Commodities & Energy Sector

The decline in oil prices accelerated this month. Although Wednesday’s moves reversed Tuesday’s sharp daily declines, Brent and WTI have fallen 11% and 10% so far in September, and 30% and 33% from their April peaks. Deteriorating demand likely drove these…

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

According to BCA Research’s Commodity & Energy Strategy service, central banks will continue to be a key source of gold demand. Central bank purchases in the first half of this year exceeded first-half purchases in every year they’ve been tracked going…

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

The risk-on soft-landing narrative dominated investors’ psyche last month and pro-cyclical assets topped the August return ranking. Asian currencies led the pack by a wide margin, while the dollar was the largest laggard. Markets pricing in an upcoming Fed…

According to BCA Research’s Commodity & Energy Strategy service, oil markets are caught in a tug-of-war that has kept oil prices in a trading range since H2 2023. Bearish demand concerns are enforcing an upper limit on the price of crude while bullish…

Brazilian equities have largely underperformed their EM peers in USD terms since the beginning of the year. Rising public debt and inflation are the two main forces weighing on the Brazilian bourse. Our Emerging Market strategists expect public debt-to-GDP…

European regulatory carbon credits (EUAs) are becoming increasingly investable as an asset class. In a Special Report published last September, our Global Investment strategists agreed to the strategic bull case for EUAs, but highlighted a bearish view on…

Gold reached new all-time highs earlier this week. The yellow metal has returned a whopping 20.2% YTD, with the rally reaccelerating over the past month. Gold prices are inversely correlated with the dollar, and the expectations for US interest rate cuts have…

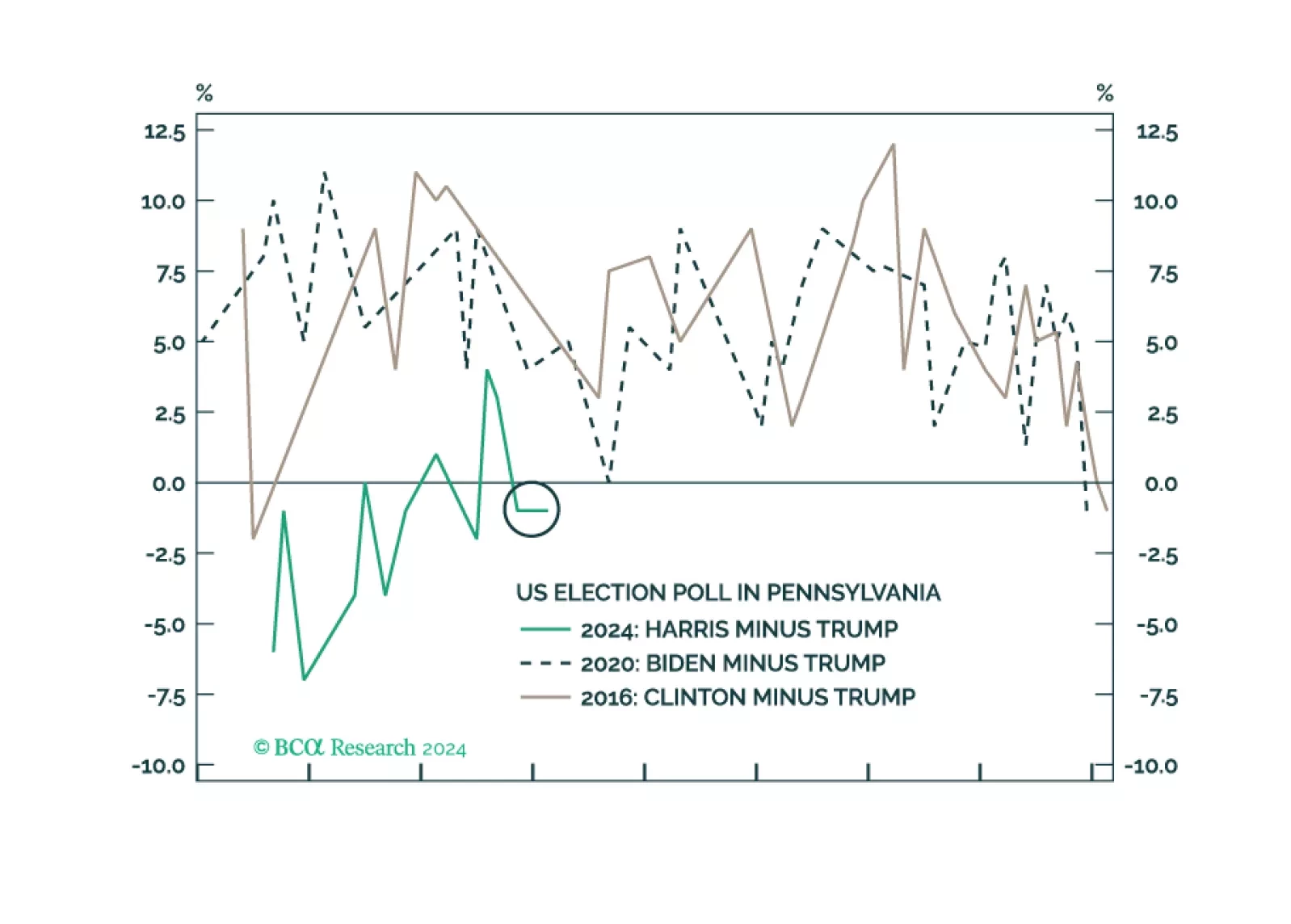

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.