Business Cycles

The silver-to-gold ratio has surged close to 10% this year on the back of silver prices catching up to gold. Silver has returned 22% on a YTD basis, against 12% for gold, 13% for industrial metals and 5% for the broad commodity complex, making the white metal…

Corporate and junk bonds are the fixed-income sectors that are most exposed to an economic downturn. We’ve highlighted that markets continue to price in a Goldilocks scenario, with spreads narrowing despite ongoing deterioration in the labor market. Spreads…

The Caixin Chinese manufacturing PMI reached a two-year high in May, expanding at a larger-than-expected rate from 51.4 to 51.7. The Caixin figure thus contrasts with the alternative NBS manufacturing PMI, which unexpectedly contracted in May. The Caixin…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the downside in May, coming in at 100.3 from 101.9, below expectation of an acceleration to 102.1. Switzerland’s economy is highly pro-cyclical and…

According to BCA Research’s Commodity & Energy Strategy service, the oil demand forecasts from the IEA, EIA, and OPEC are too optimistic. The IEA, EIA, and OPEC all anticipate oil demand growth to slow this year following a robust post-pandemic…

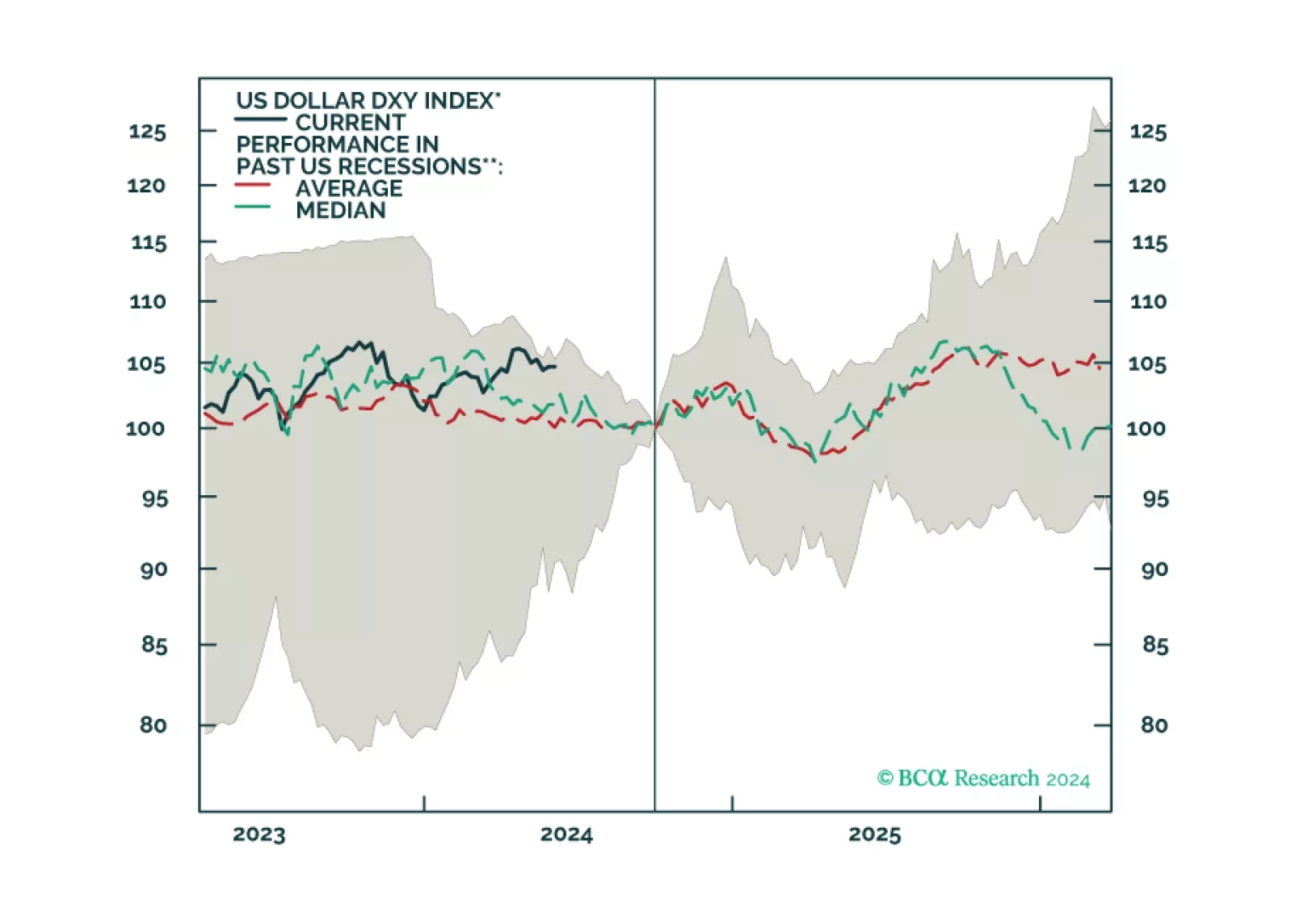

In this report, we gauge the outlook for the dollar given client visits in Africa.

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised higher. Real final sales to…

Chinese PMIs from the National Bureau of Statistics (NBS) disappointed in May. The manufacturing PMI contracted in May (49.5), breaking a two-month expansion streak and disappointing expectations of continued growth. Meanwhile, the services sector PMI…

Euro Area CPI accelerated for the first time this year from 2.4% y/y to a faster-than-expected 2.6% y/y in May. Preliminary estimates also suggest that core CPI accelerated from 2.7% y/y to 2.9% y/y, against expectations of a constant growth rate. …

According to BCA Research’s US Political Strategy service, Trump’s conviction will not be a game changer in the upcoming Presidential election. President Trump was convicted of 34 felony charges by a 12-person jury in a New York state court on May 30 for…