Asset Allocation

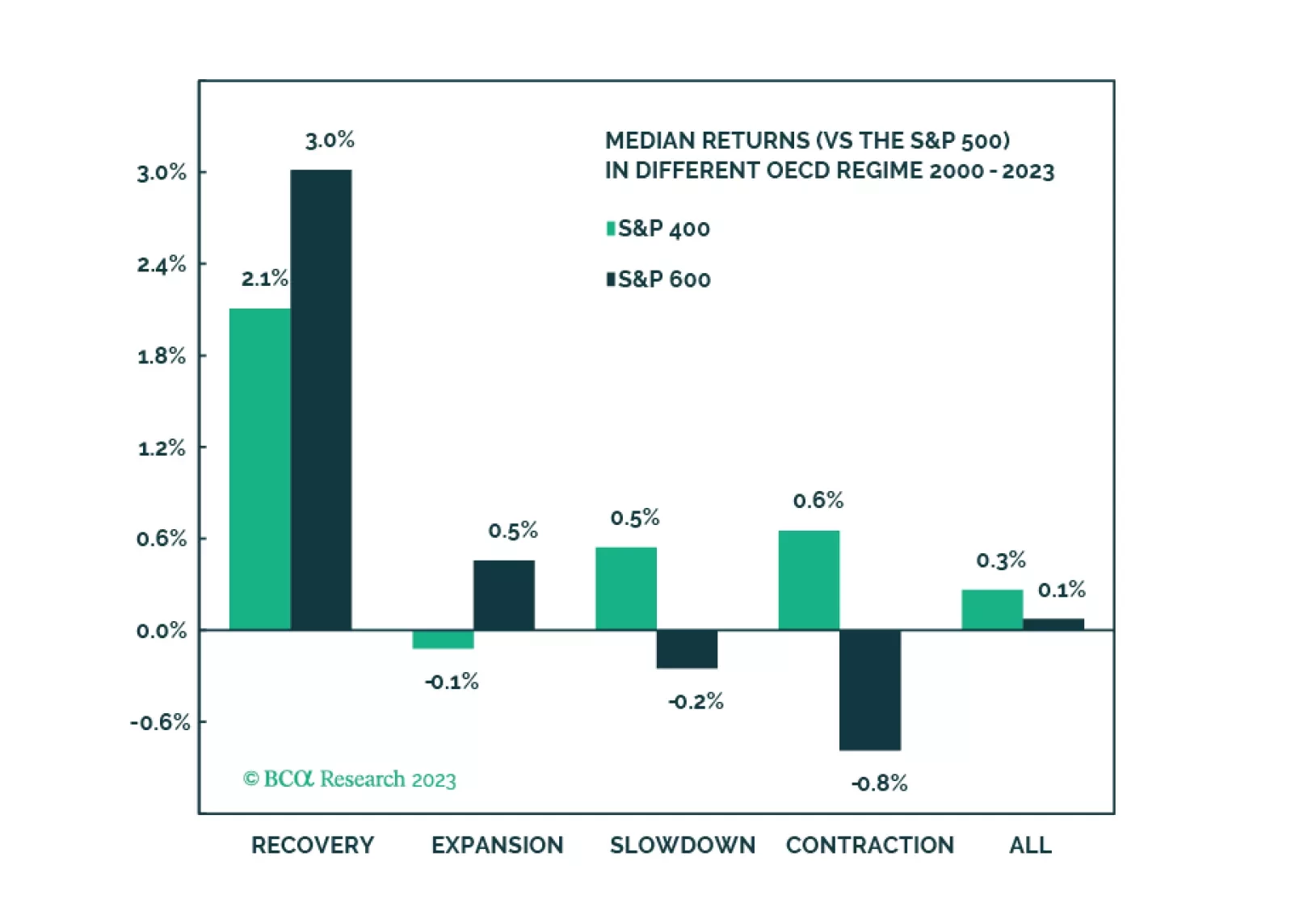

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

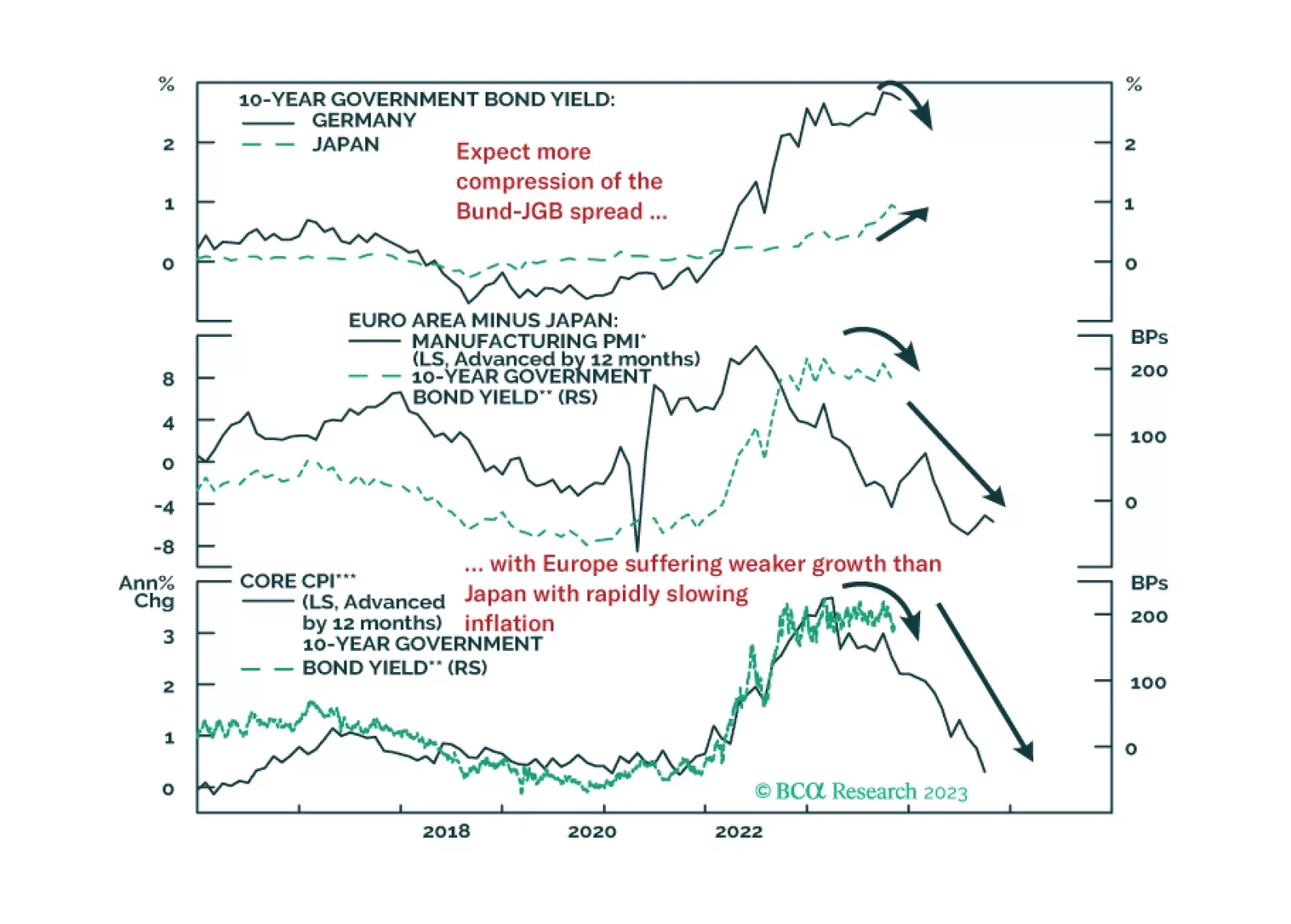

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

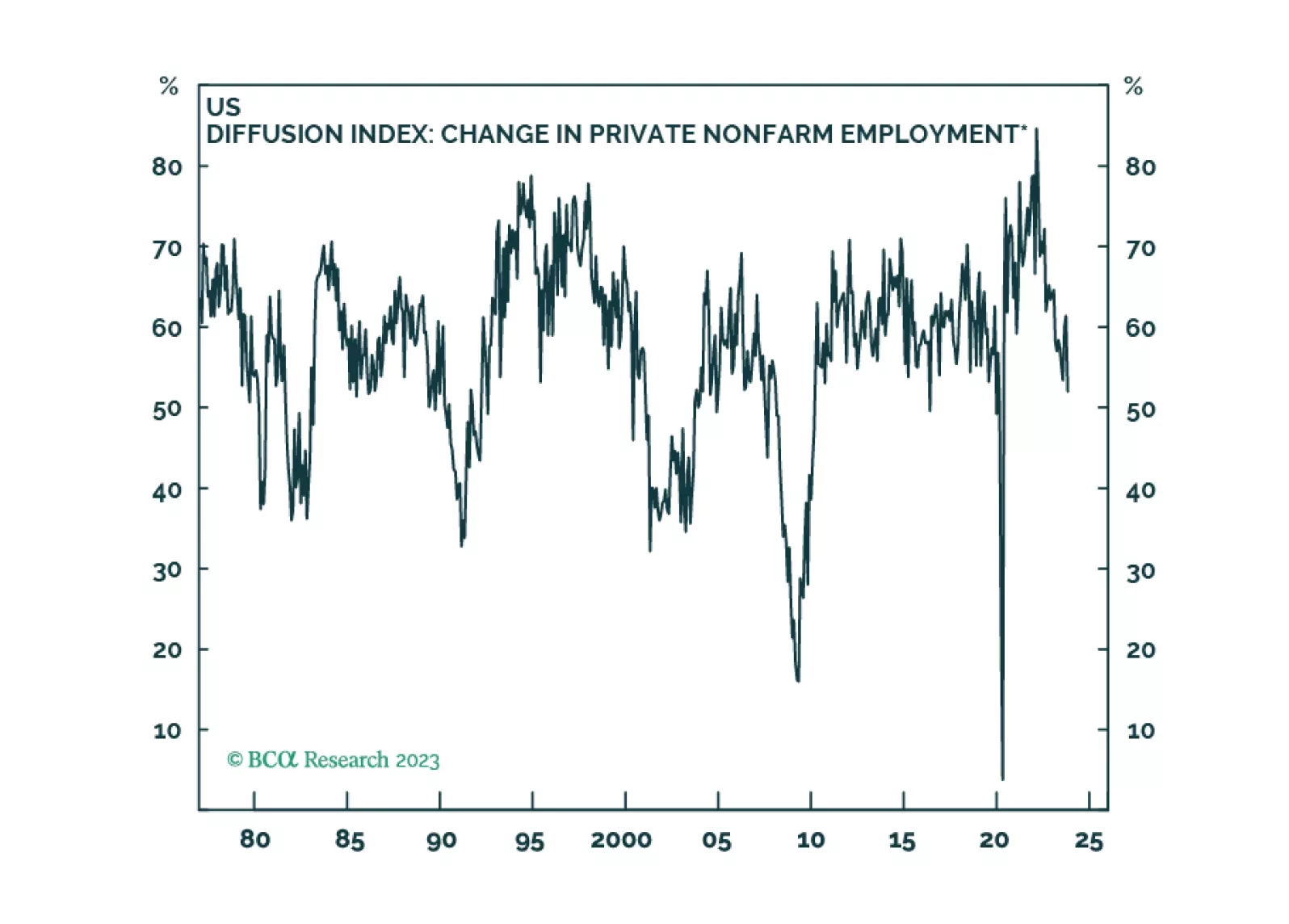

Labor markets are softening in most developed economies, as is usually the case in the lead-up to recessions. Our base case is that the global recession will begin in the second half of 2024, but we will be monitoring our MacroQuant model on a daily basis for confirmation.

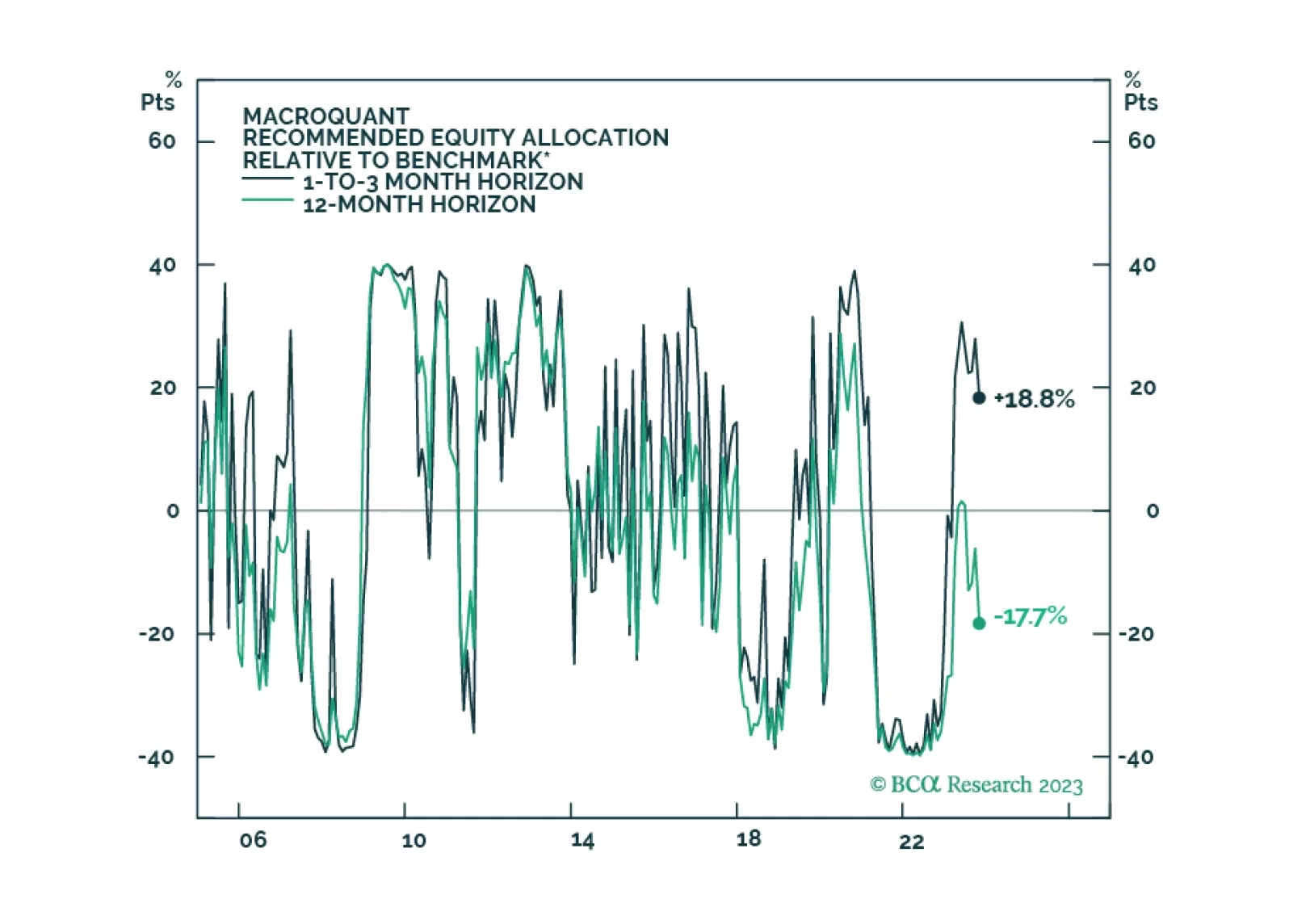

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.