Asset Allocation

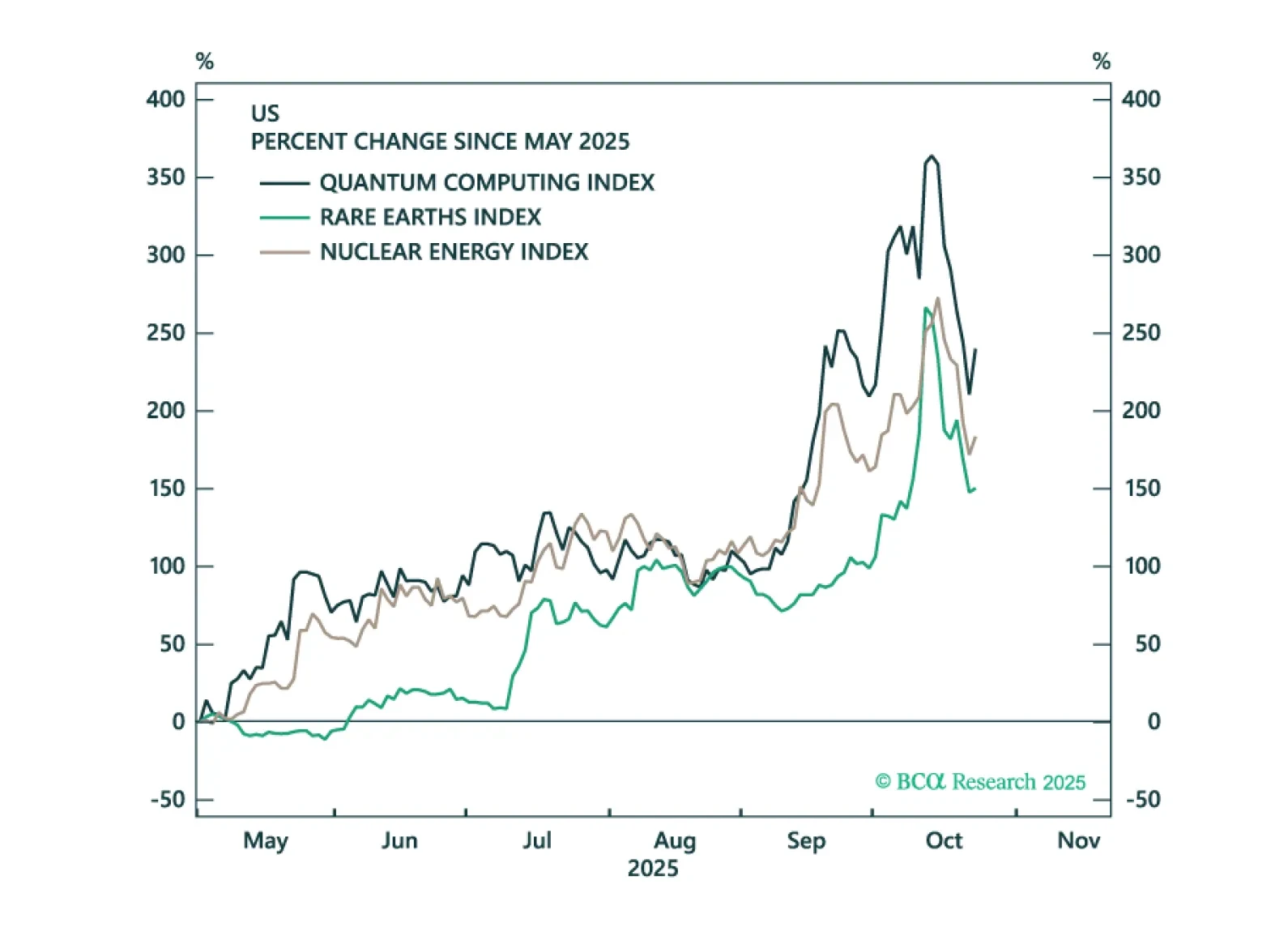

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

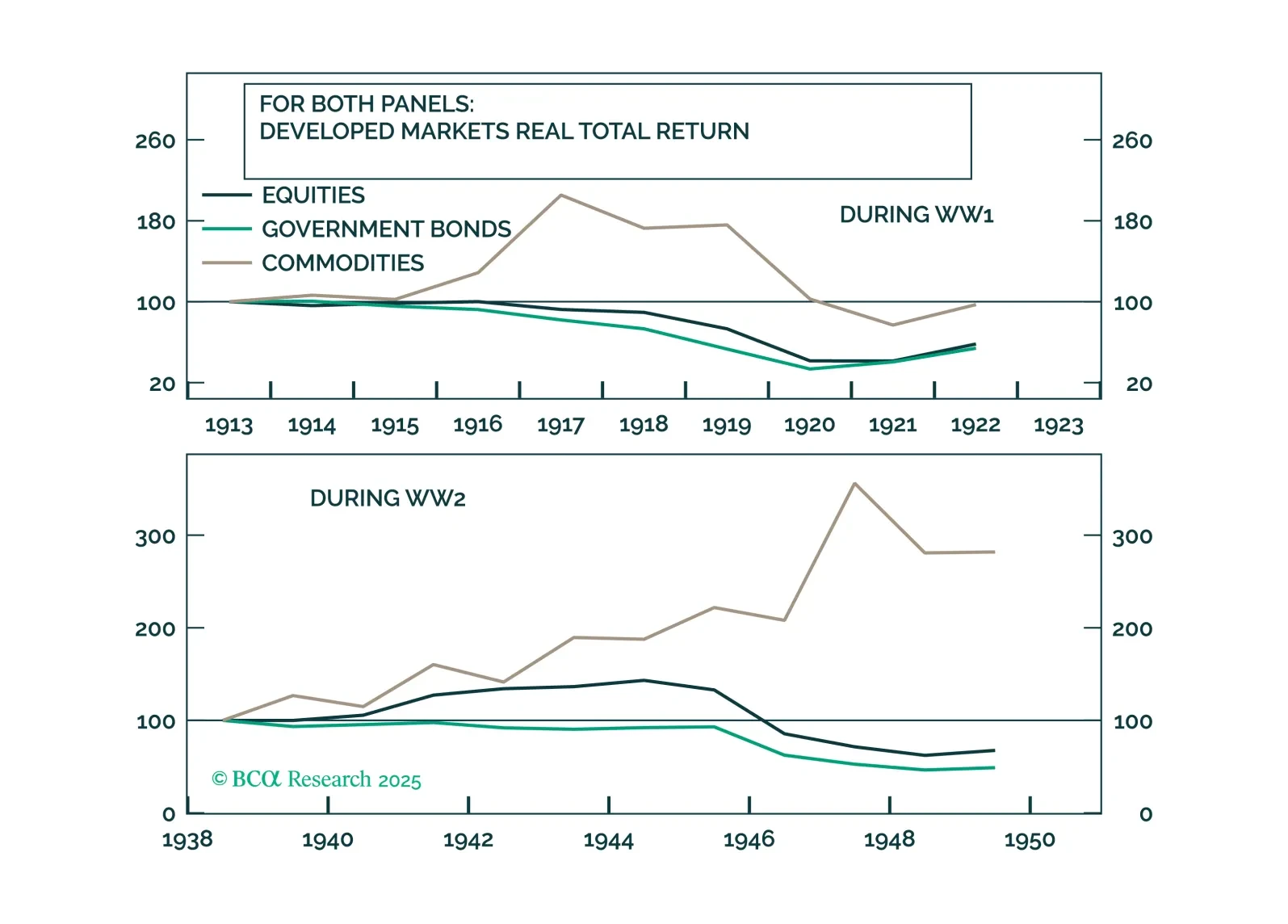

World War III will not happen. But if you disagree, here is our portfolio to hedge it: commodities, neutrals, and crypto.

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

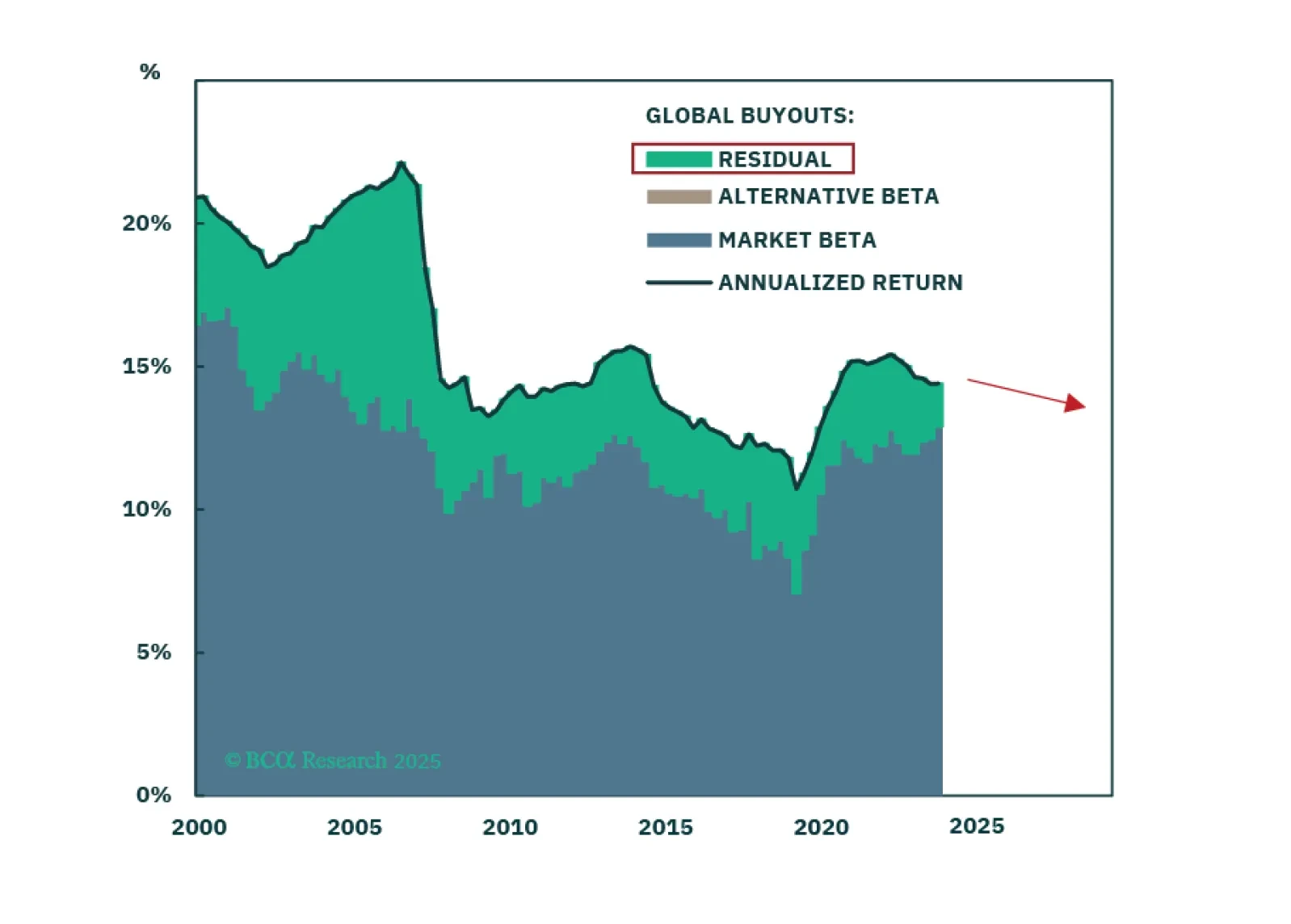

Private Markets are entering a new phase as TPA and Evergreen funds expand. Shifts in access, implementation, and market leadership will have important implications for institutions, Wealth Management, and future Private Equity returns.

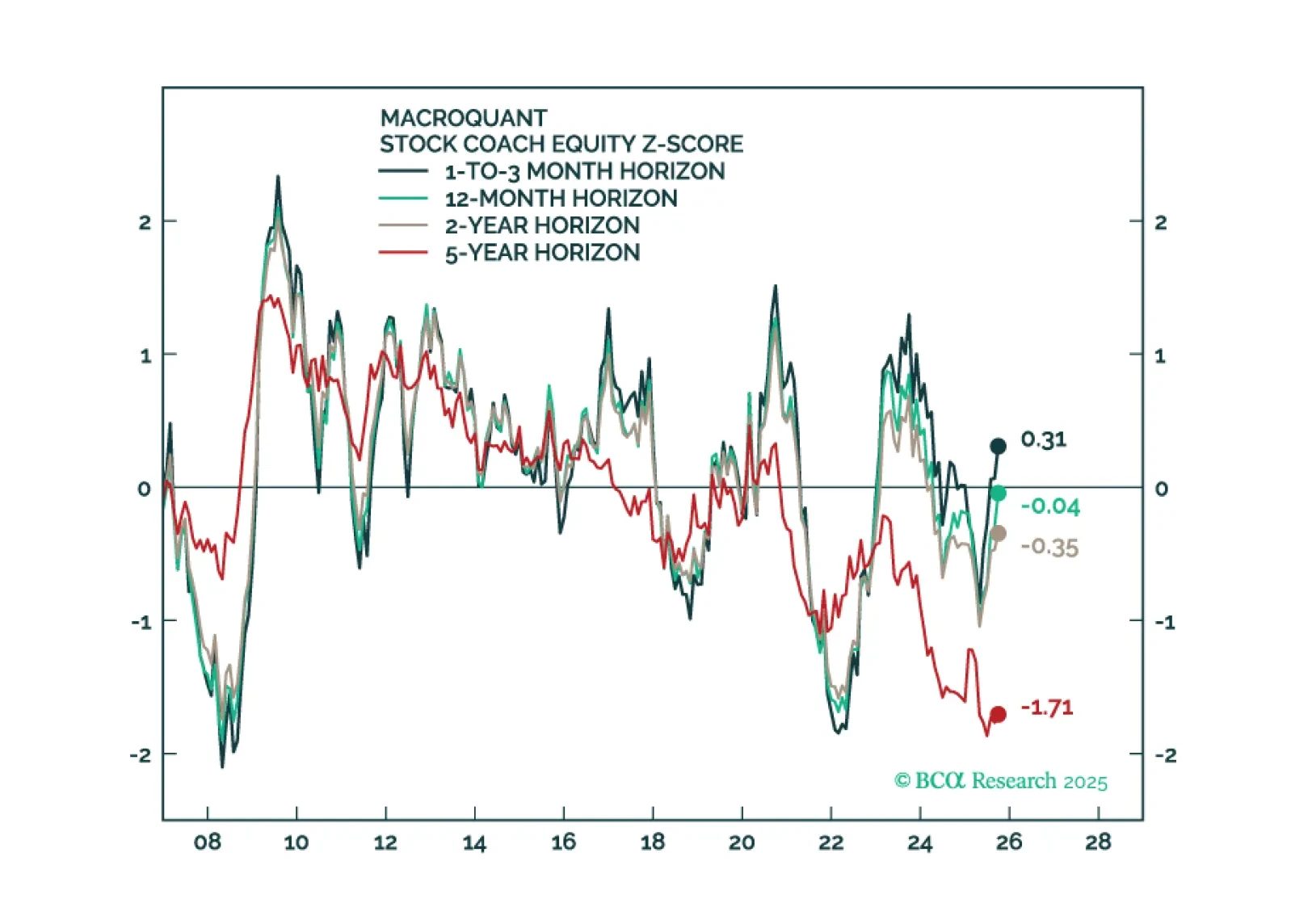

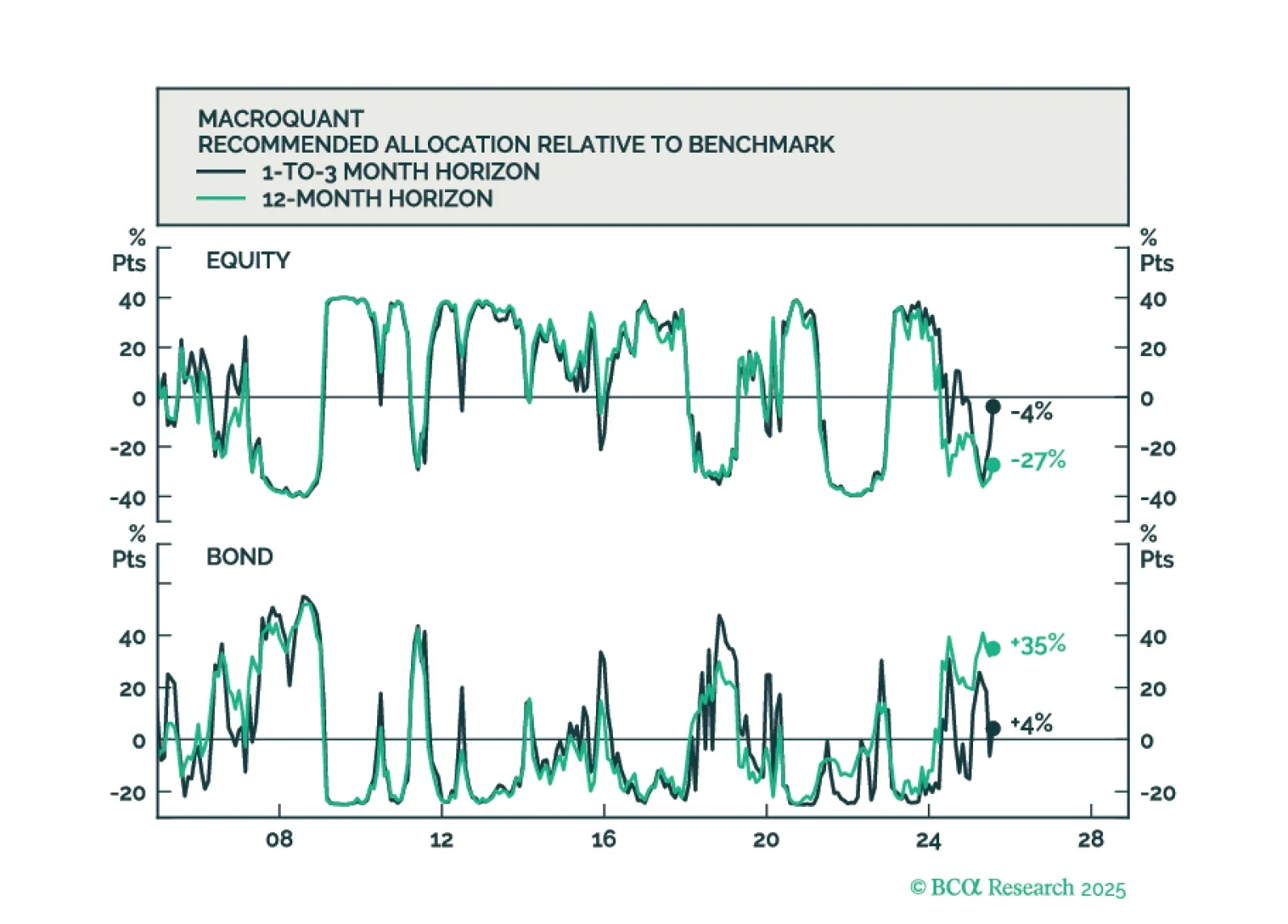

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

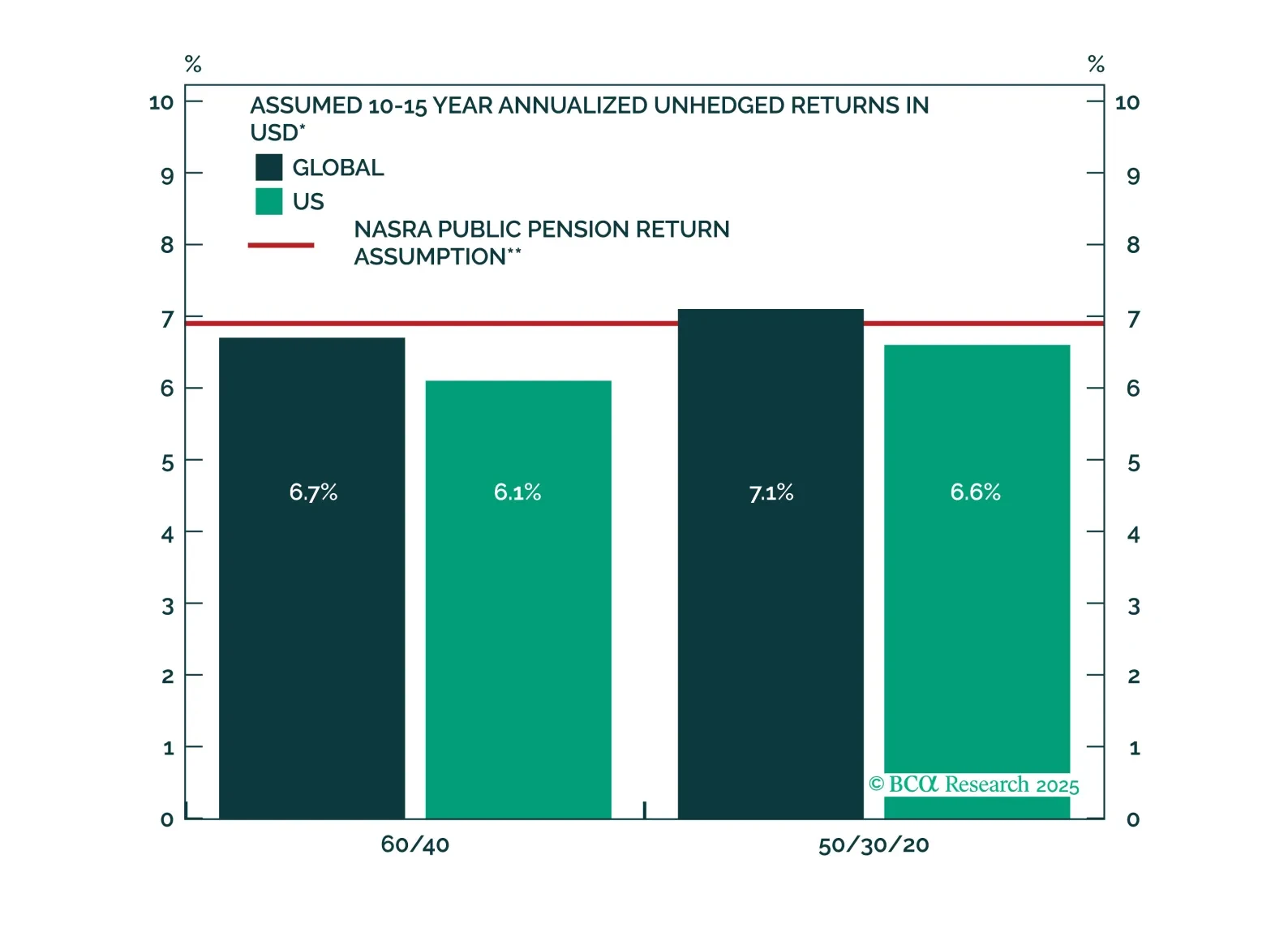

We revamp several of our methodologies in this edition of our return assumptions. We estimate that a US 60/40 portfolio will return 6.1% over the next 10 years. This is slightly below the return assumptions for US pension funds. Investors can obtain better returns by diversifying internationally and to alternative assets.

In our Beta report, we introduce a new framework for thinking about long-term investing in a multipolar world: The Garrison State. Investors need to shed their outdated view that geopolitical risks are... a risk. History teaches us that pressure makes diamonds. And geopolitical pressure makes Garrison States, which tend to outperform precisely because by definition, the bevy of risks that surrounds them is existential.