BCA Indicators/Model

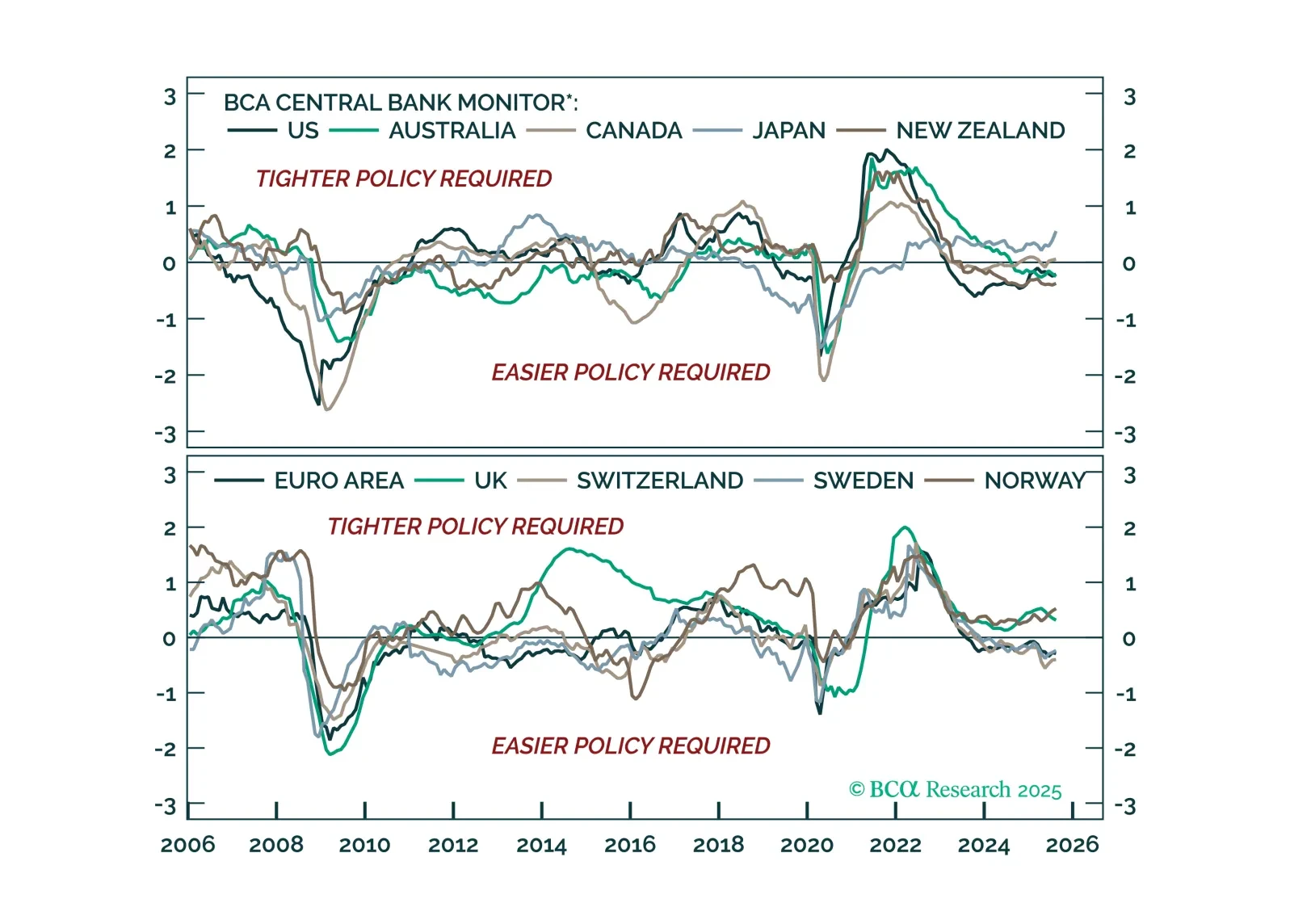

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

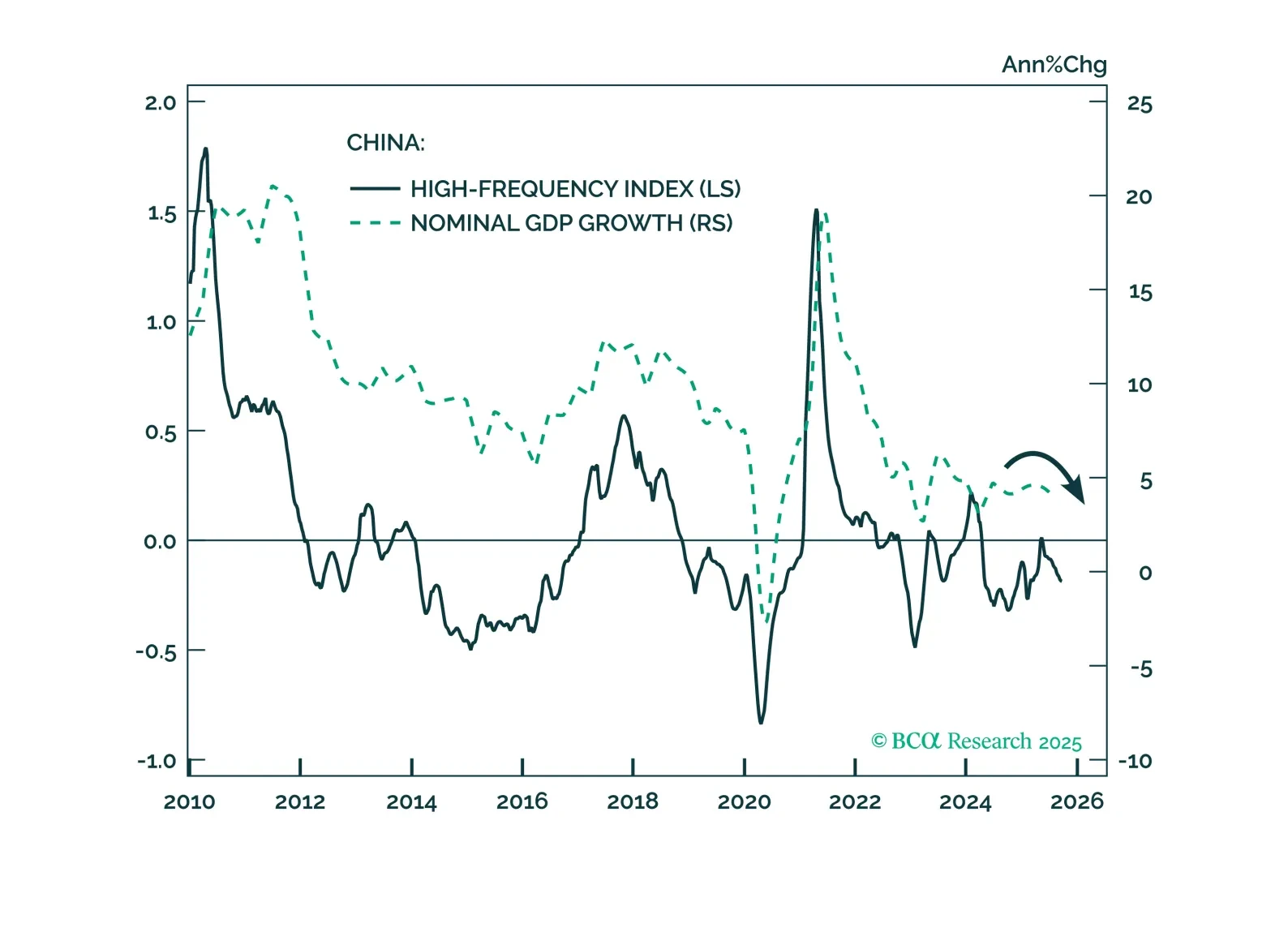

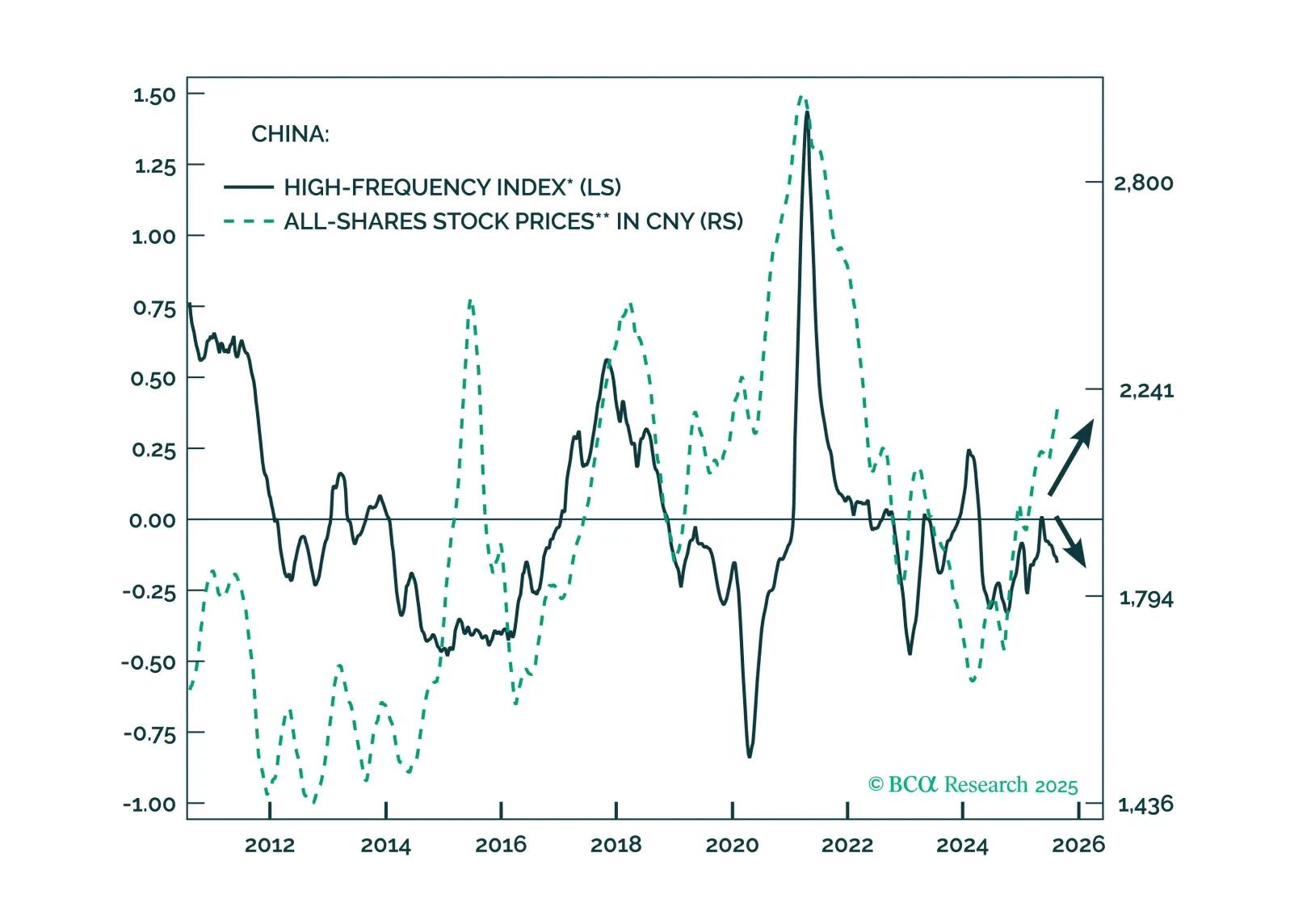

Our high-frequency indicators show China’s growth momentum weakening further in September, increasing the likelihood of new stimulus in the weeks ahead. We remain tactically cautious on Chinese equities, but strategically constructive on offshore Chinese shares.

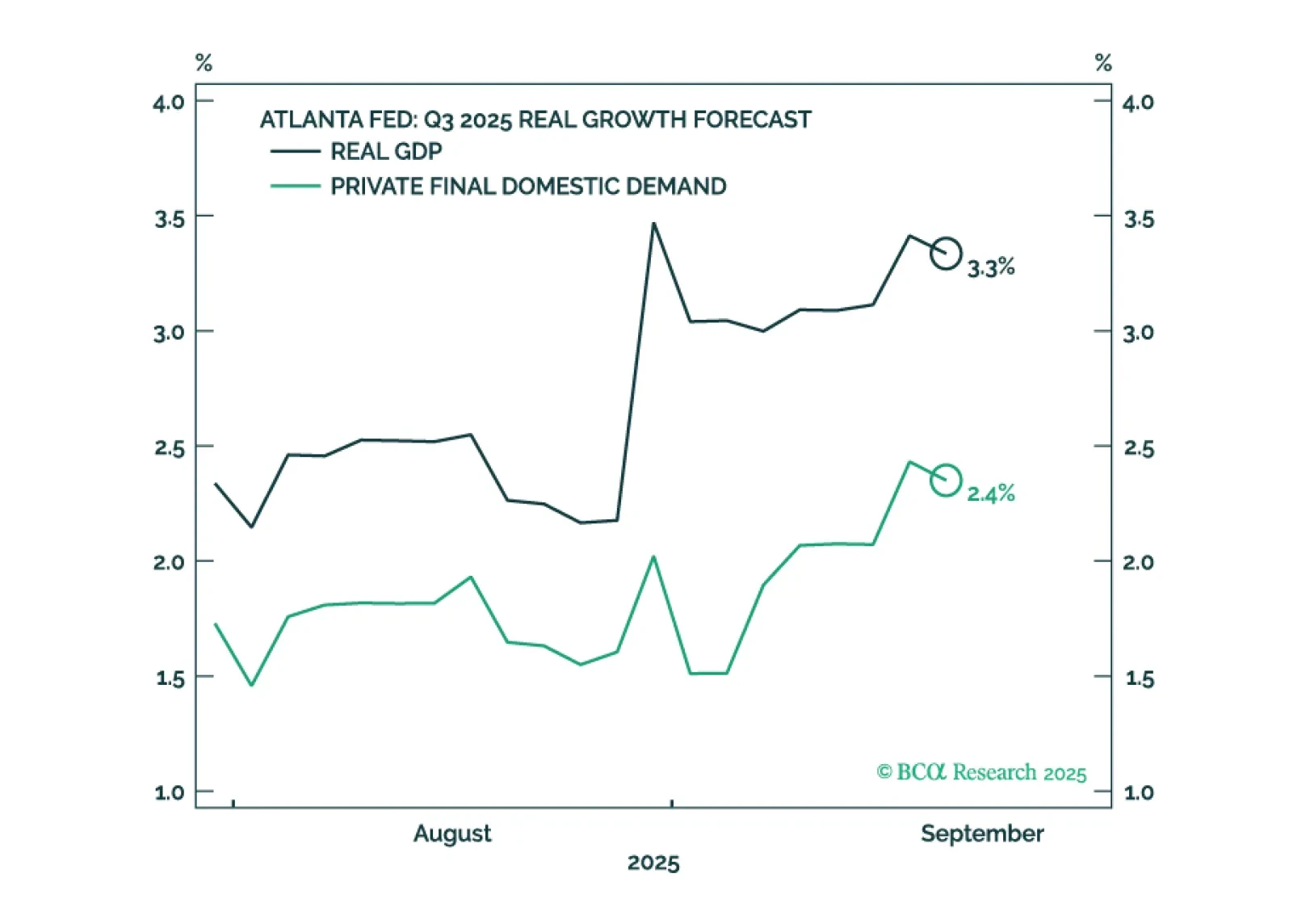

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

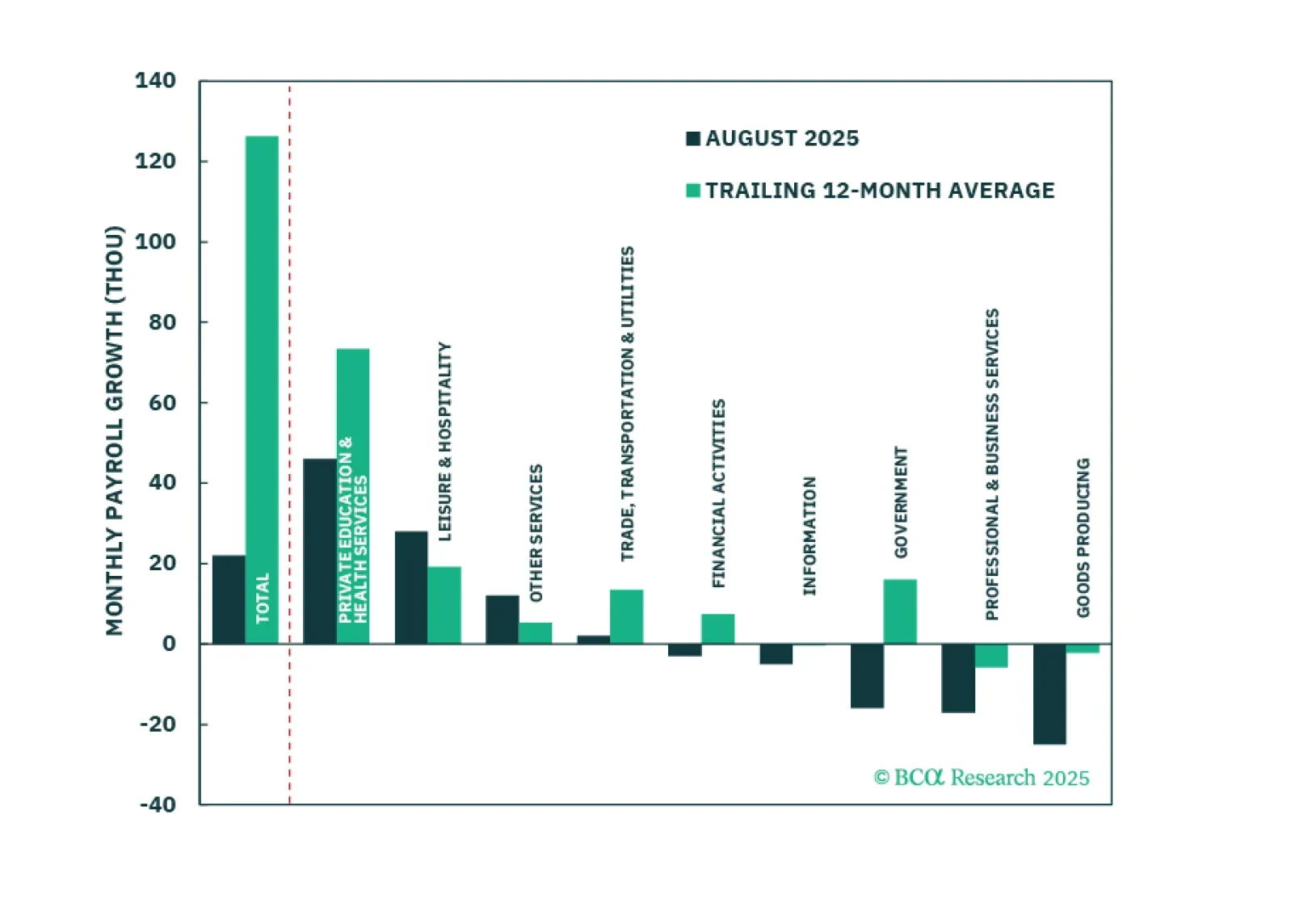

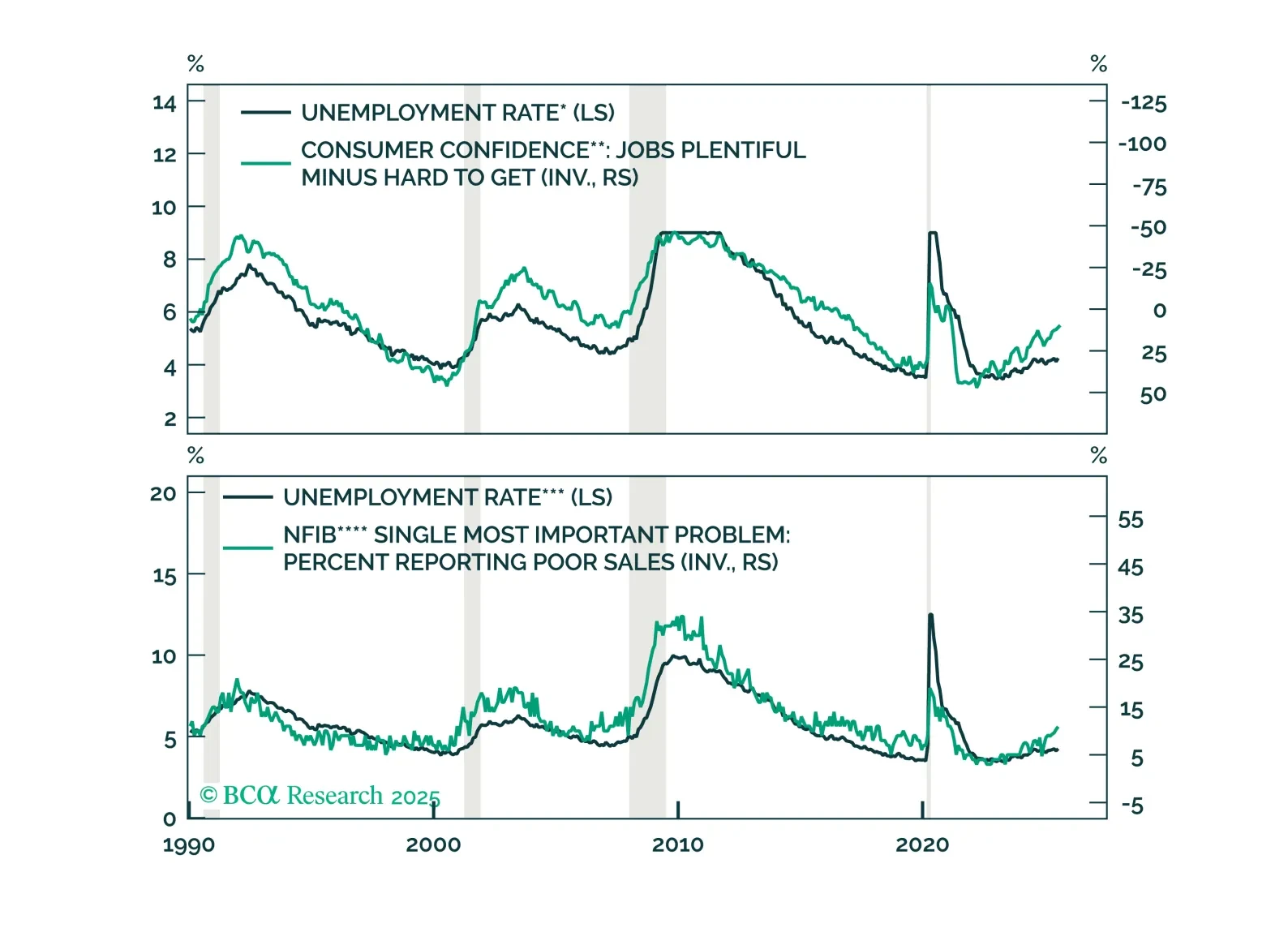

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

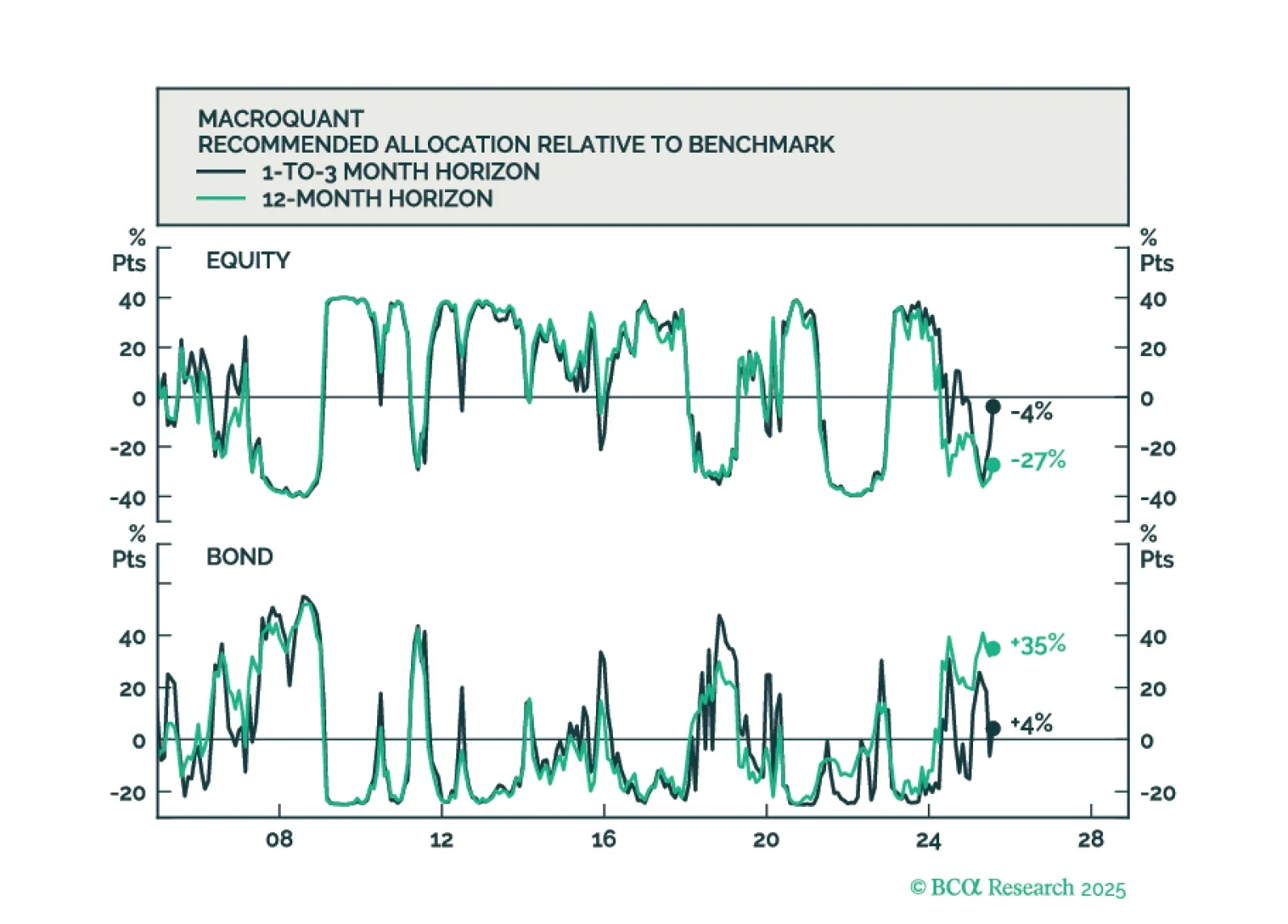

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

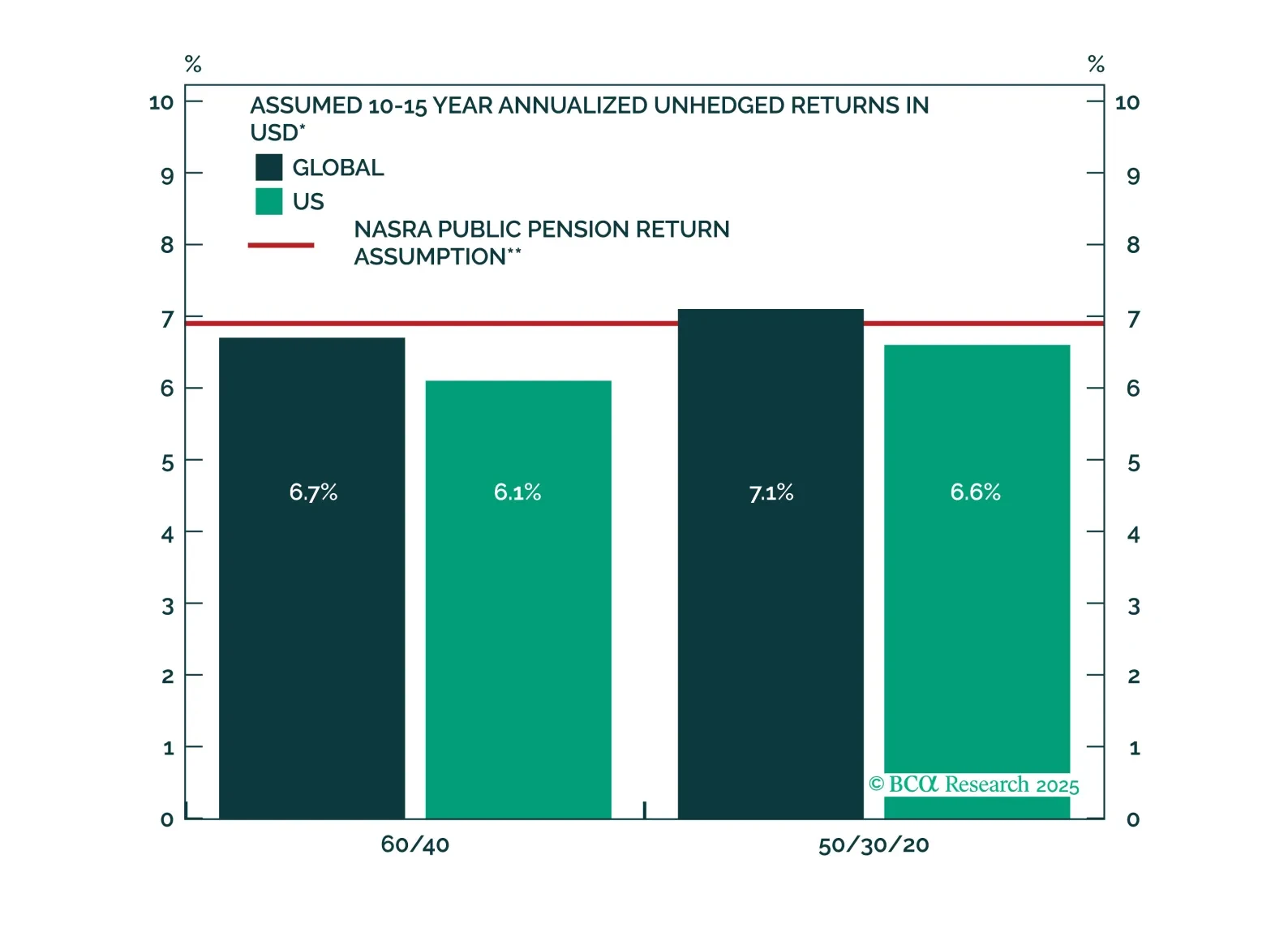

We revamp several of our methodologies in this edition of our return assumptions. We estimate that a US 60/40 portfolio will return 6.1% over the next 10 years. This is slightly below the return assumptions for US pension funds. Investors can obtain better returns by diversifying internationally and to alternative assets.

In this week’s Special Report, we introduce our newly constructed China High-Frequency Index (HFI). The HFI provides a timely measurement of China’s current economic conditions, helping investors to gauge cyclical turning points in the economy earlier and identify mini swings within a business cycle.

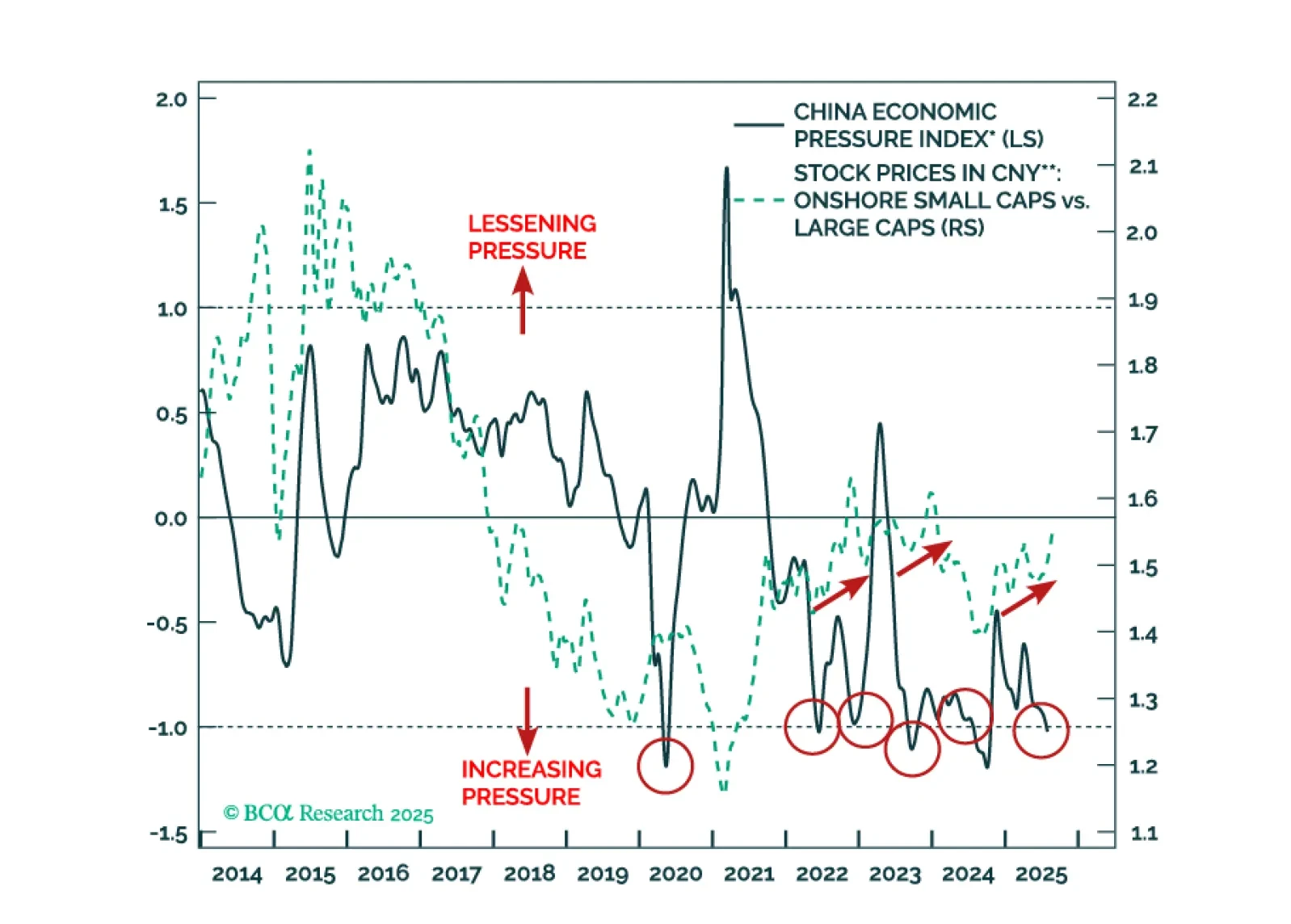

Our newly constructed China Economic Pressure Indicator shows intensifying household stress, raising the likelihood of new policy support in the coming months. We recommend a tactical trade as a stimulus hedge.