Commodities & Energy Sector

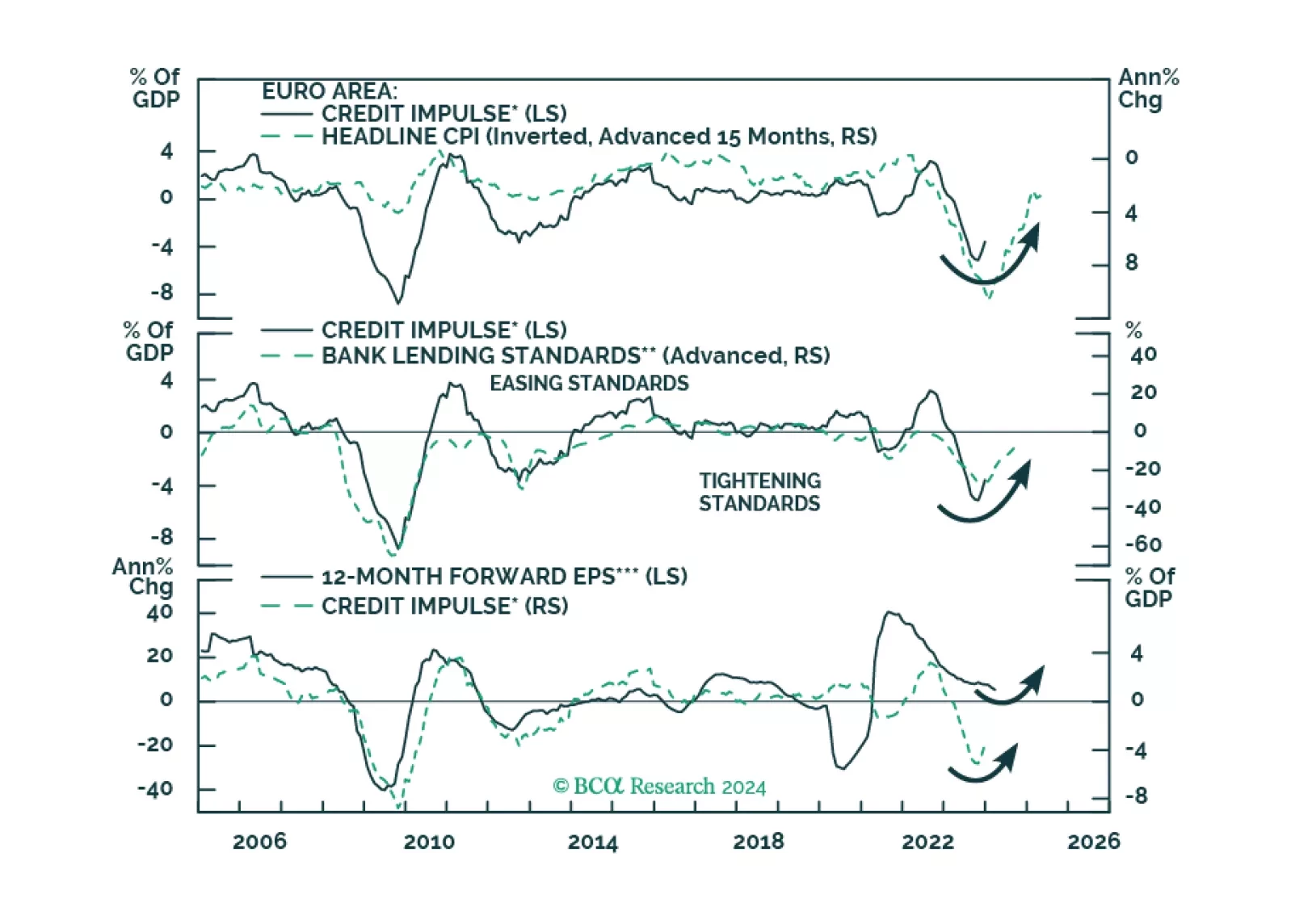

Europe credit flows are stabilizing, hence a major drag on the region’s growth will dissipate. What does this development imply for European equities?

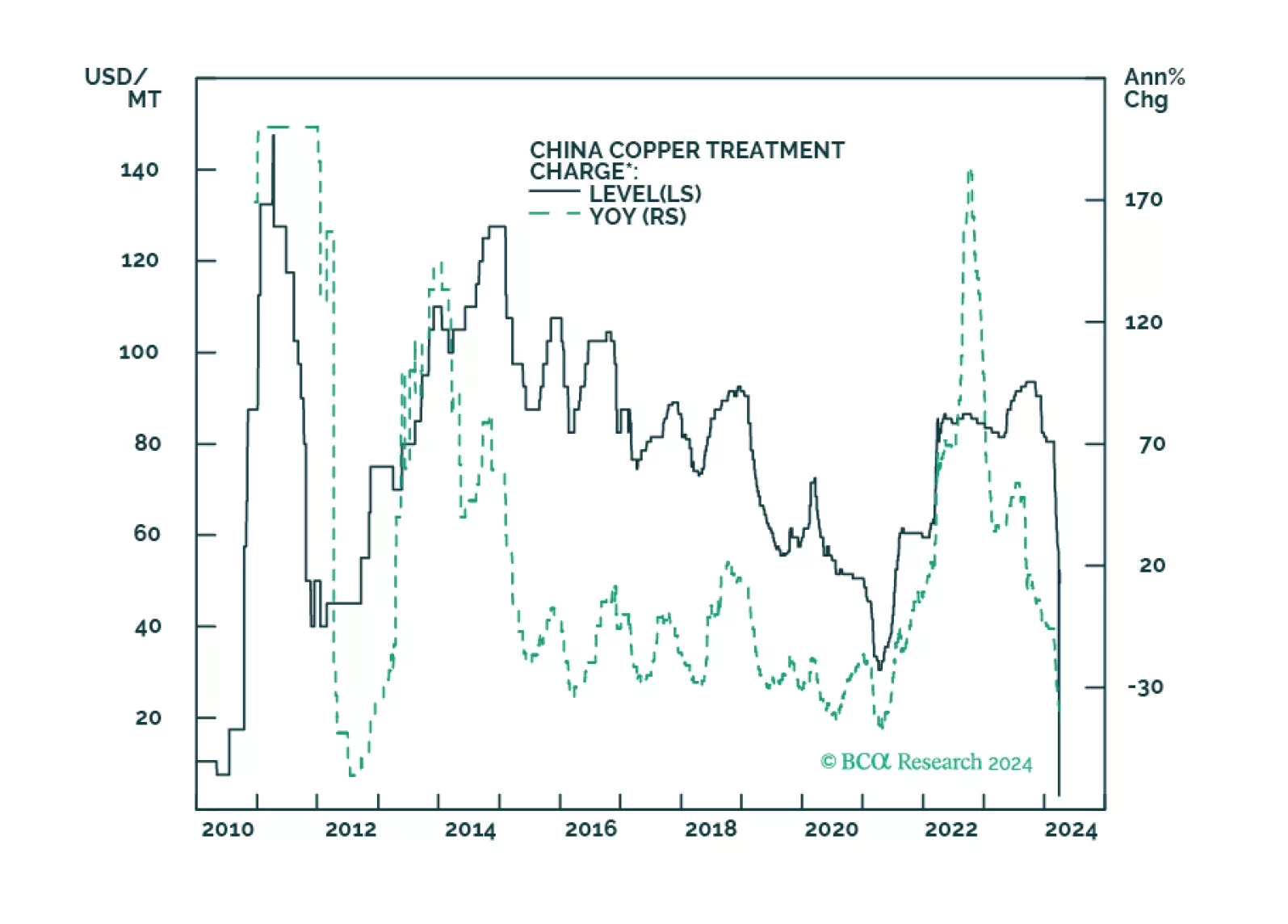

Copper markets are fast approaching a price breakout, as Chinese smelters scramble to find ore to meet increasing refined-copper demand in the wake of a global manufacturing rebound. We are holding fast to our expectation of $4.50/lb (COMEX) this year. We remain long the XME ETF to retain exposure to copper miners and refiners, and the COMT ETF to retain exposure to commodity flat price and the copper backwardation we expect.

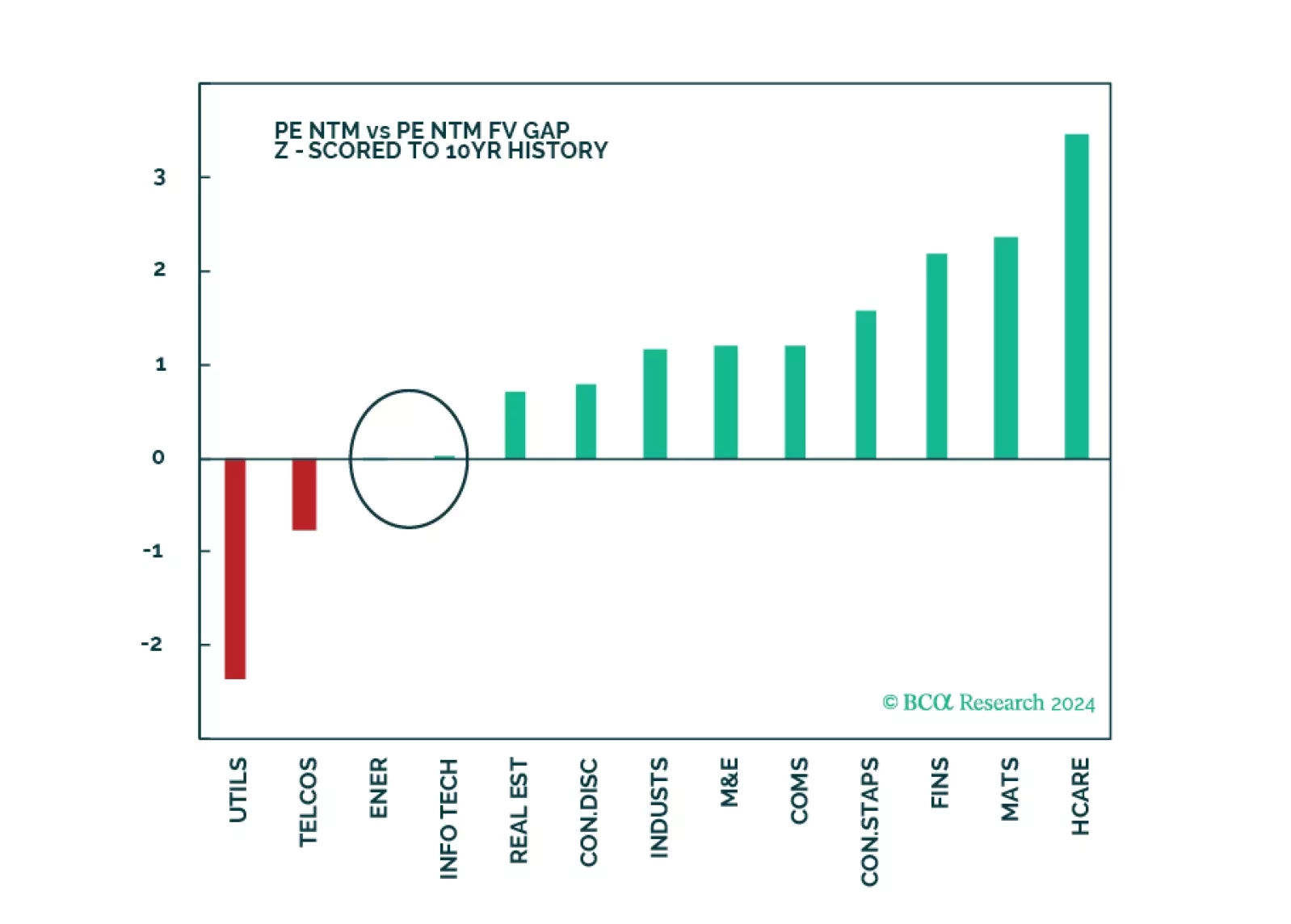

The equity rally extended into March as hard landing outcome was priced out. It has broadened, as money flowed into less over-loved pockets of the market. Our models signal that margins are about to stabilize, and earnings growth will accelerate as the year progresses. However, companies are raising prices again and the no-landing outcome and fewer than three rate cuts this year are increasingly likely.

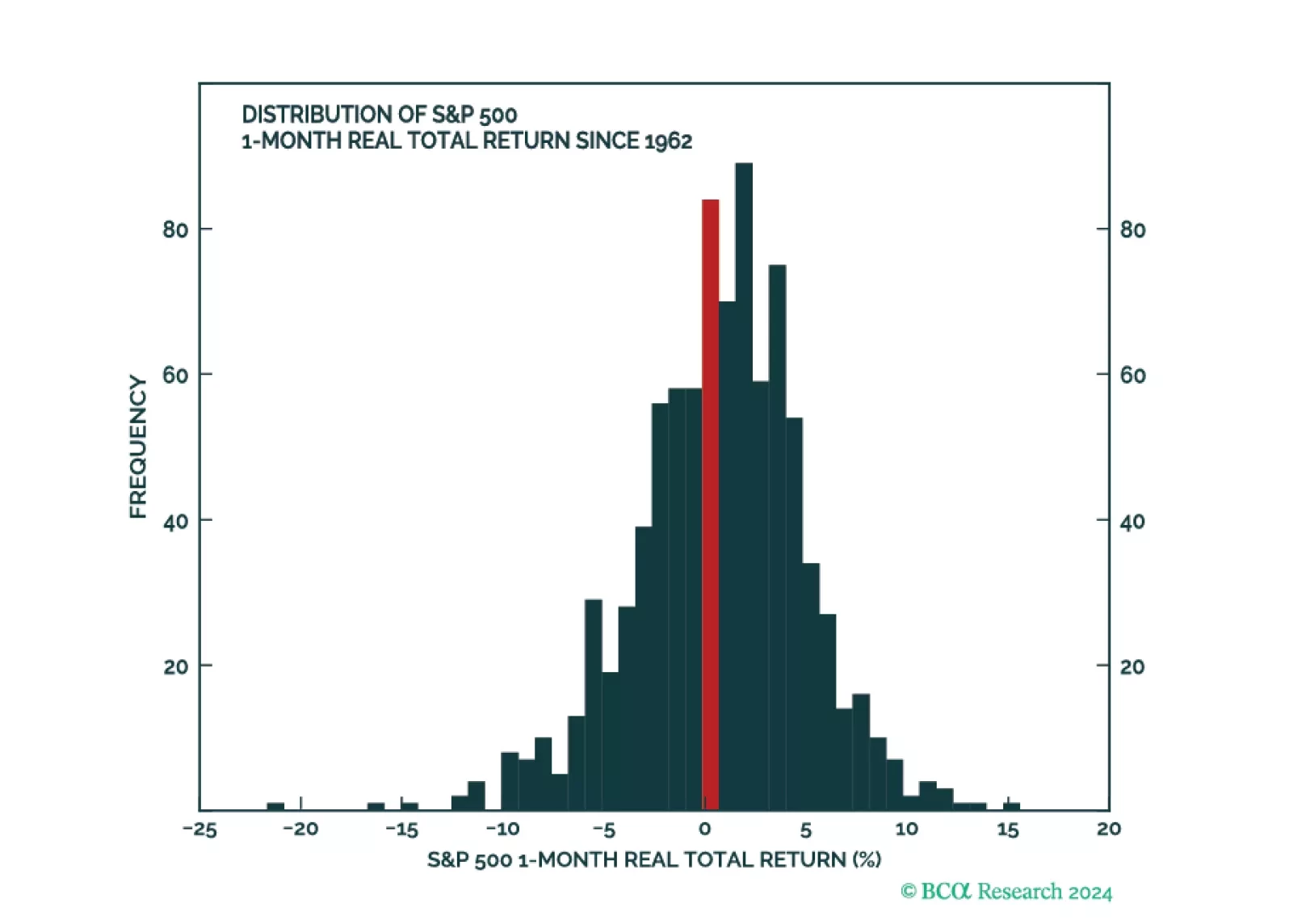

MacroQuant downgraded equities from overweight to neutral on a 1-to-3 month horizon. The model maintains a negative view on stocks over a 12-month horizon.