China

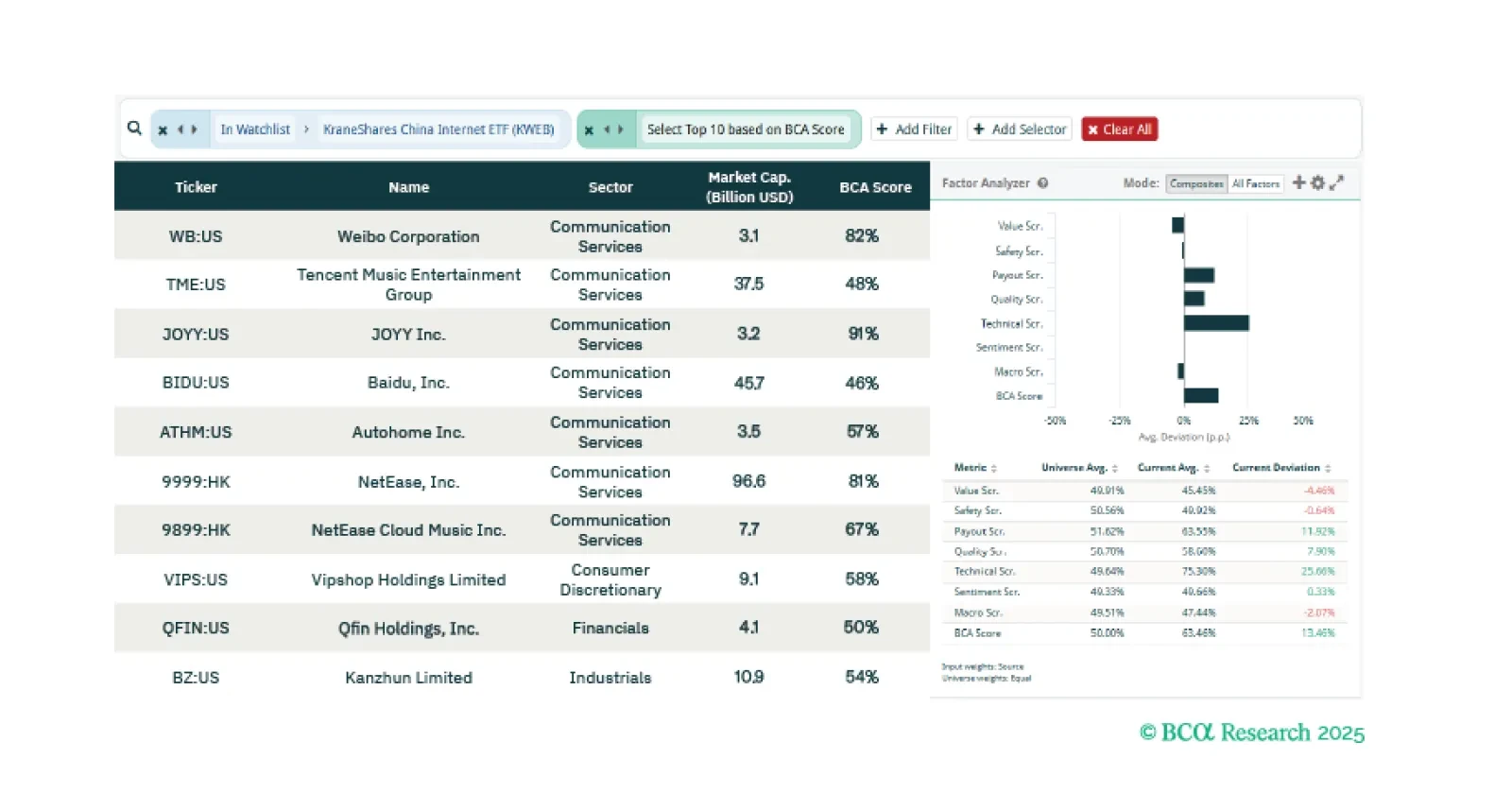

This week our screeners explore offshore Chinese internet stocks, US Healthcare equities, and sectoral opportunities in the Canadian bourse.

Rising Russia-NATO risks, tactical oil/gold trades, tougher sanctions on Russia (maybe China), China stimulus with ~5% growth target, and US checks on Trump’s ambitions will define Q4.

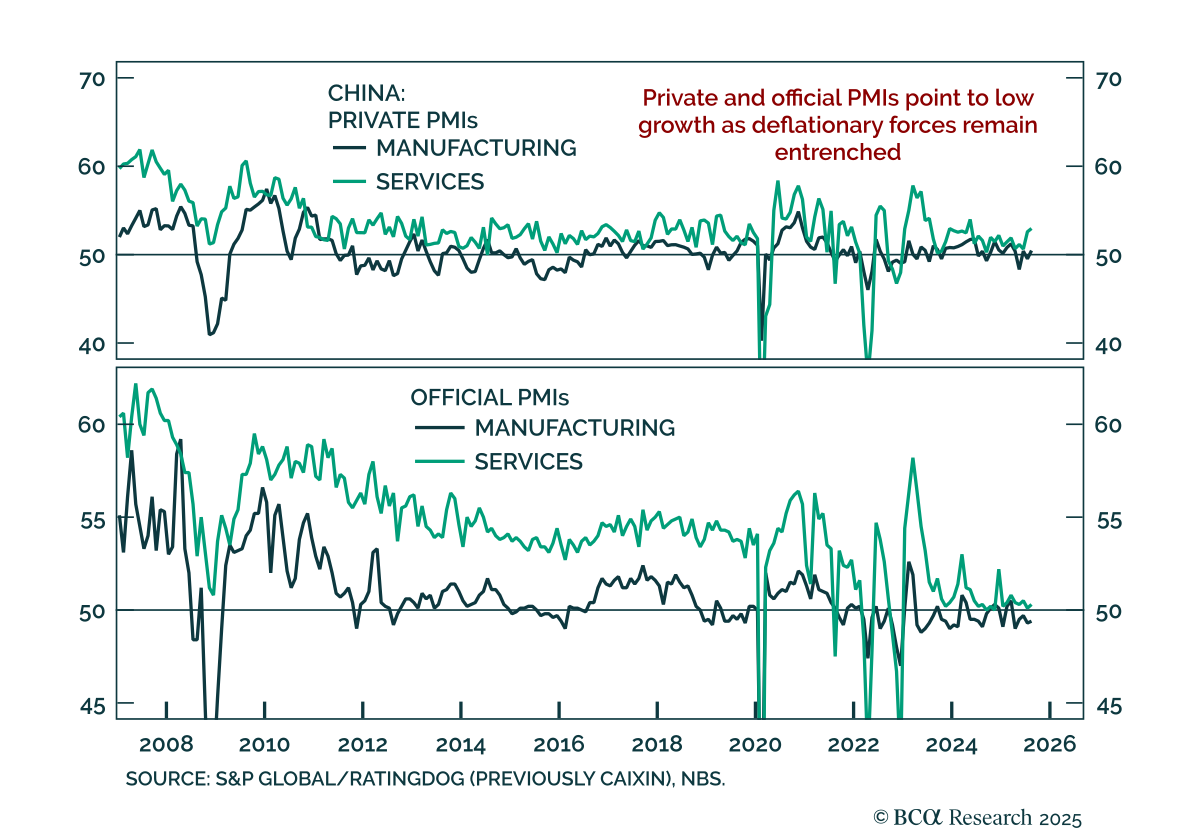

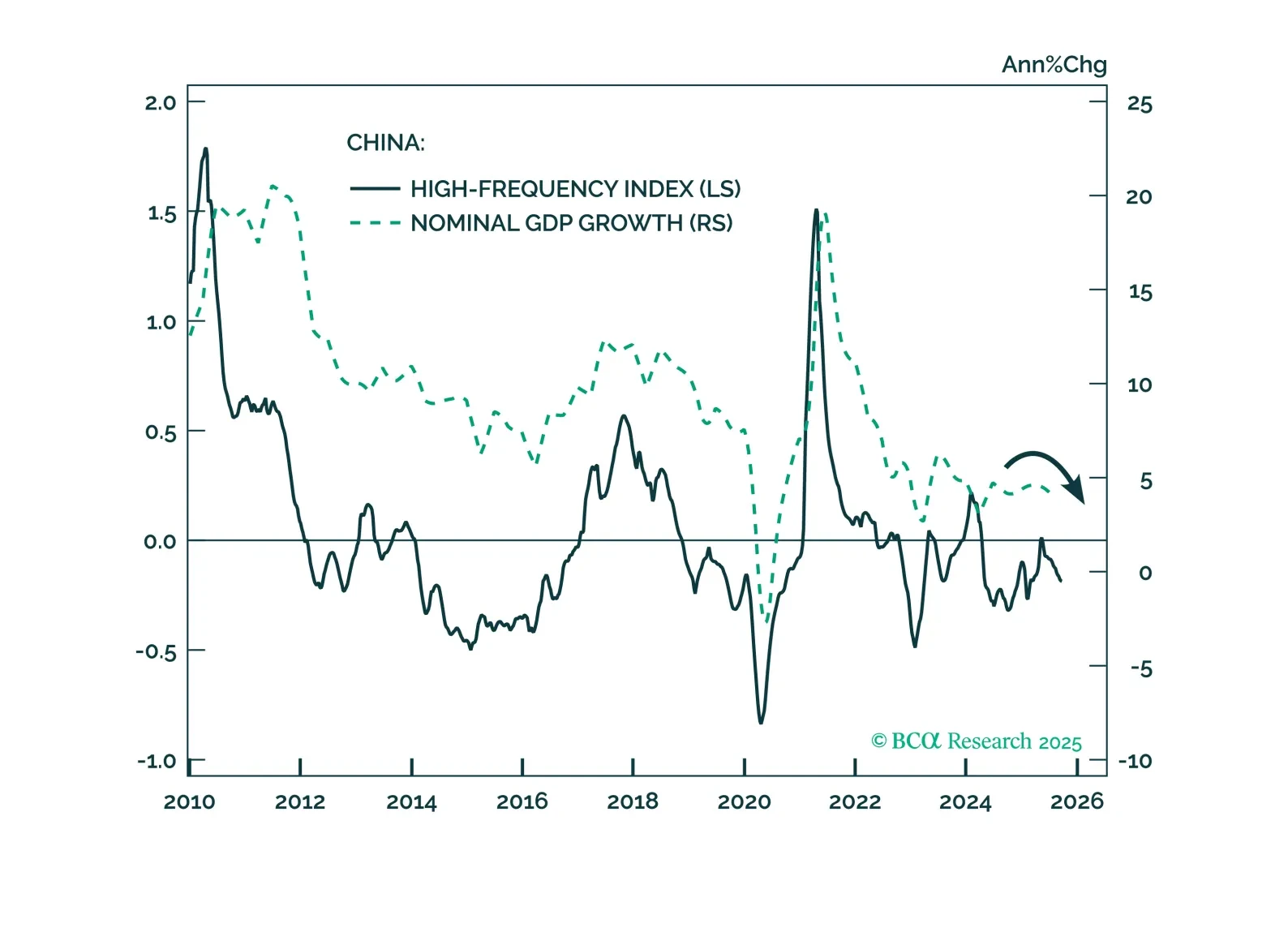

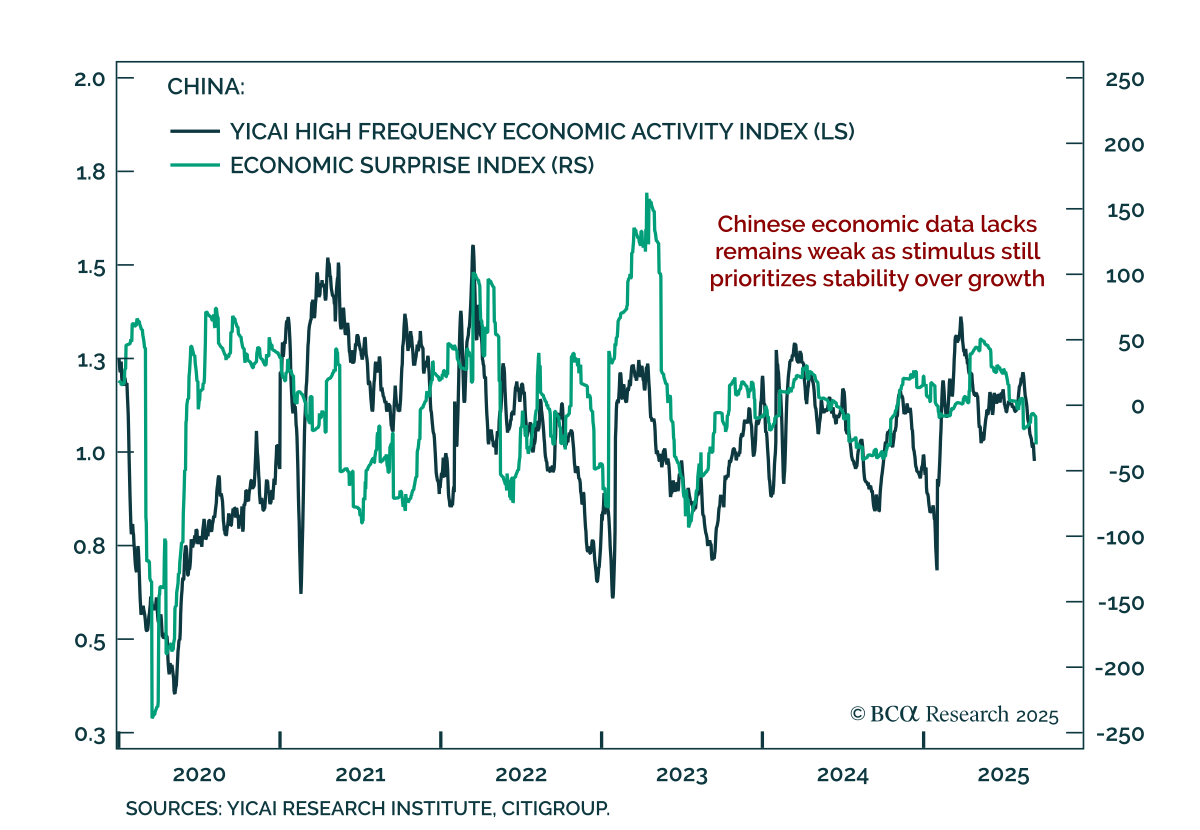

Our high-frequency indicators show China’s growth momentum weakening further in September, increasing the likelihood of new stimulus in the weeks ahead. We remain tactically cautious on Chinese equities, but strategically constructive on offshore Chinese shares.

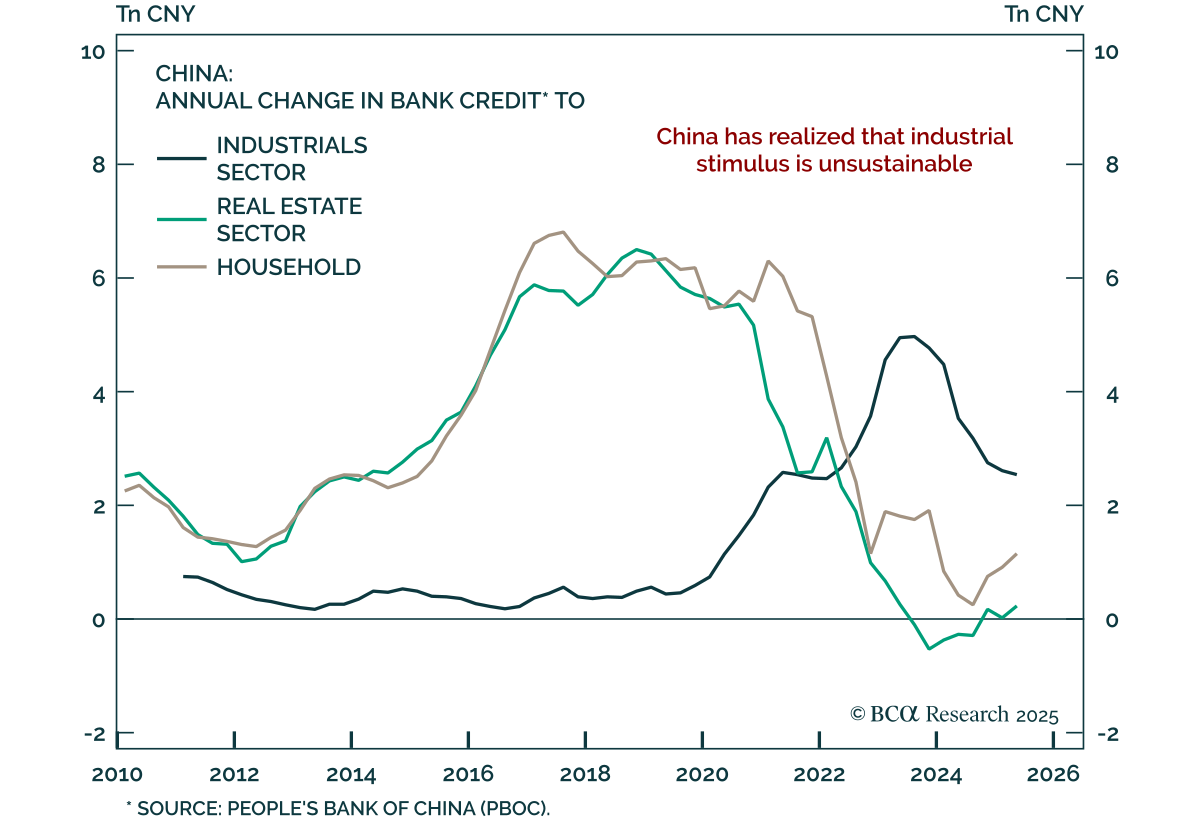

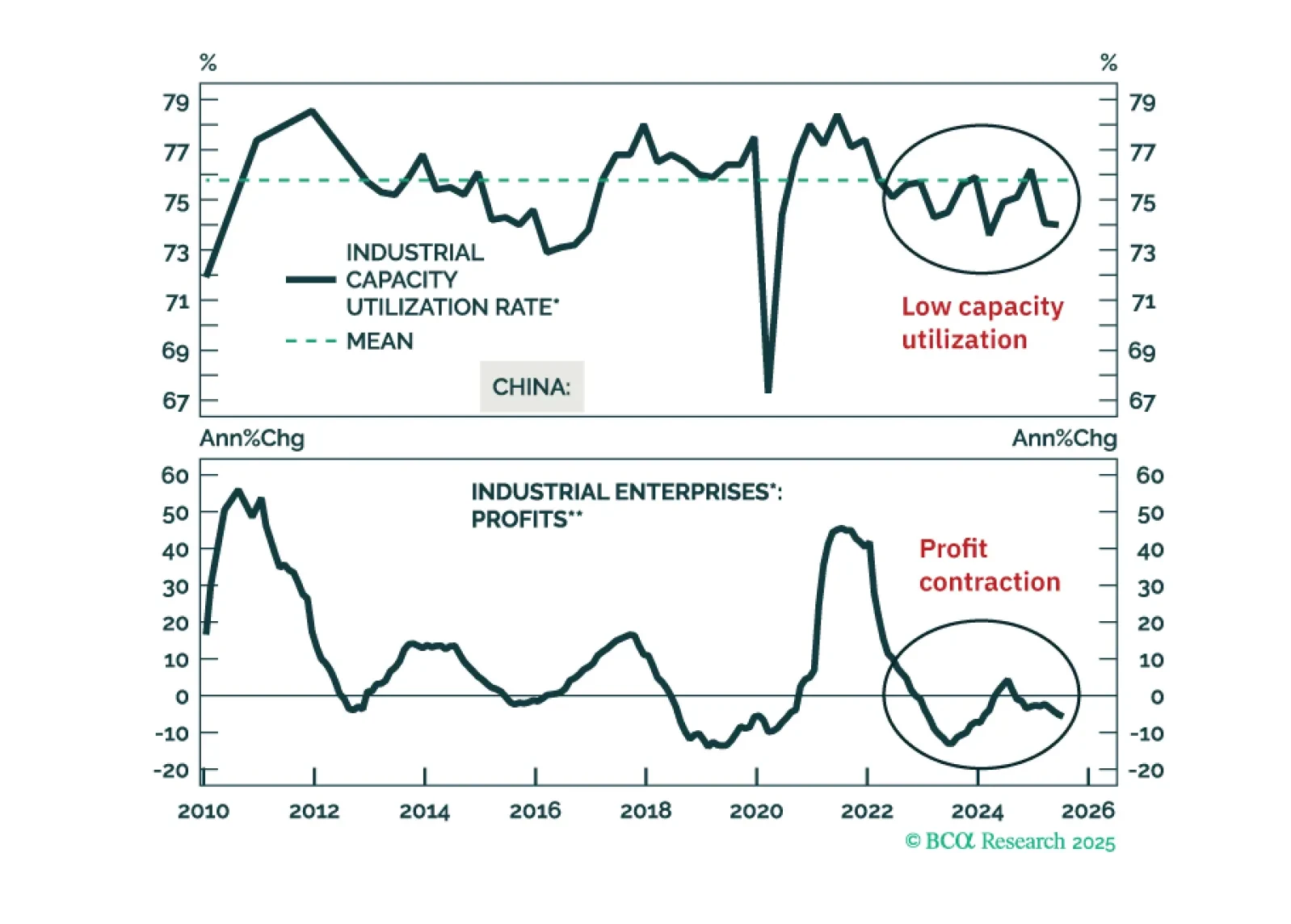

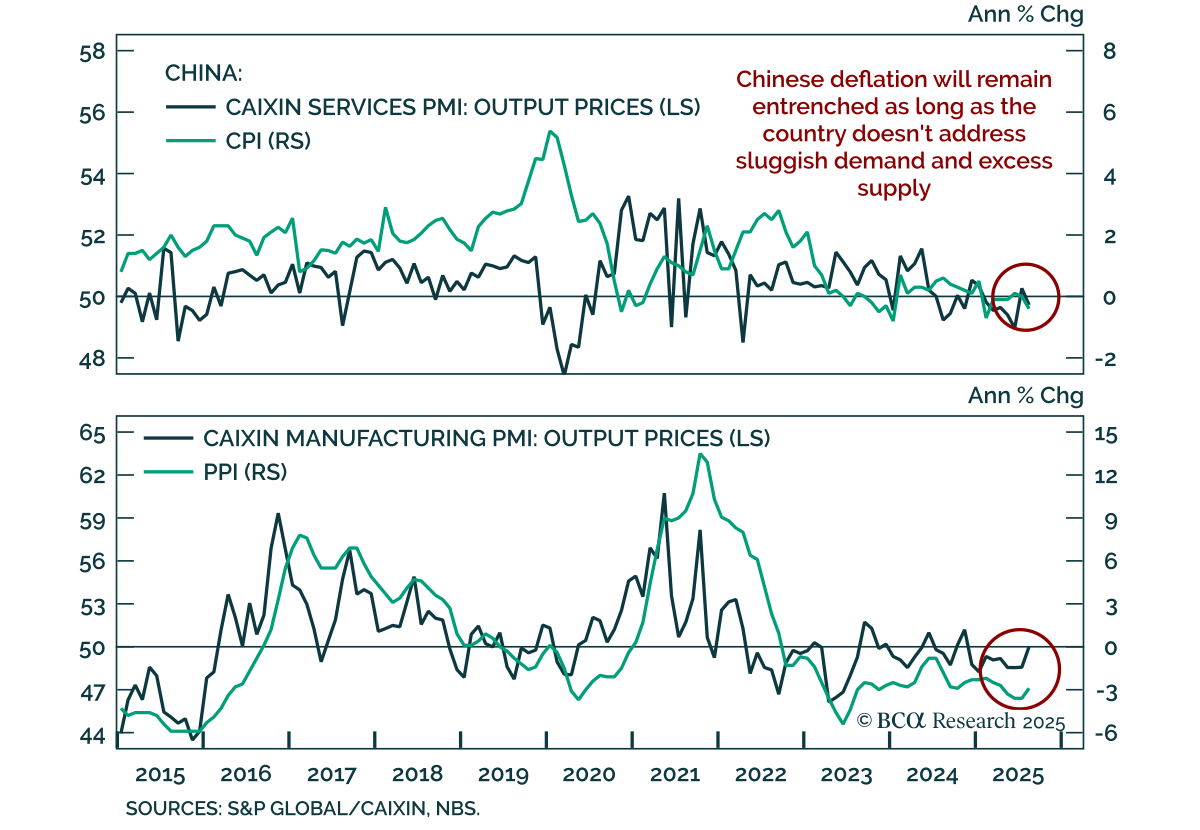

China’s policy-driven constraints prevent the “destruction” part of the creative destruction process. Instead, they entrench overcapacity, deflation, and poor profitability. We are reluctant to chase the rally in Chinese stocks in absolute terms.

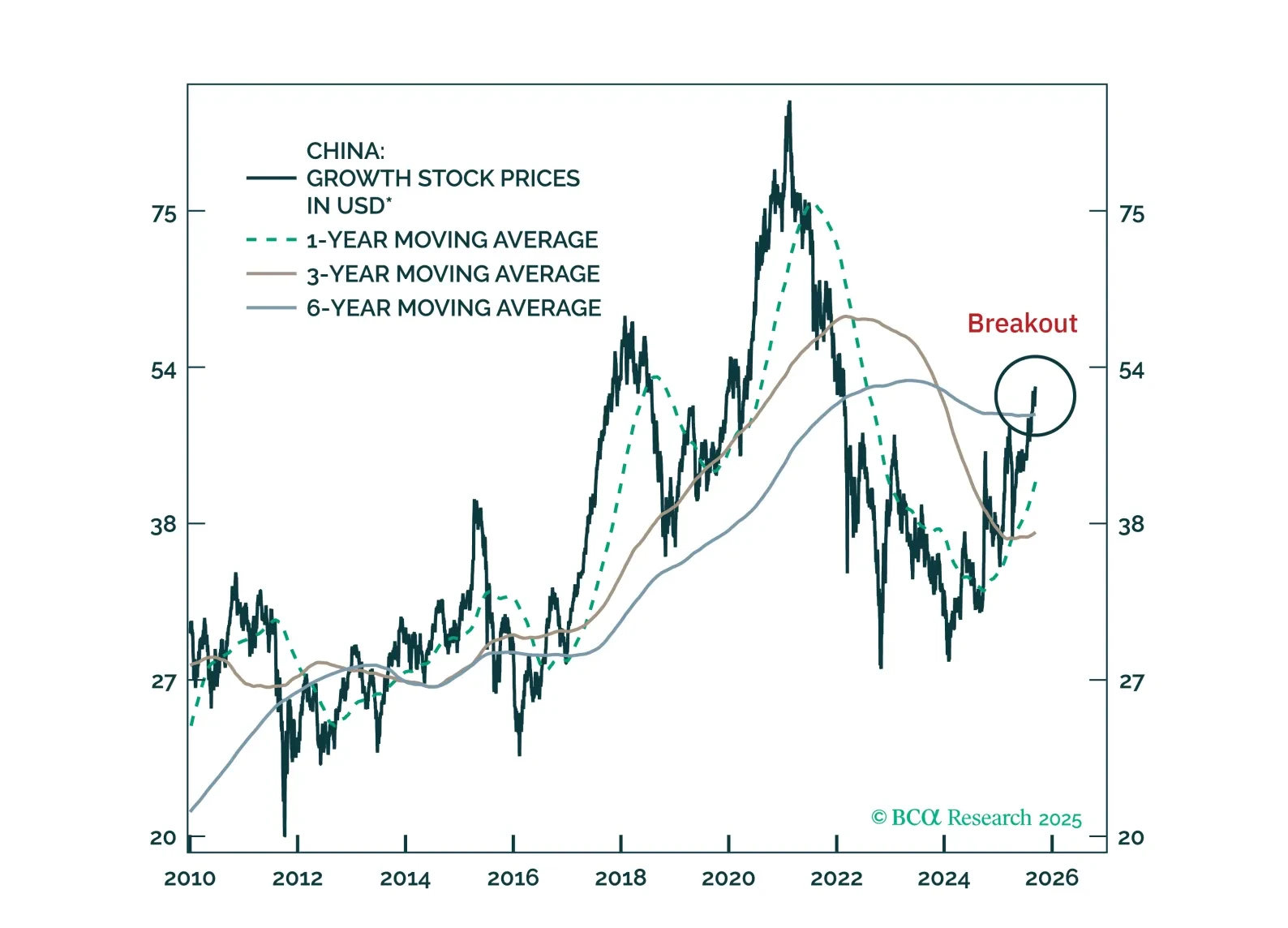

We are turning more constructive on Chinese internet stocks after several years of caution. We recommend going long offshore internet equities in absolute terms and upgrading MSCI China to overweight in a global equity portfolio.

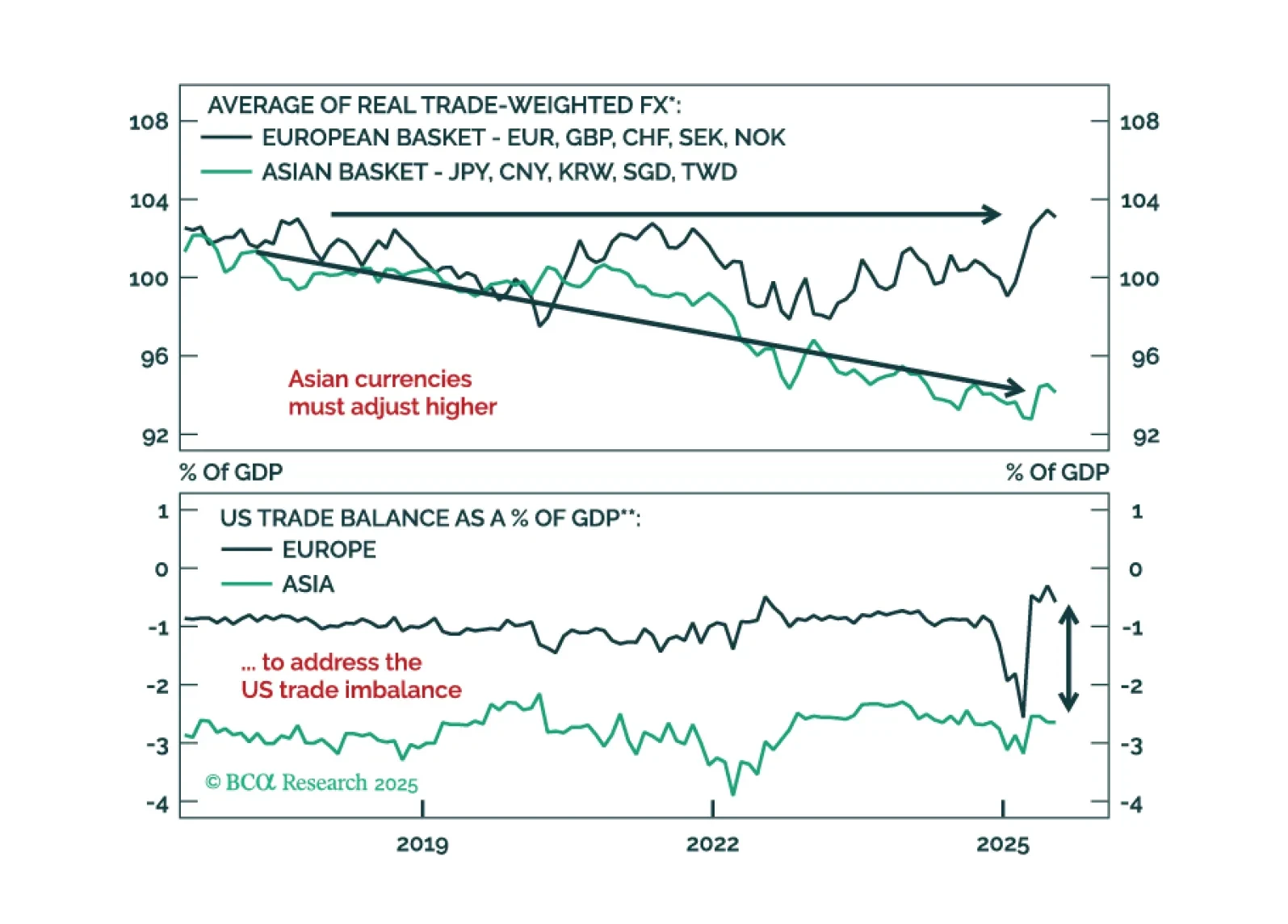

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.