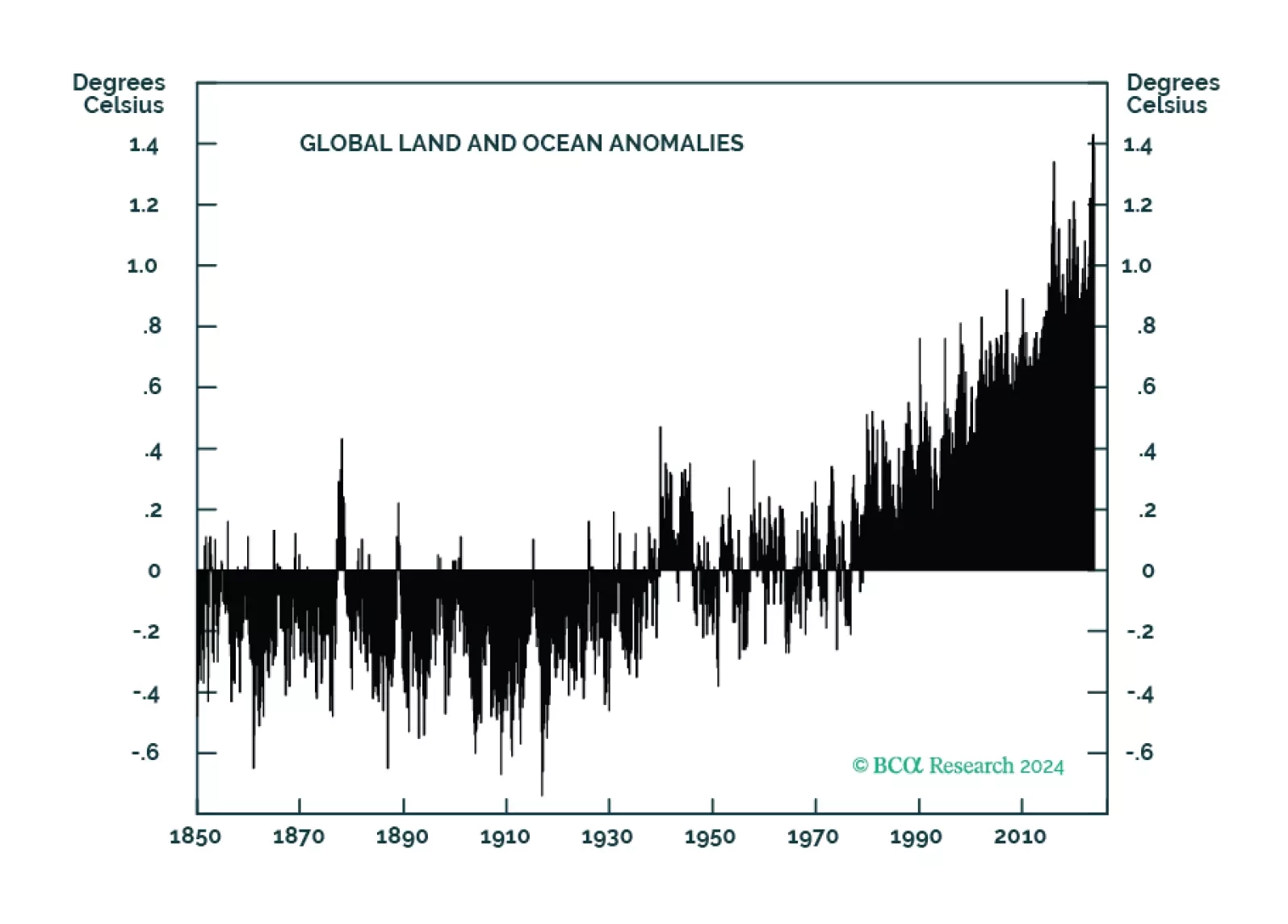

Climate Change

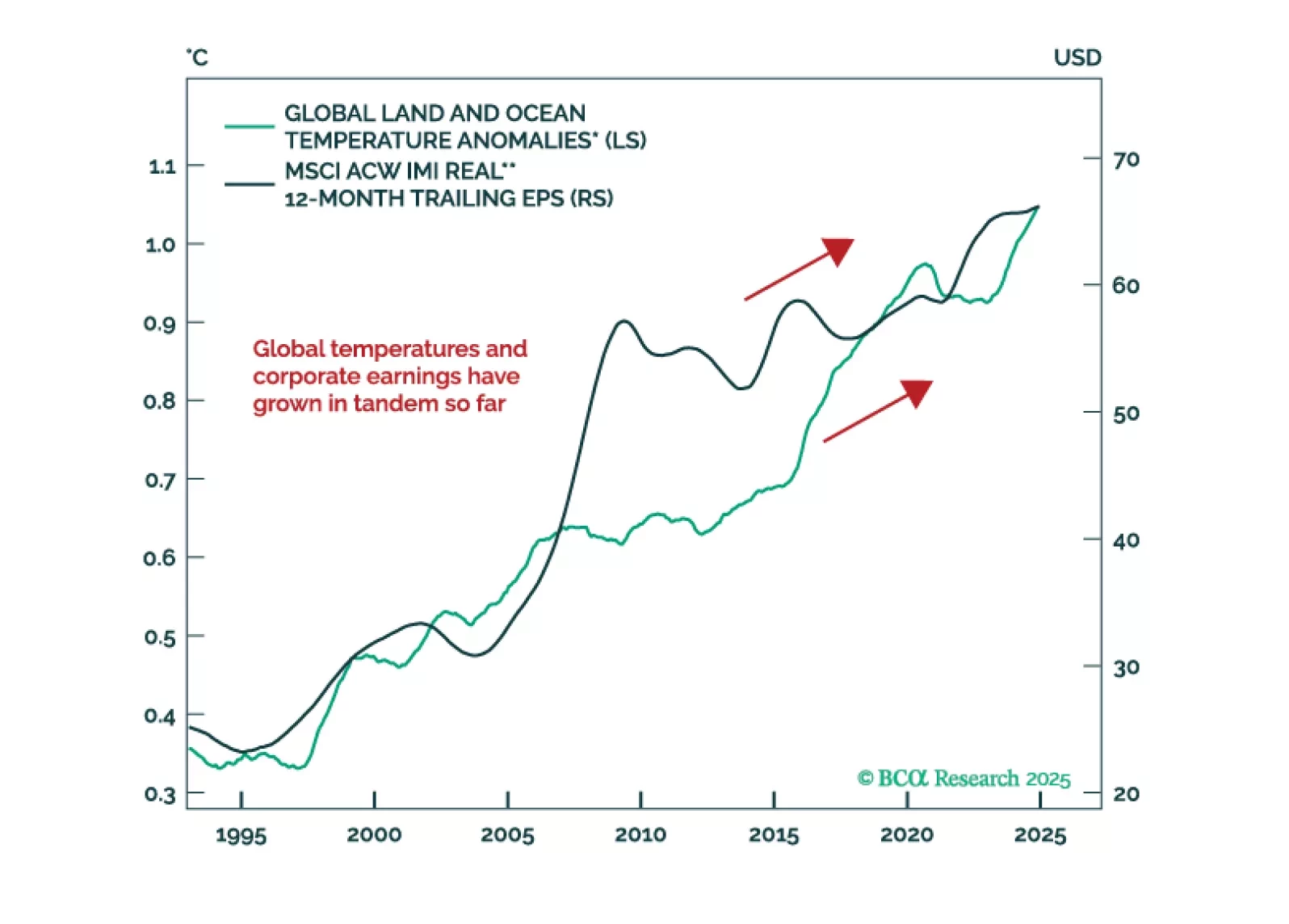

In our Beta report, we take a break from US politics and focus on the investment implications of climate change. Our colleague Ritika Mankar, of BCA’s Global Investment Strategy, makes a case for long-term investors to actually completely ignore climate change in their strategic asset allocation. Global warming will simply not make any difference, macroeconomically speaking, over the next five to ten years. Over a longer time horizon, climate change may even spur more economic growth, although with higher inflation as well.

Western policymakers are pursuing three capital “T” Truths: China is evil, climate change is a major risk, and Russia is… also evil. Pursuing all three priorities at the same time presents a version of the classic “impossible trinity.”

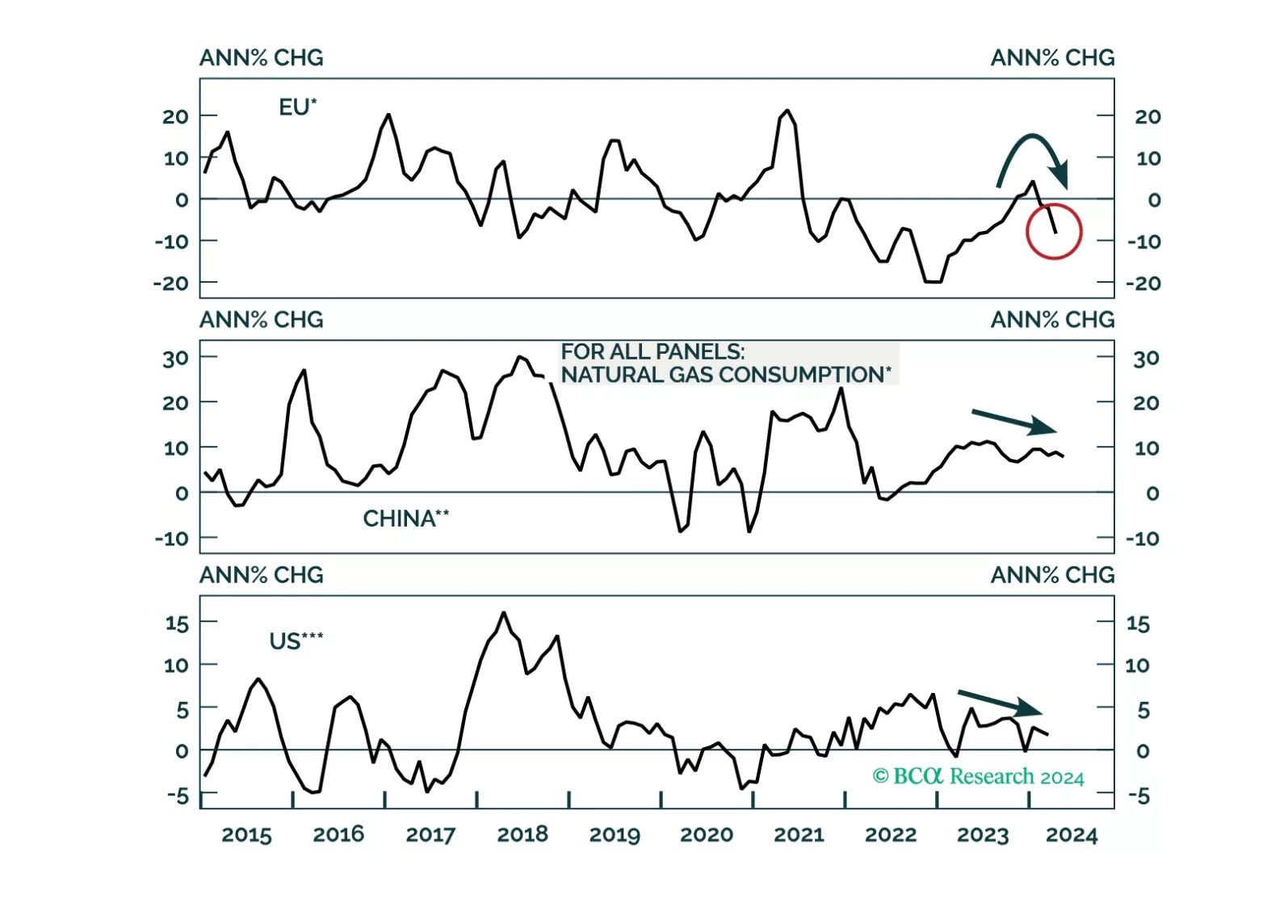

A global economic downturn will be a headwind for natgas prices over the cyclical horizon. Thereafter, LNG capacity additions will help keep the market in balance into the end of the decade. That said, Europe’s increased dependence on global LNG flows raises its exposure to market dynamics in the rest of the world. This will keep volatility elevated versus pre-Ukraine war.

The green energy transition will drive a surge in copper demand over a long-term horizon. However, a better entry point to get long will emerge after the next economic downturn begins.

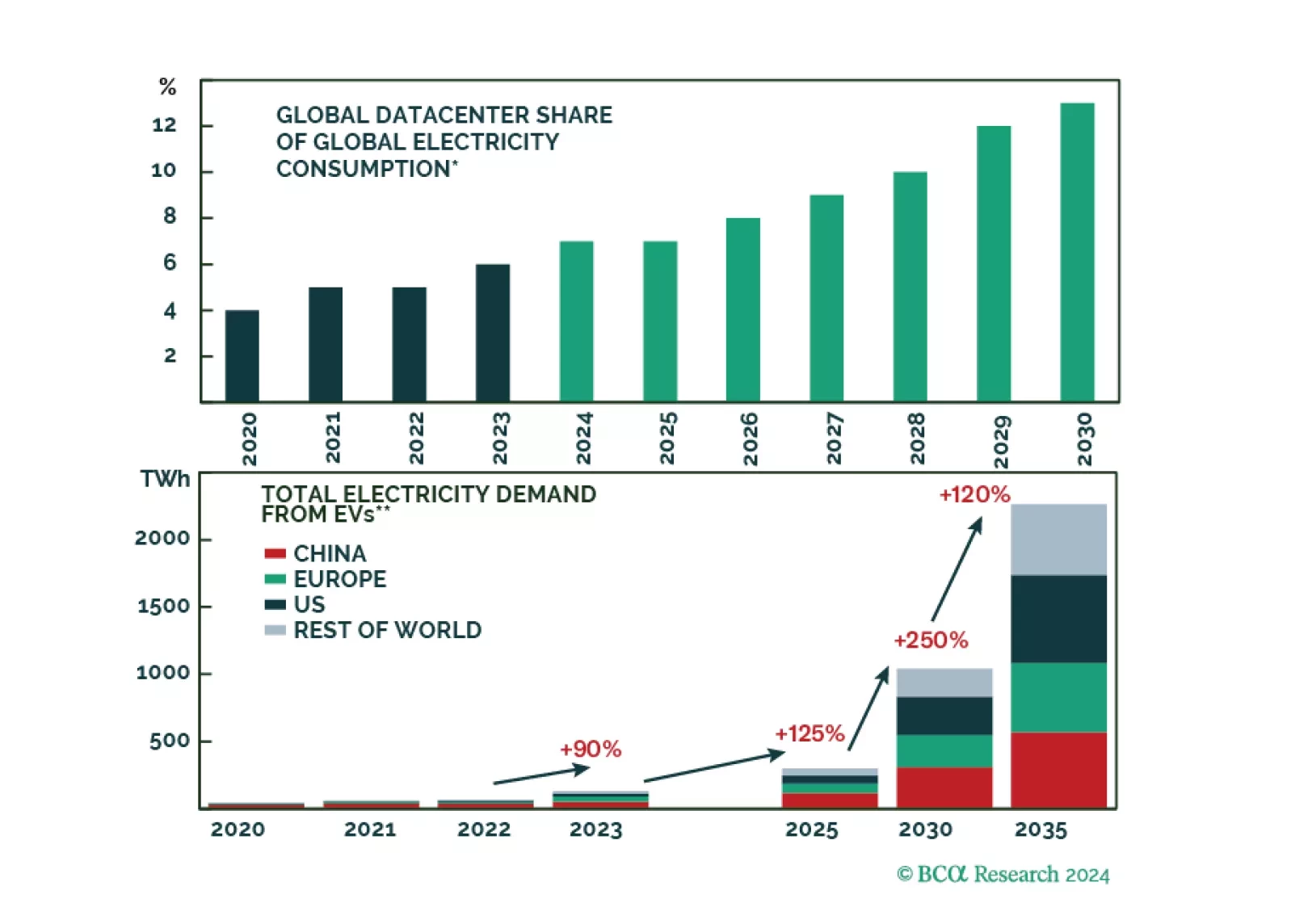

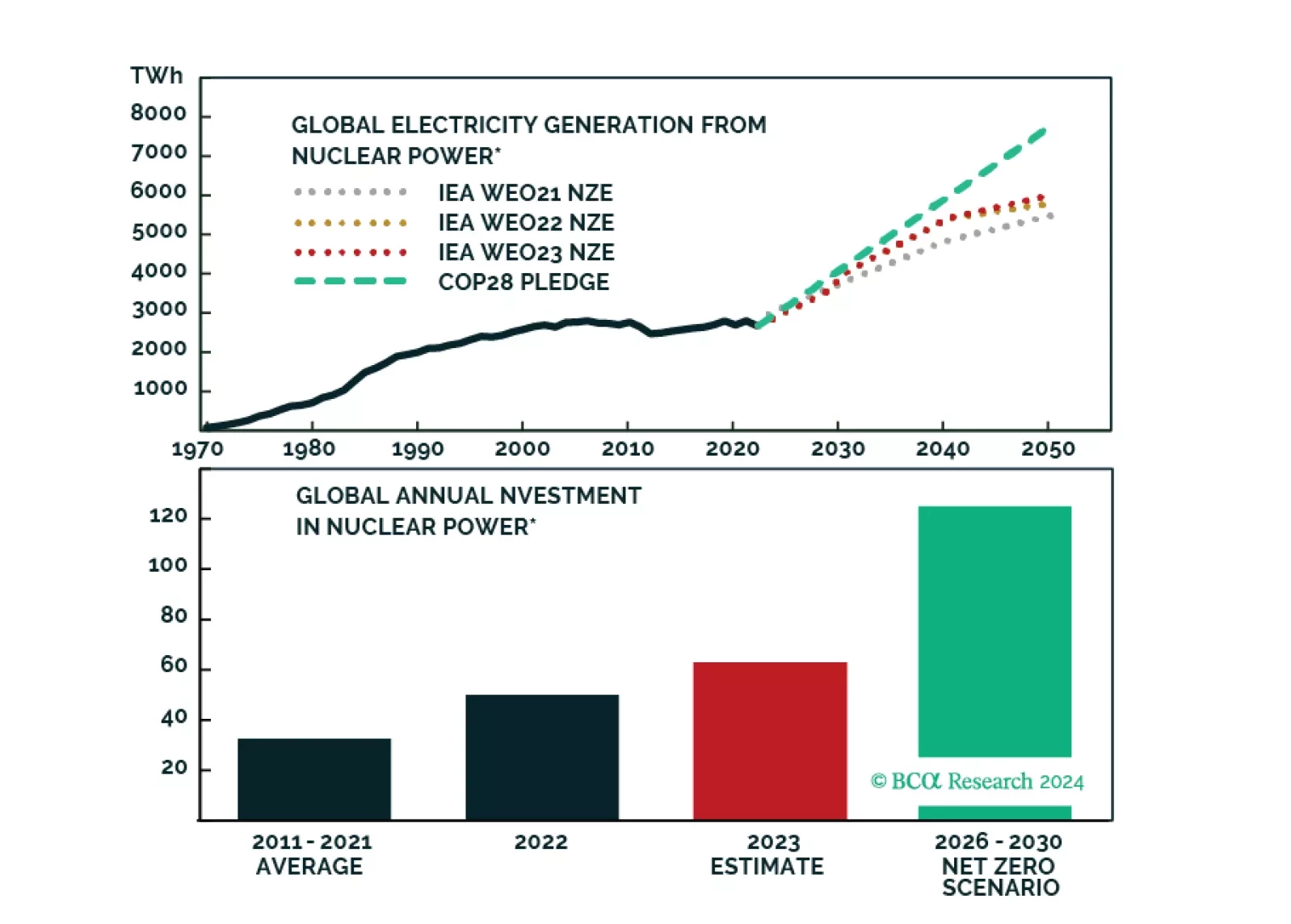

AI, EVs, and reshoring will lead to a massive surge in demand for electricity. Carbon-free, cheap, baseload nuclear energy stands to greatly benefit from these megatrends going forward.

Global ag markets will become more volatile as anthropogenically induced climate change continues to degrade farmland. This will make price signals emanating from these markets less efficient in terms of processing supply-demand fundamentals. All else equal, food prices likely move higher, which will contribute to inflationary biases in the medium-to-long run. Investors will continue to seek out farmland investments as a way to diversify portfolio risk and raise absolute returns.

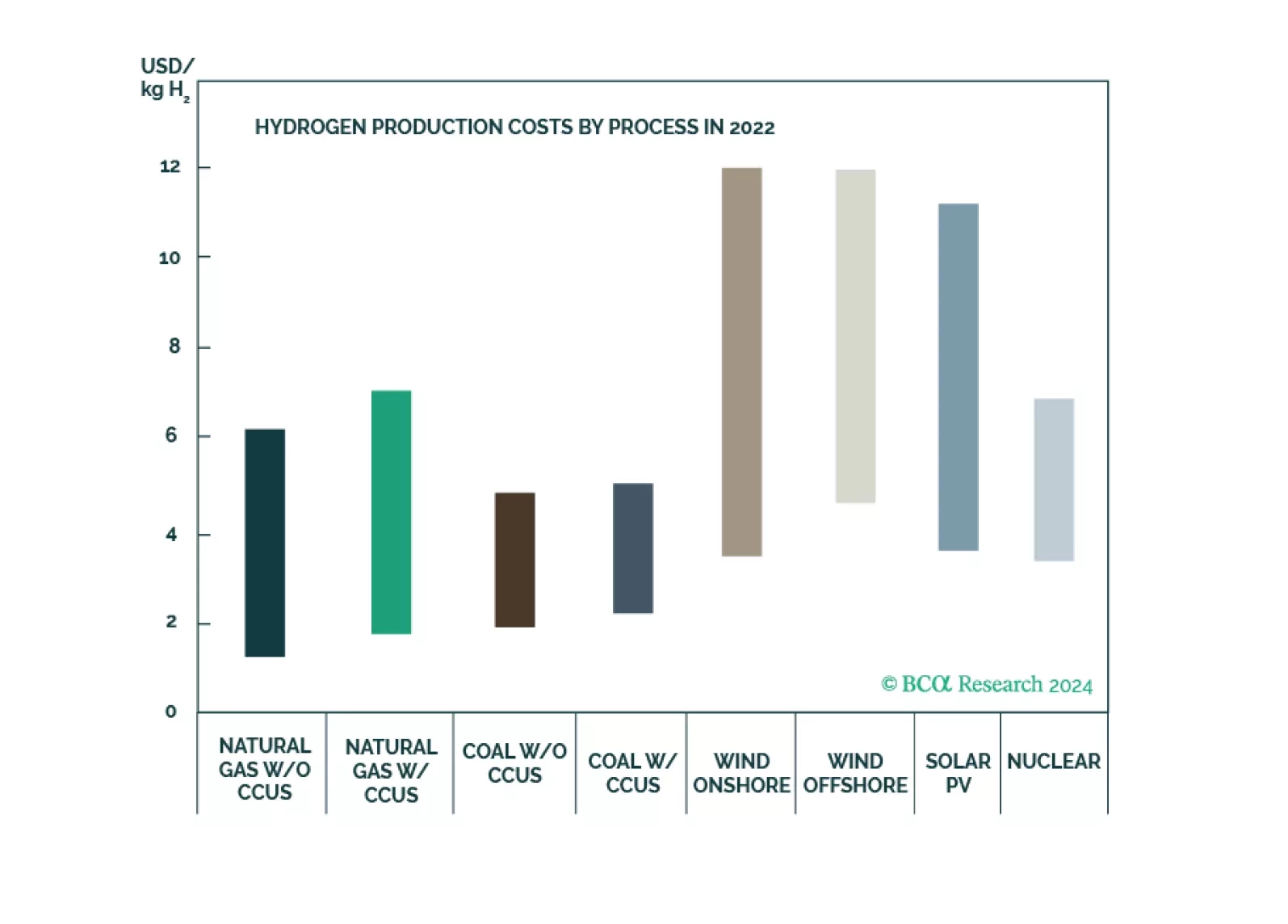

Naturally occurring hydrogen as a clean-energy source has the potential to satisfy significant energy demand growth at low cost. Oil and gas E+P companies and pipelines are ideally positioned to take a leading role in this clean-energy evolution, given their core competencies include large-scale resource extraction, storing and transporting gaseous commodities. Blending gold hydrogen with natural gas in pipeline systems could accelerate the industry’s learning curve in finding and delivering clean-energy fuels.

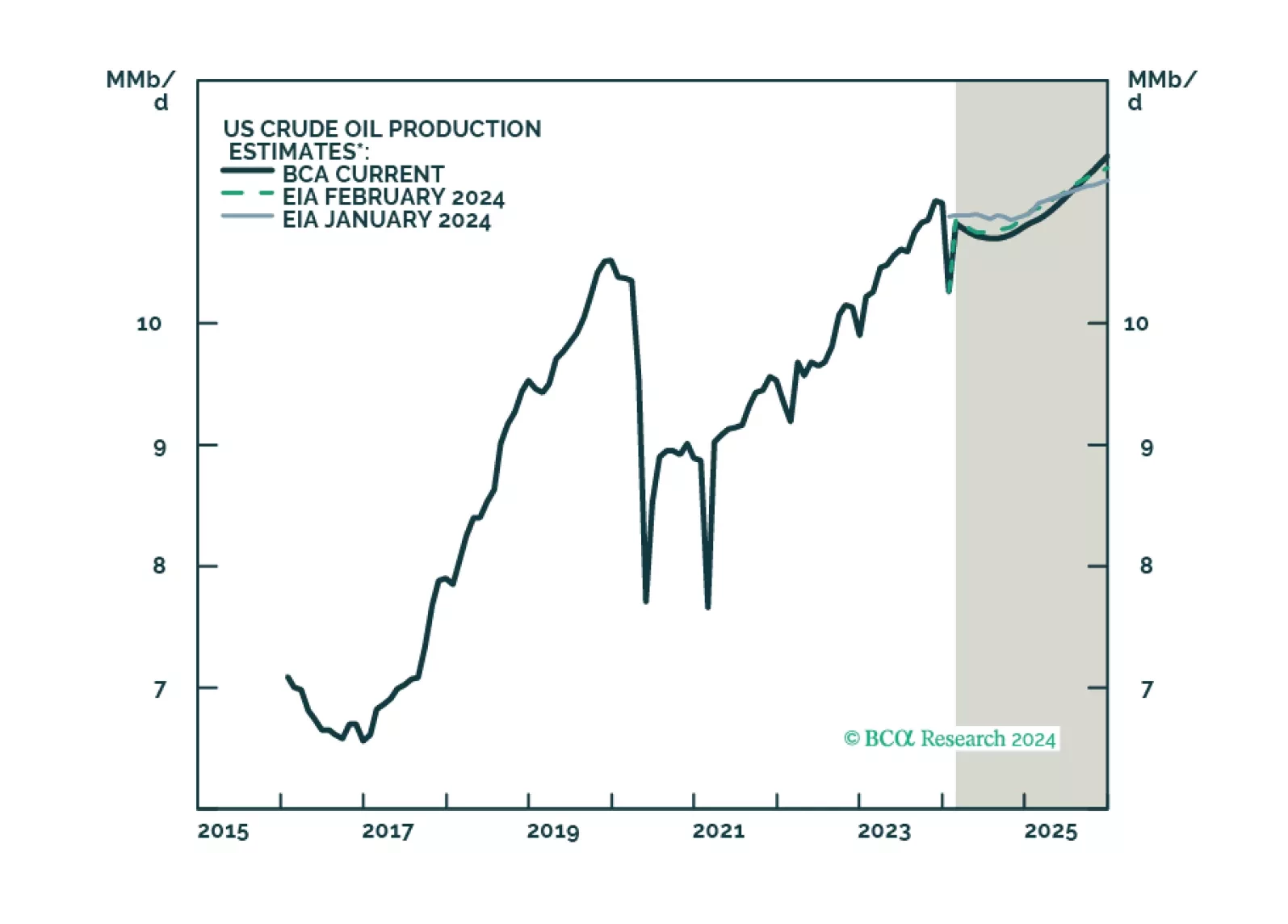

Energy markets are balanced in the short run, which keeps our Brent price forecasts at $95/bbl and $105/bbl in 2024 and 2025. Structurally, we see an upward bias to inflation, as geoeconomic fragmentation fundamentally alters supply chains; higher costs follow. Military access to oil will be prioritized. Renewables are the future, but war will be fought with hydrocarbons. We remain long the COMT, XOP and PPA ETFs.

BCA Research presents a limited monthly special series about the Nuclear Renaissance.

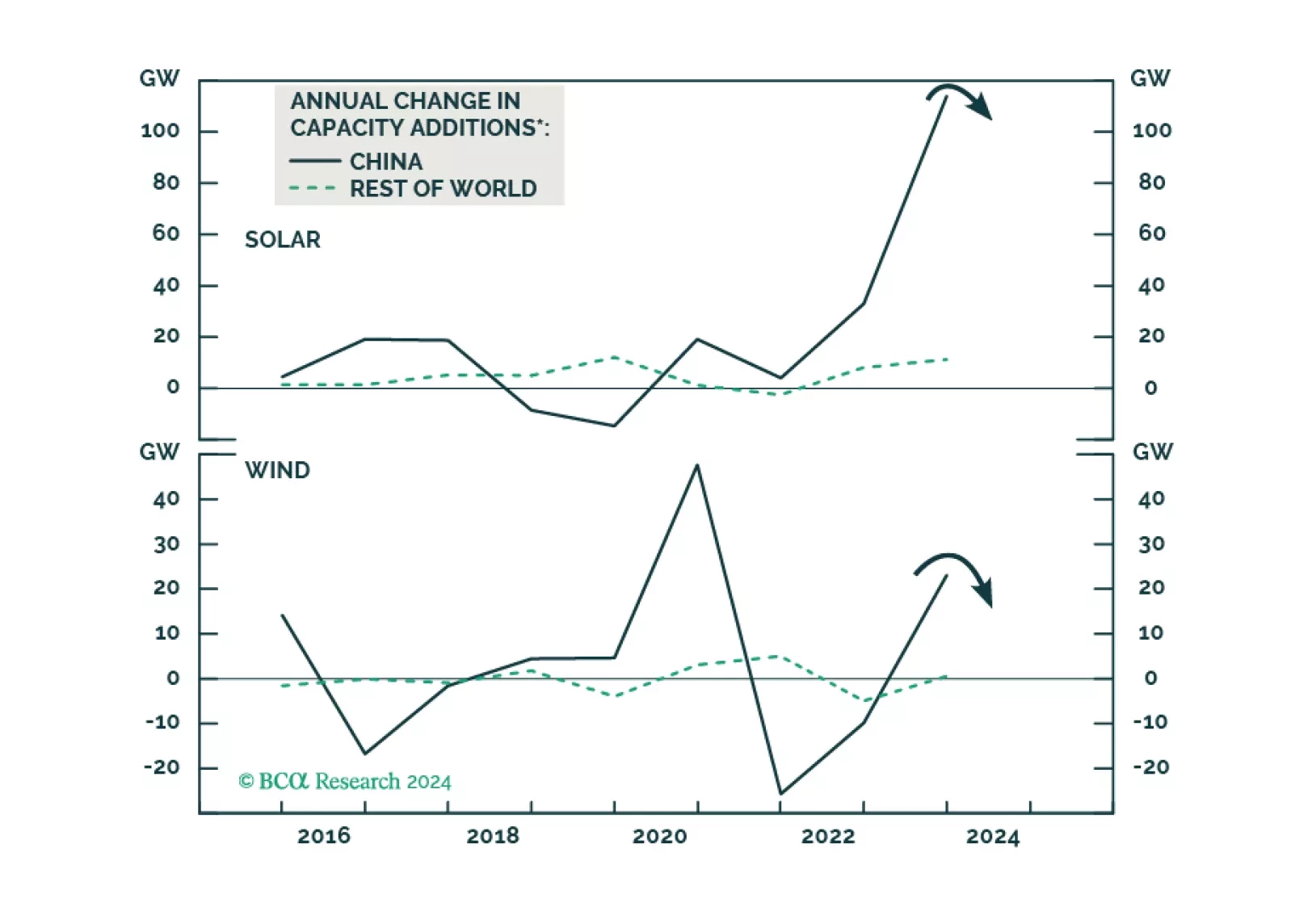

The global green energy rush faces mounting headwinds. Additional global solar and wind capacity installations will have considerable growth reduction this year. Copper prices did not drop much in 2023 due to surging demand from green power build-up. Green power will be less positive for copper demand in 2024 than in 2023. We expect more downside in global renewable energy stocks.