Commodities & Energy Sector

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

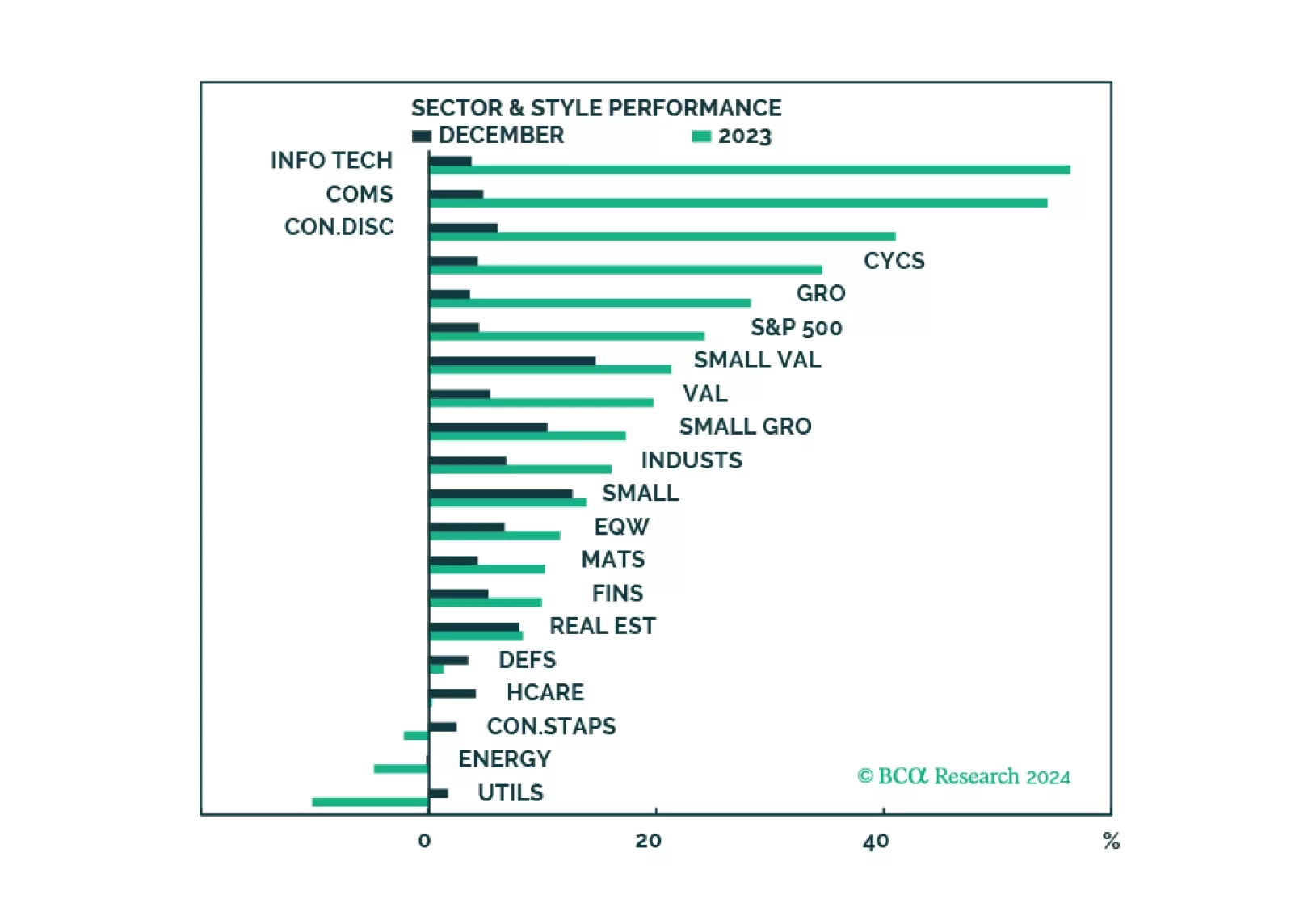

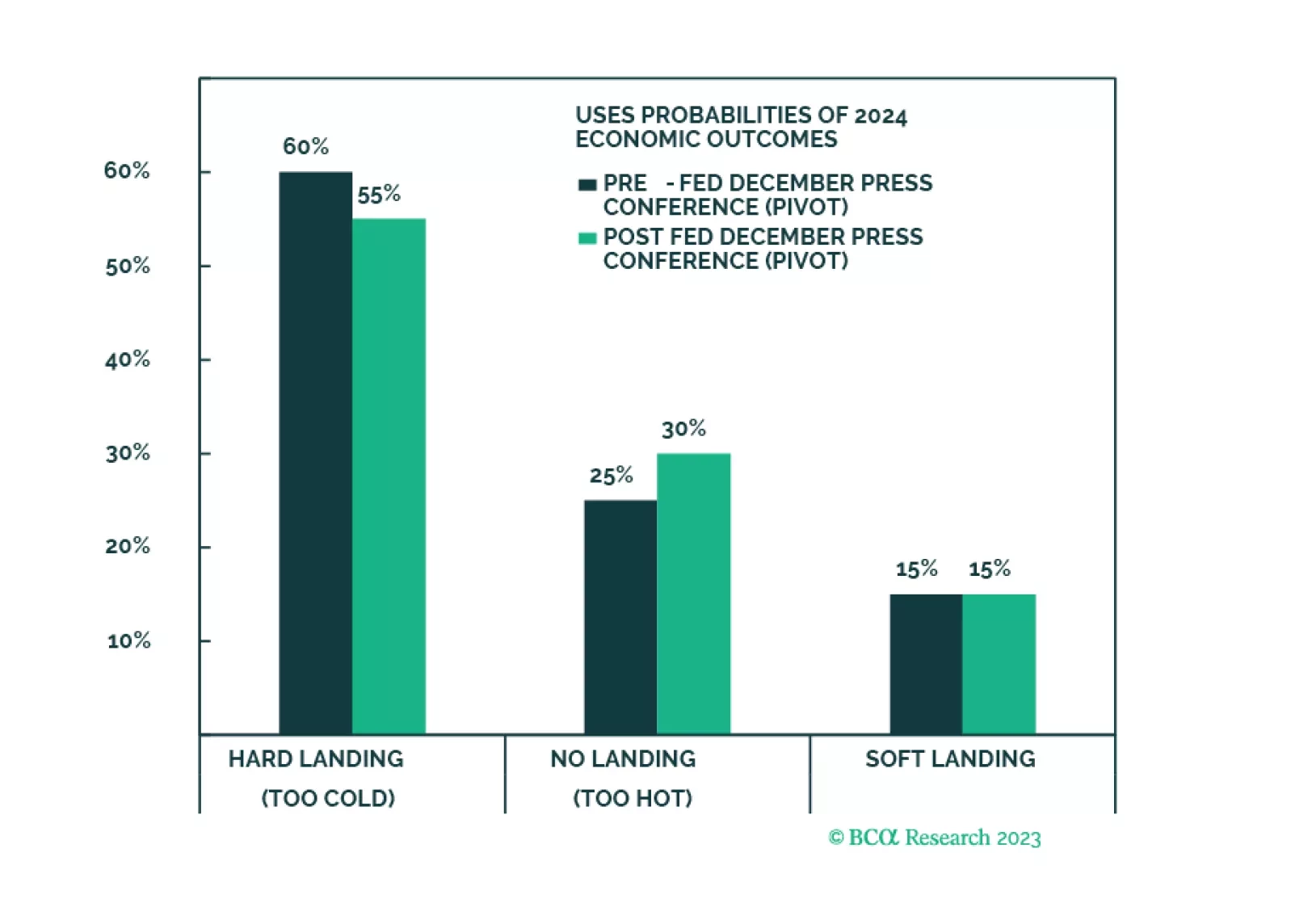

The Santa Claus rally has been fueled by investors optimism about a soft landing which is the least likely macro outcome in 2024. A pullback in the market is imminent as the probability of "too hot" or "too cold" will get priced in. We are downgrading Software and Services on a tactical basis to take profits but maintaining a strategic overweight in the same trade.

The attacks on Red Sea commercial tankers by Iran’s Yemeni proxies, the Houthi movement, are an inflation risk inasmuch as they lengthen voyage times for any shipping forced to avoid the Bab el-Mandeb Strait. The risk of an expansion of these attacks is, in our view, limited, given Iran’s inability to project naval power in the region.

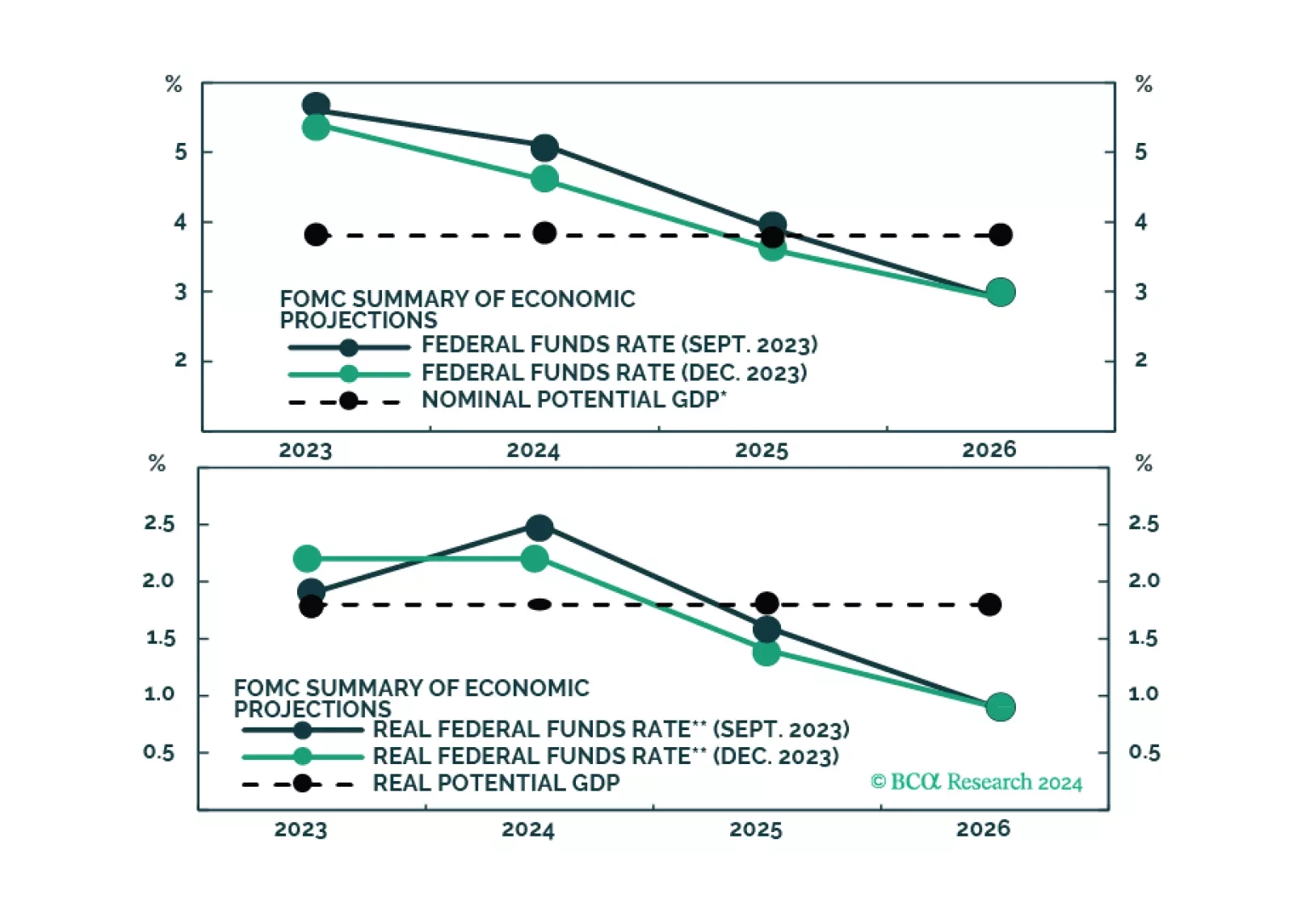

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

In this final note for the year, we take profits and close several long-term investment positions: Overweights in Insurance and Commercial Services, and underweights in Utilities, and Retail and Commercial REITs.

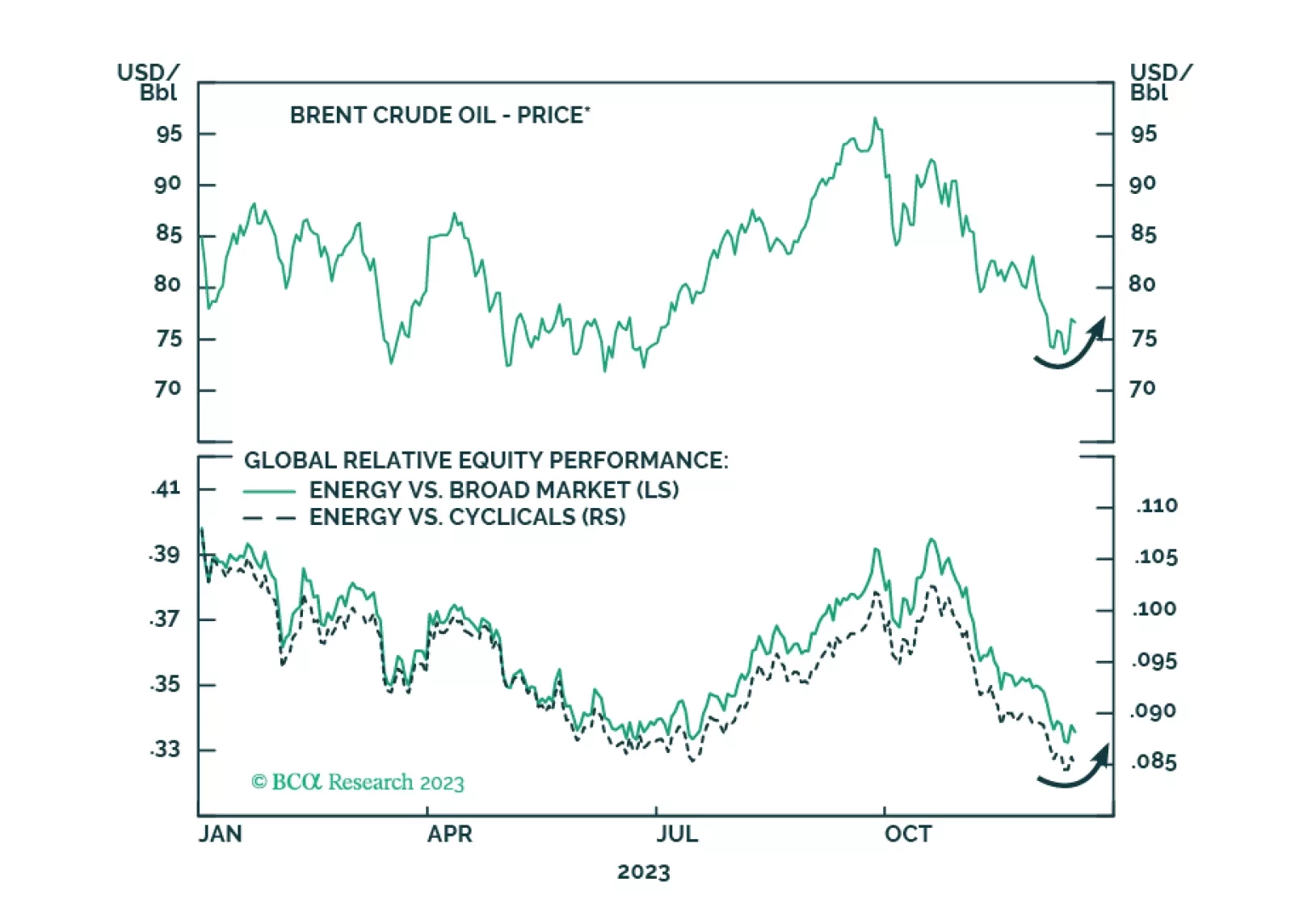

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.