Commodities & Energy Sector

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

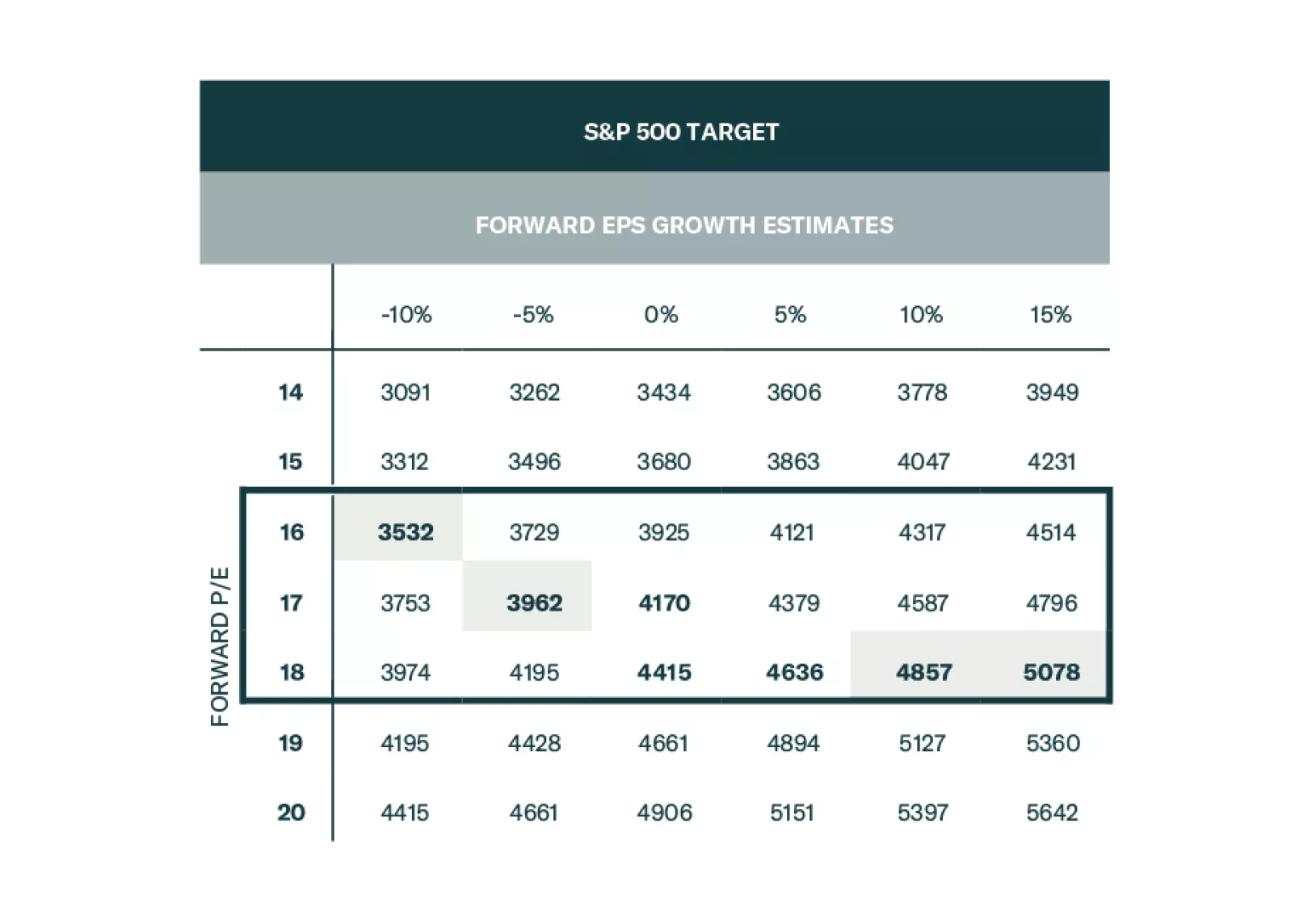

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

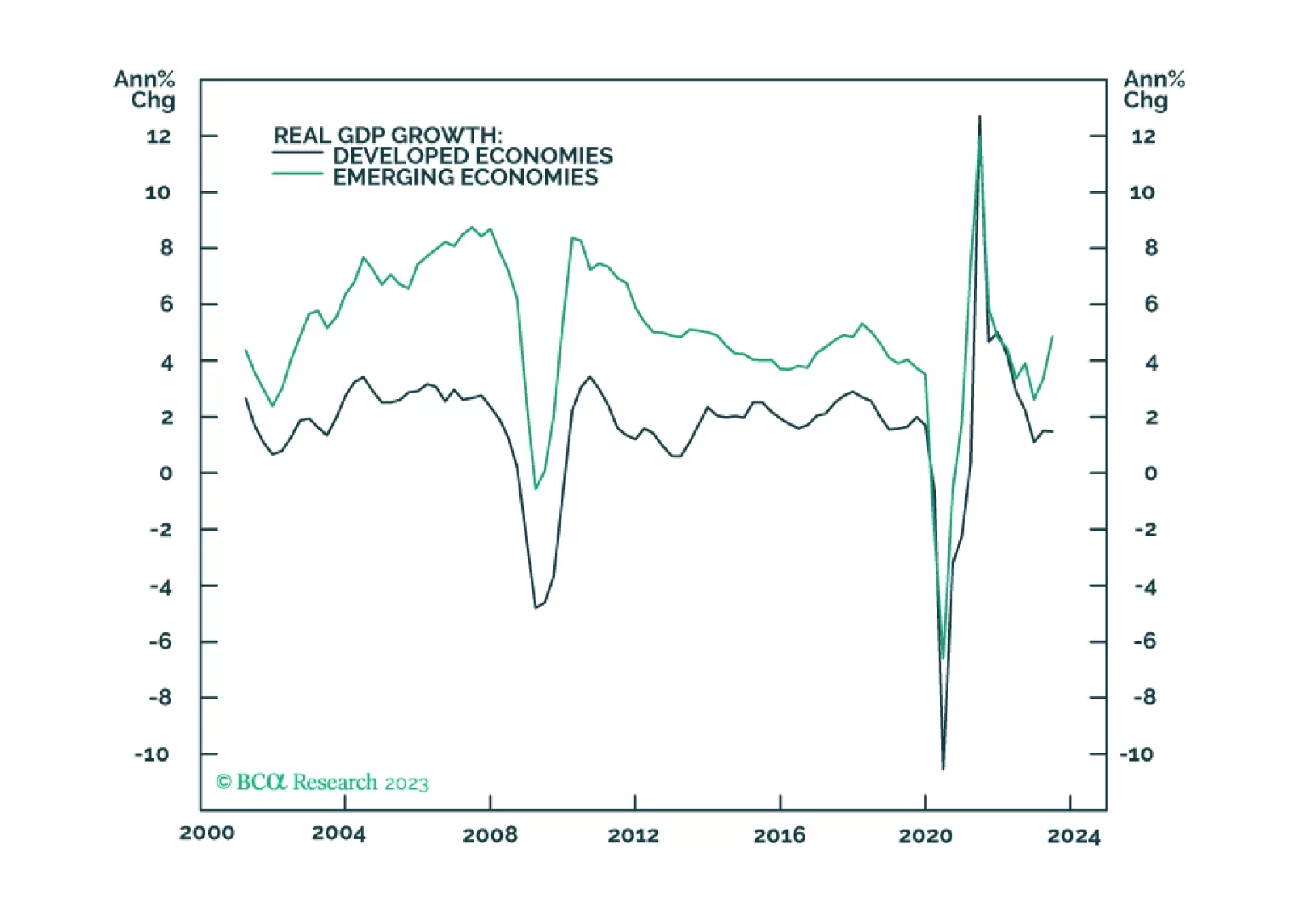

In our simulations of fairly deep global recessions averaging -1.5% in 2024 global GDP growth, we expect OPEC 2.0 to reduce output enough to offset lost demand. Even so, we find oil prices drop ~ $22/bbl – from ~ $100/bbl in 1H24 to ~ $78/bbl in 2H24. We remain long the XOP and COMT ETFs to retain oil and commodity exposures.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

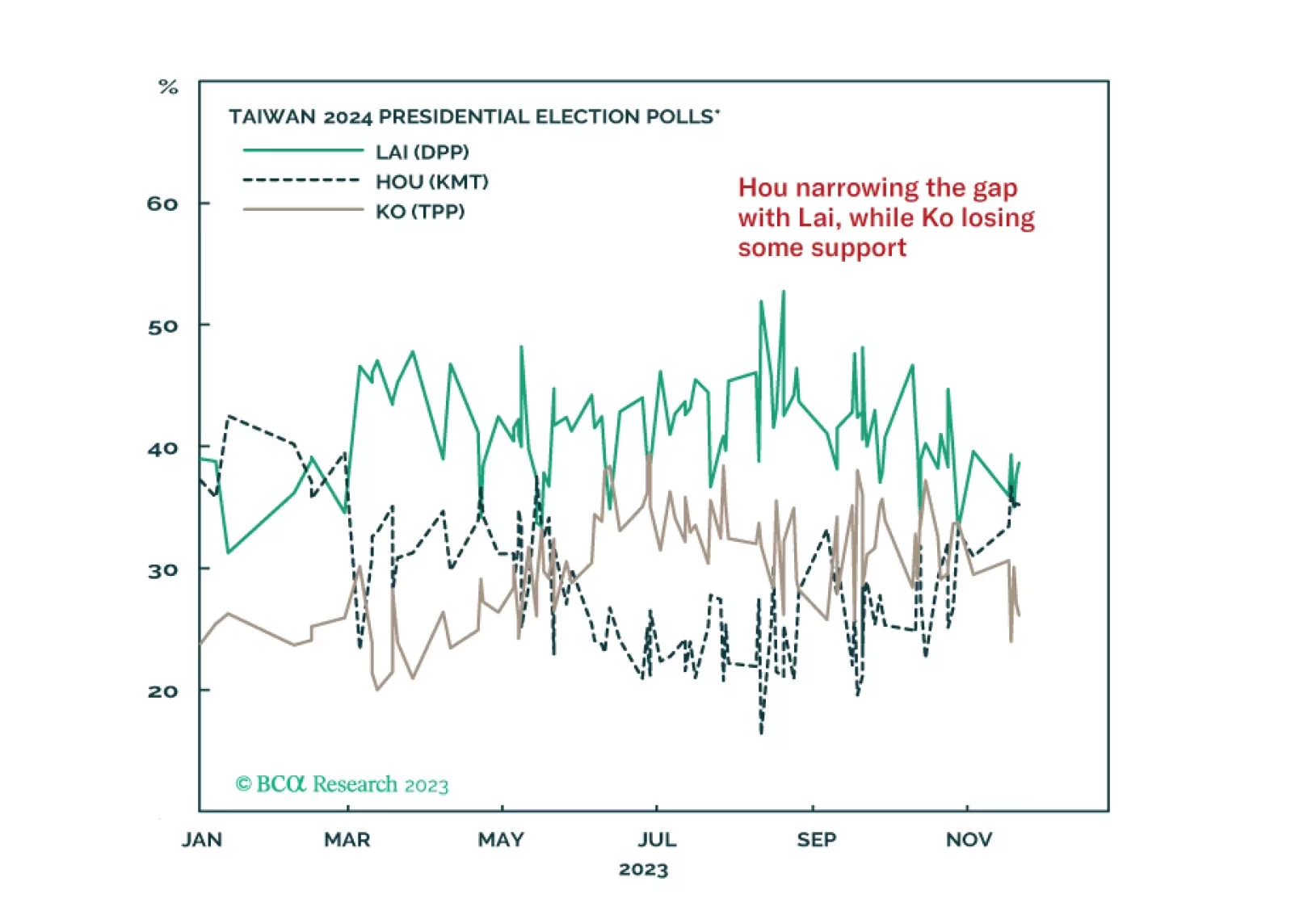

A series of notable events took place over the Thanksgiving holiday but none of them force us to change our fundamental assessments. The conflict in the Middle East is likely to escalate rather than de-escalate, while the Taiwan Strait has at least a 50/50 chance of seeing tensions escalate next year.

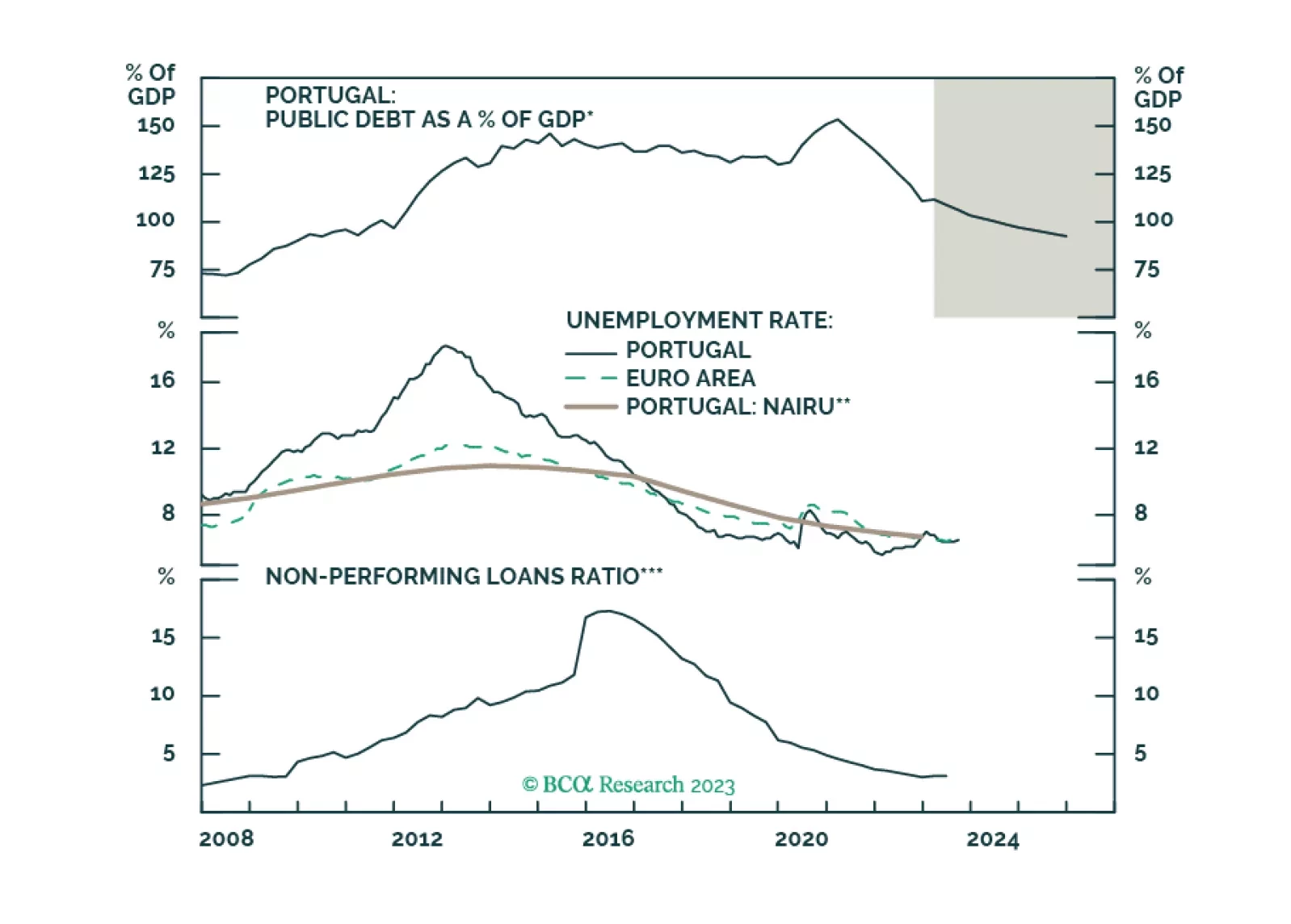

The first stop of the EIS Special Series: PIGS Have Wings takes us to Portugal.