Base Metals & Iron Ore

We share the edited transcript of a webinar we participated in discussing global trade, trade wars and tariffs, as well as de-risking strategies.

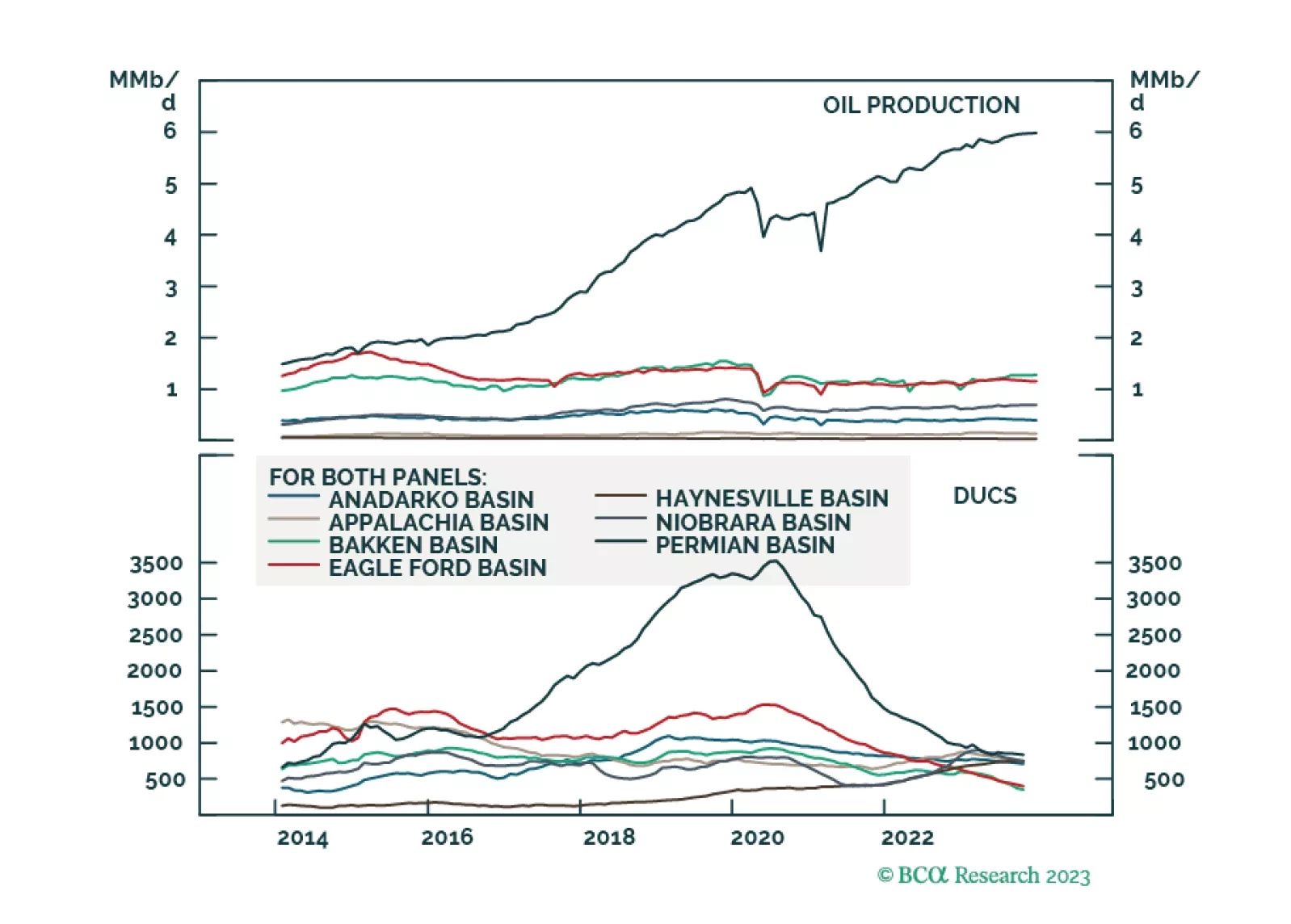

Political economy dominates fundamentals going into 2024, as states prepare for war and de-risk supply chains. Asynchronous global growth will elevate commodity-price volatility. We expect oil to trade above $100/bbl in 2024 and continue to favor equity exposure to oil-and-gas producers. Given weak capex, we also favor metals miners and refiners. We remain long the Gold, the XME and COMT ETFs We were stopped out of our XOP ETF with a 12.5% gain; we will re-establish it at tonight’s close.

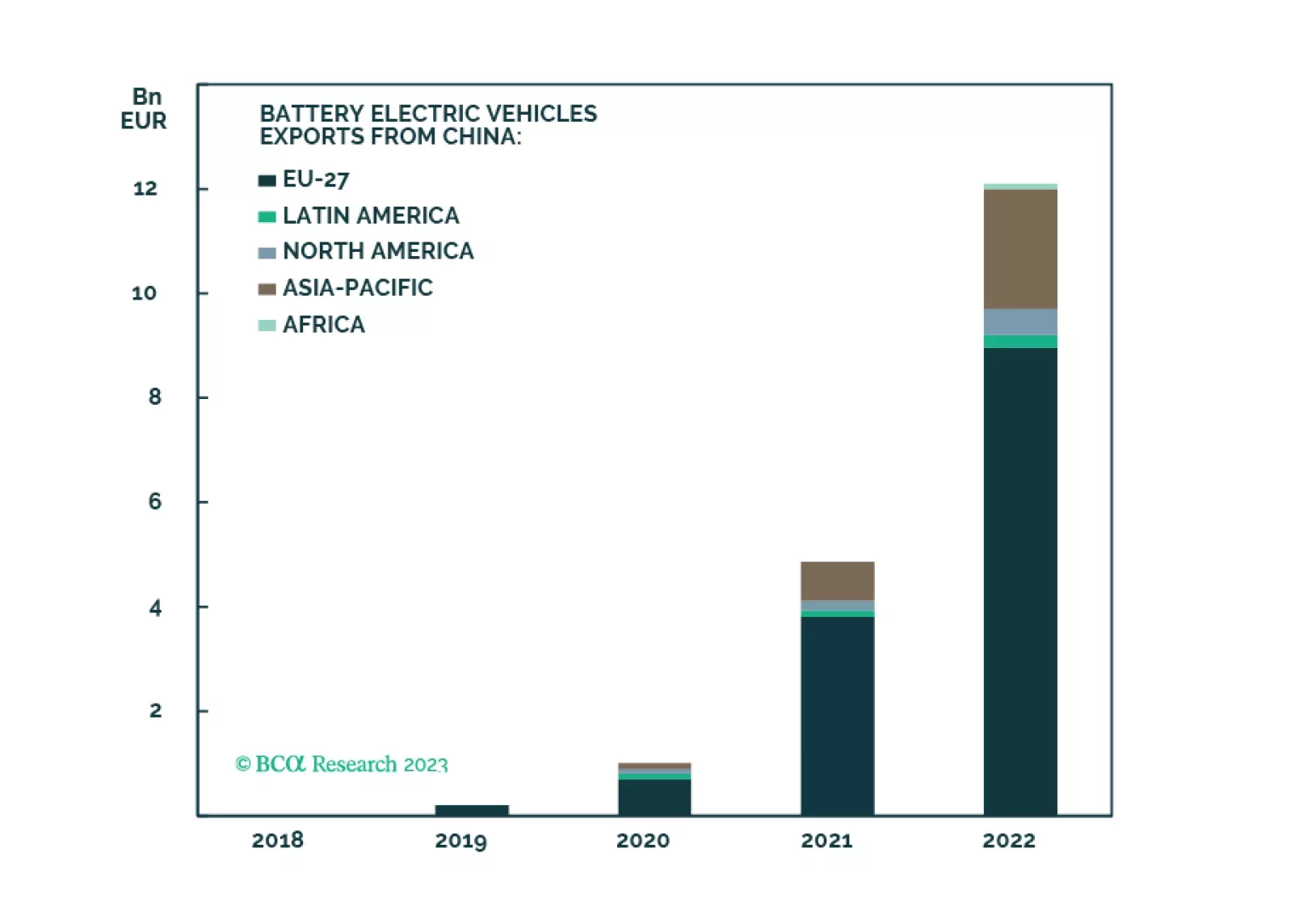

China’s push to dramatically expand its copper-refining capacity will be complemented by further vertical integration of mining assets. However, surplus refining capacity will push treatment and refining charges lower in the short run. The threat of EU tariffs on Chinese EV imports looms large, and could be costly to China’s expansion of its already-dominant supply-chain ecosystem for EVs and metals refining. We remain long the XME and COMT ETFs to retain exposure to metals miners and refiners.

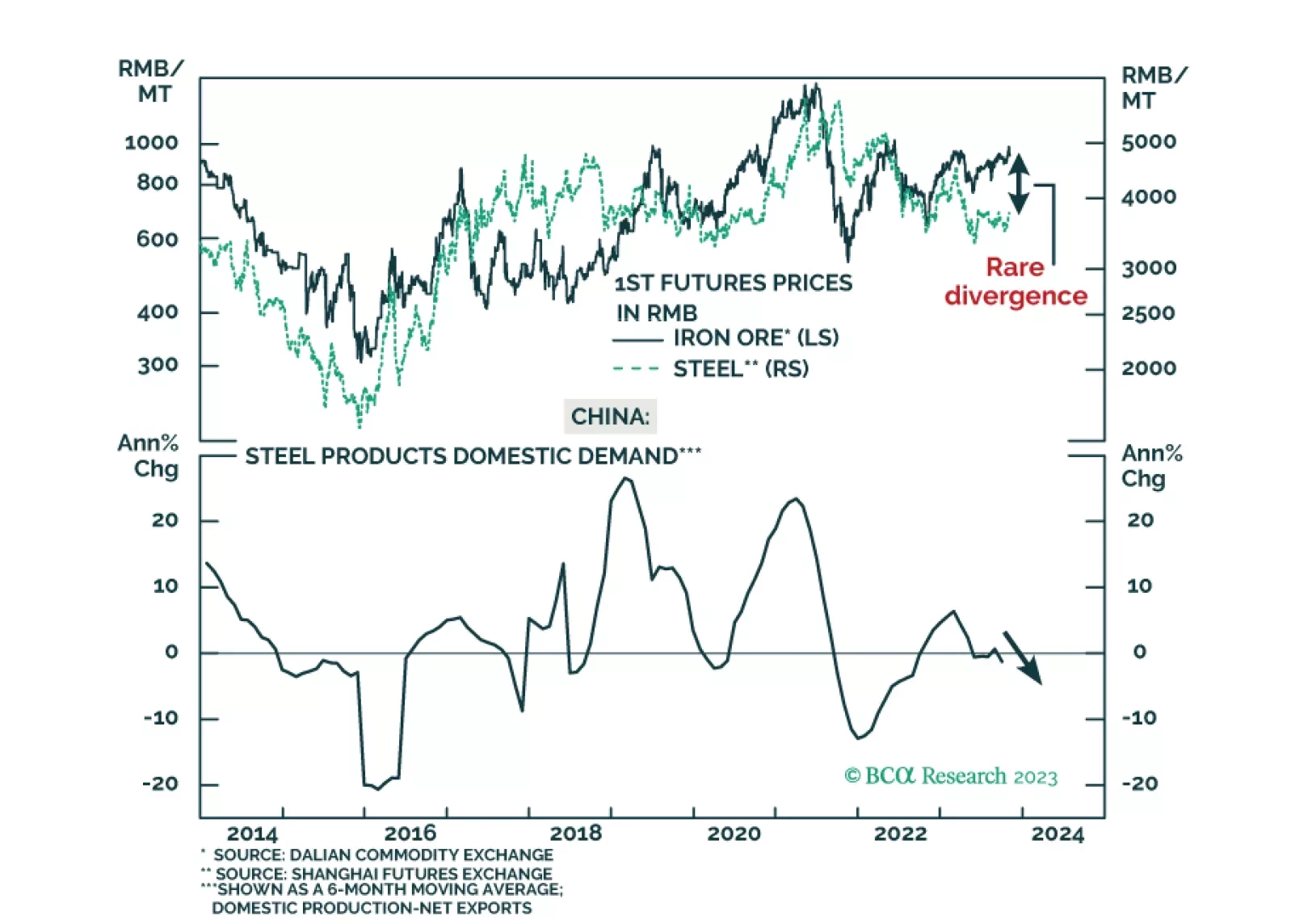

Increasing iron ore prices coupled with declining steel prices represent an unsustainable disparity. Iron ore prices will pivot downward in the next six months. A sizeable reduction in China’s steel production will likely occur, reducing global iron ore demand. Meanwhile, global iron ore supply will increase moderately.

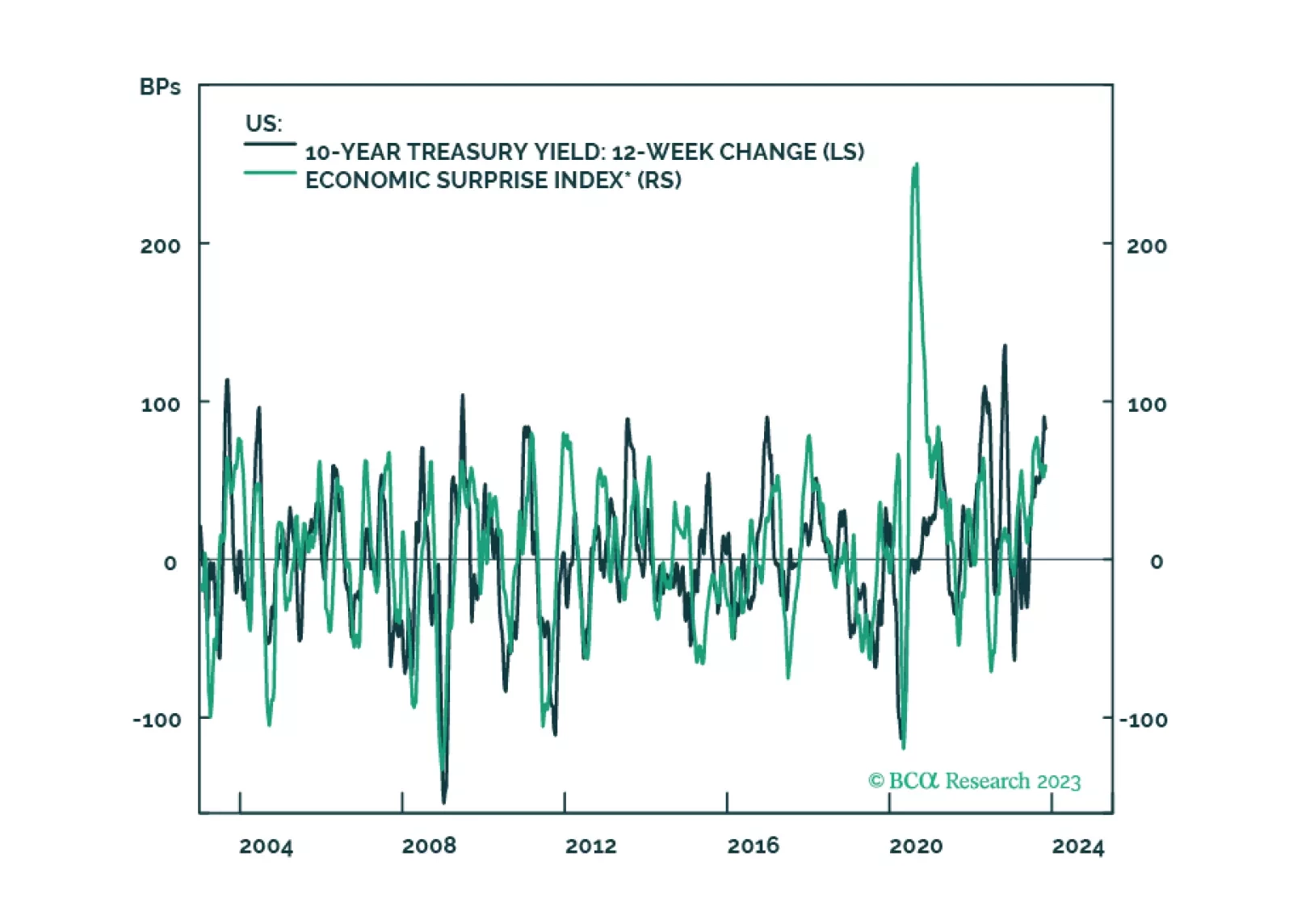

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.