Asset Allocation

The global economy is wobbling precariously between slowing growth and reaccelerating inflation. This is unlikely to end well. Stay cautious, and hedge against both recession and inflation.

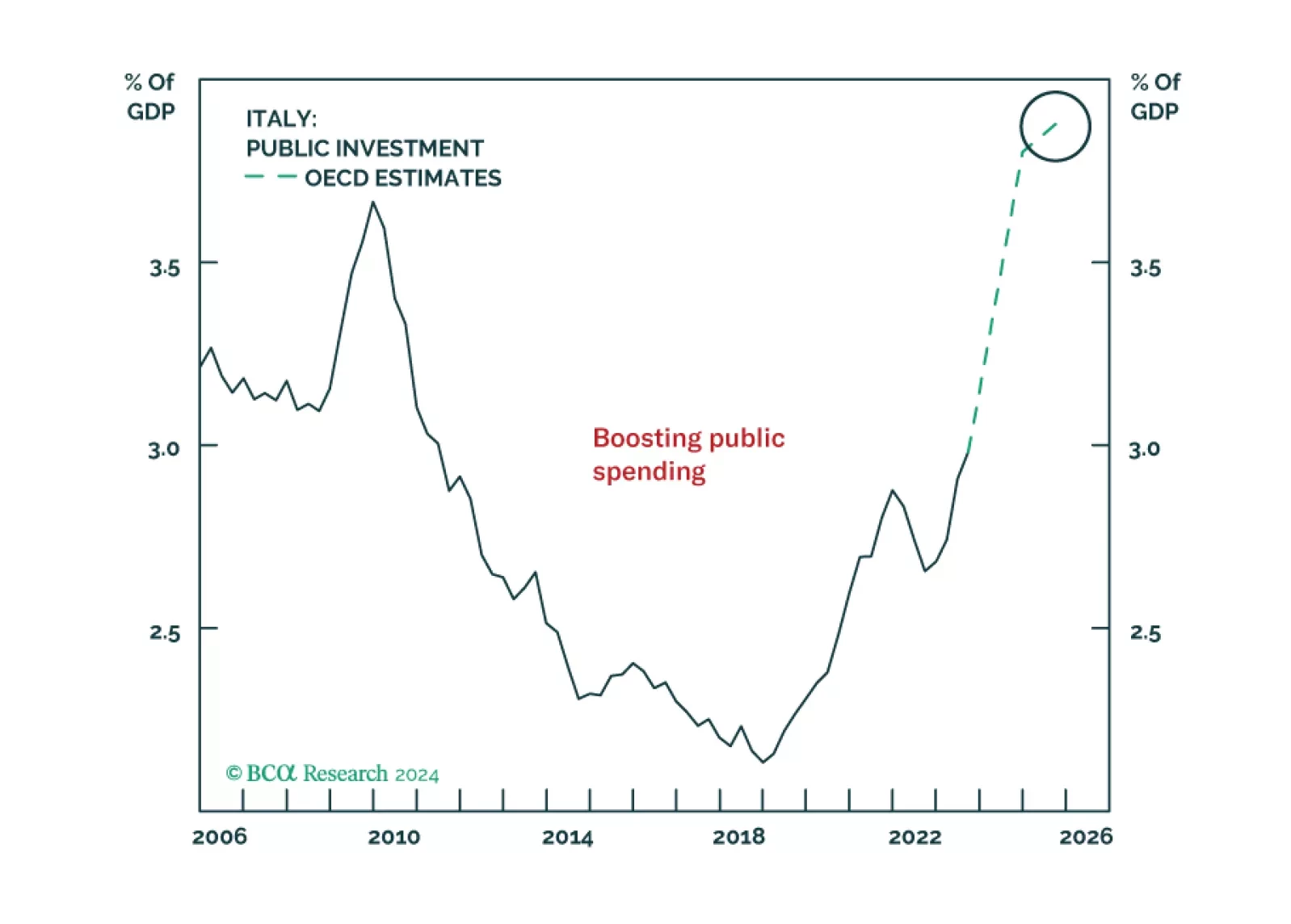

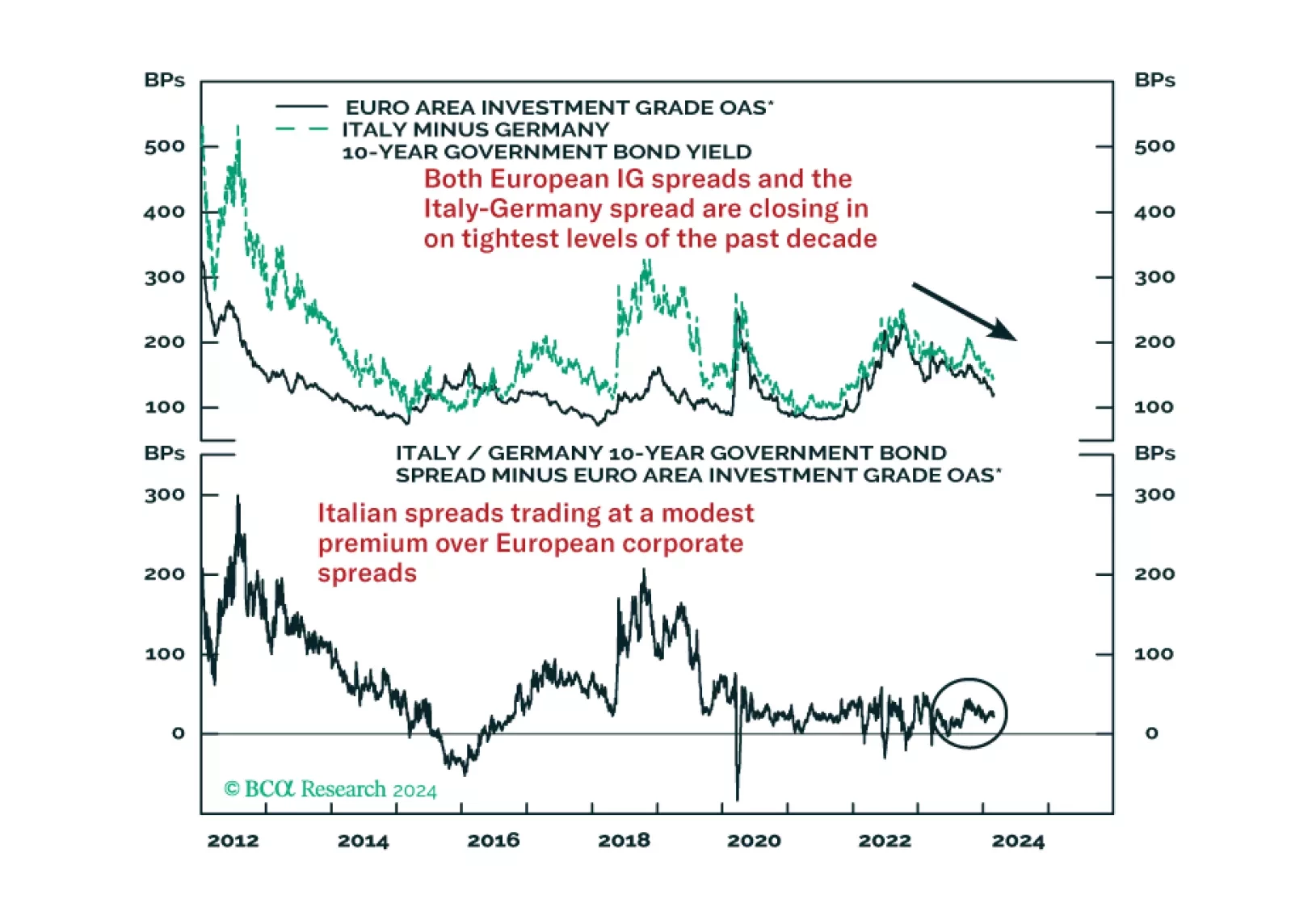

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.

MacroQuant downgraded equities from overweight to neutral on a 1-to-3 month horizon. The model maintains a negative view on stocks over a 12-month horizon.

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

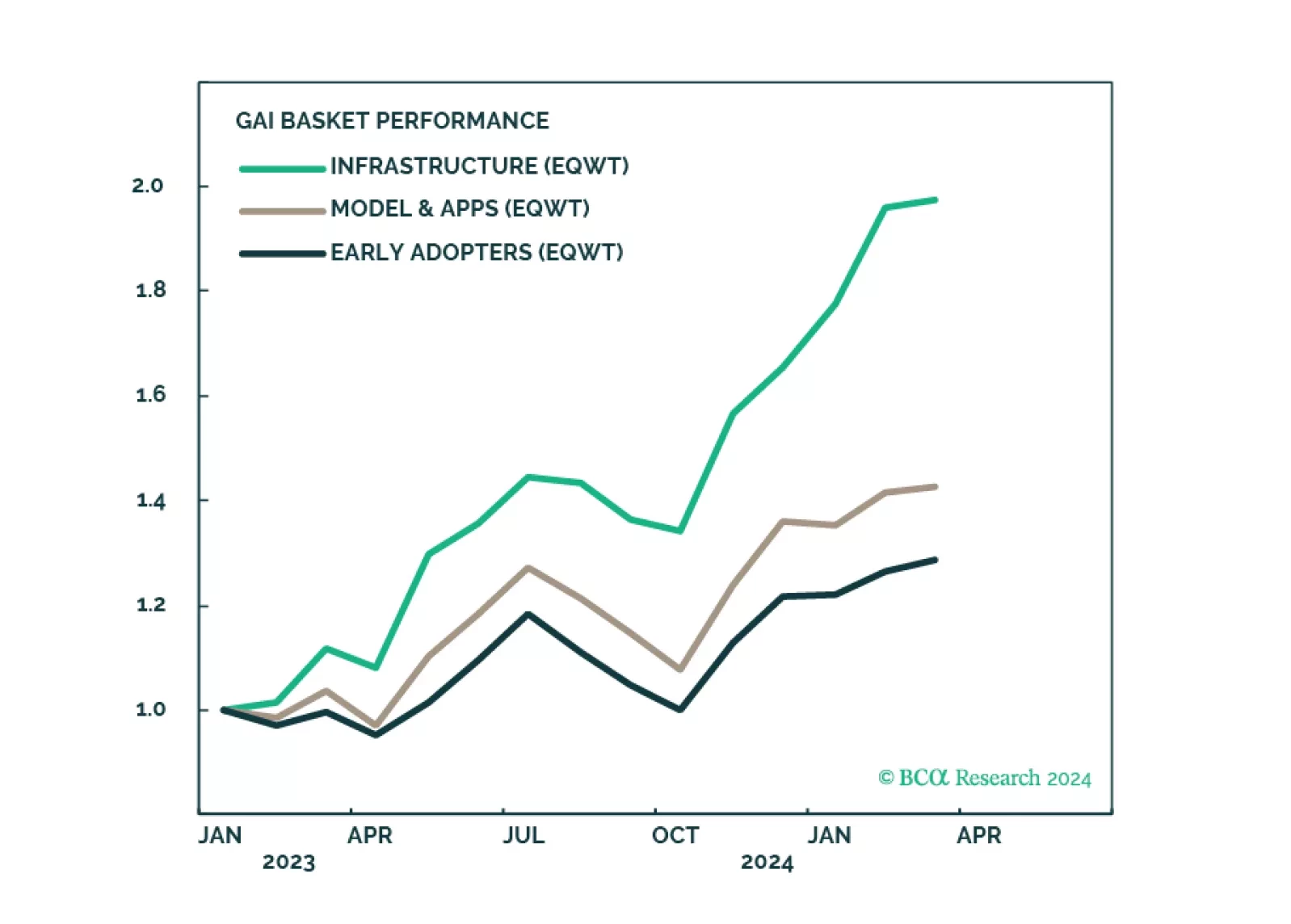

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

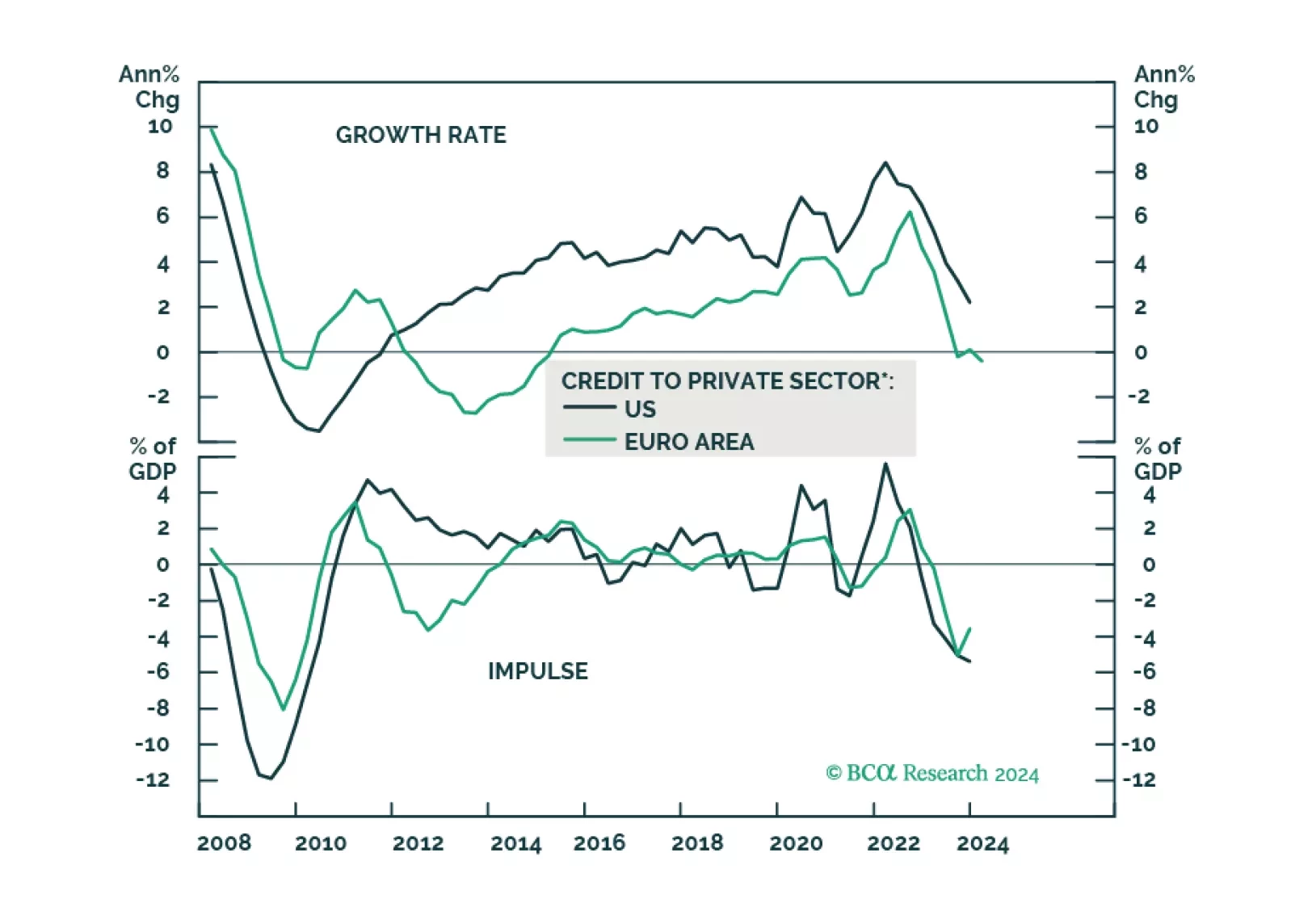

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

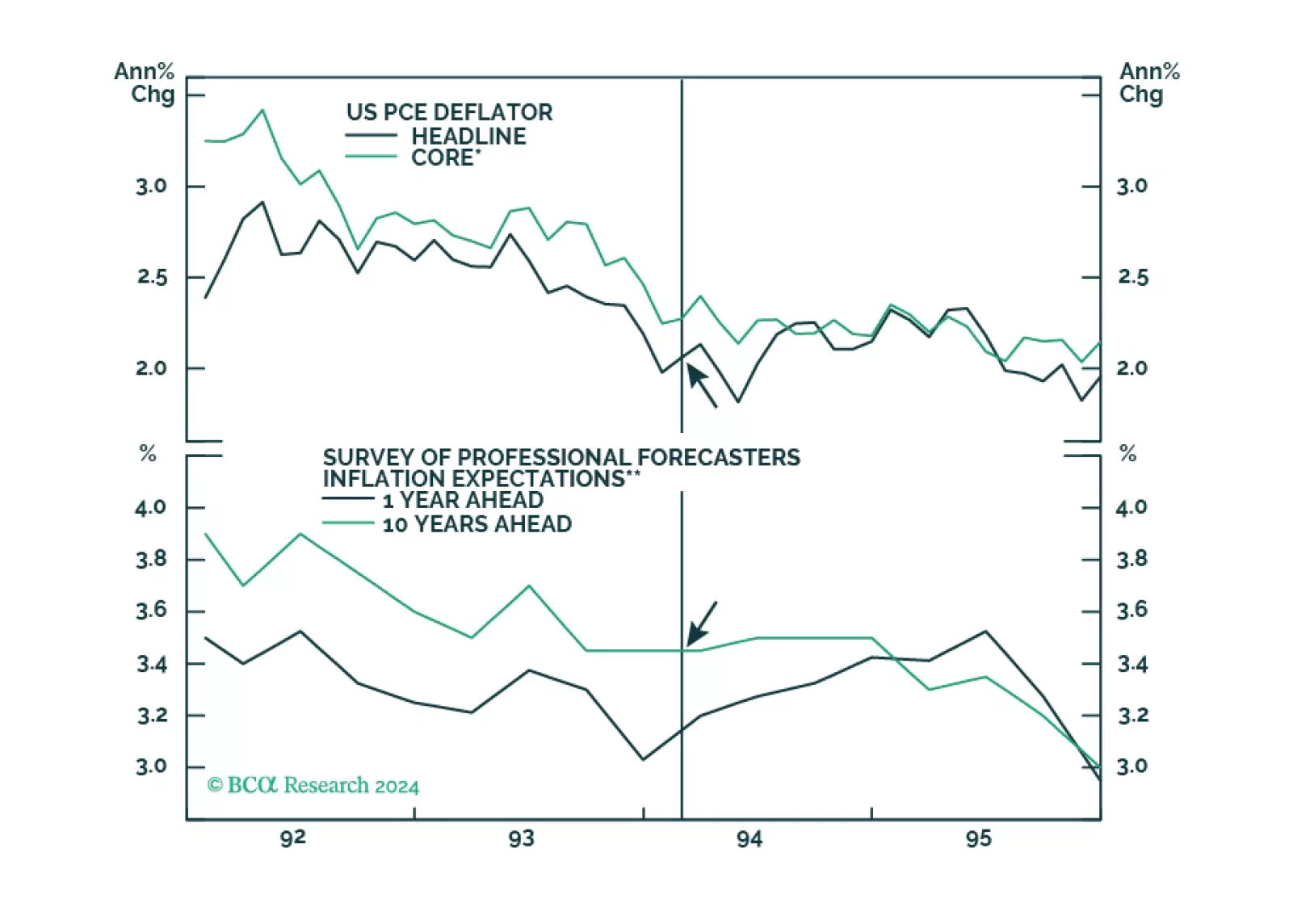

Many investors have cited the 1994 tightening cycle as an example of how the Fed managed to raise rates without triggering a recession. However, the unemployment rate was 6.5% in early 1994, which meant that inflation was less of a risk than it is today. Productivity growth also accelerated starting in the mid-1990s. While something similar may happen again thanks to AI, so far this is not visible in the aggregate productivity data.

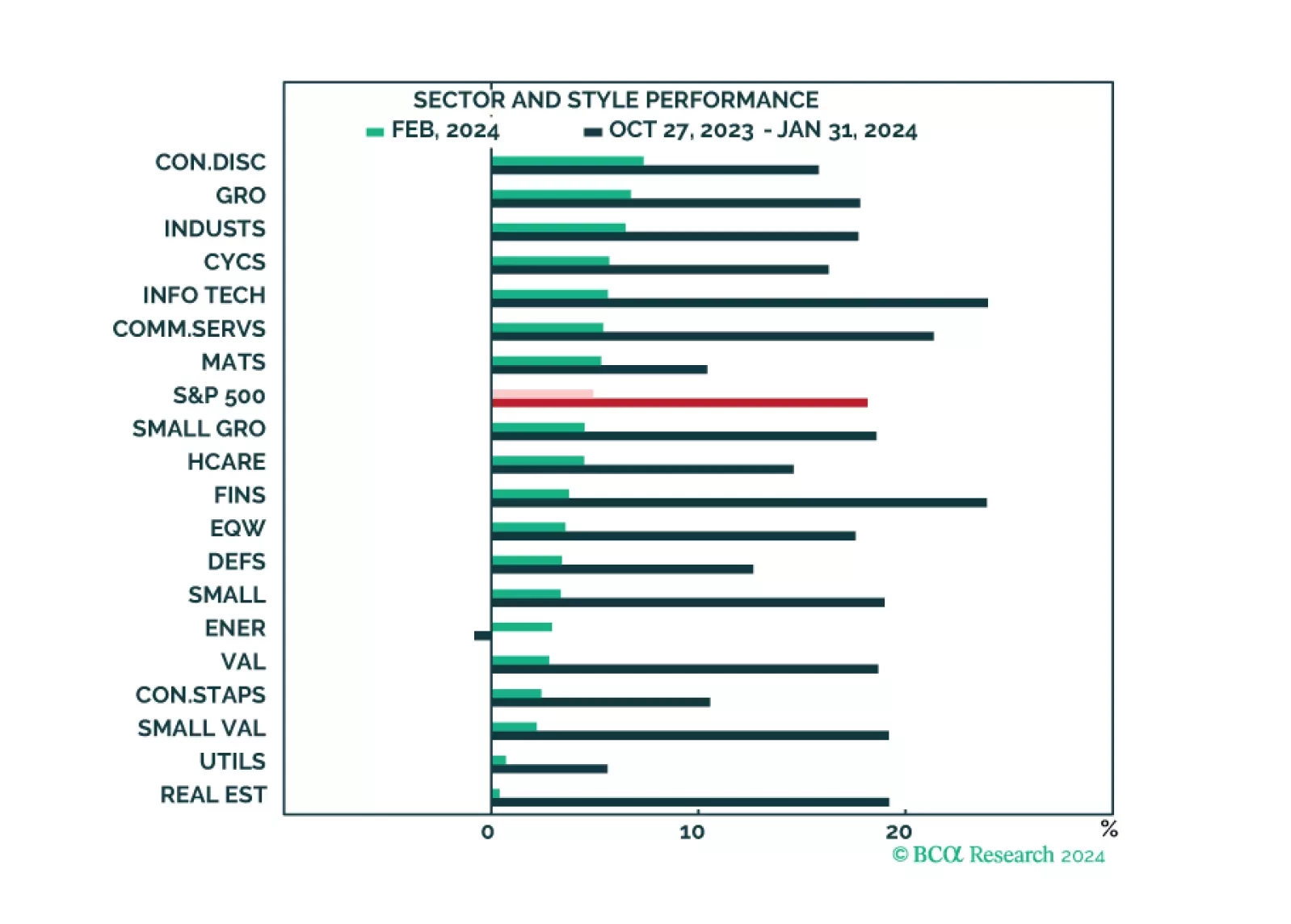

The market narrative continues to be dominated by the Magnificent Six, which drove both market performance and strong Q4 earnings results. While all sectors and styles have recently turned green, the rally is still mostly narrow. Earnings growth appears to be strong, but outside of the Magnificent Six, many companies are struggling. The market appears expensive and overbought, but that is mostly down to the high valuations and the popularity of the Magnificent Six.

In this Strategy Insight, we take a comparative look at two of the largest spread product sectors in Europe – Italian government bonds and investment grade corporates. We make the case for favoring Italy over investment grade in the event of a downturn in European economic sentiment.