BCA Indicators/Model

We maintain our 12-month US recession probability at 60%. However, until the “whites of the recession’s eyes” are more clearly visible, we would refrain from moving to a fully defensive stance.

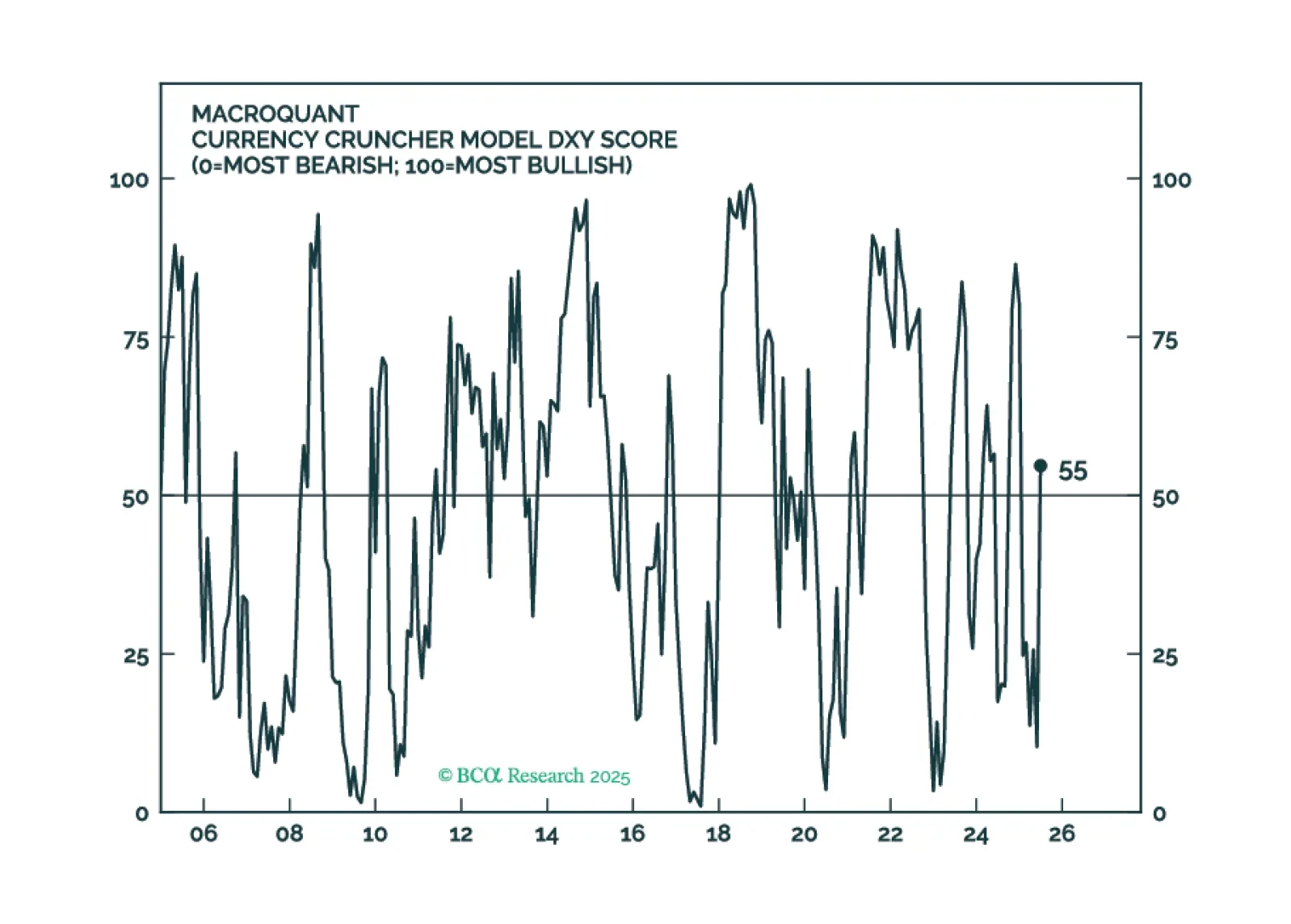

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

We apply a systematic approach to investing based on economic, inflation, and monetary policy surprises to the foreign exchange market. The signals from this framework are broadly consistent with the tactical views of our FX strategists, which anticipate a pause in the USD’s decline and a partial reversal of the recent euro strength.

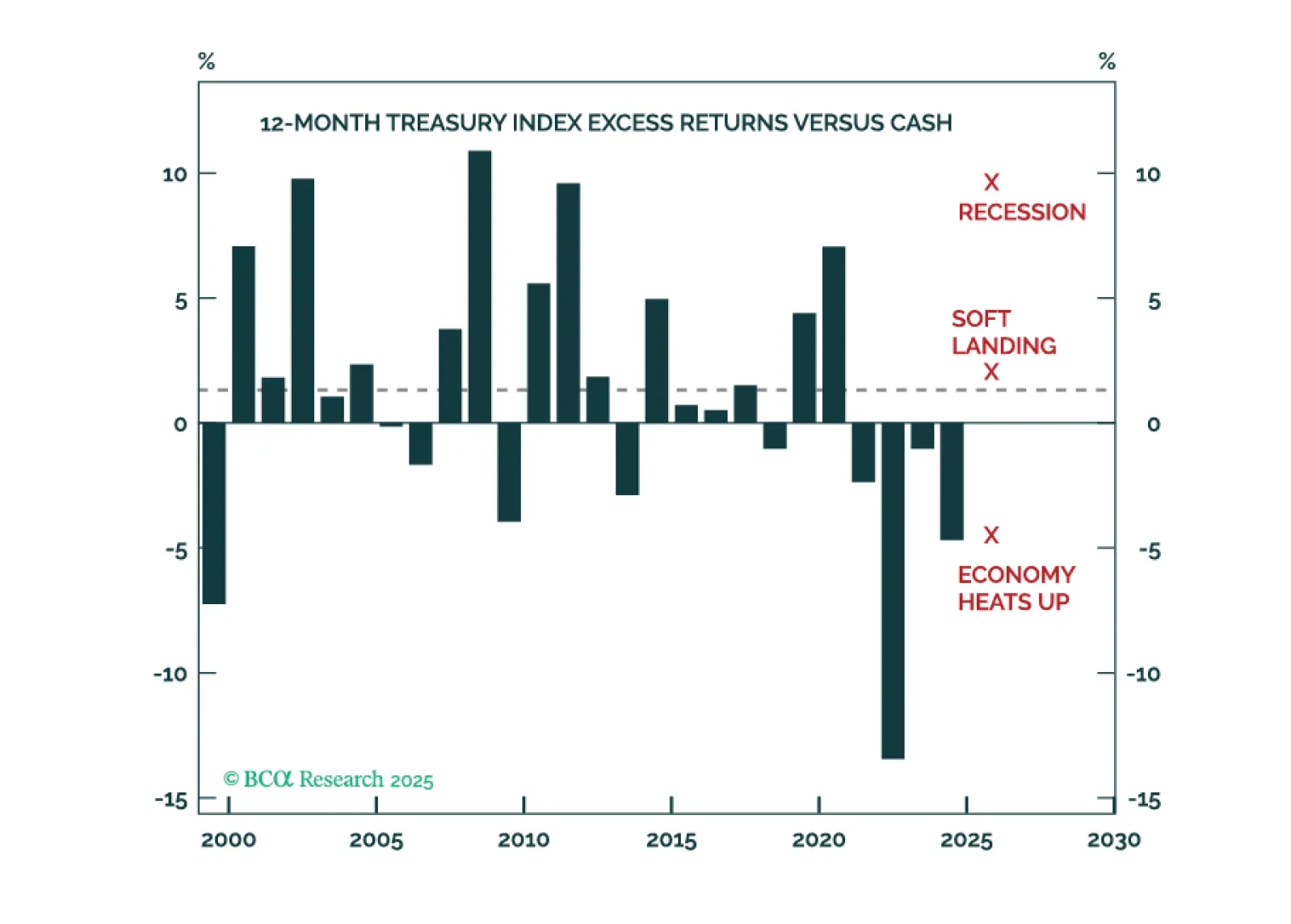

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

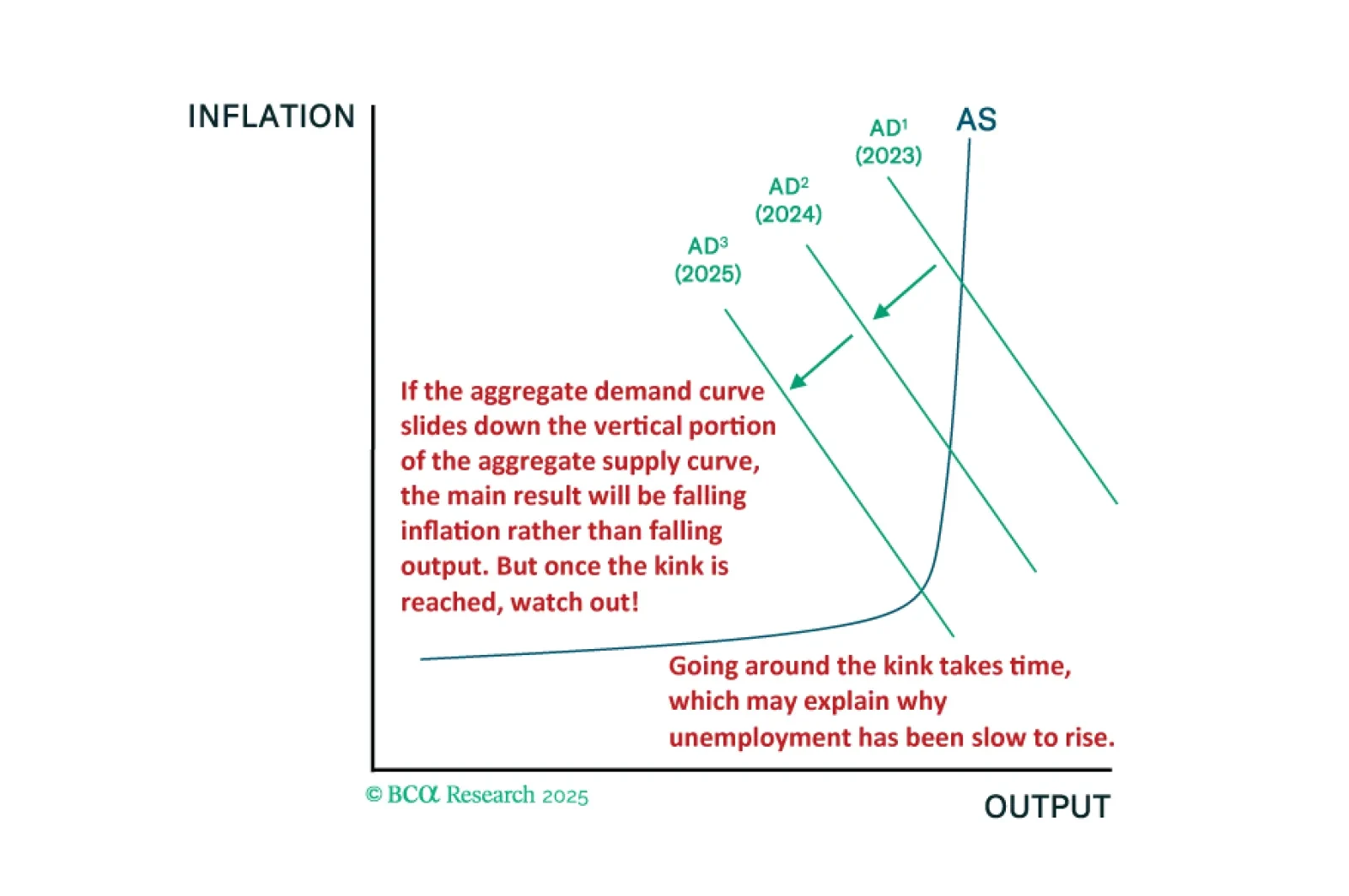

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

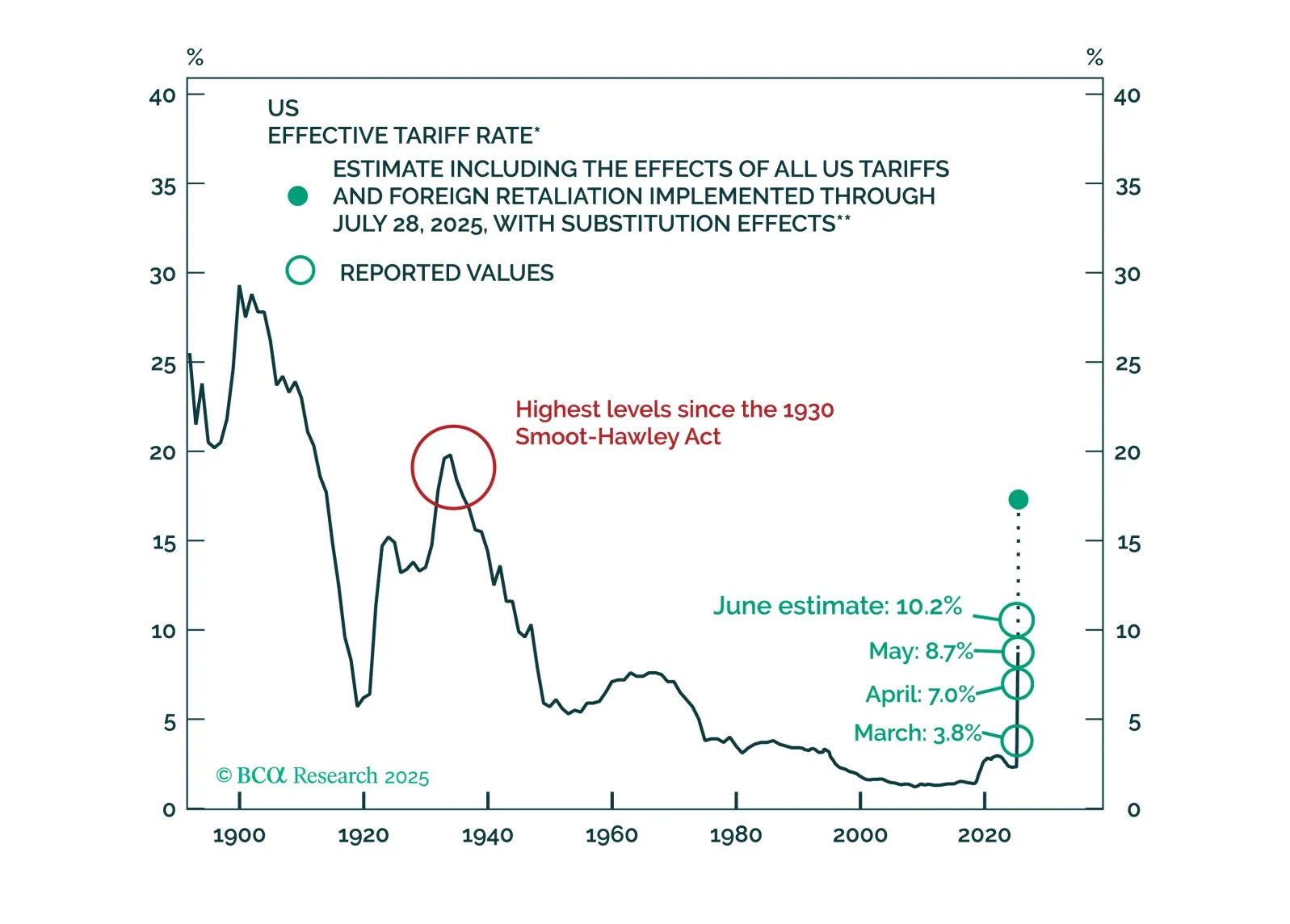

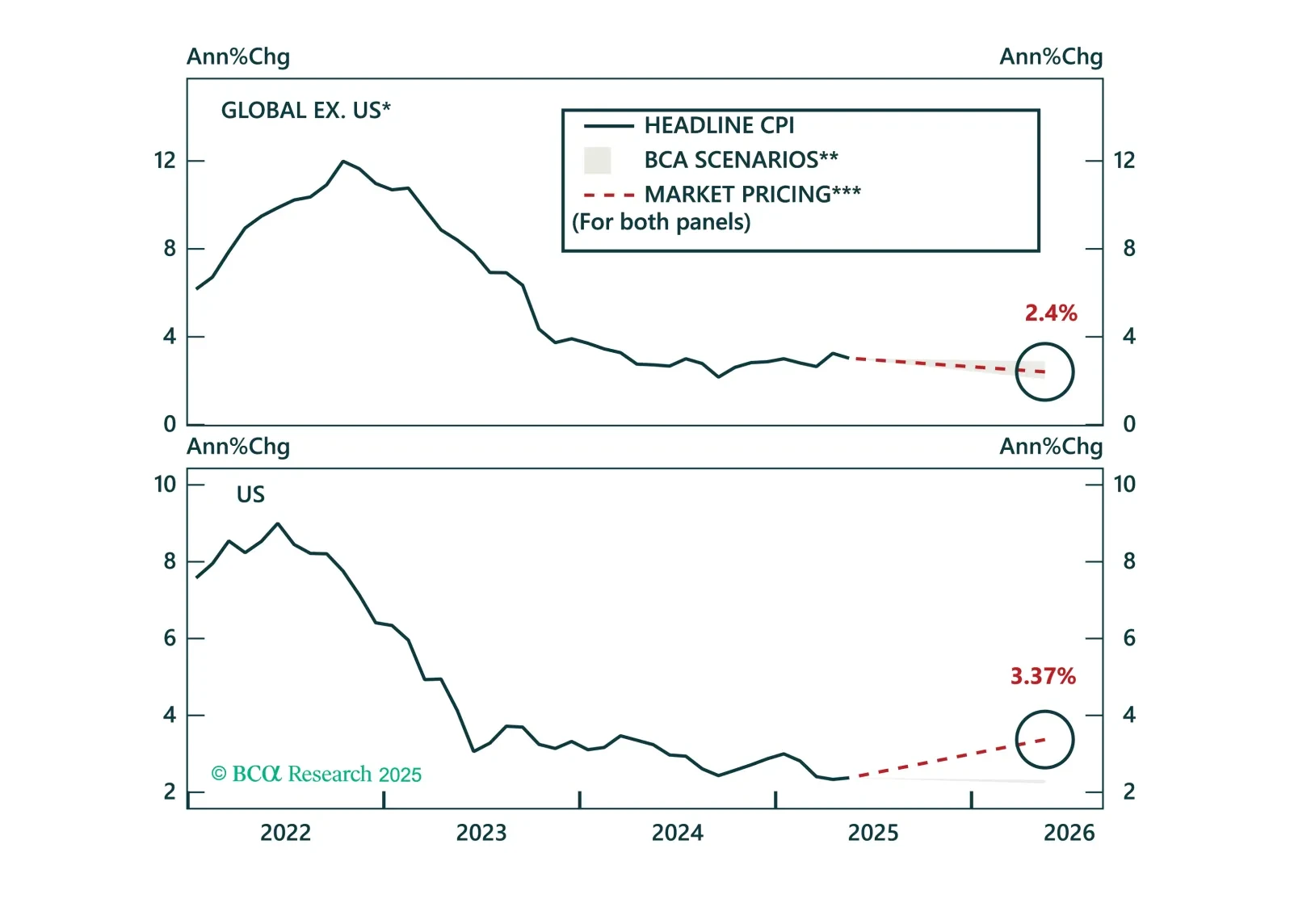

Disinflation continues to unfold globally, and markets are finally catching up. Inflation expectations have broadly realigned with fundamentals, prompting us to shift our global ILB allocation to neutral. While tariff risks are inflating US expectations, pricing in the UK, Japan, and Australia has adjusted sharply. Today’s Strategy Report reviews these developments and updates our country-level ILB positioning.

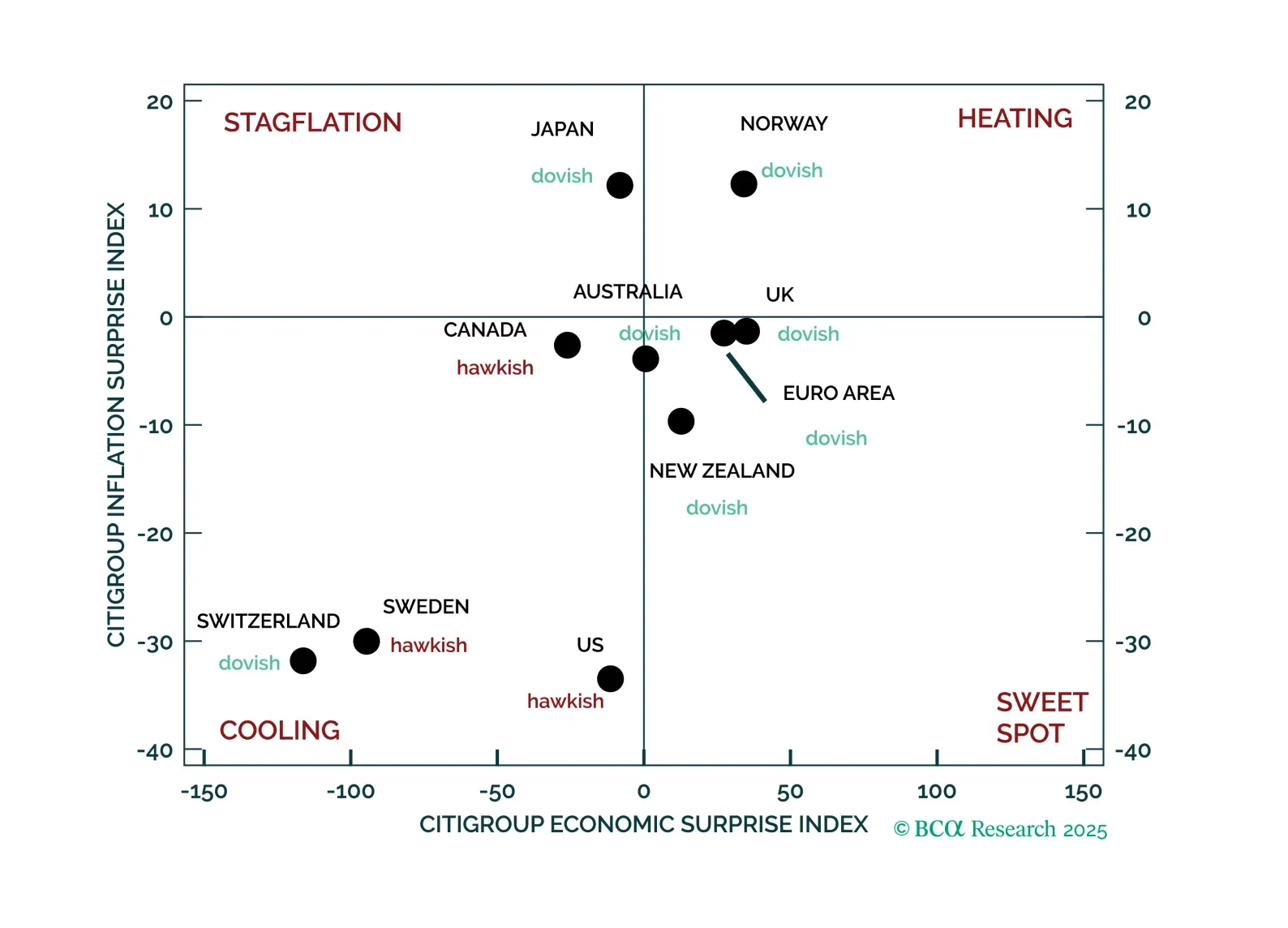

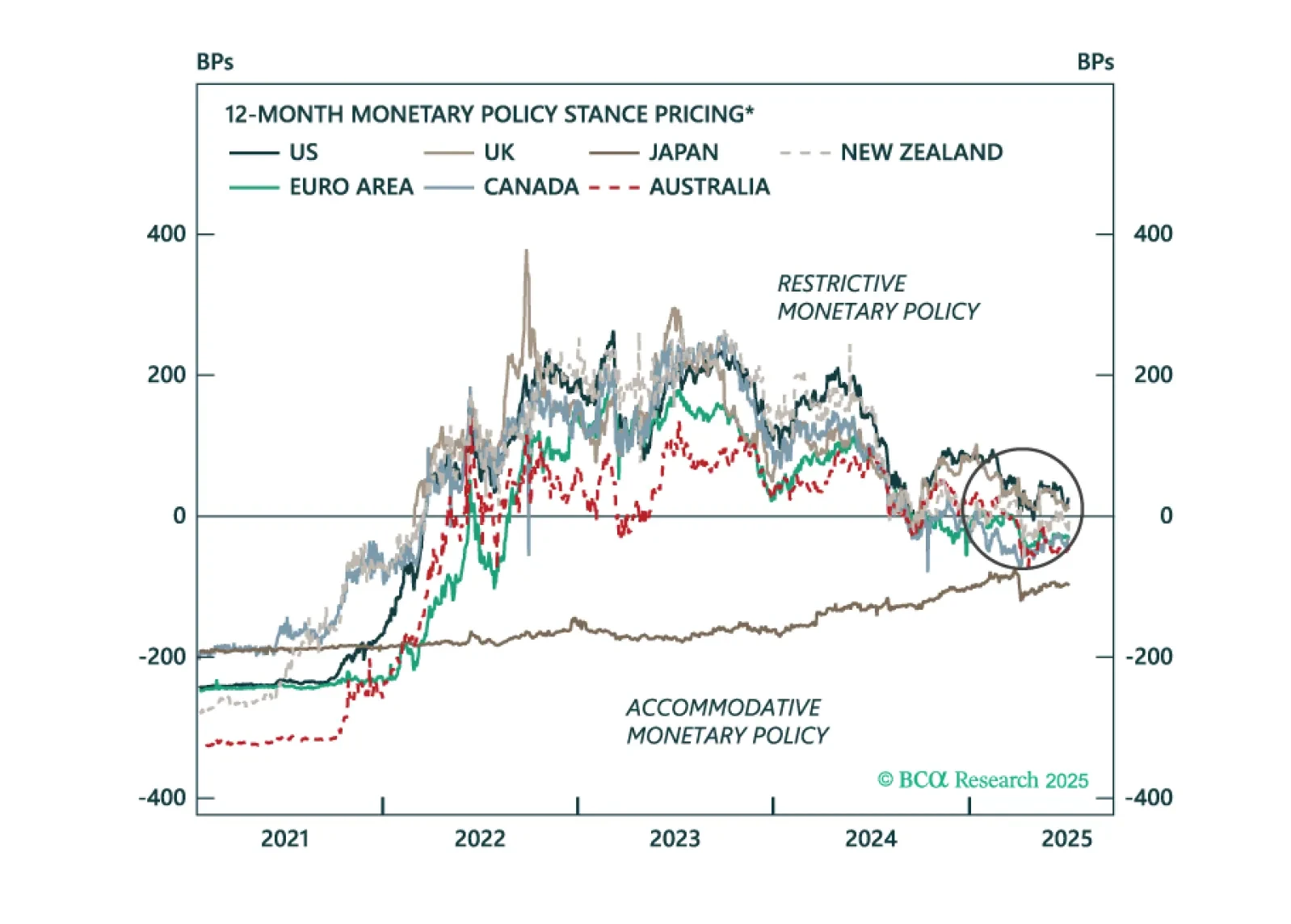

Markets are pricing a return to a neutral policy stance for the major central banks within the next 12 months. However, recession risks still loom amid slowing growth. We unpack where recession risks are underappreciated and what it means for bond positioning.