China

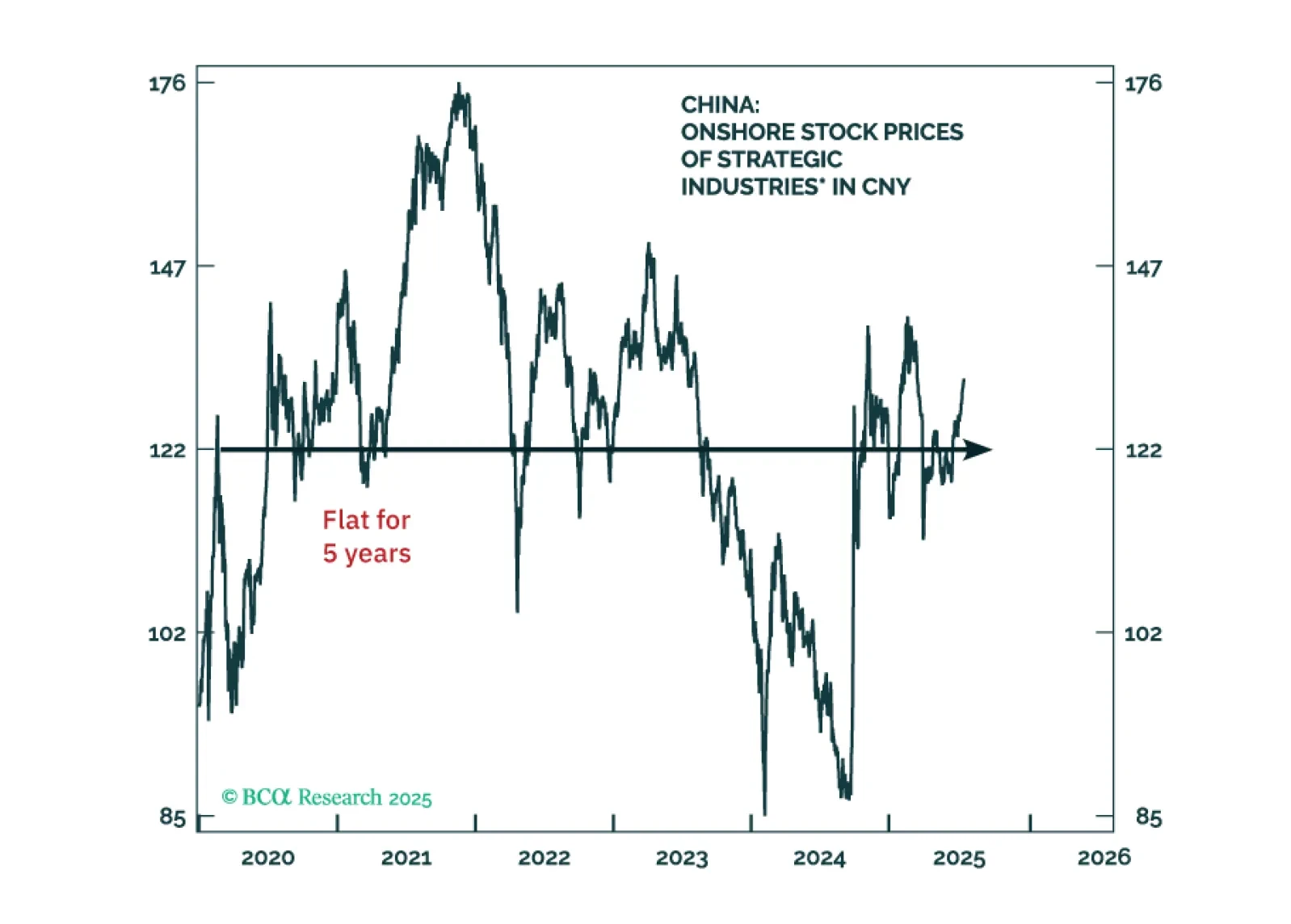

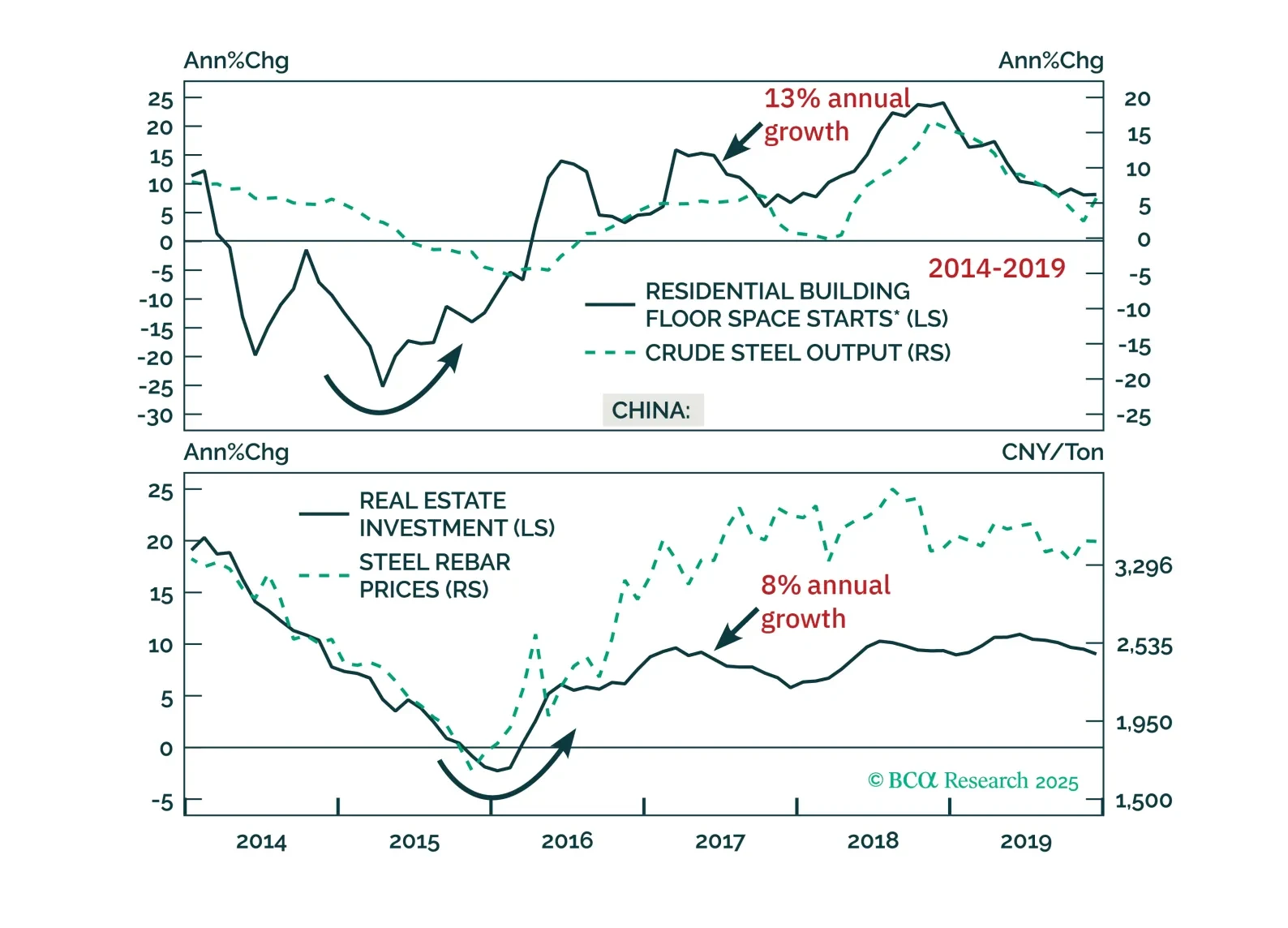

Investors often ask us which industries the Chinese government is prioritizing for expansion. The assumption is that investing in sectors hand-picked authorities will produce solid investment returns. Yet, this assumption has not held over the past decade.

Euro area and Chinese interest rates must fall much further to prevent monetary policy from becoming ultra-restrictive. But Trump’s attempts to force unwarranted rate cuts from the Fed risks a vicious backlash from the bond vigilantes.

Beijing’s supply-side push faces steeper hurdles than in 2016. With limited demand support and tighter constraints on cutting capacity, today’s reforms are unlikely to pack the same punch.

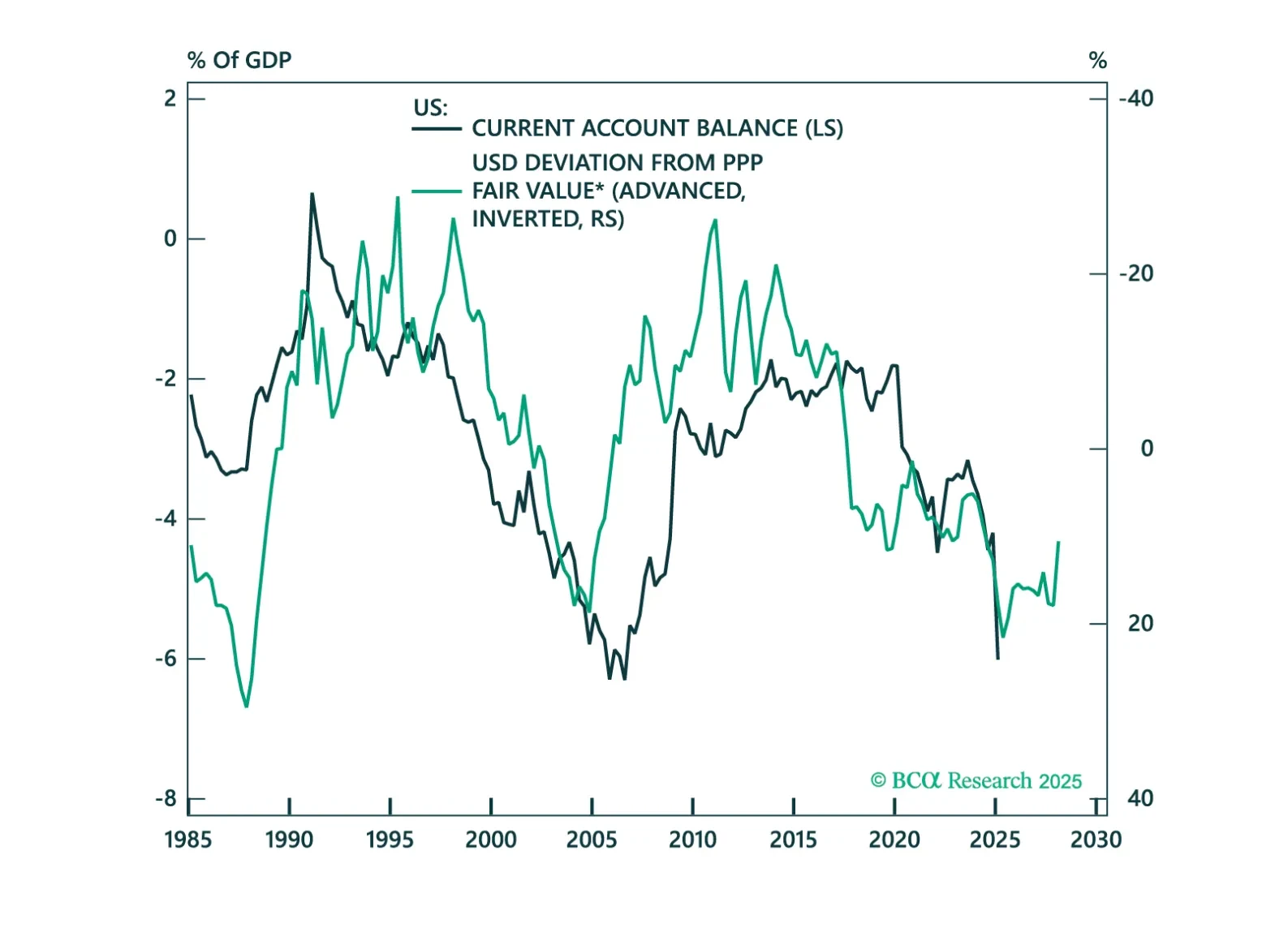

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

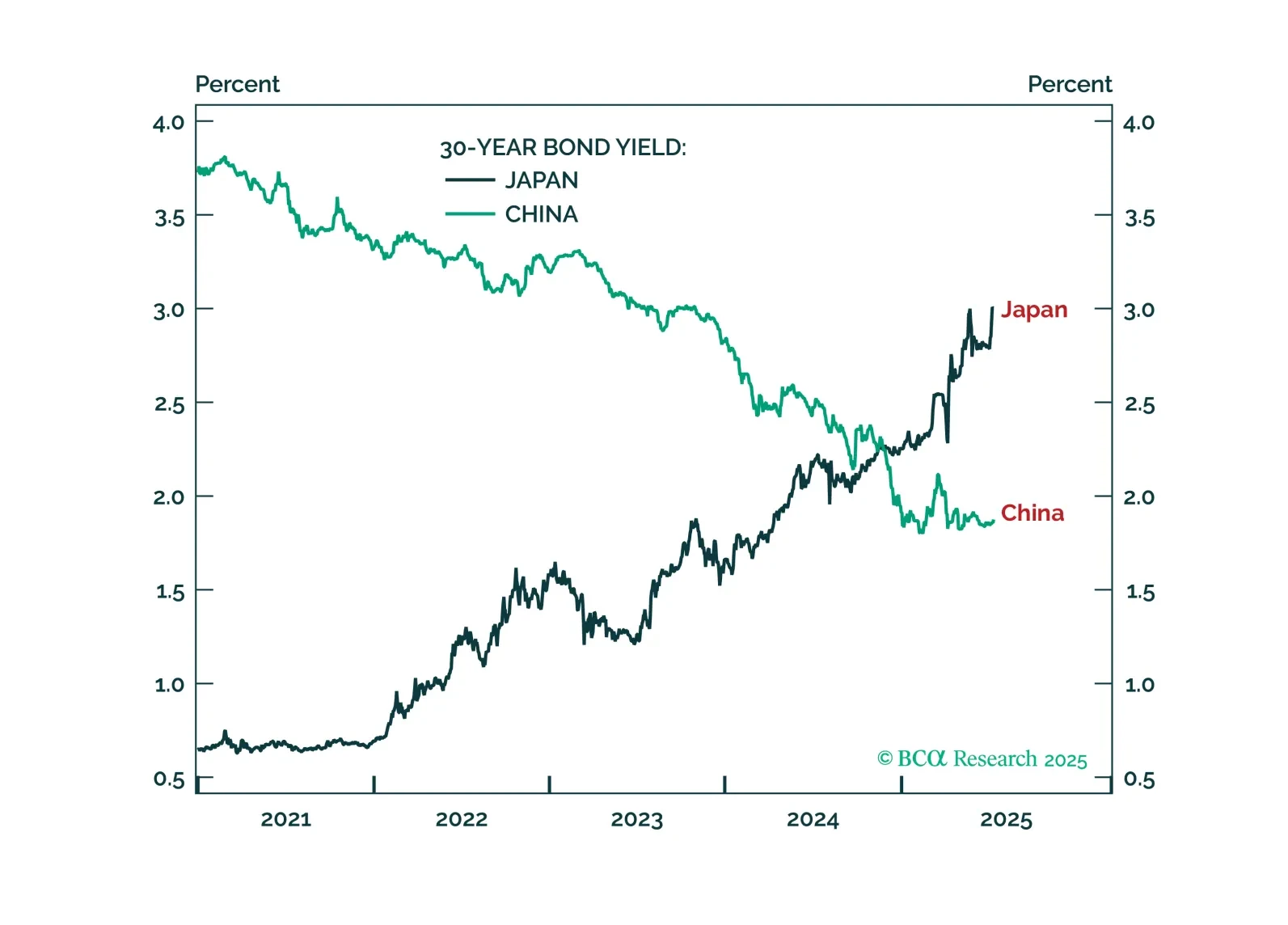

Upward pressure on Japan’s real bond yield justifies overweighting the yen and underweighting overvalued tech. Plus: two new tactical trades are long JPY/EUR and short platinum.