China

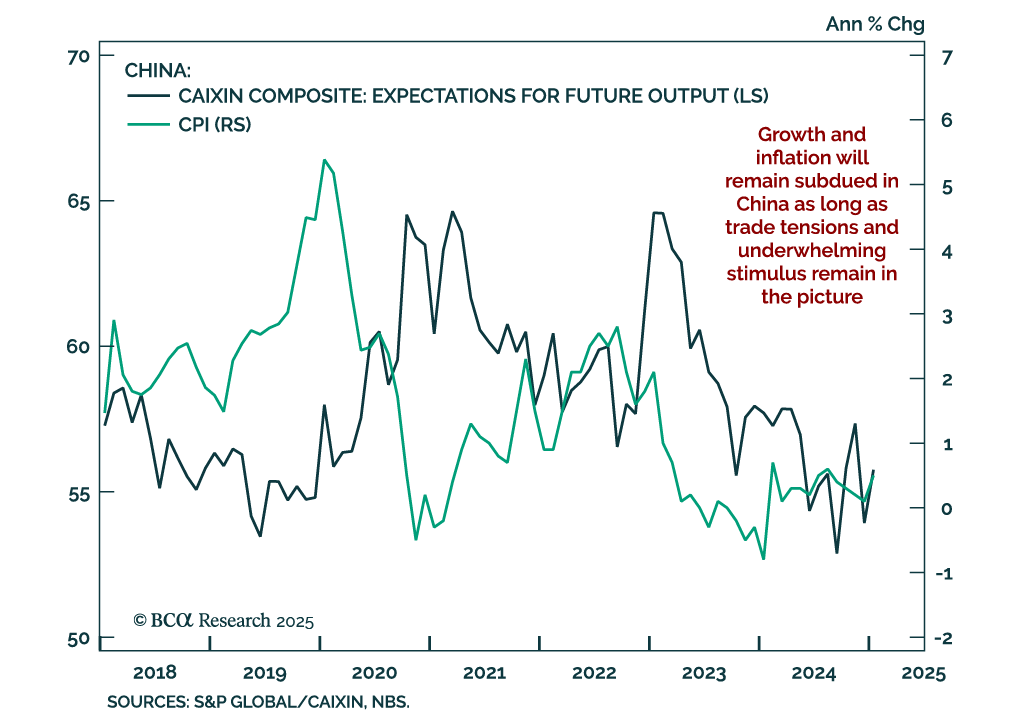

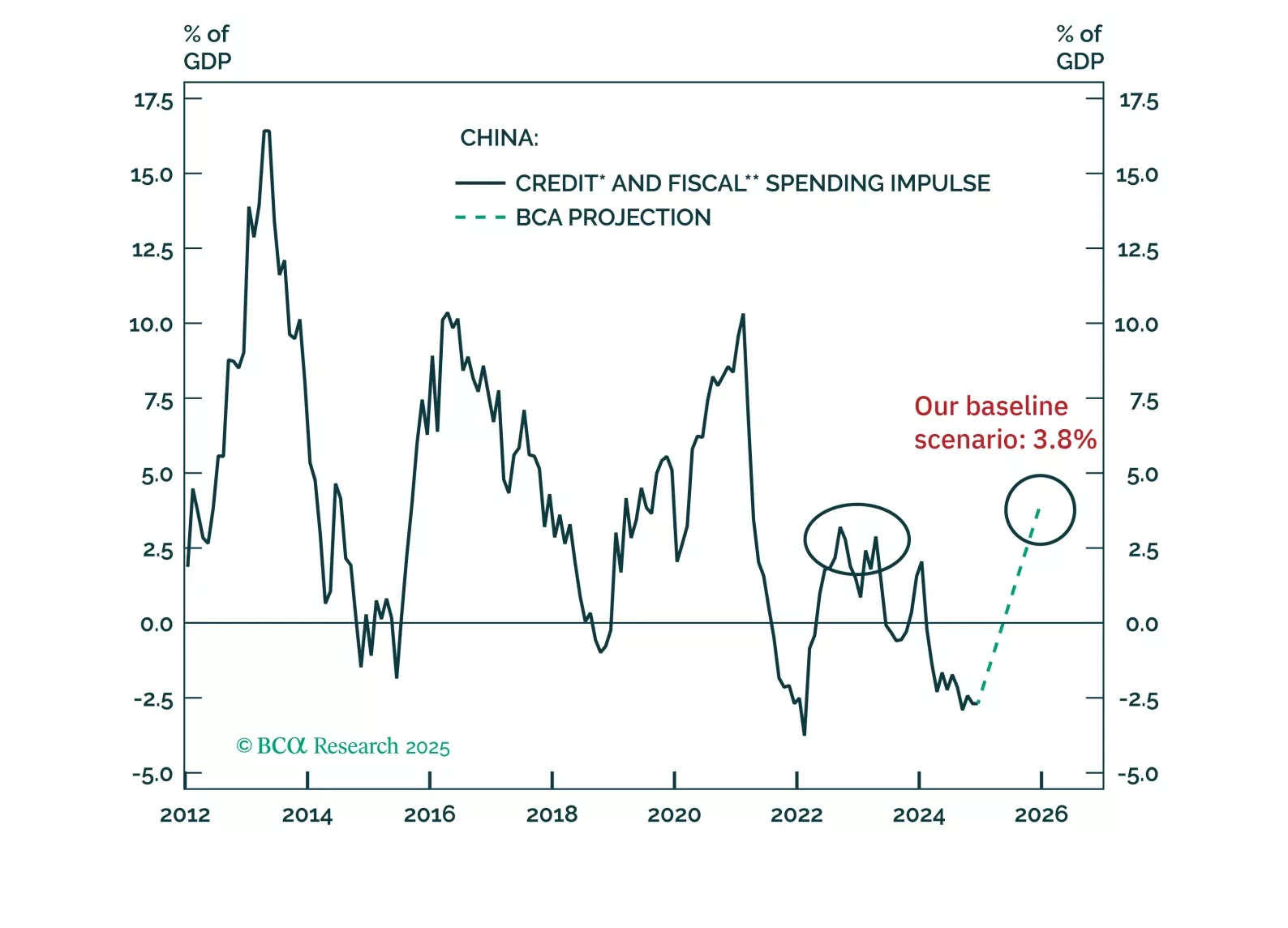

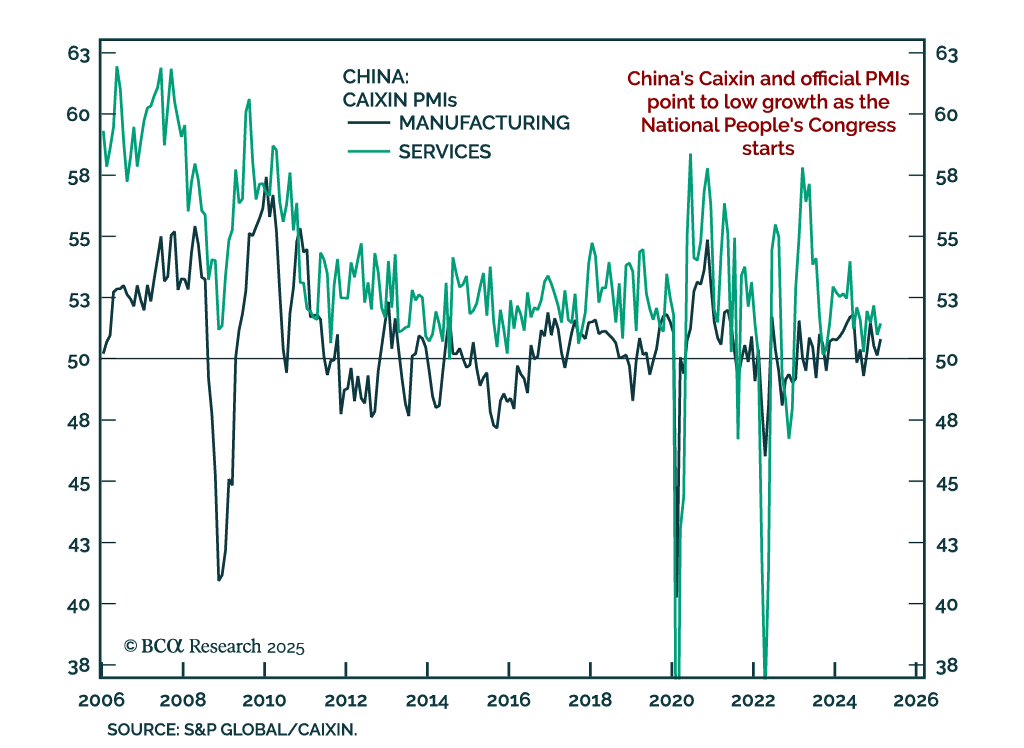

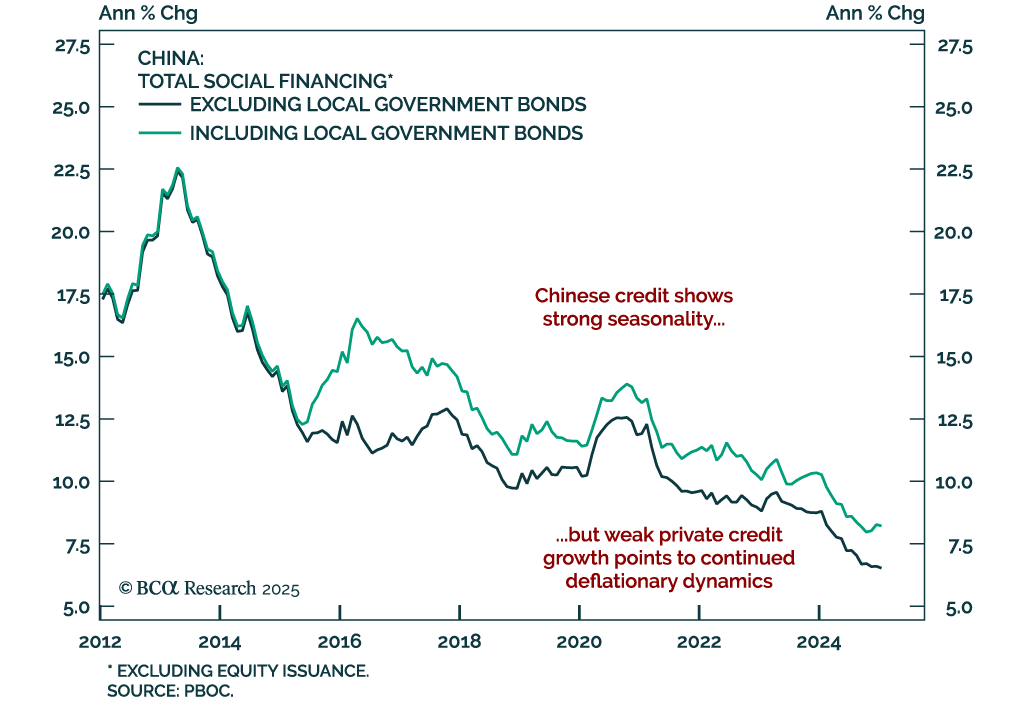

The fiscal stimulus announced at this year’s National People’s Congress is only slightly larger than last year’s. Notably, the details of the measures suggest that it will be challenging for fiscal stimulus to effectively counterbalance the country’s economic difficulties this year.

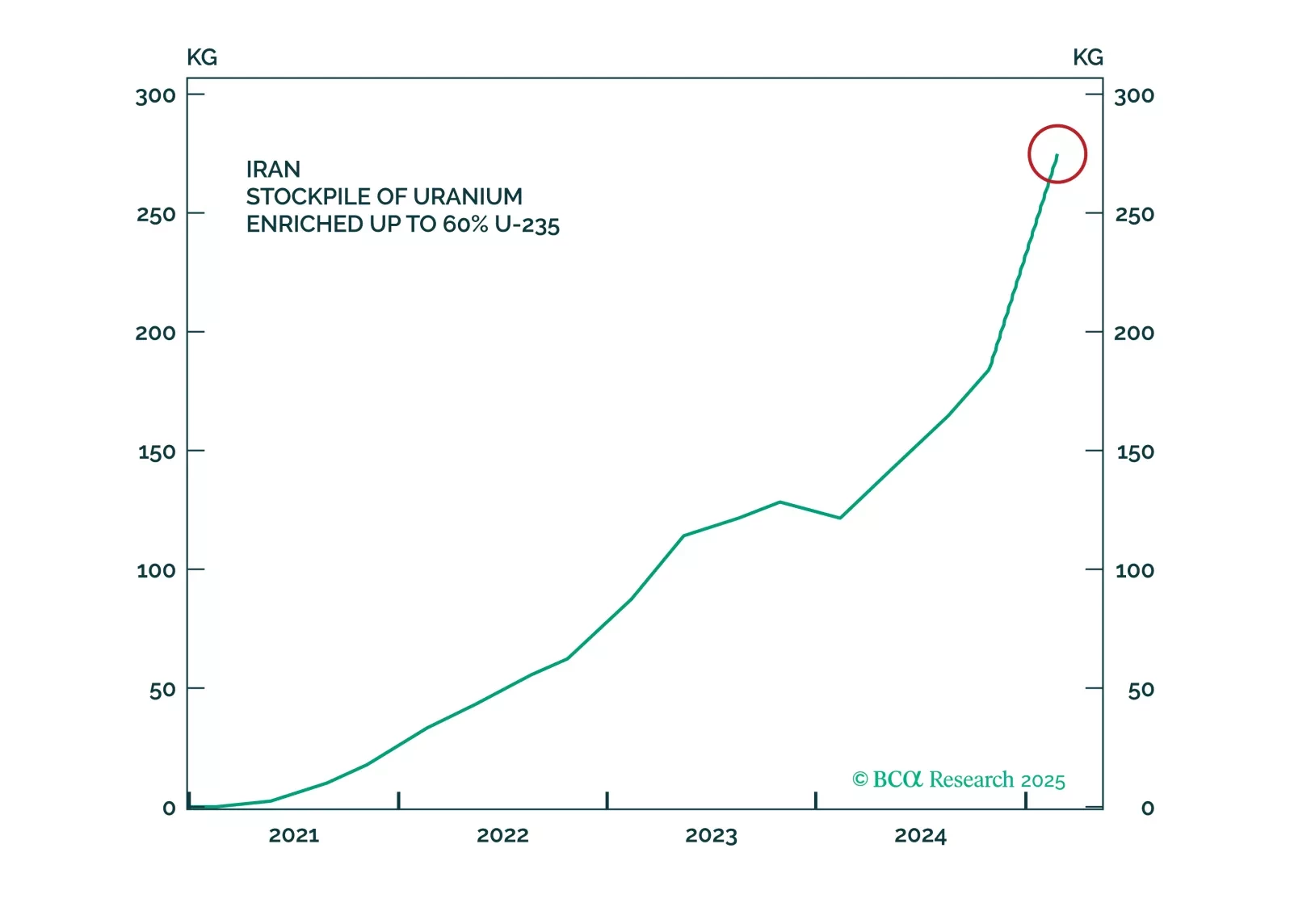

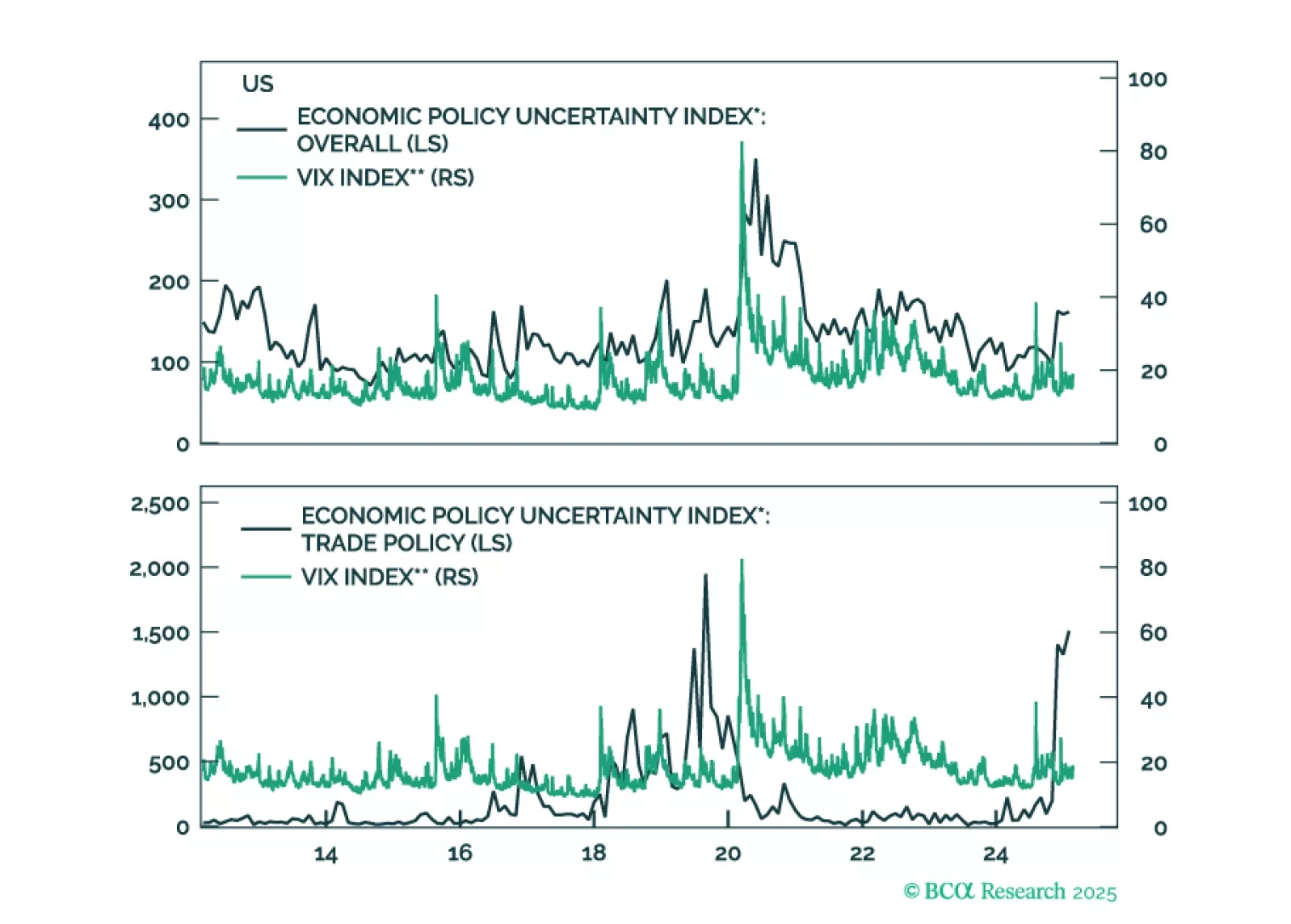

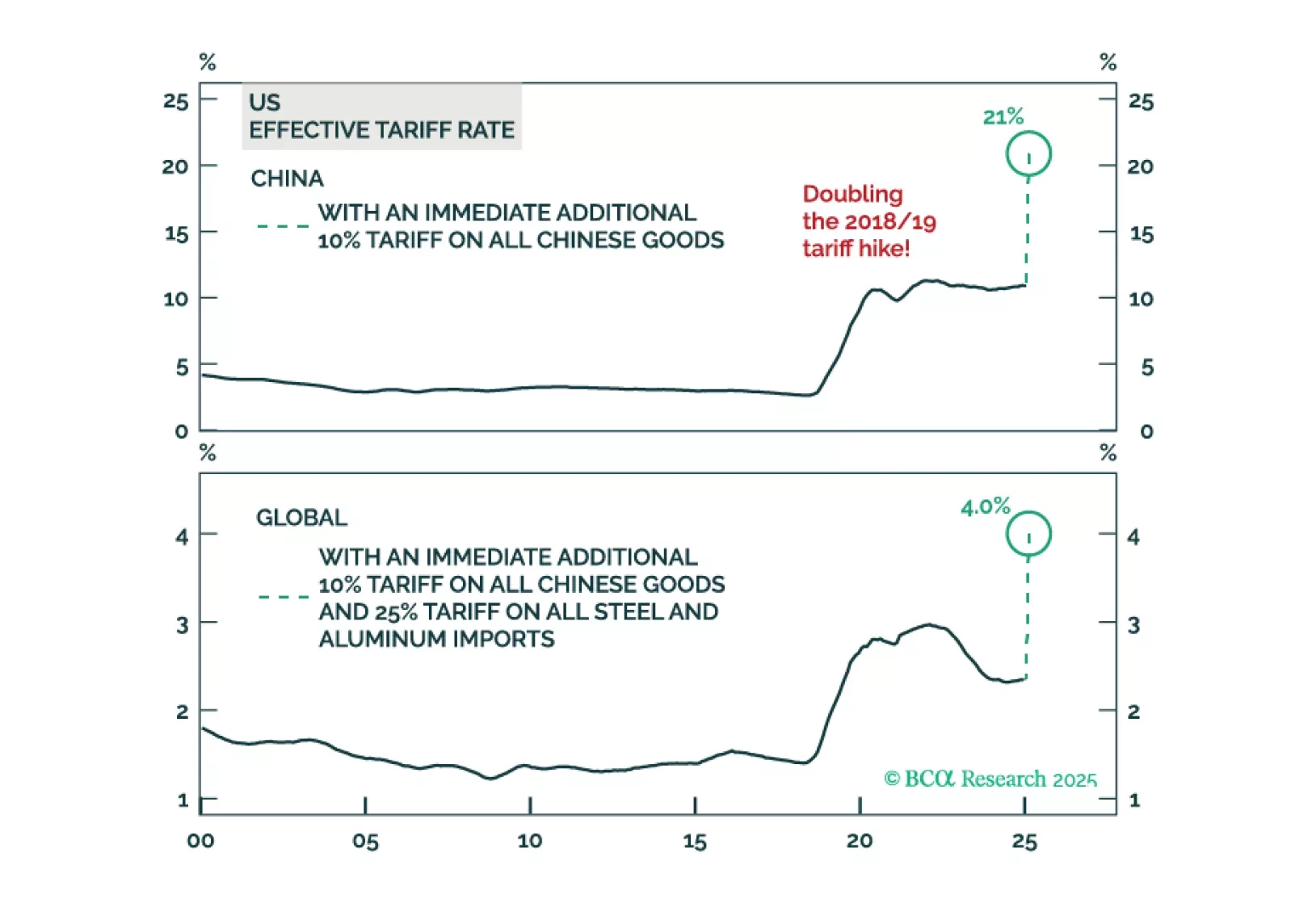

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.

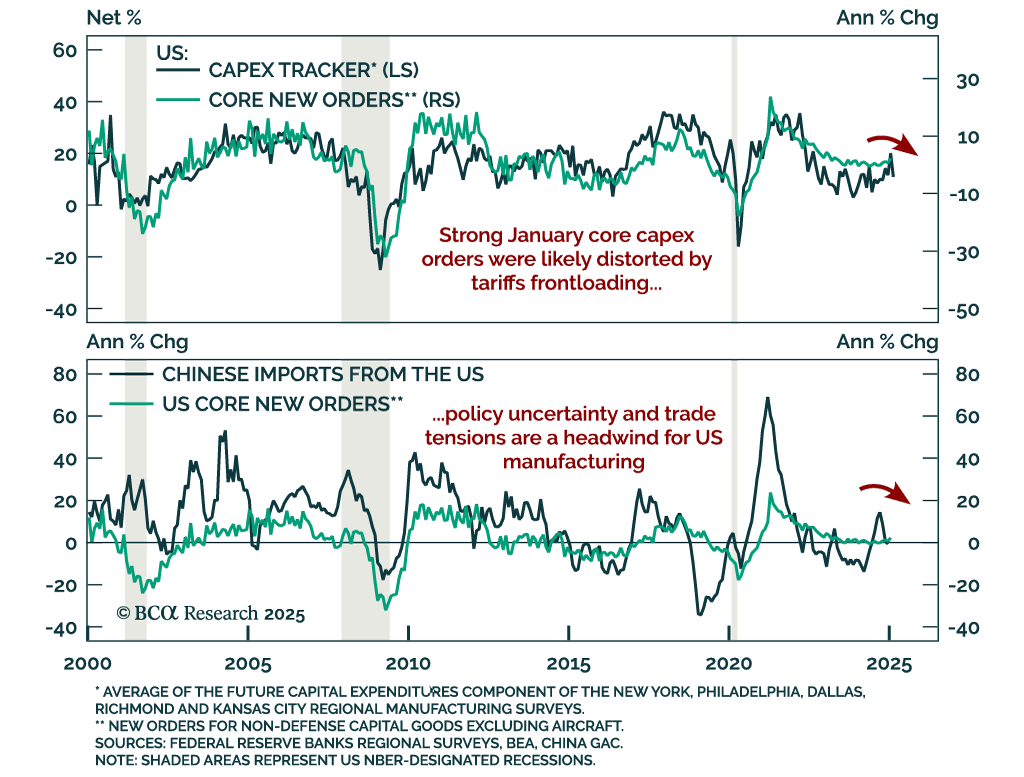

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

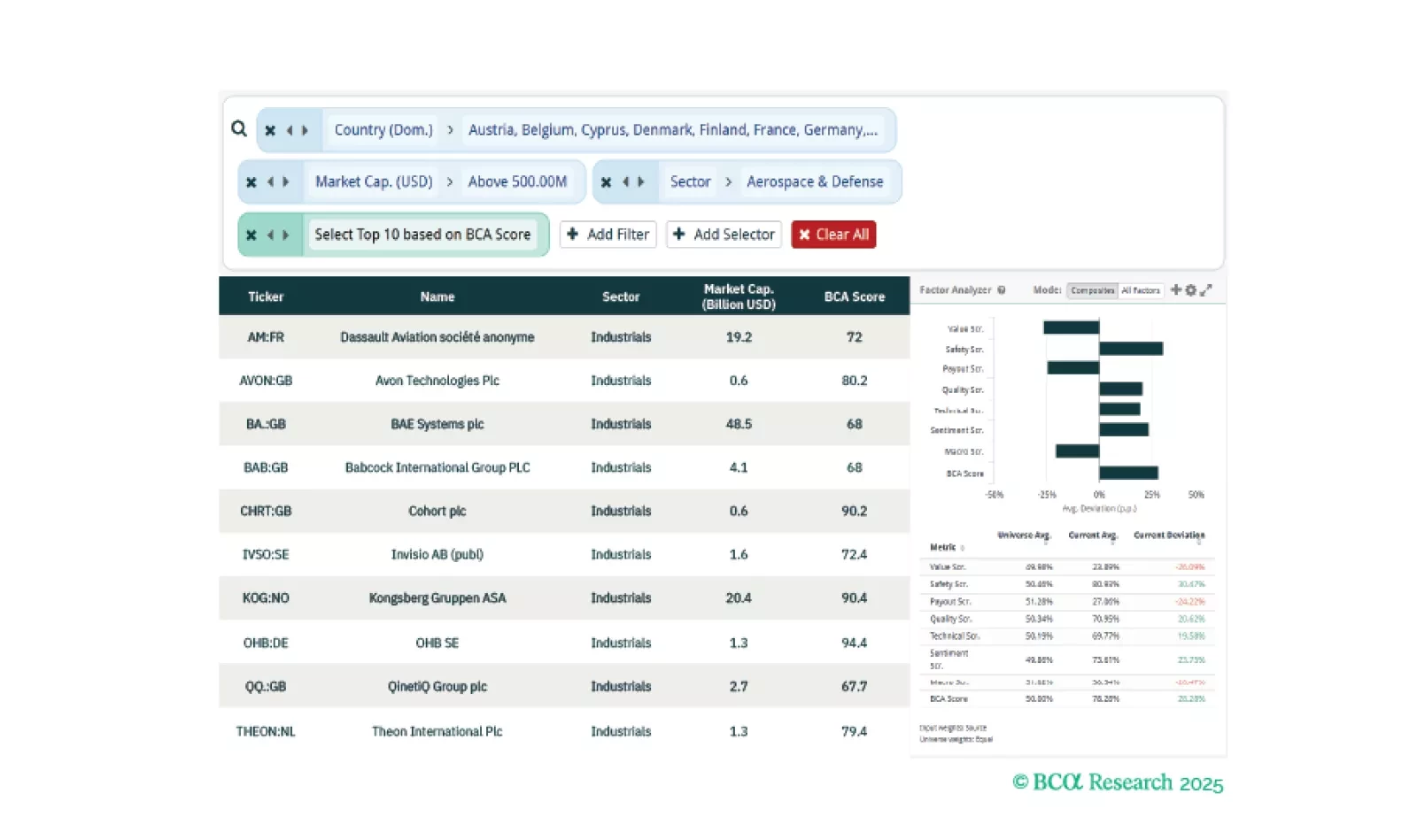

This week, our three screeners cover equity plays in European Defense, Chinese Tech, and “Boring Stocks”.

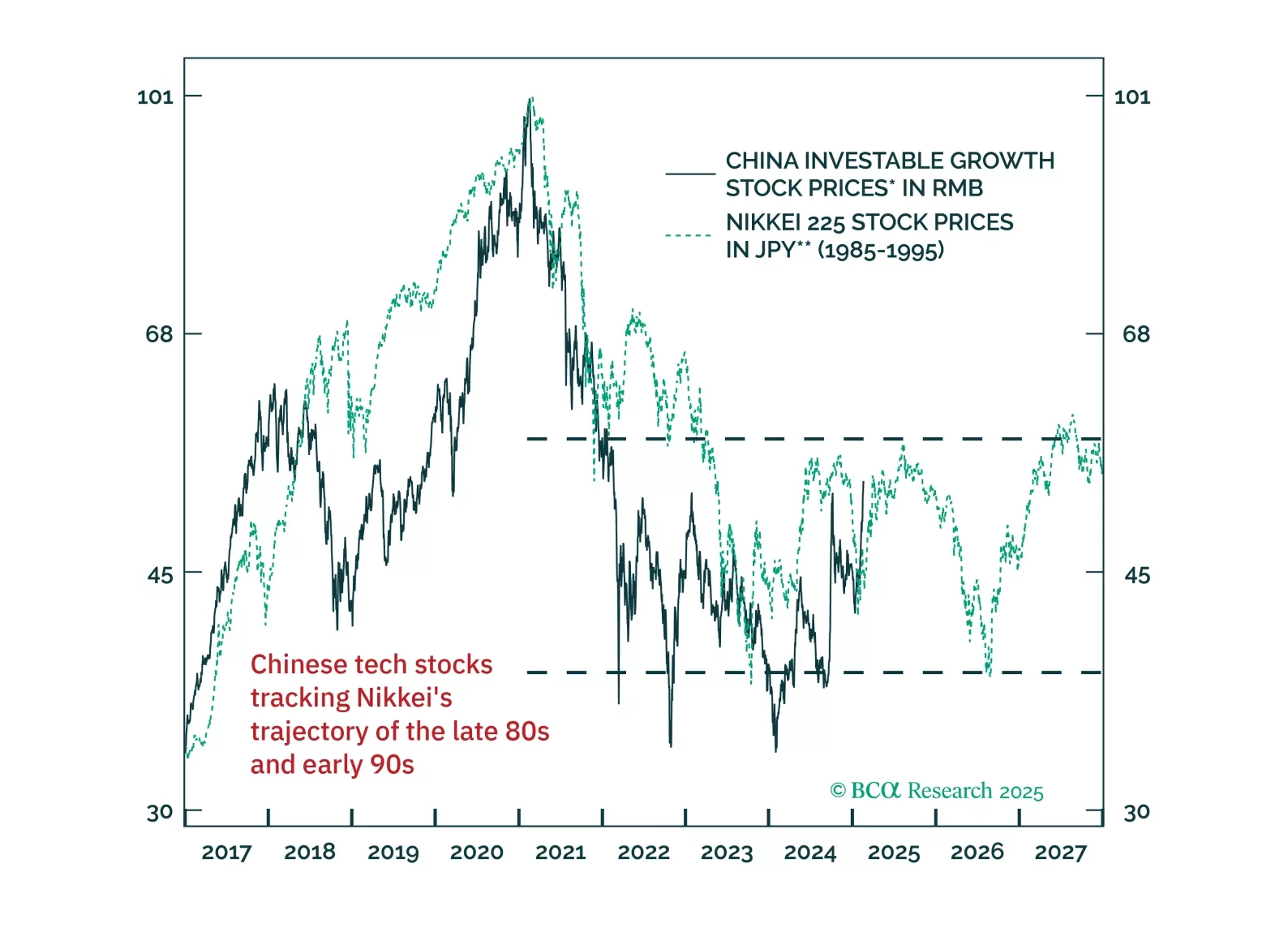

DeepSeek's AI breakthrough will likely enhance China’s productivity gains. But does it justify a re-valuation in Chinese tech stocks? Sustaining the Chinese tech rally will require corporate profits to overcome the pressures of China’s deflationary cycle. Meanwhile, DeepSeek’s innovations may fuel greater competition, intensifying price wars and putting further strain on Chinese tech companies’ profit margins.

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.