BCA Indicators/Model

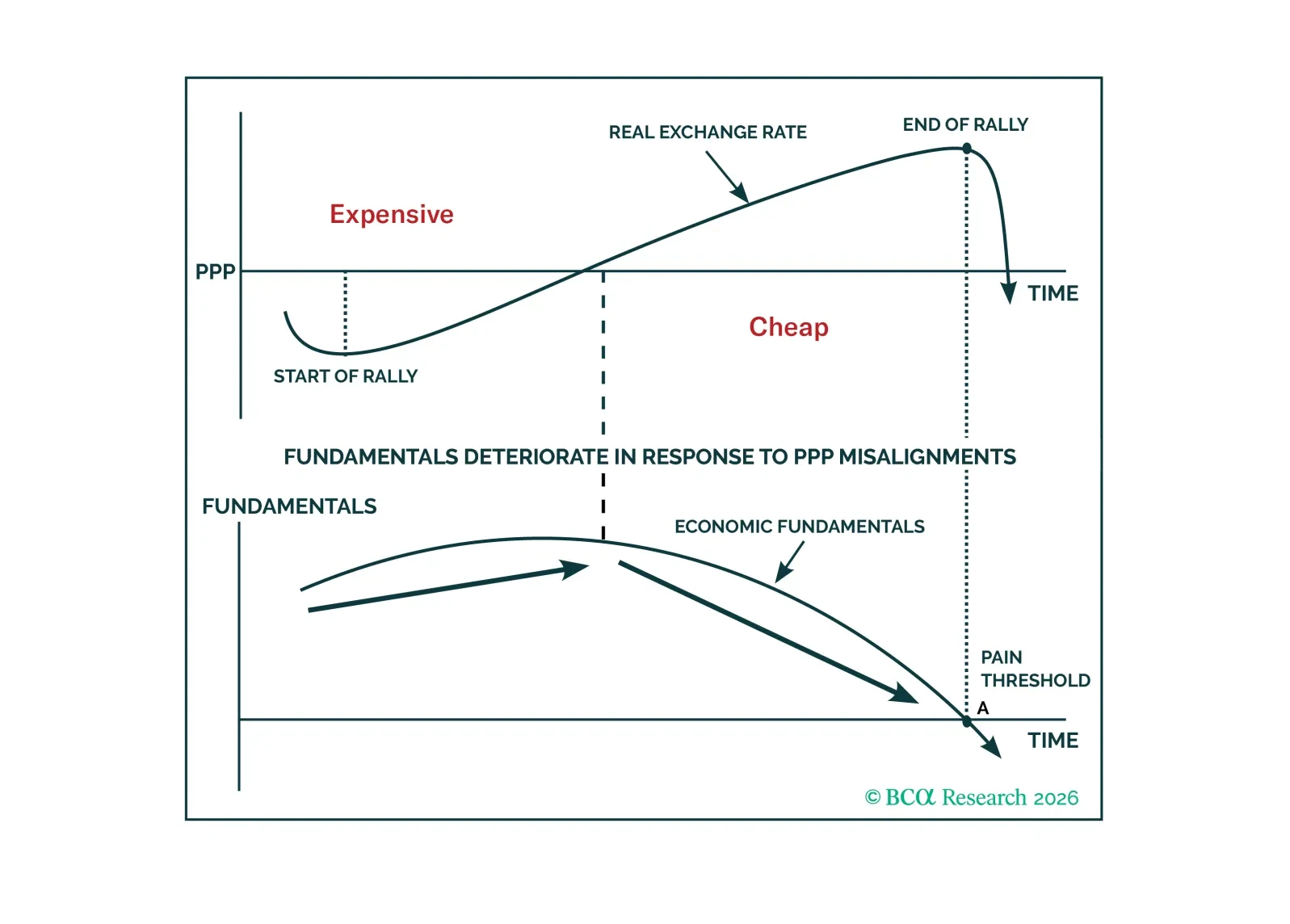

FX often looks random because no single model dominates across regimes. We lay out our long-term framework anchored in valuation, productivity, external balances, and the fiscal-monetary mix to identify when currencies are likely to mean-revert and where the long-run risk-reward is asymmetric.

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

We introduce our Macro Regime Indicators (MRI), a framework for forecasting growth and inflation surprises in the US. The MRI on the economy shows no substantial mispricing in either growth or inflation over the next 12 months.

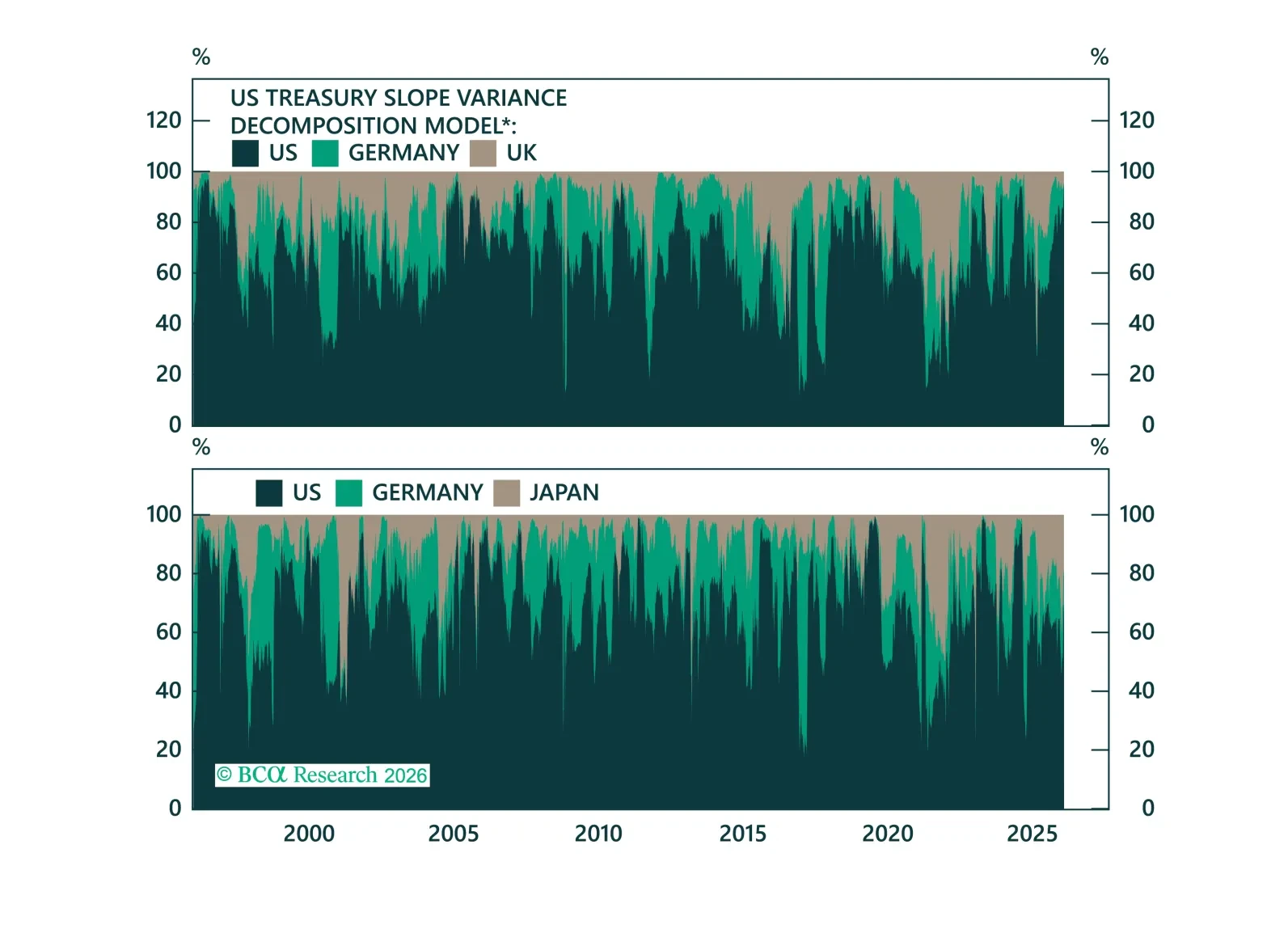

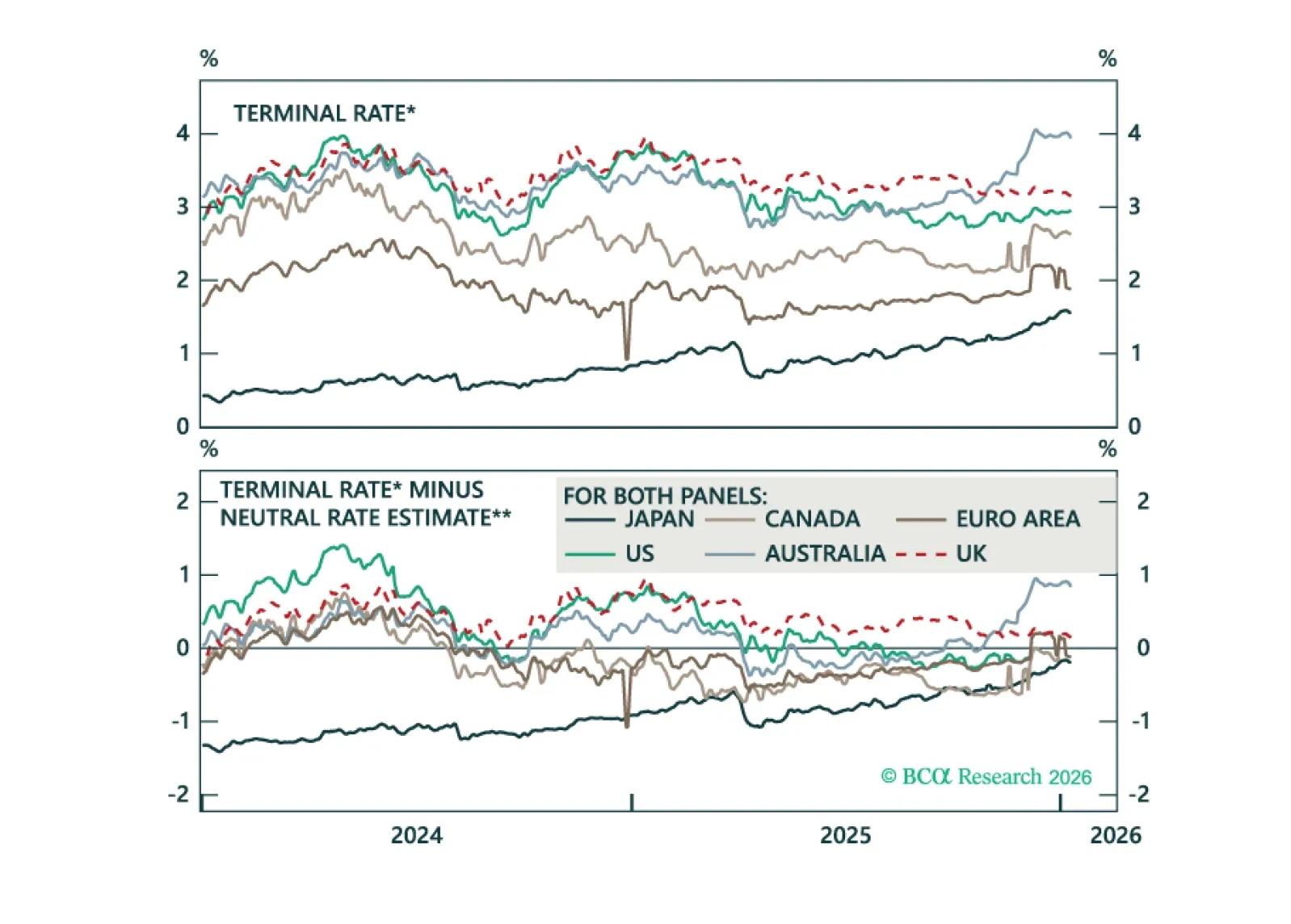

What’s driving government bond yields, and how do different bond markets impact each other? In today's Strategy Insight, we decompose yield moves into global drivers and idiosyncratic local drivers.

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

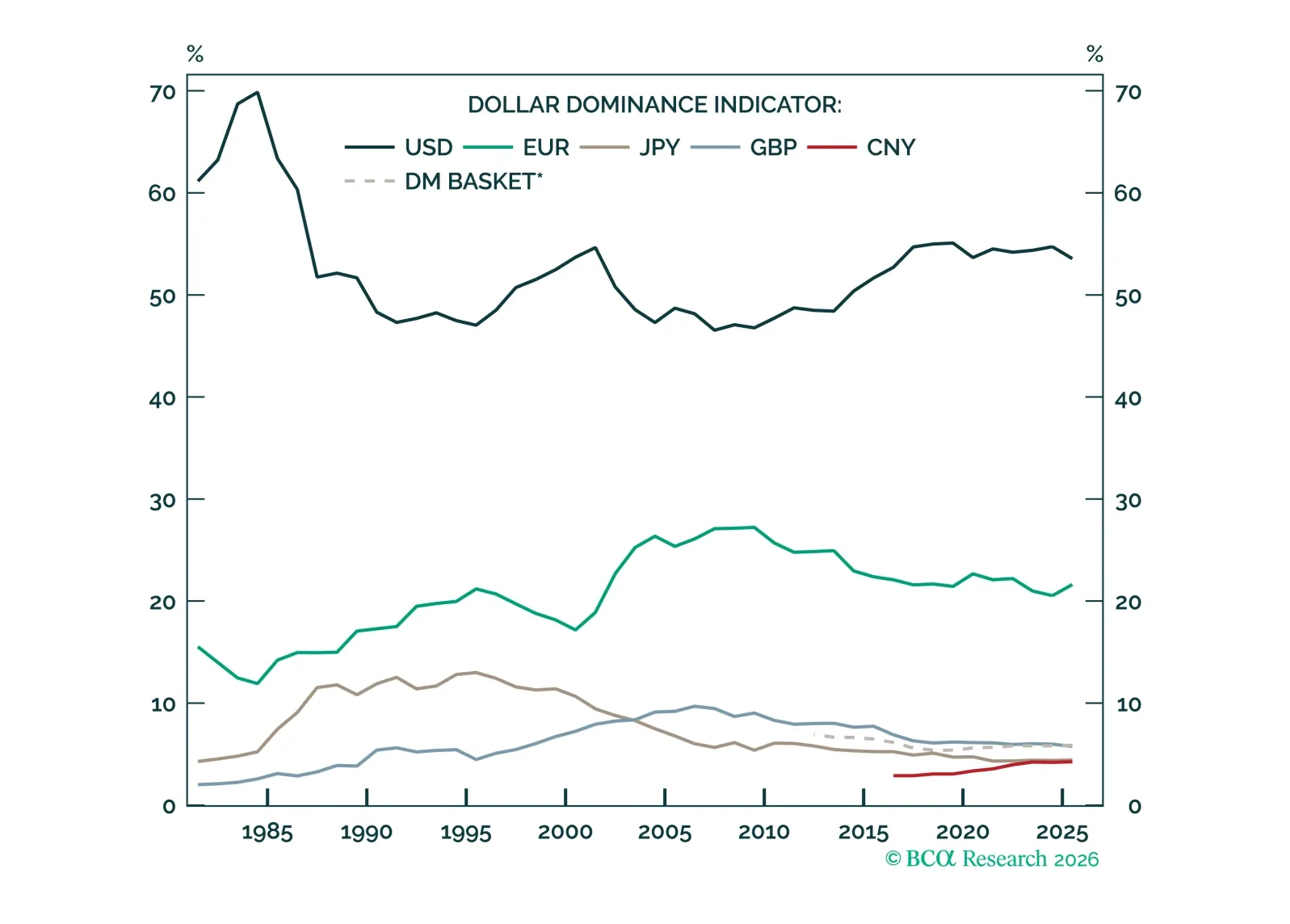

The dollar’s grip on global finance remains formidable, but the foundations are slowly shifting. Our new Dollar Dominance Indicator cuts through the noise, showing why USD usage stays sticky even as reserve demand erodes, and what this long transition means for FX and alternative reserve assets.

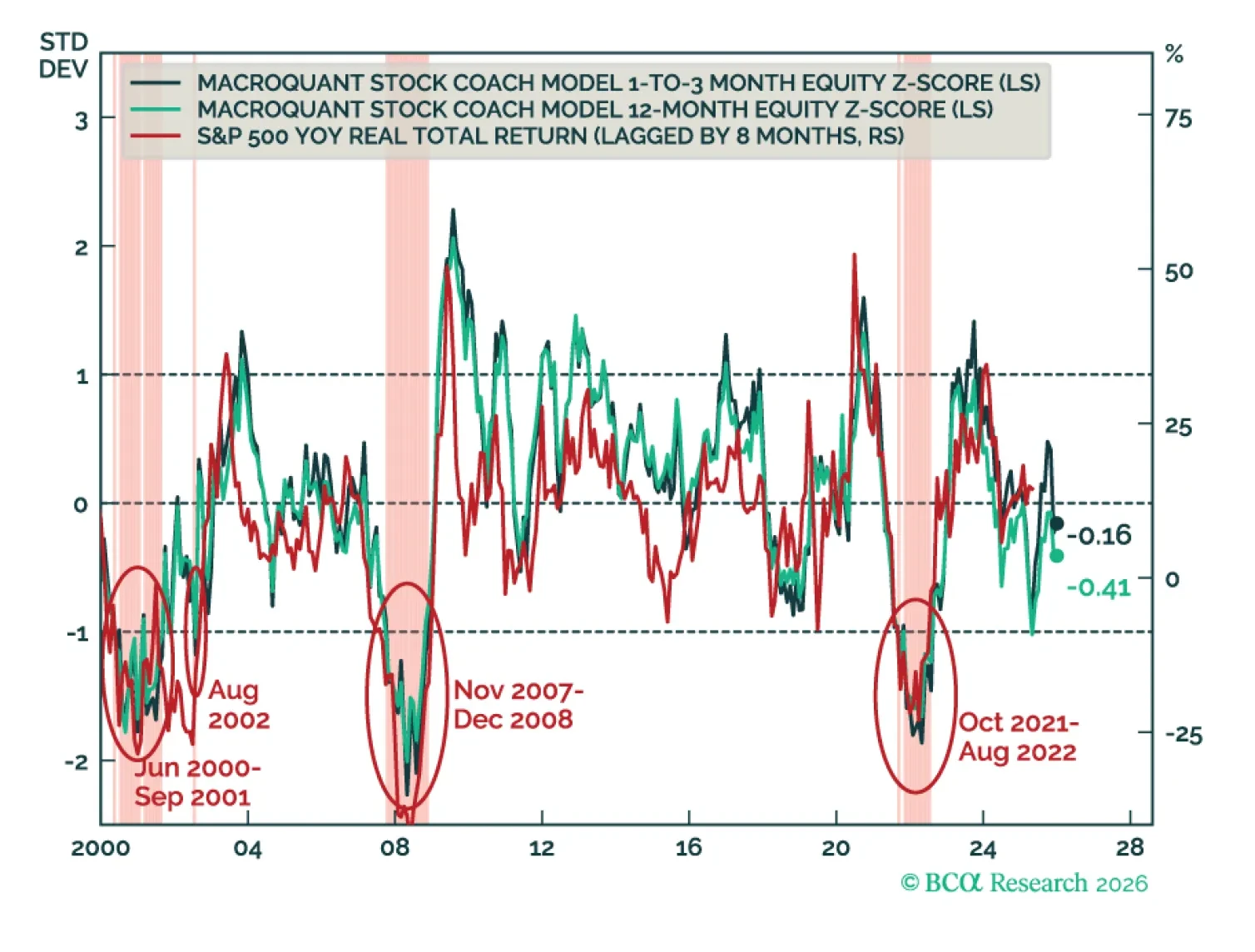

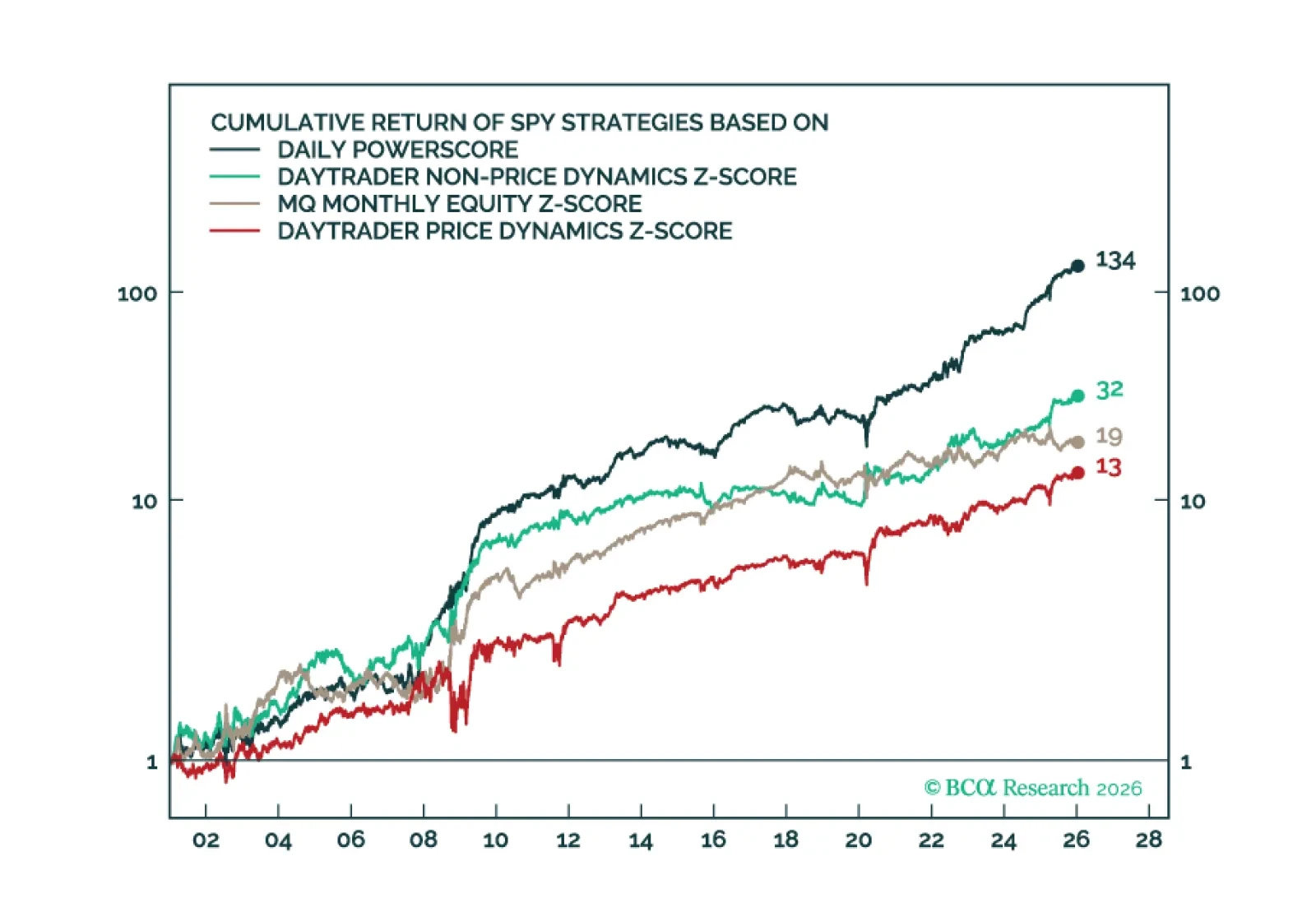

Over the past few months, we have been deploying new market-timing tools aimed at improving the accuracy of our calls. Today’s report highlights our ultra high-frequency Daily Oscillators, which provide daily signals on the near-term direction of the S&P 500 and long-term Treasuries.

Our Q1 outlook maps global growth, curve dynamics, and policy surprises, which we then translate to our recommended global fixed income portfolio allocations and trades.

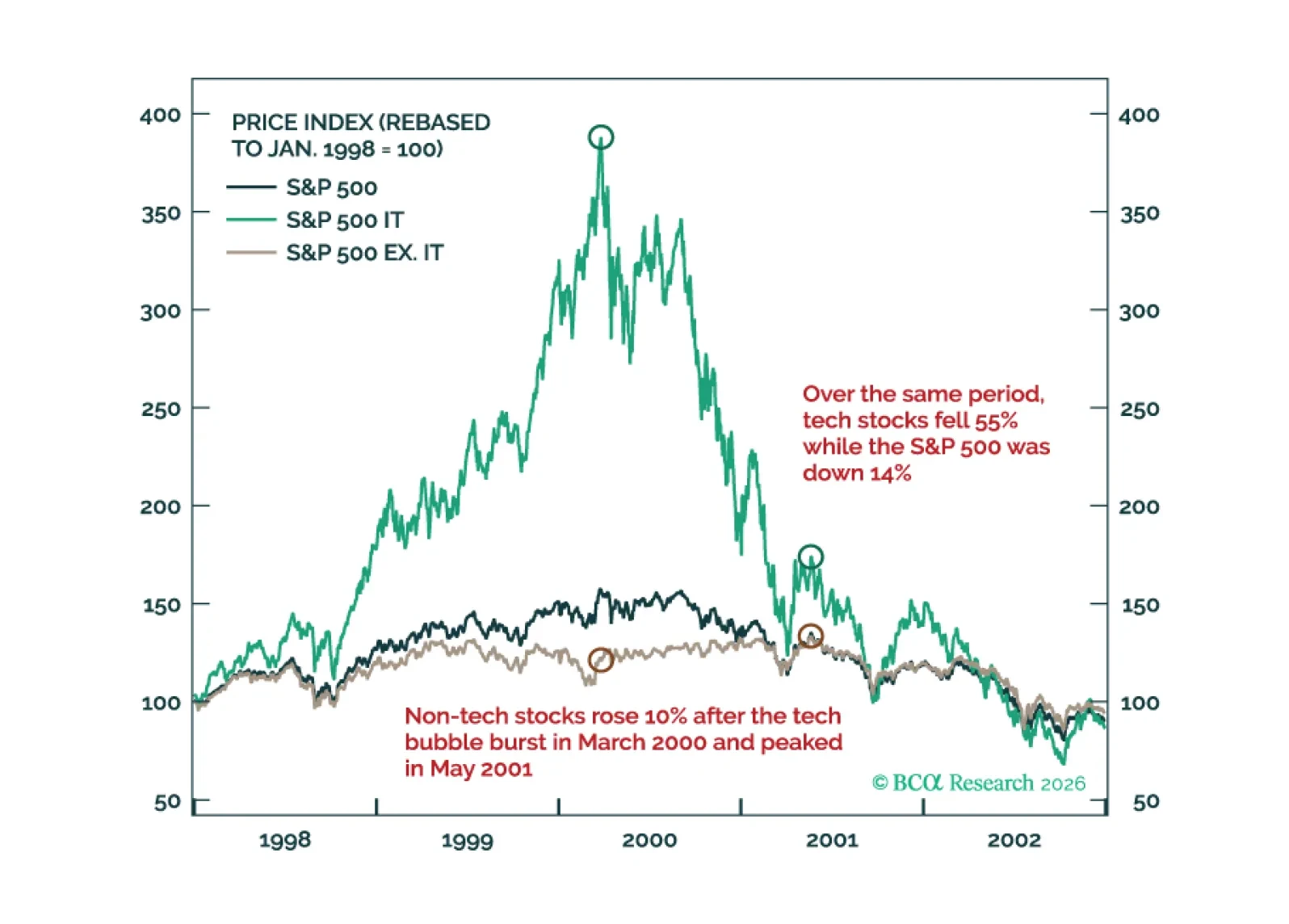

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

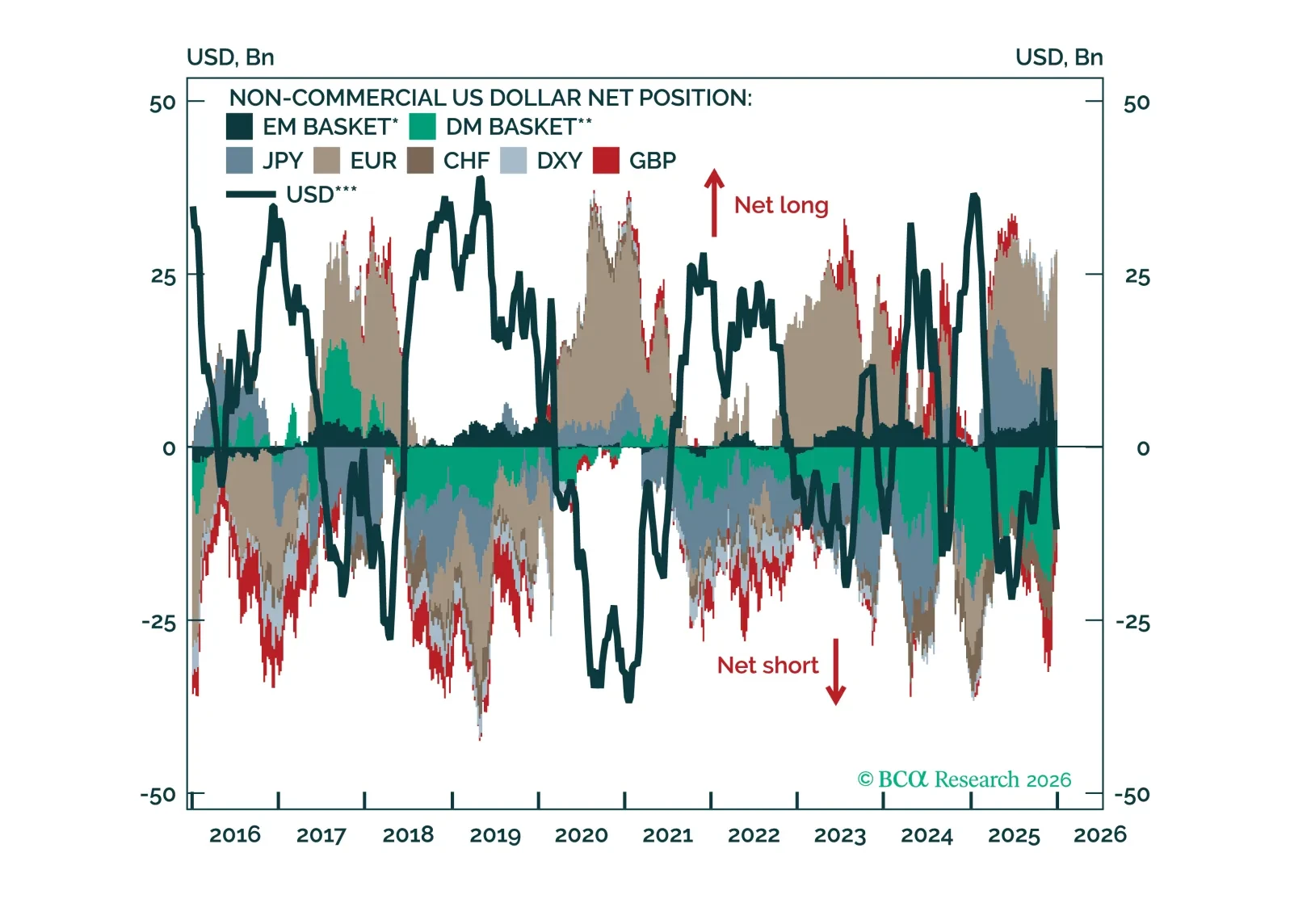

With FX volatility near cycle lows, this Insight examines where positioning has become most stretched across G10, EM FX, and precious metals – and what that implies for near-term moves and reversal risks.