Asset Allocation

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

Bitcoin’s recent volatility masks a deeper story – the widest disconnect from traditional macro drivers since 2022. With sentiment now deeply negative and institutional demand still building, the conditions for a realignment with fundamentals are falling into place.

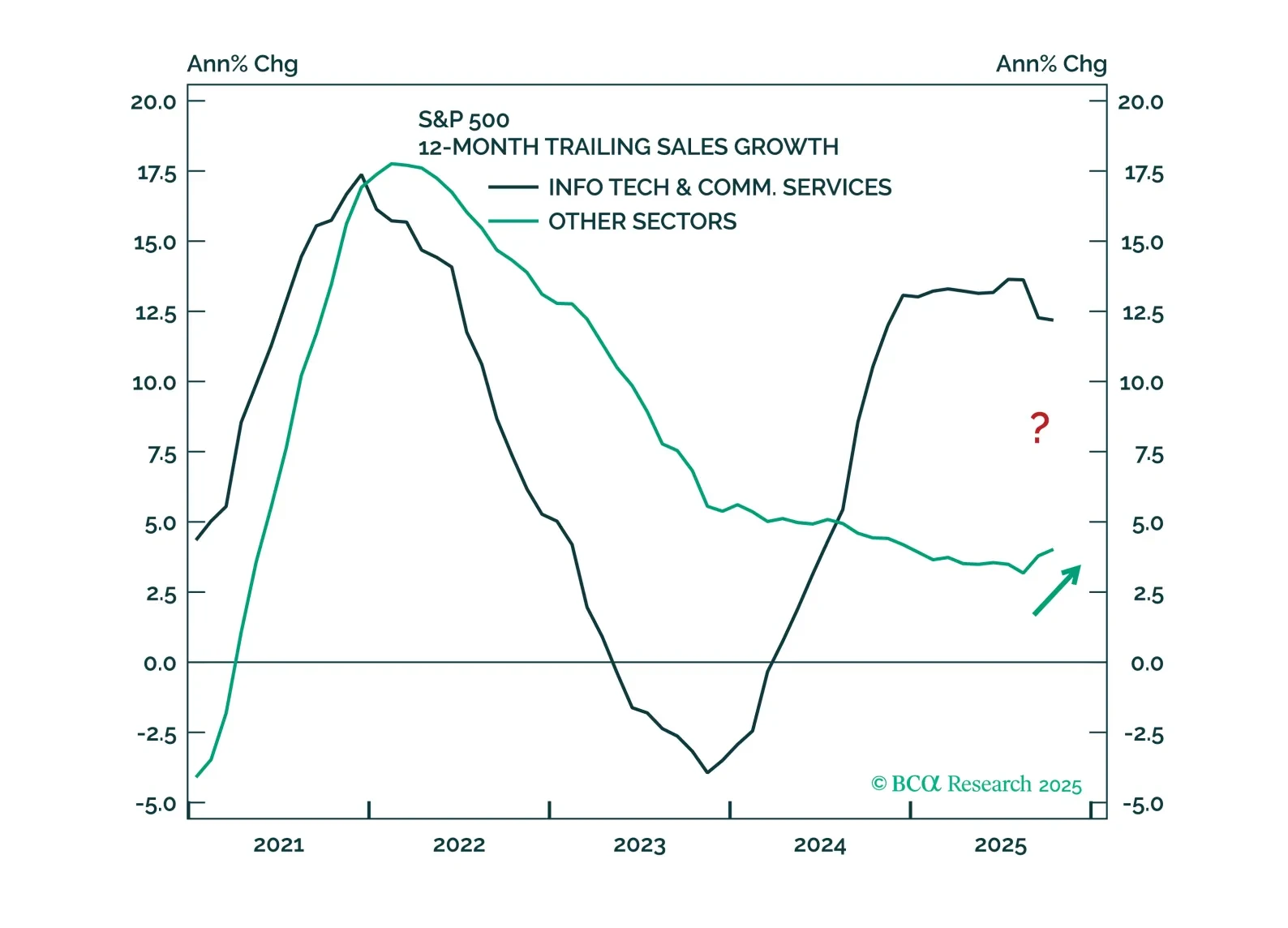

The K-shaped economy will likely reverse in 2026, with the cyclical parts of the economy doing better. Upgrade Financials and Materials from neutral to overweight. Downgrade Communication Services and Utilities from overweight to neutral. Favor value stocks. Upgrade Bitcoin from neutral to overweight.

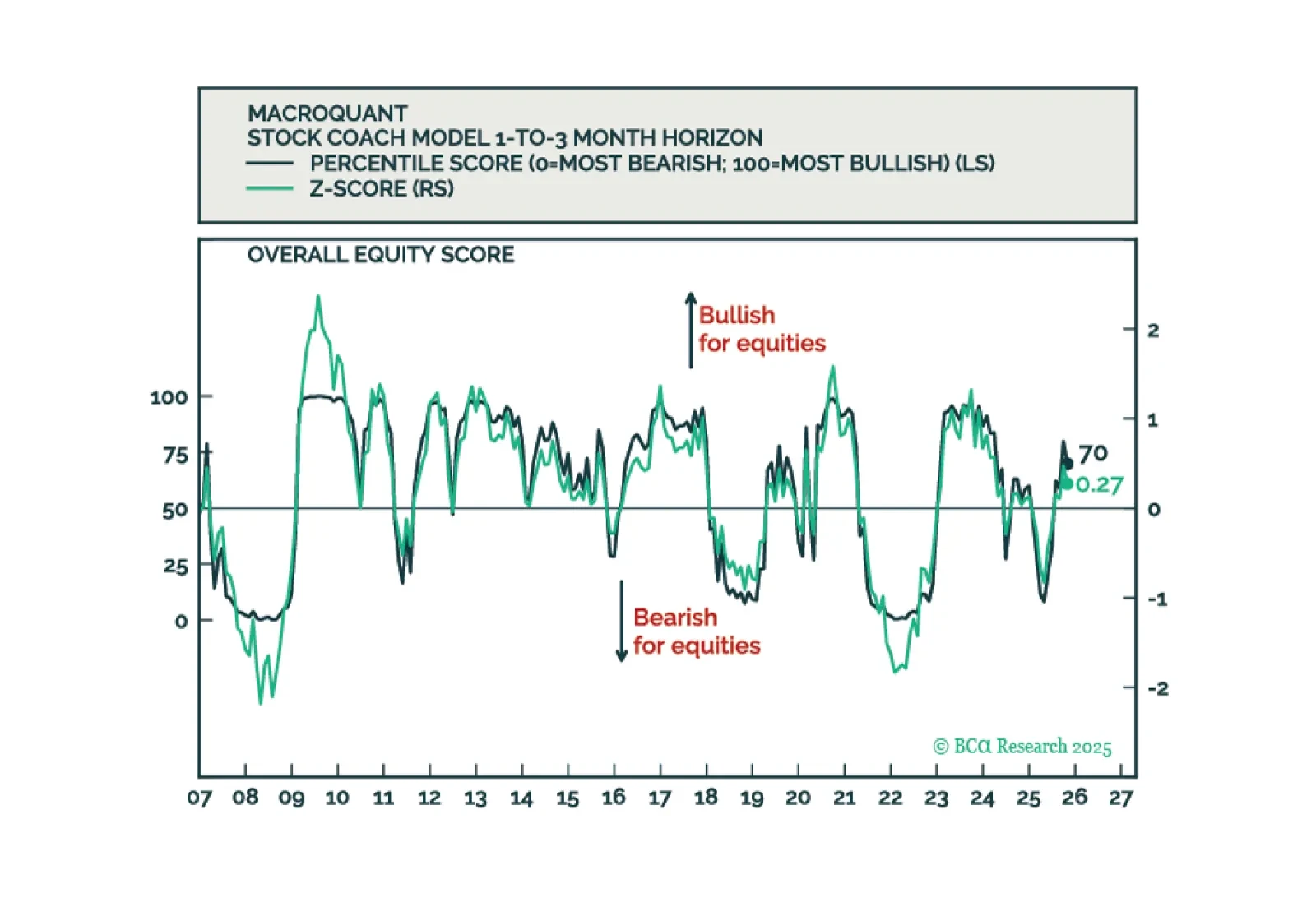

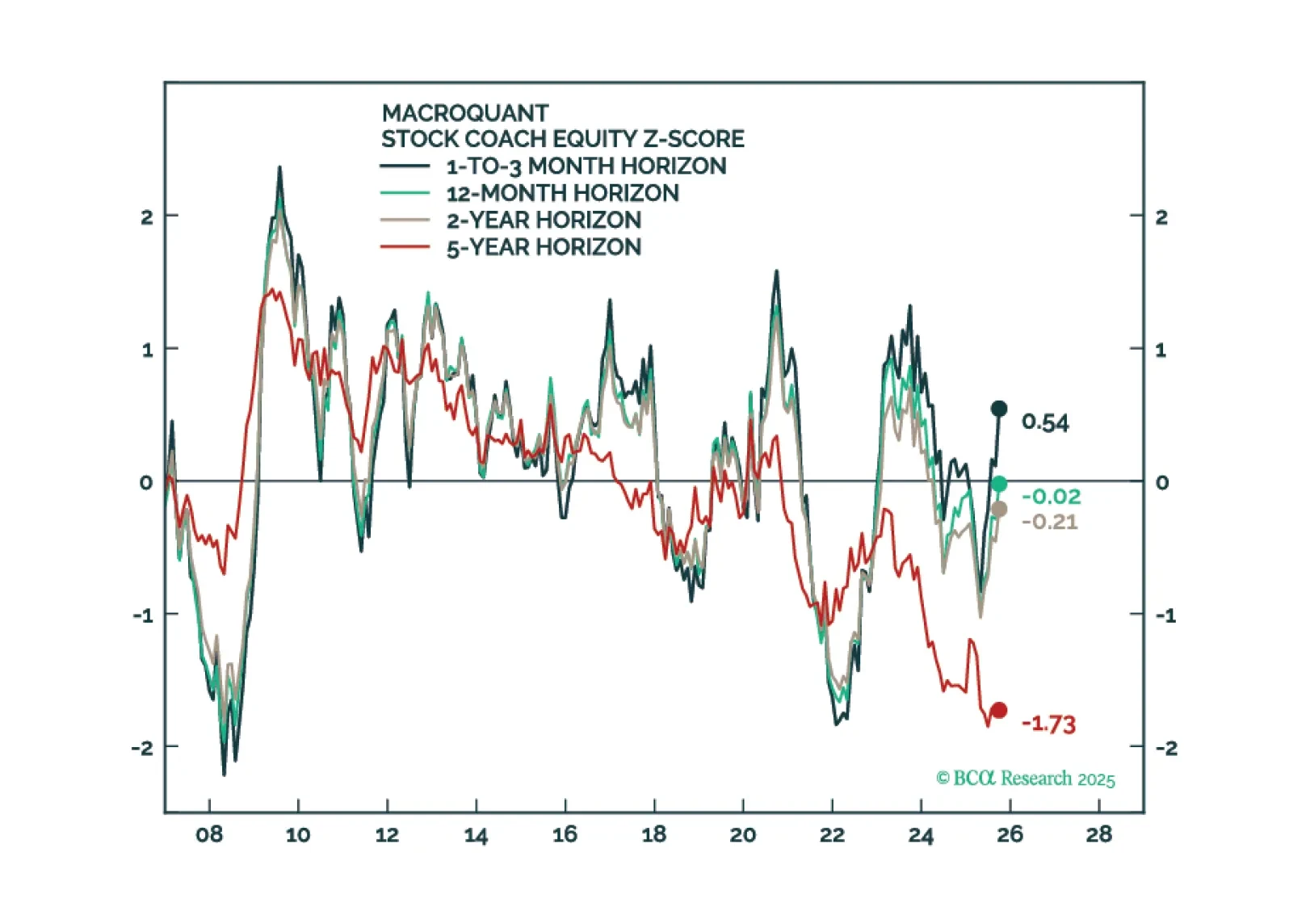

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

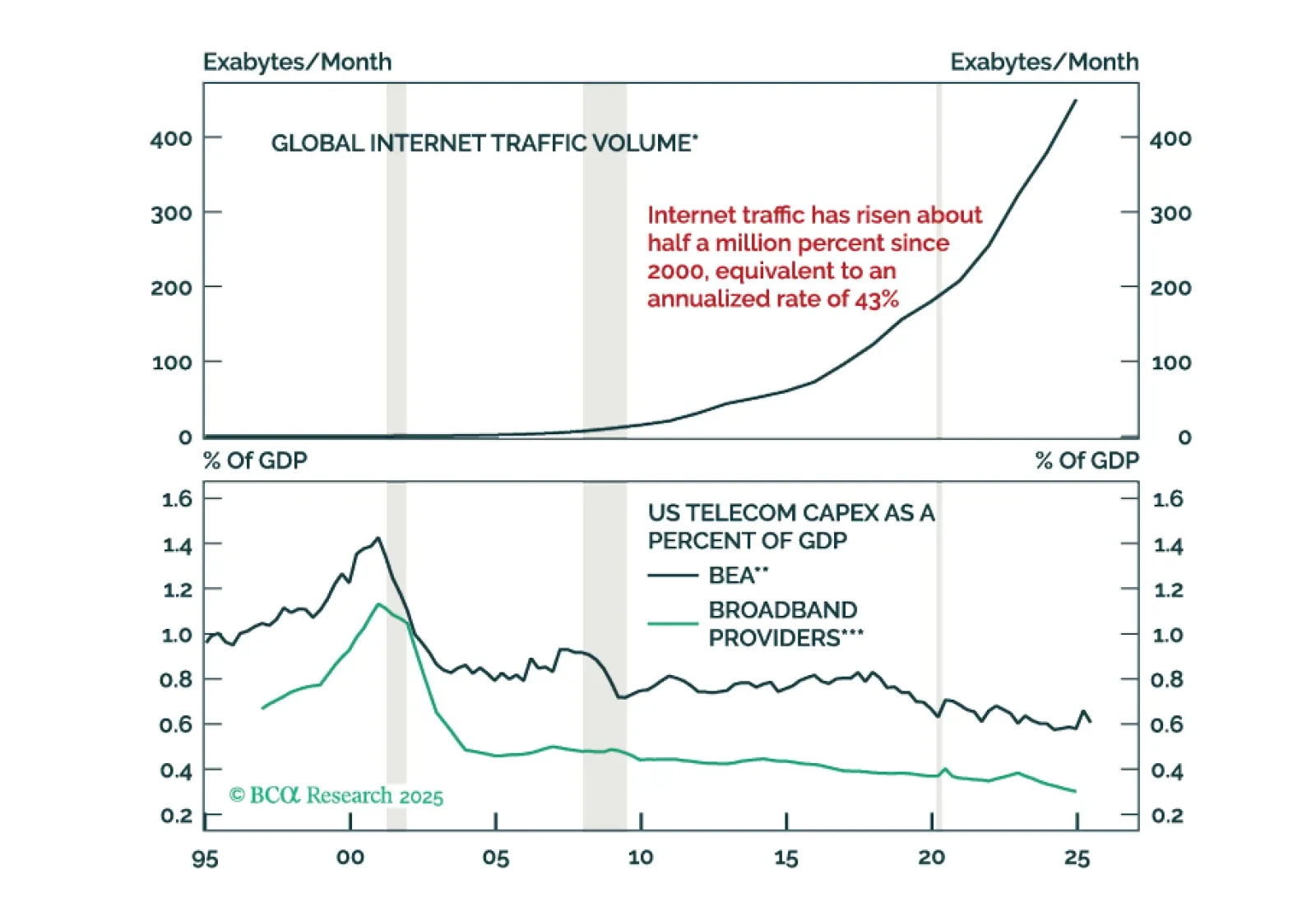

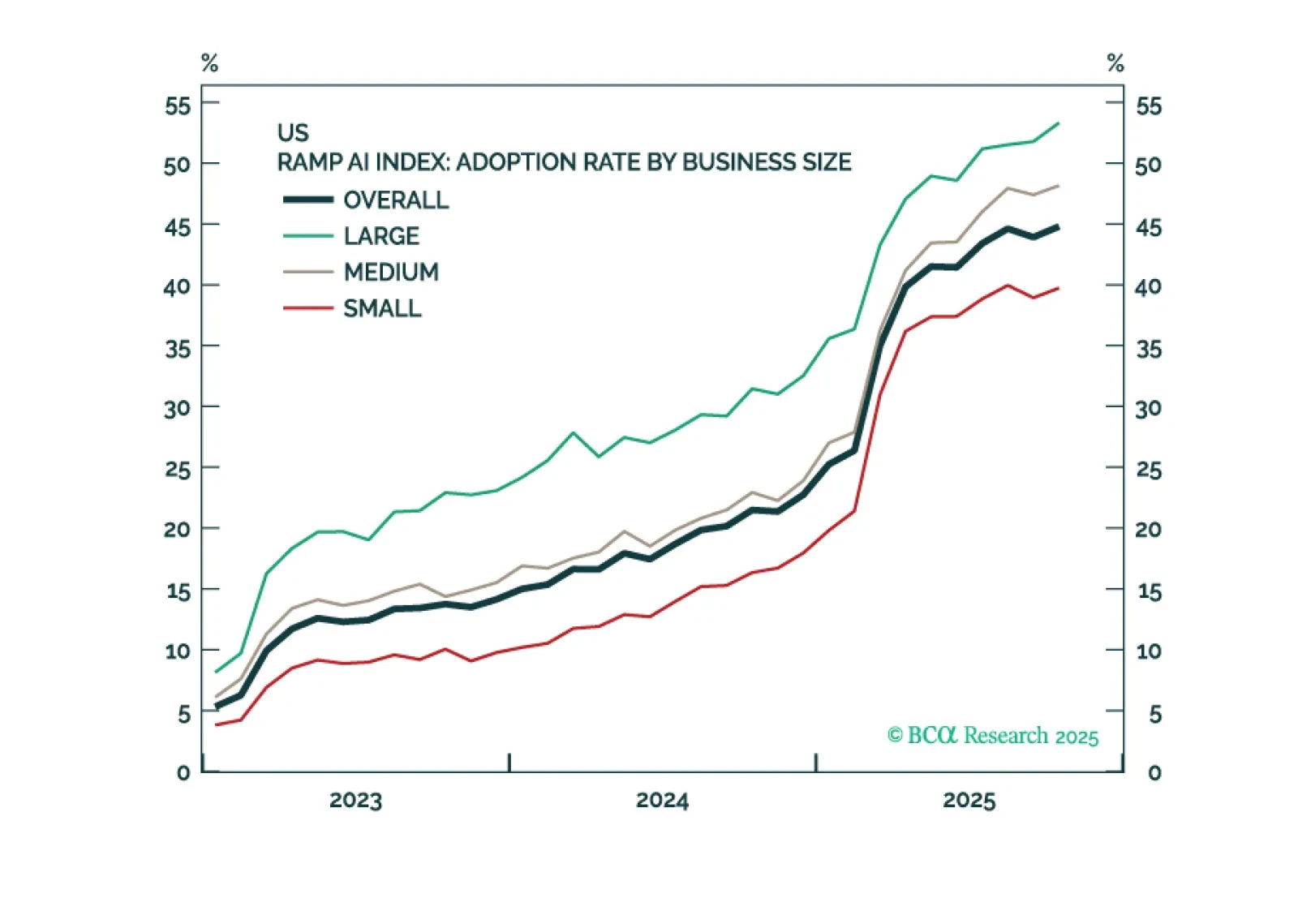

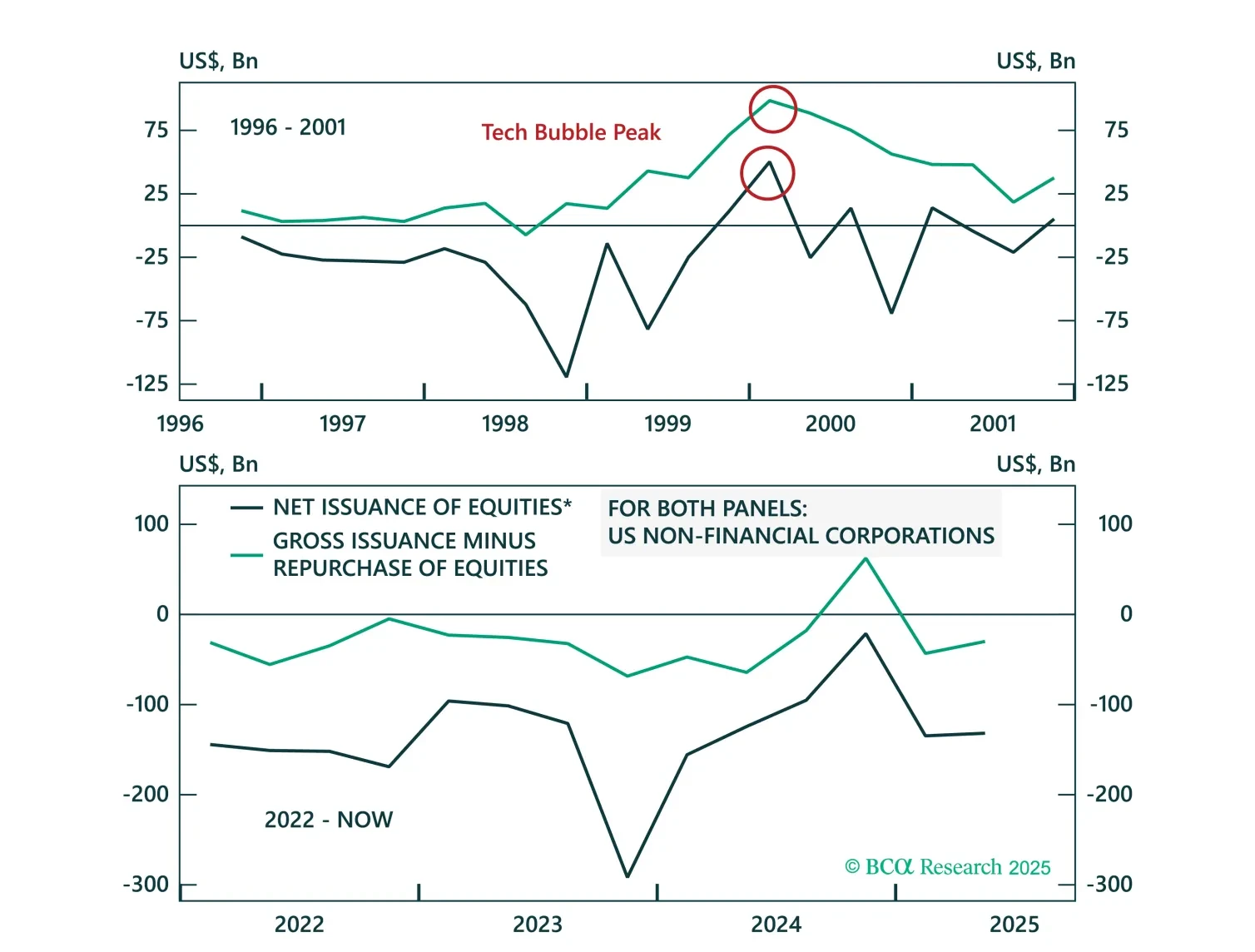

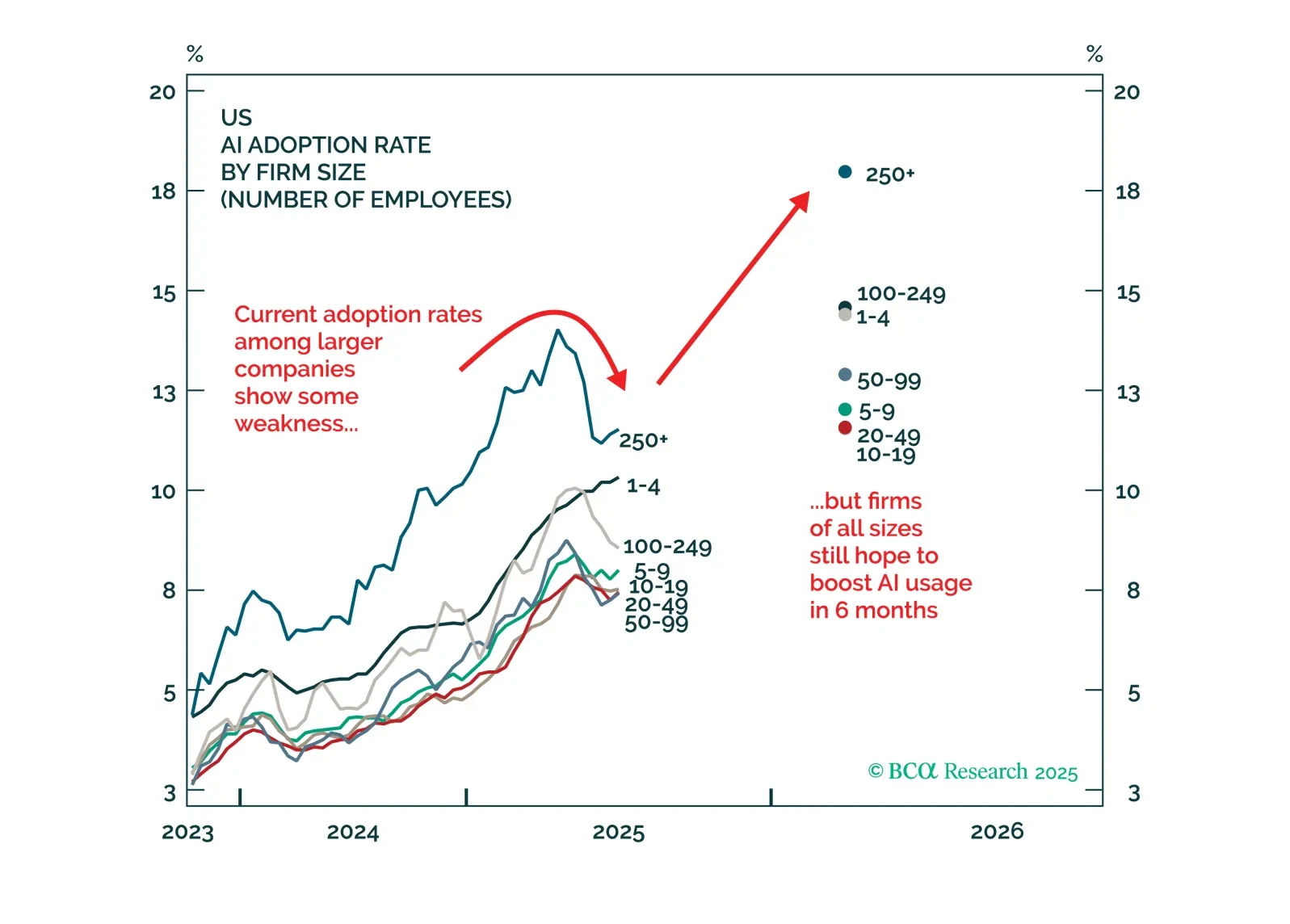

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

Today, we are sending you the BCA annual outlook for 2026. The report is an edited transcript of our recent conversation with Mr. X and his daughter Ms. X, who are long-time BCA clients. Our discussion featured BCA’s economic and financial market outlook for the year ahead.

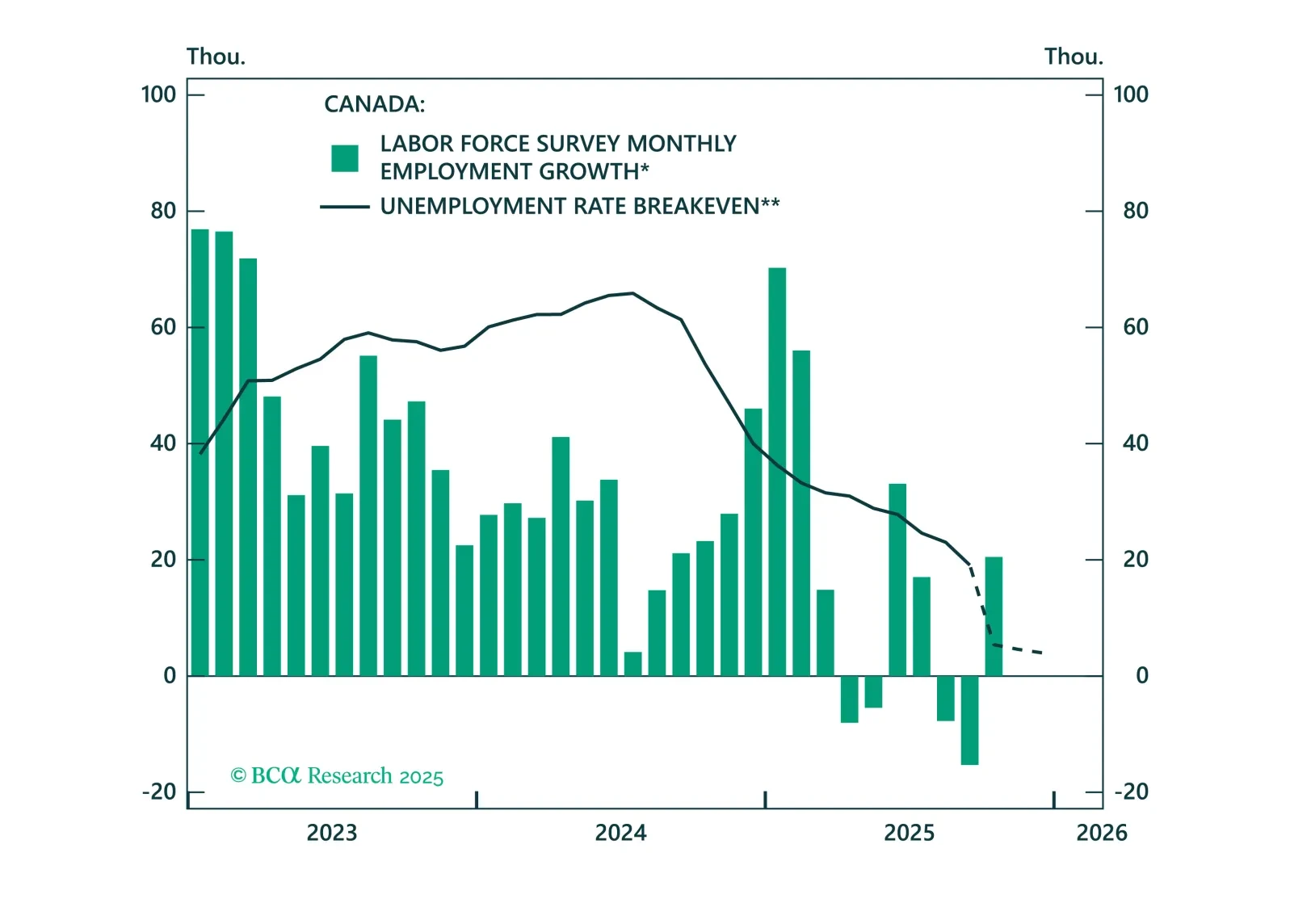

The trade war hit Canada’s economy hard, but the worst is over. In our latest update on Canada, we assess the aftermath of the trade shock, the new budget, and the effects of BoC easing. We outline what this means for duration, the Loonie, and Canadian stocks heading into 2026.

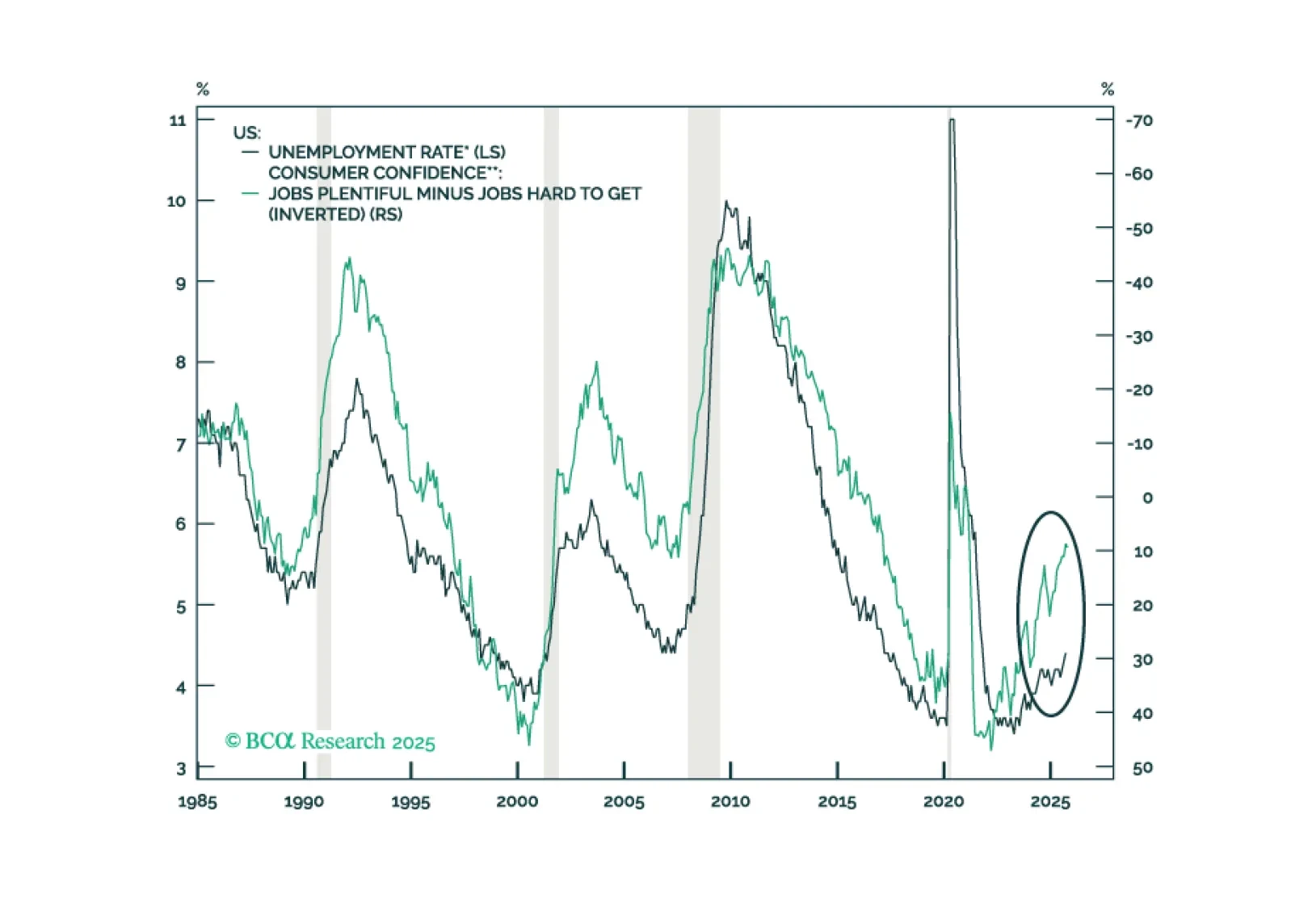

We discuss which variables we are tracking to assess the risks to the bull market in the absence of government data. So far, we do not see any obvious red flags. Remain overweight on equities and fixed income.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

The rush to build AI infrastructure is based on a false premise: that there are significant advantages to being the first to come to market.