Auto Manufacturers

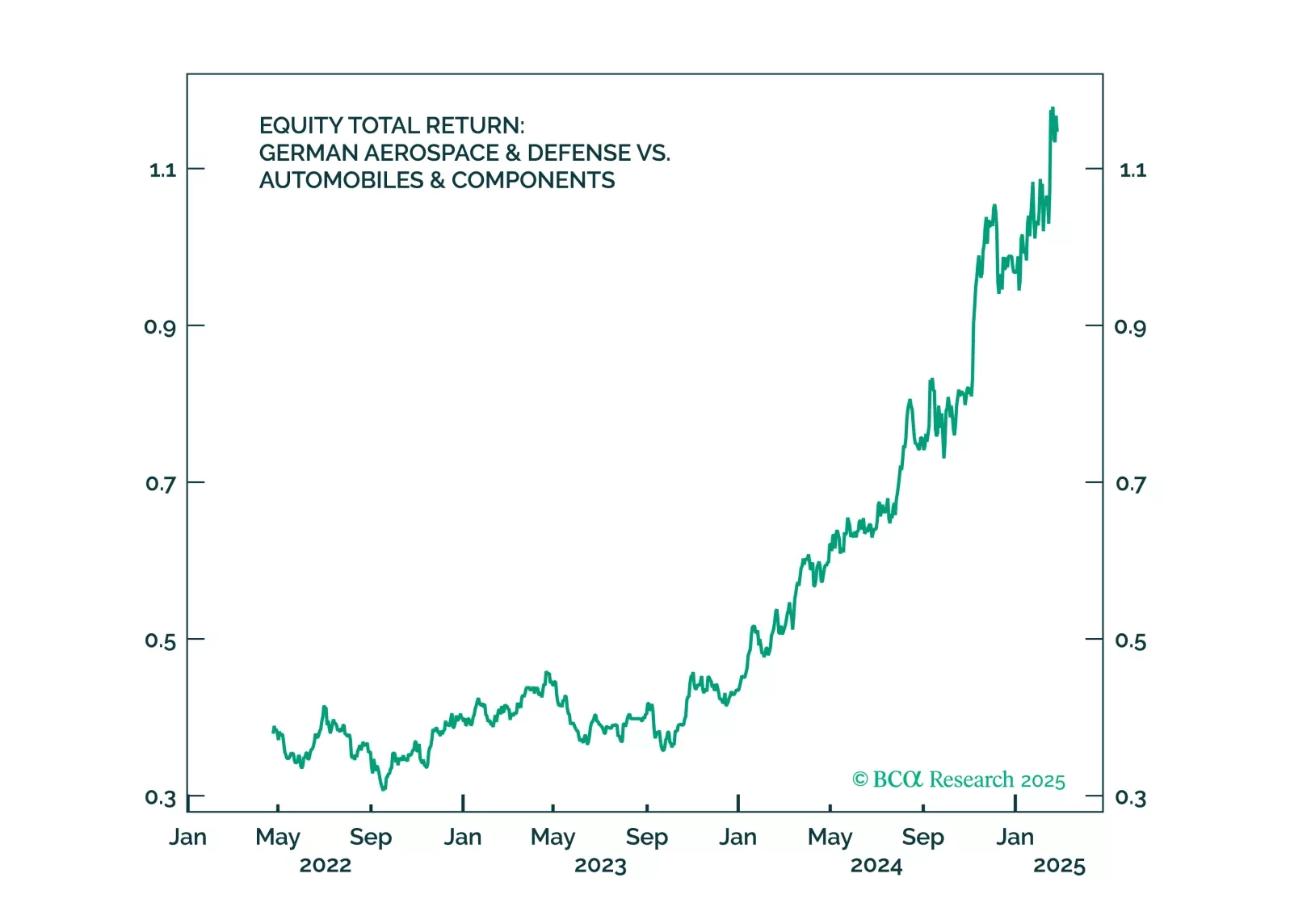

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

The EU's import tariff increases on Chinese EVs are expected to have a minimal impact on China's overall exports. We anticipate that most Western-brand EV shipments from China will be less affected by the EU import tax hike. Beijing will likely pursue continued negotiations with the EU rather than resort to harsh retaliatory measures.

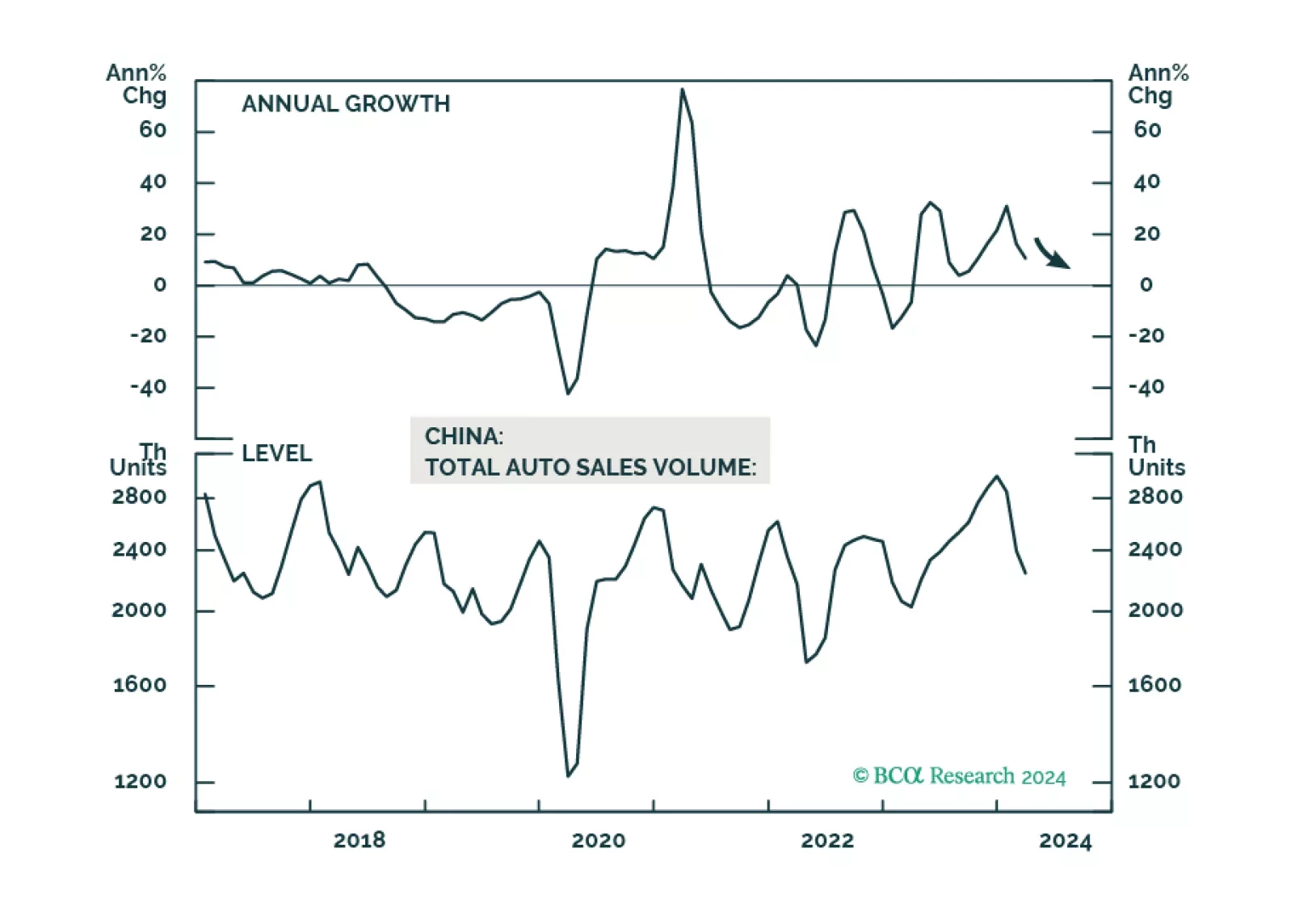

This year’s cash for clunkers program will have only a mildly positive impact on domestic demand for automobiles and home appliances in China. In the meantime, the equipment renewal program will prop up domestic manufacturing moderately as well as help the country reduce its reliance on high-end equipment imports. We recommend continuing to overweight onshore auto stocks relative to the A-Share Index.

The expectation that China is best placed to win the global EV race presumes the persistence of the status quo. Reality, however, may differ as the sector looks set to be hit by a range of changes. If nonlinearity were to emerge in the global auto sector, as it often does, then the EV transition could end up spawning a very unexpected list of winners and losers.

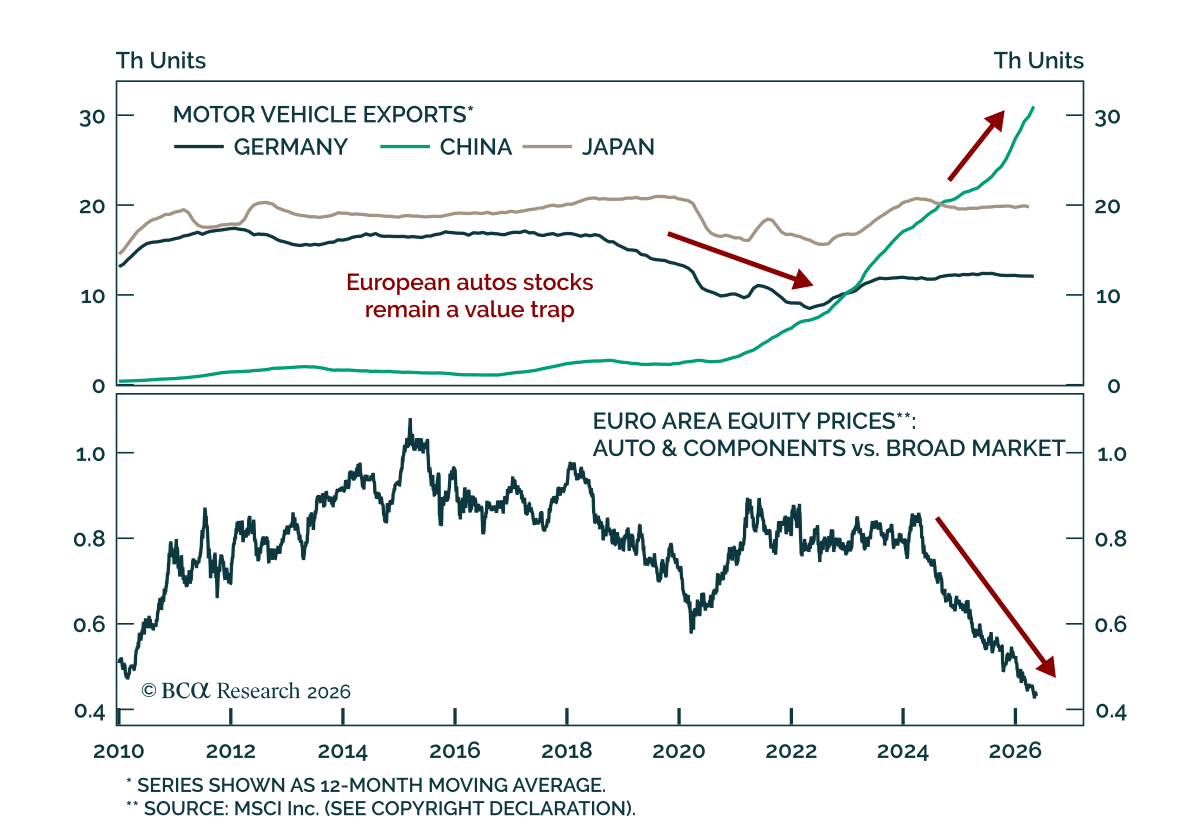

European auto stocks are cheap, but even if European carmakers can rise to the challenge created by Chinese EVs, shareholders will suffer.