Australian Dollar

This week’s report explores factors behind the recent rise in the dollar, and whether this could continue in the next month.

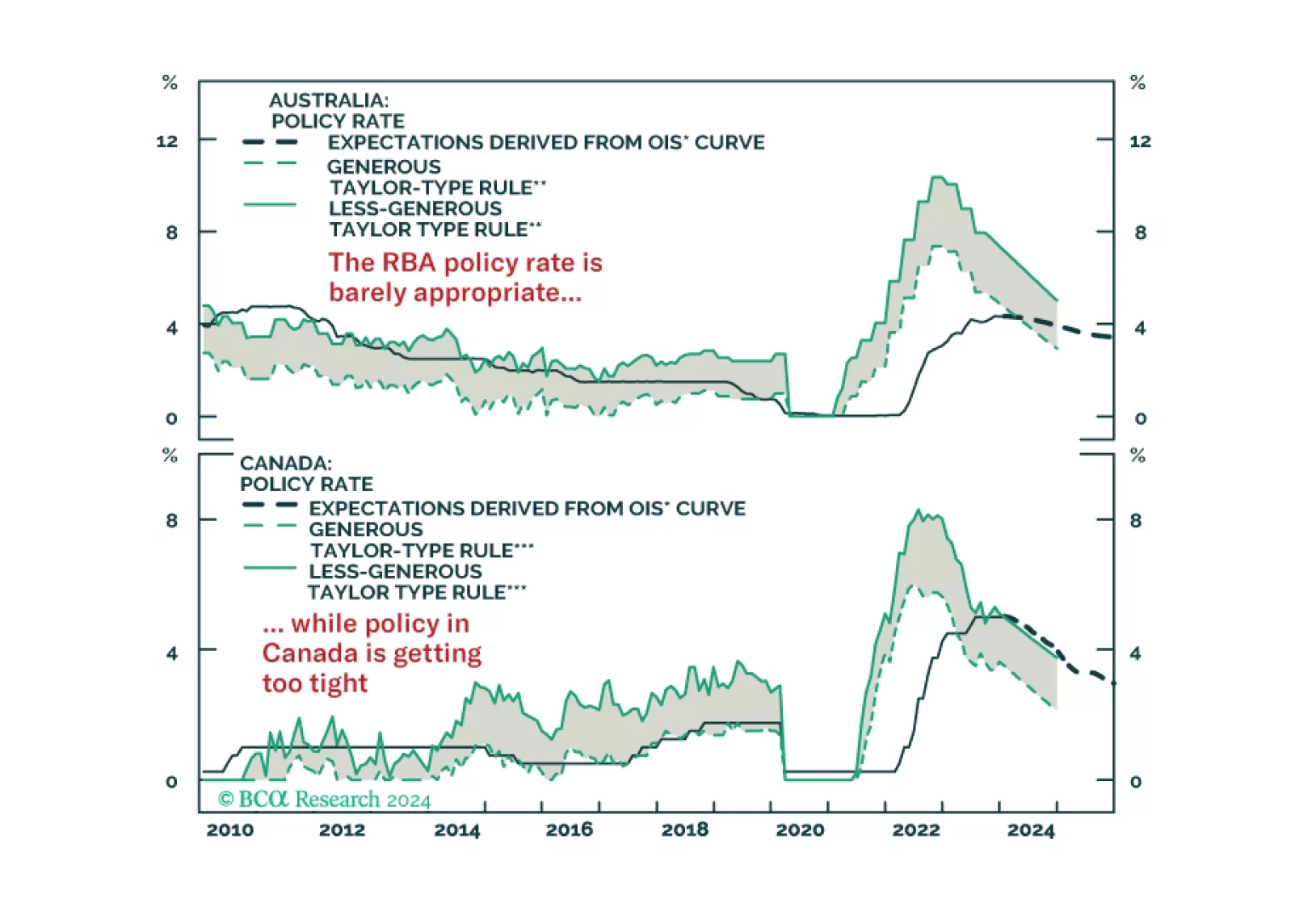

In this Strategy Insight, we assess the monetary policy path for Australia and Canada in 2024 and we discuss how to profit from a growing divergence between the two economies.

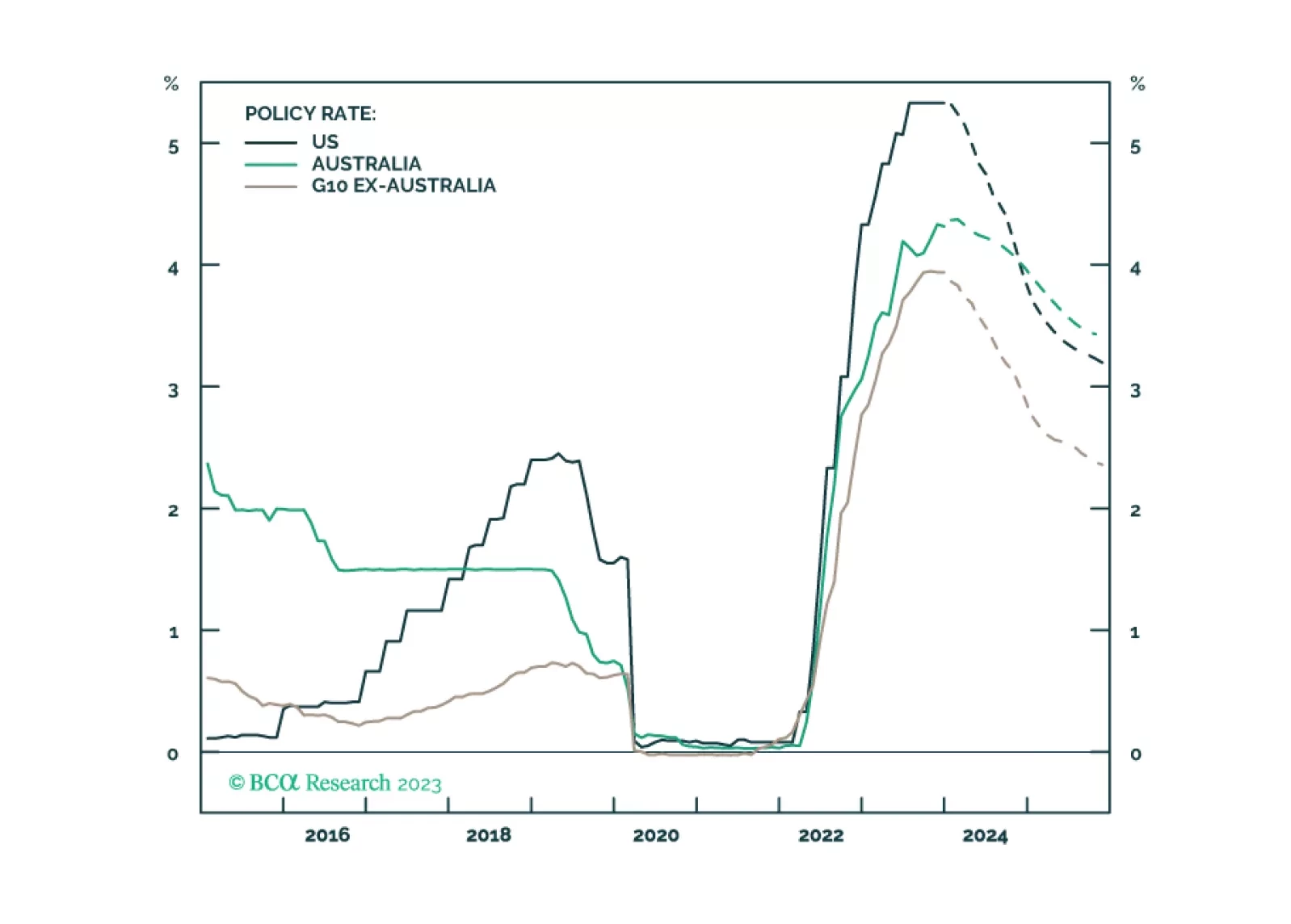

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.

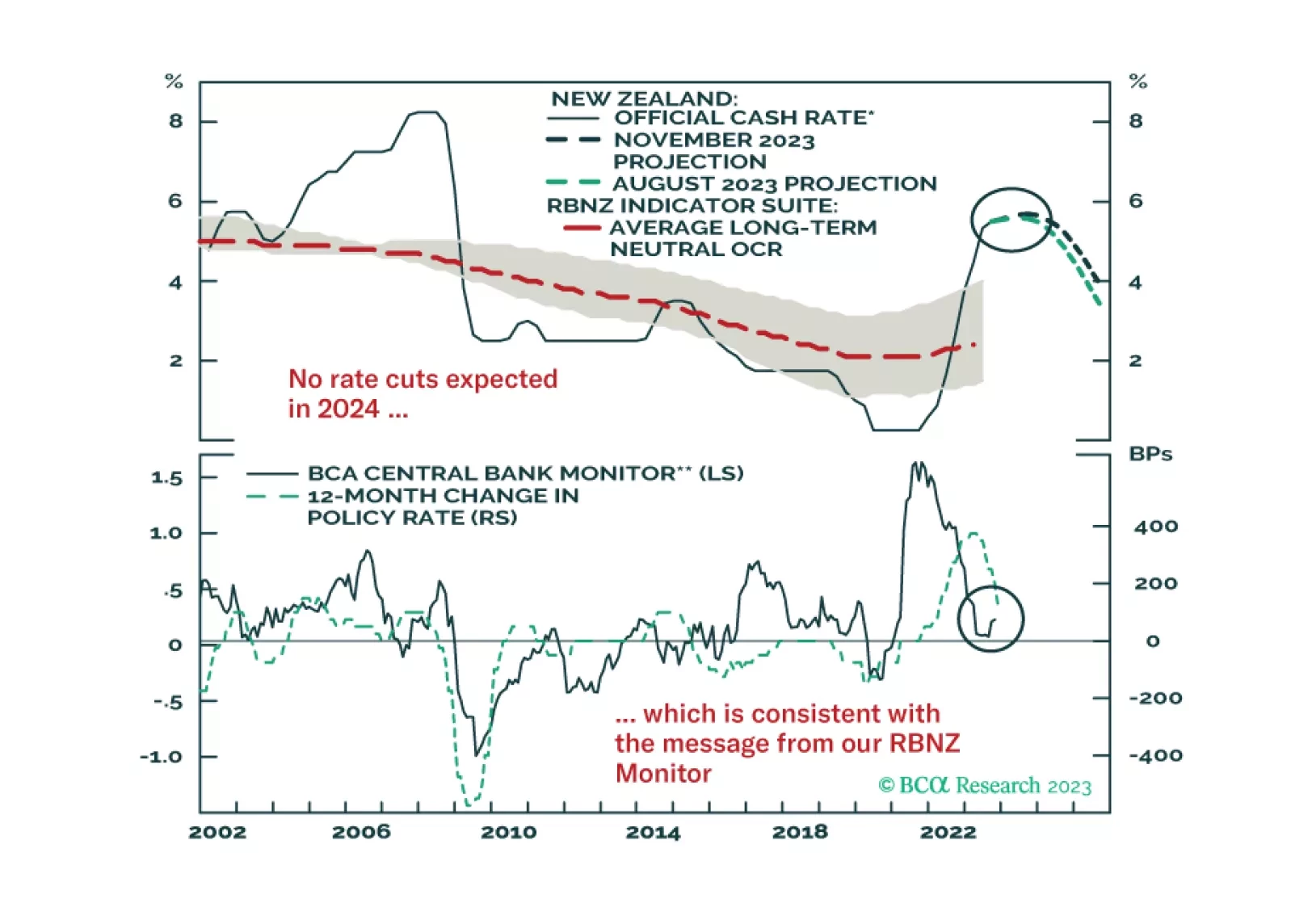

In this Insight, we discuss the outlook for monetary policy in New Zealand after this week’s RBNZ policy meeting, and introduce related fixed income and currency trade ideas.

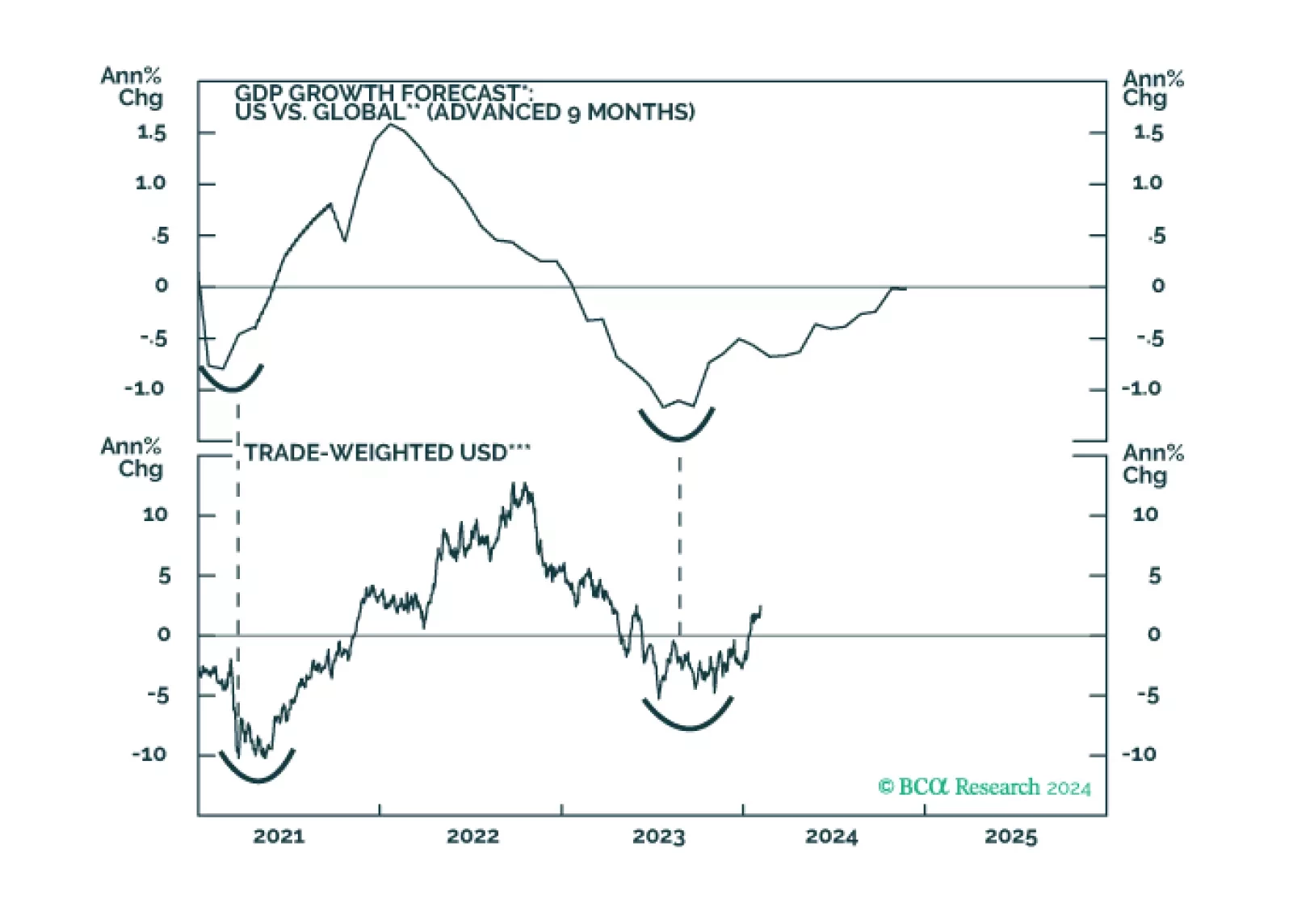

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

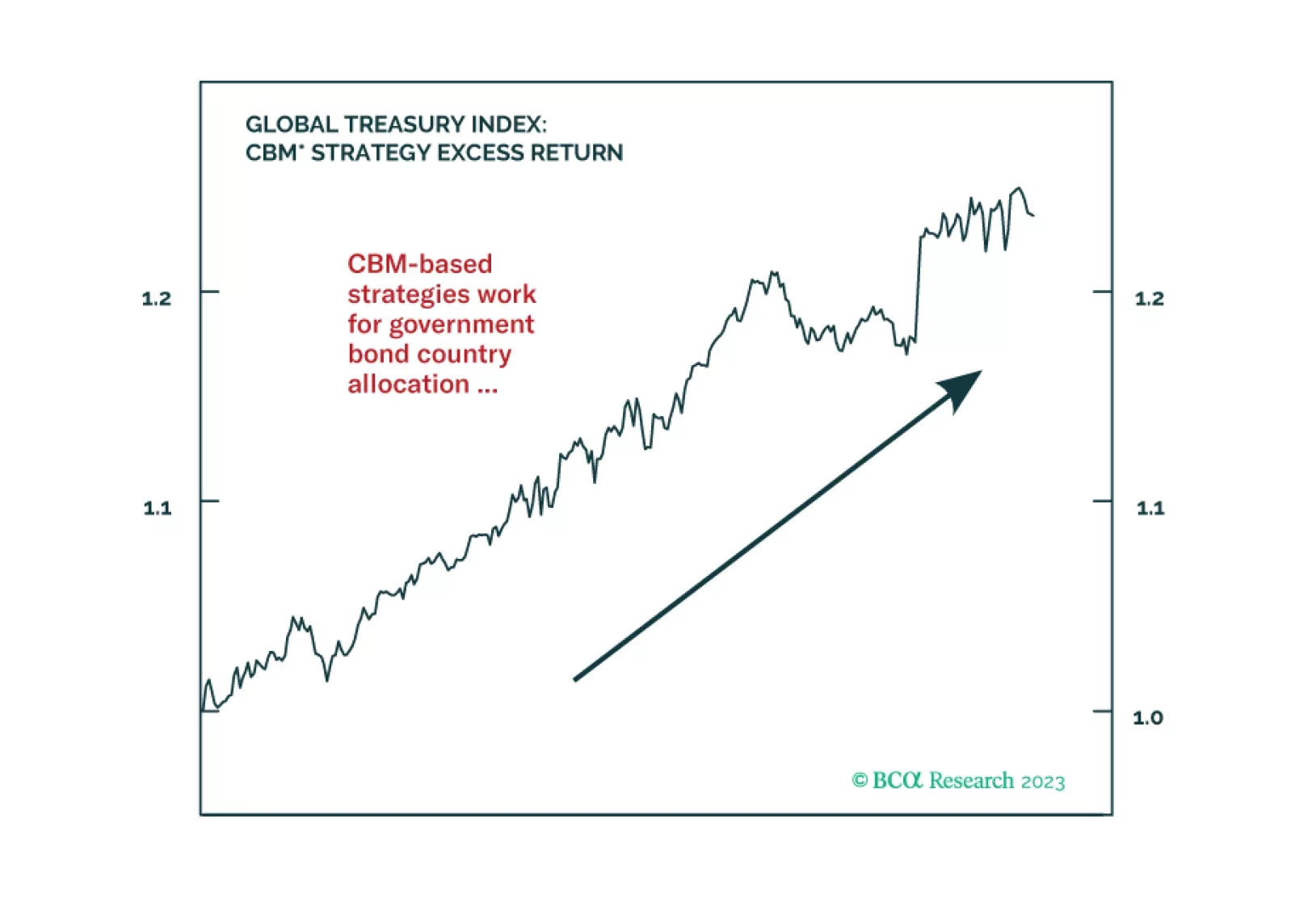

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

In this update to the two Special Reports on FX hedging of global equity portfolios with nine different home currencies, published in 2017, we show that BCA’s proprietary dynamic FX hedging strategies have consistently added value to global equity portfolios. We value quant models as an important input in our decision-making process, but we do not suggest any investor to slavishly follow them, because models cannot capture all the important fundamental changes, as demonstrated in the details of this report.

In this update to the two Special Reports on FX hedging of global equity portfolios with nine different home currencies, published in 2017, we show that BCA’s proprietary dynamic FX hedging strategies have consistently added value to global equity portfolios. We value quant models as an important input in our decision-making process, but we do not suggest any investor to slavishly follow them, because models cannot capture all the important fundamental changes, as demonstrated in the details of this report.

In this report, we highlight why there are upside risks to Brent crude oil and copper prices going into 2024, with the production side expected to drive deficits in these markets. To take advantage of a potential rally, we suggest basket plays for hedging this outcome.