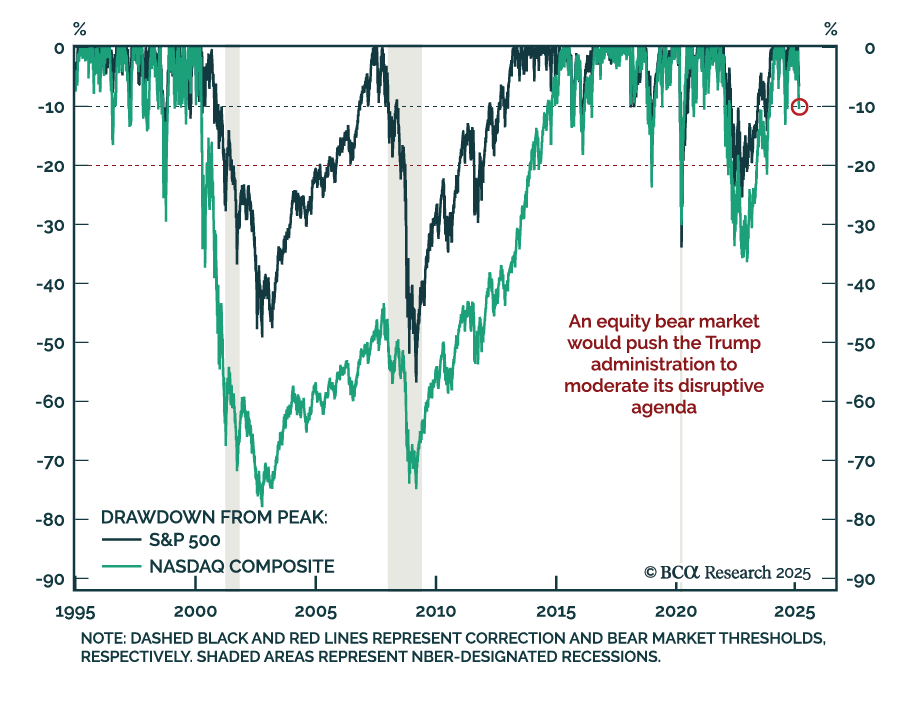

Bear/Bull Market

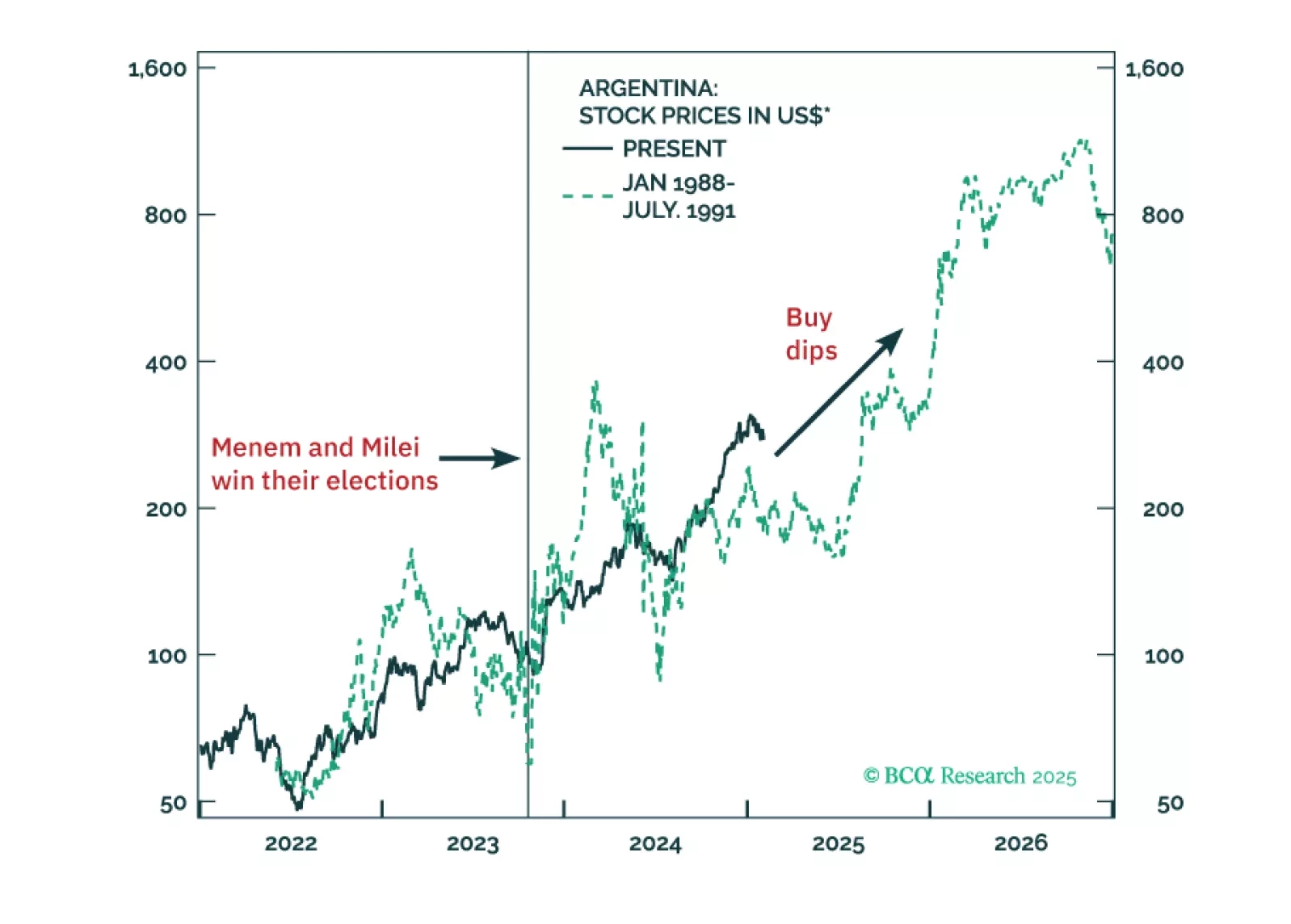

Argentina is entering a regime shift from the traditional short boom-bust cycles of the past 50 years. Profound structural reforms will result in a productivity boom, leading to a more durable economic expansion while keeping with the disinflation trend. Authorities will likely lift capital and currency controls in the second quarter of this year. All in all, odds are that Argentinian assets have entered a multi-year bull market.

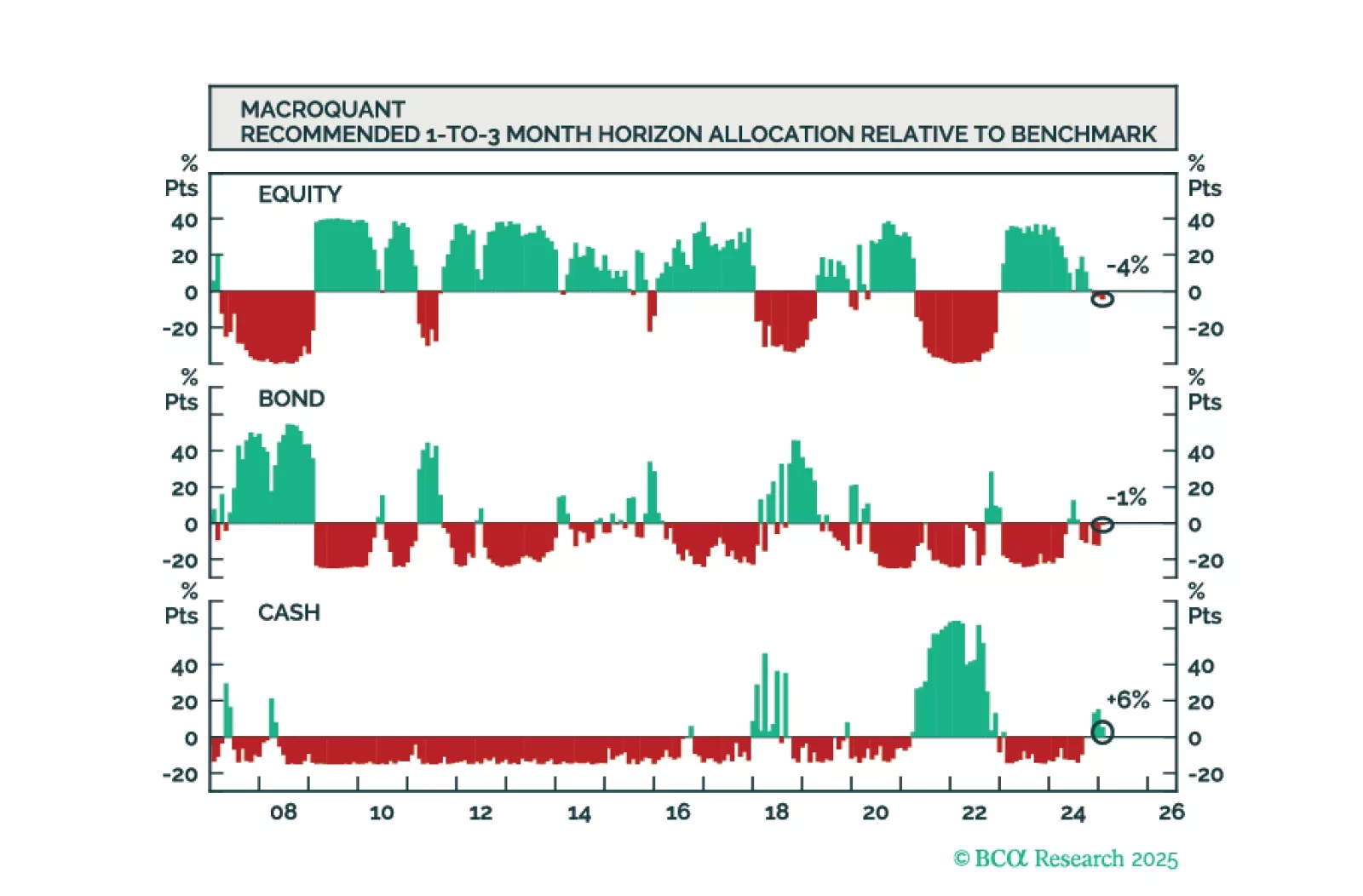

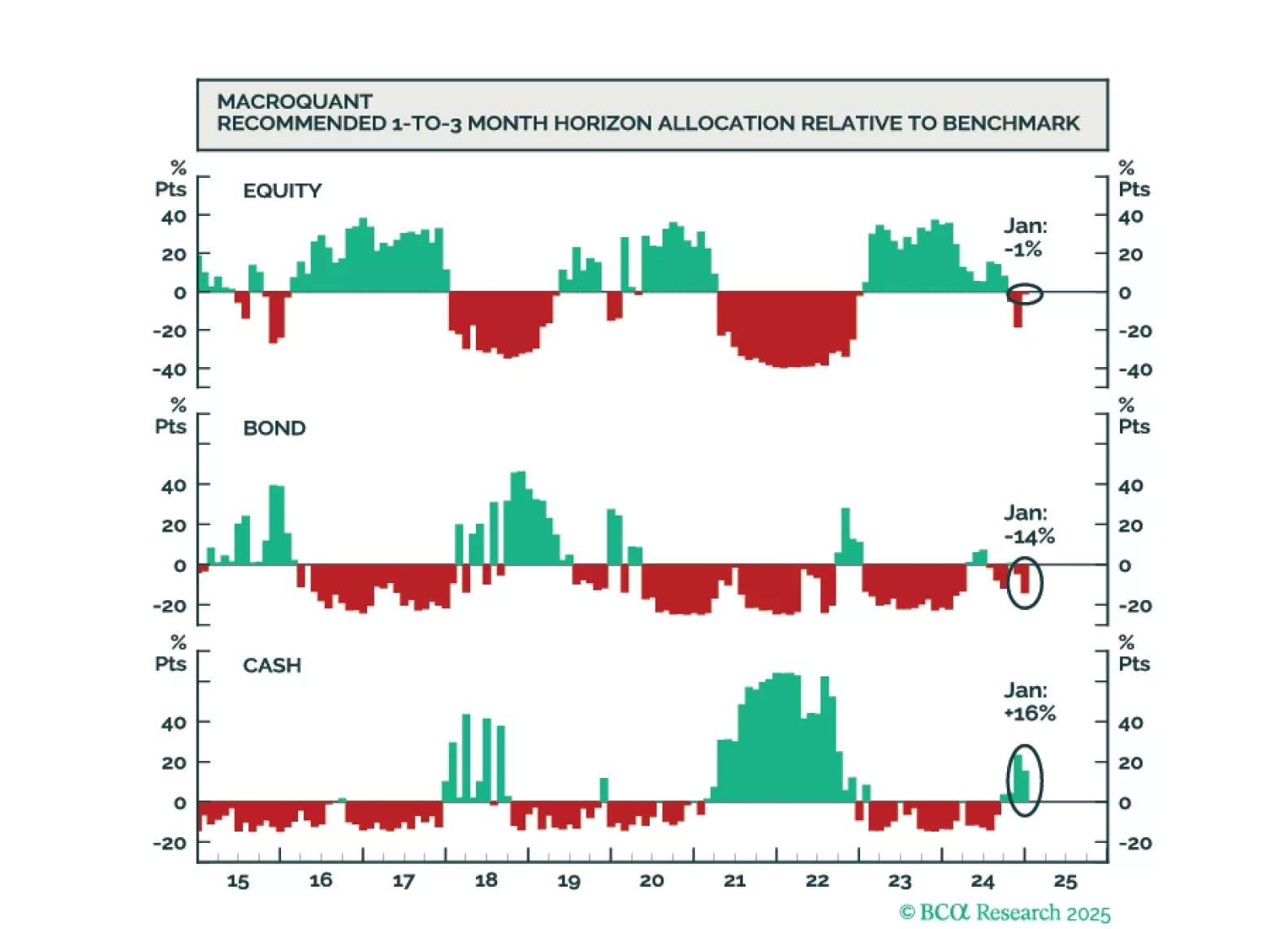

While the US economy could remain upright on the tightrope for a while longer, it will inevitably fall, leading to a major bear market in stocks. We will be looking to our MacroQuant model for guidance on when to turn fully defensive. We are not there yet.

The month of November has brought us S&P 6,000! President Trump has won a “Red Sweep” (as we expected all year) and has ushered in a regime change in America. For now, we are open to chasing momentum. However, the biggest risk to the market are bond yields, which should rise as investors start to price President Trump’s policies and their impact on deficits.

The prospect of a new trade war more than offsets the other pro-business parts of Trump’s agenda. With the labor market already weakening going into the election, we are raising our 12-month US recession probability from 65% to 75%.

After resisting the consensus narrative in 2022 that a US recession was imminent, and then predicting an immaculate disinflation for 2023, the Global Investment Strategy team has joined the dark side and is now expecting a recession to start in the US within the next six months. Accordingly, we recommend that investors underweight stocks and overweight government bonds.