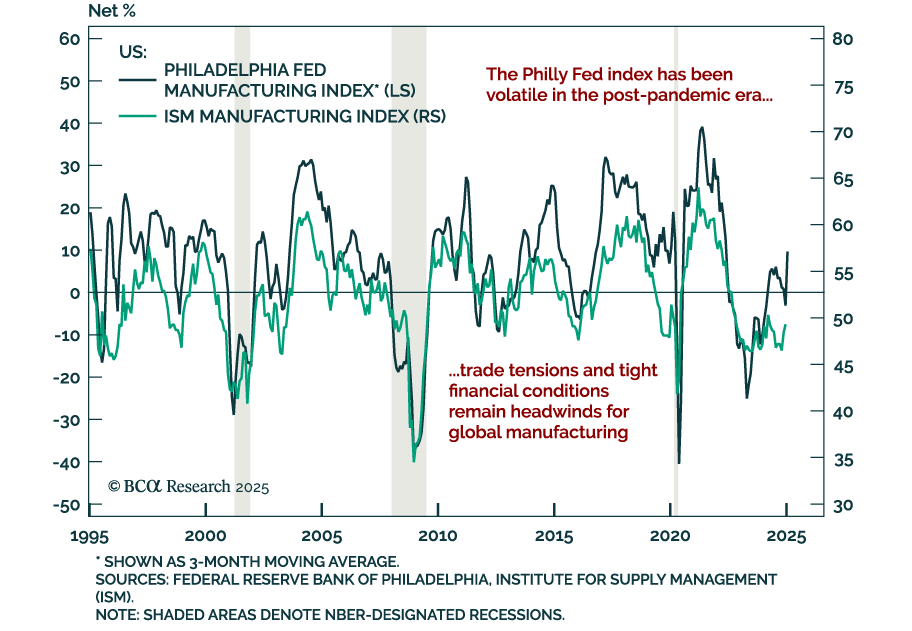

The January Philly Fed Manufacturing index blew past estimates, soaring to 44.3 vs. a revised 10.9 points contraction in December. Most subcomponents rose for both the current and expected categories. Measures of prices paid and received also ticked…

December US retail sales missed estimates, with the headline number printing at 0.4% m/m, a decline from an upwardly revised 0.8% in November. On the positive side, the control group beat estimates at 0.7%. Netting it all out, the report was uninspiring,…