Asset Allocation

According to our Bank Credit Analyst service, an inflection point in the relative performance of US stocks is not likely to occur over the coming 6-12 months. A recession favors US equities in common currency terms barring substantially less global ex-US…

Preliminary estimates suggest that US durable goods orders growth rebounded sharply from a 6.9% m/m contraction to 9.9% growth in July, upending expectations of a more muted 5.0% monthly increase. However, a 34.8% m/m rise in transportation equipment orders…

We’ve highlighted that continued deterioration in consumer fundamentals will tip the US economy into a recession. Slower compensation growth, tighter lending standards for consumer loans and dwindling excess savings will constrain spending in an economy where…

Back in May, our Commodity and Energy strategists argued that OPEC, EIA, and IEA oil demand forecasts were likely too optimistic. Indeed, while all three major oil price forecasters projected a moderation in demand this year, none of them anticipated weak…

It didn't take long for markets to utterly shrug off the surprise rise in July's unemployment rate. On Tuesday, the S&P 500 closed higher than it was the day before the July Employment Situation report was released. The Russell 2000 gained 5.2% since…

EM equities have dramatically underperformed their US and Eurozone peers in USD terms over the past 15 years. The inability of EM and EM Asia companies to grow their EPS largely explains EM equities “lost decade” (and a half). Since 2010, US EPS have grown…

Markets have recouped some of the losses incurred in the aftermath of the July US Employment Situation report. Was the surprise rise in the unemployment rate a false alarm? Supply-side dynamics alone cannot explain the overall rise in the unemployment…

Chinese exports in USD terms missed expectations in July, growing by 7.0% y/y, down from 8.6% in June. Conversely, imports rebounded smartly from a 2.3% contraction, rising by 7.2% in July and upending expectations of 3.2%. Slower export growth is…

August’s selloff has featured a rotation out of Big Tech. The Nasdaq shed 8% across Thursday, Friday, and Monday, led by concentrated selling among several Mega caps. Nvidia, Tesla, Microsoft and Amazon shed 14%, 14%, 6% and 14% over the last three sessions,…

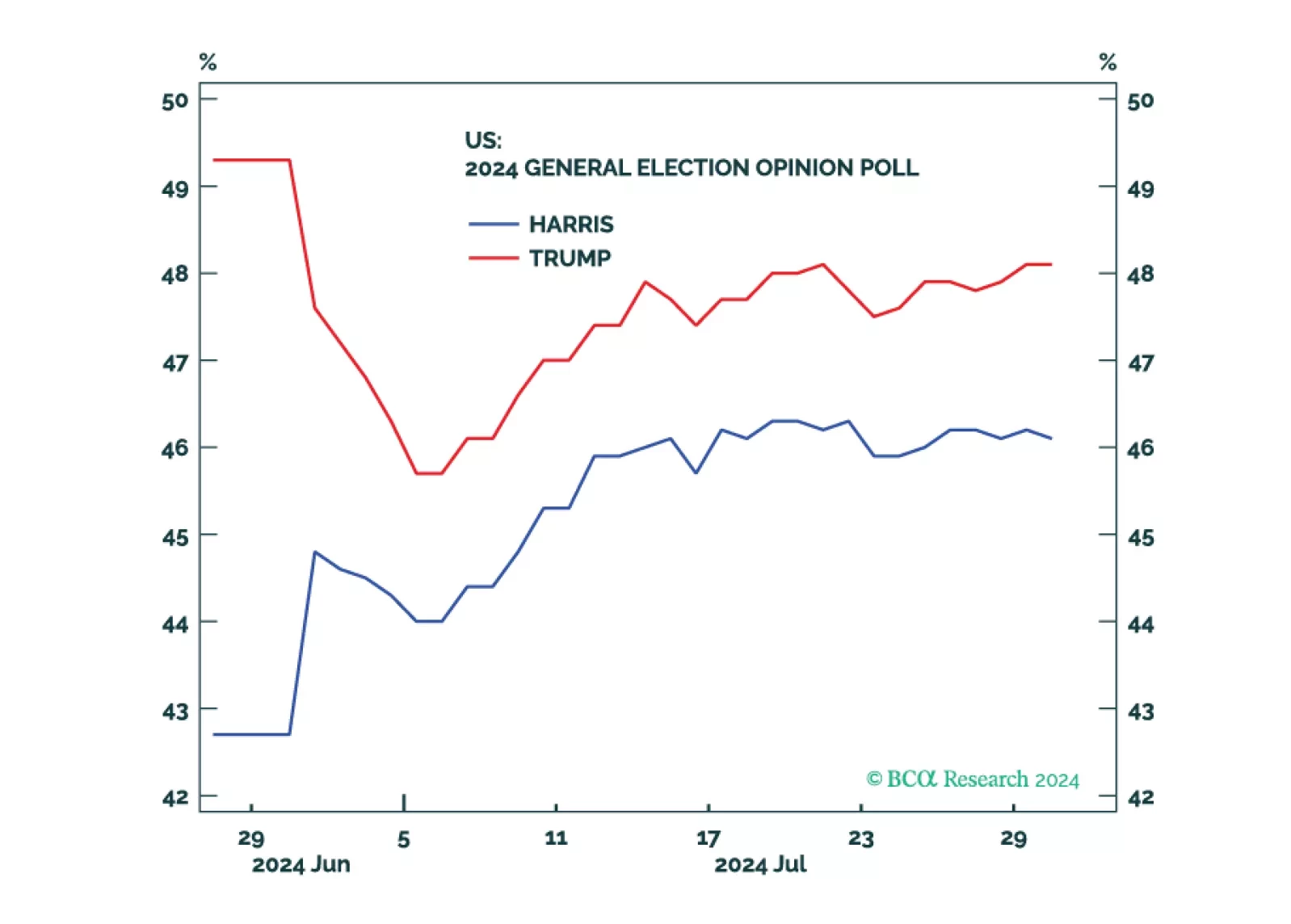

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.