Asset Allocation

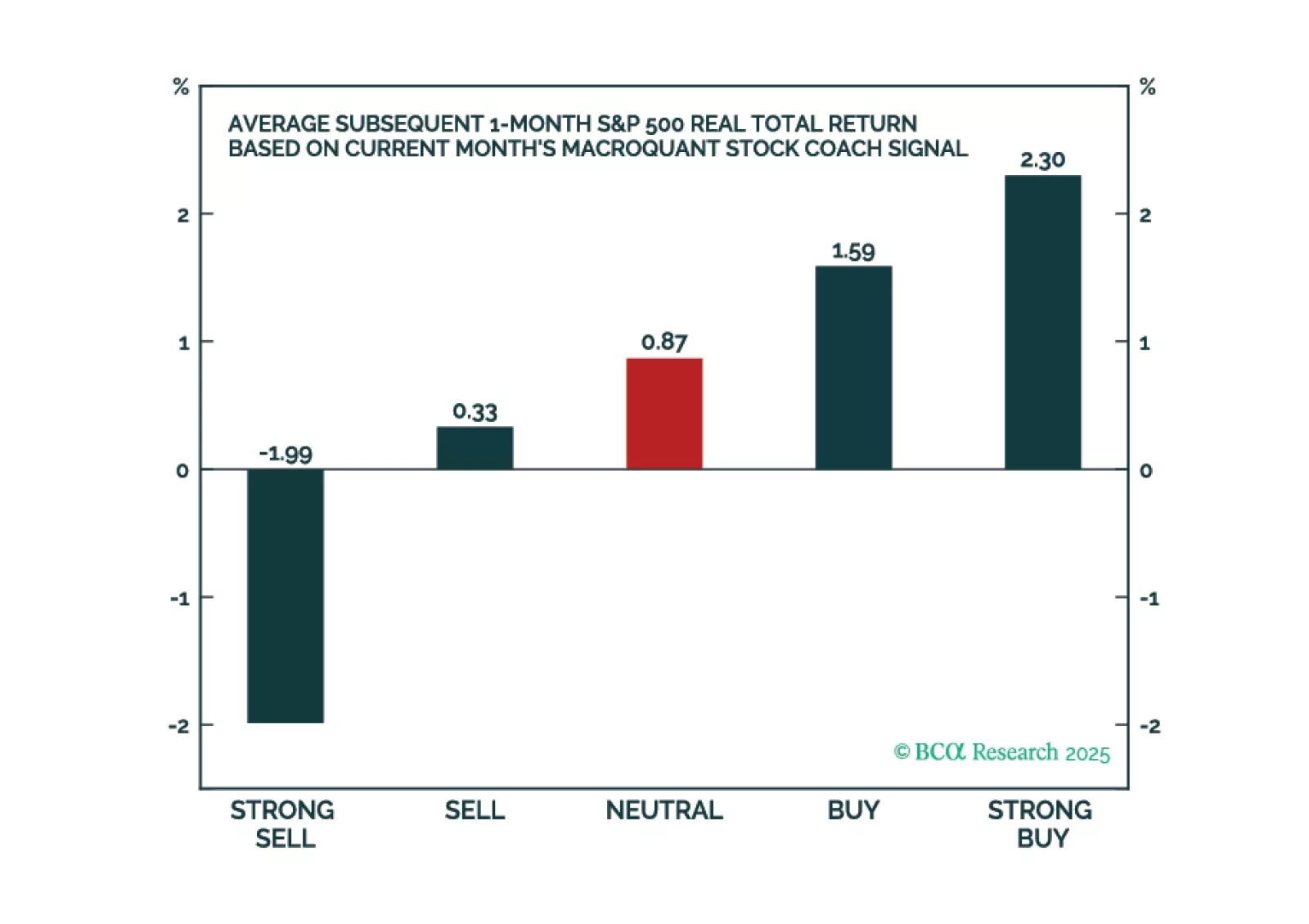

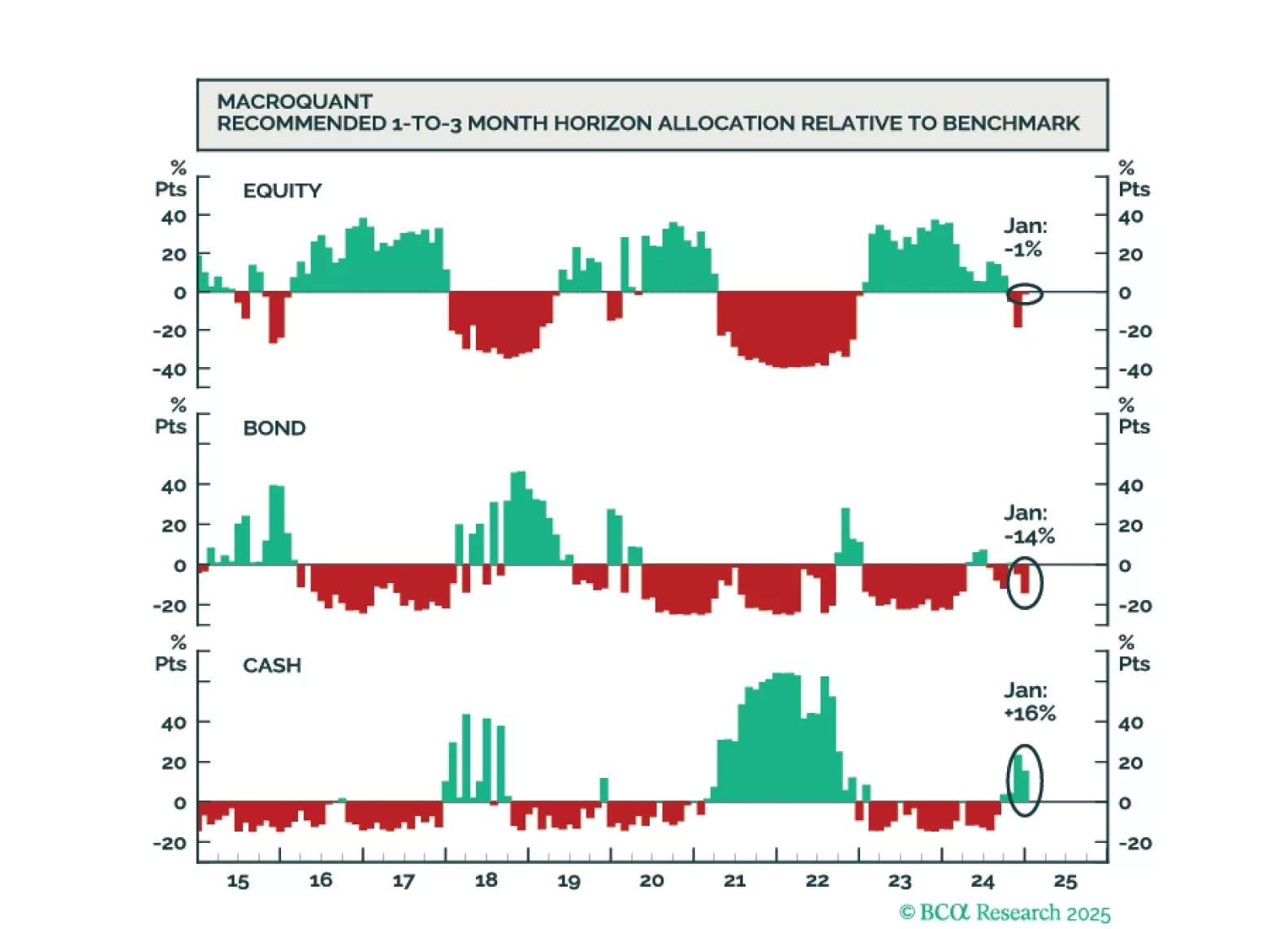

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

While the US economy could remain upright on the tightrope for a while longer, it will inevitably fall, leading to a major bear market in stocks. We will be looking to our MacroQuant model for guidance on when to turn fully defensive. We are not there yet.

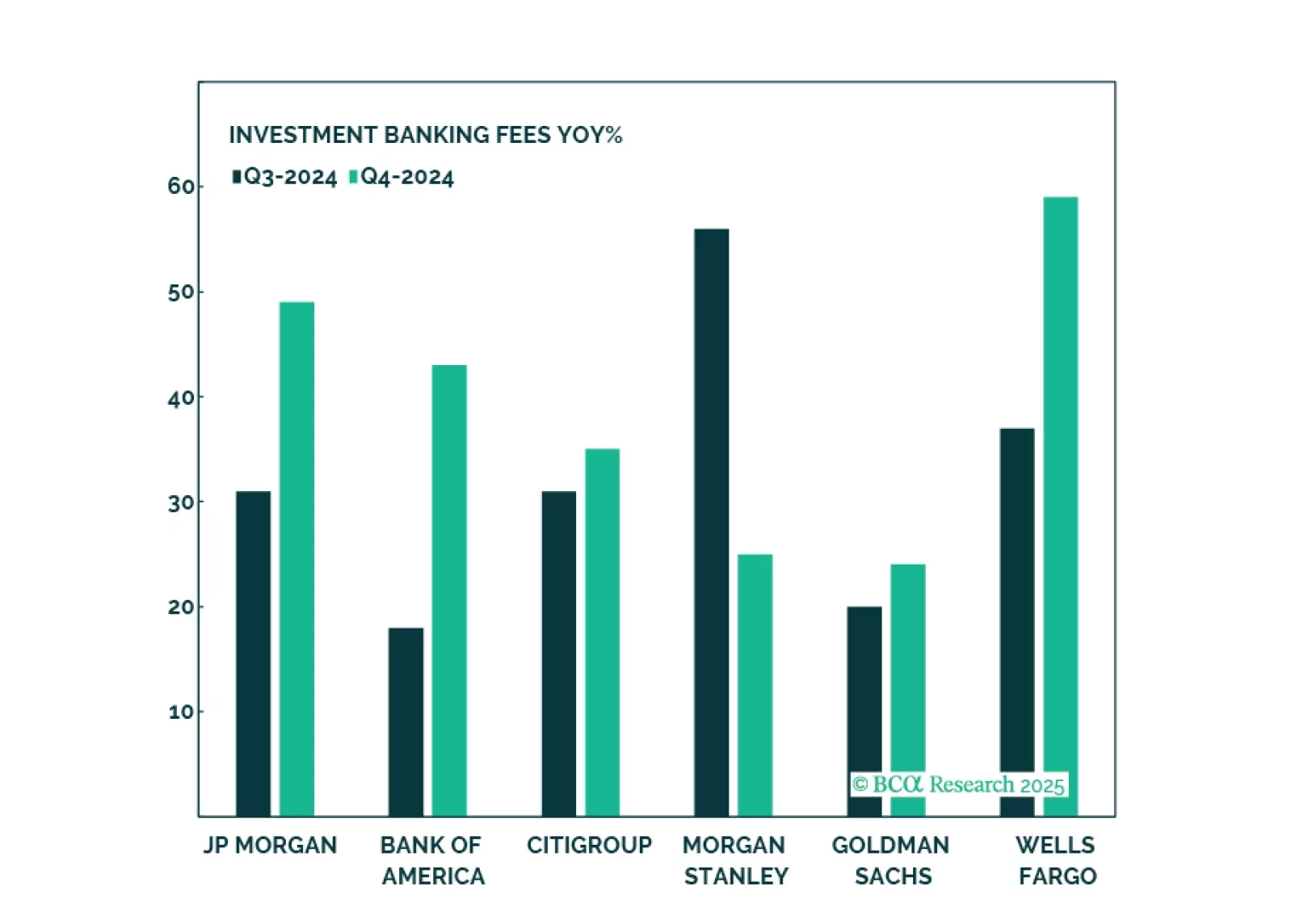

Banks have had an amazing run, and while such strong performance is unlikely to repeat, there is still oomph left in the trade thanks to a more favorable regulatory environment, stronger demand for loans, a steeper yield curve, and a strong pipeline of capital market activity. Key risks are further tightening of monetary policy and an increase in bad loans. We reiterate our overweight on Capital Markets, Diversified Banks, and Regional Banks.

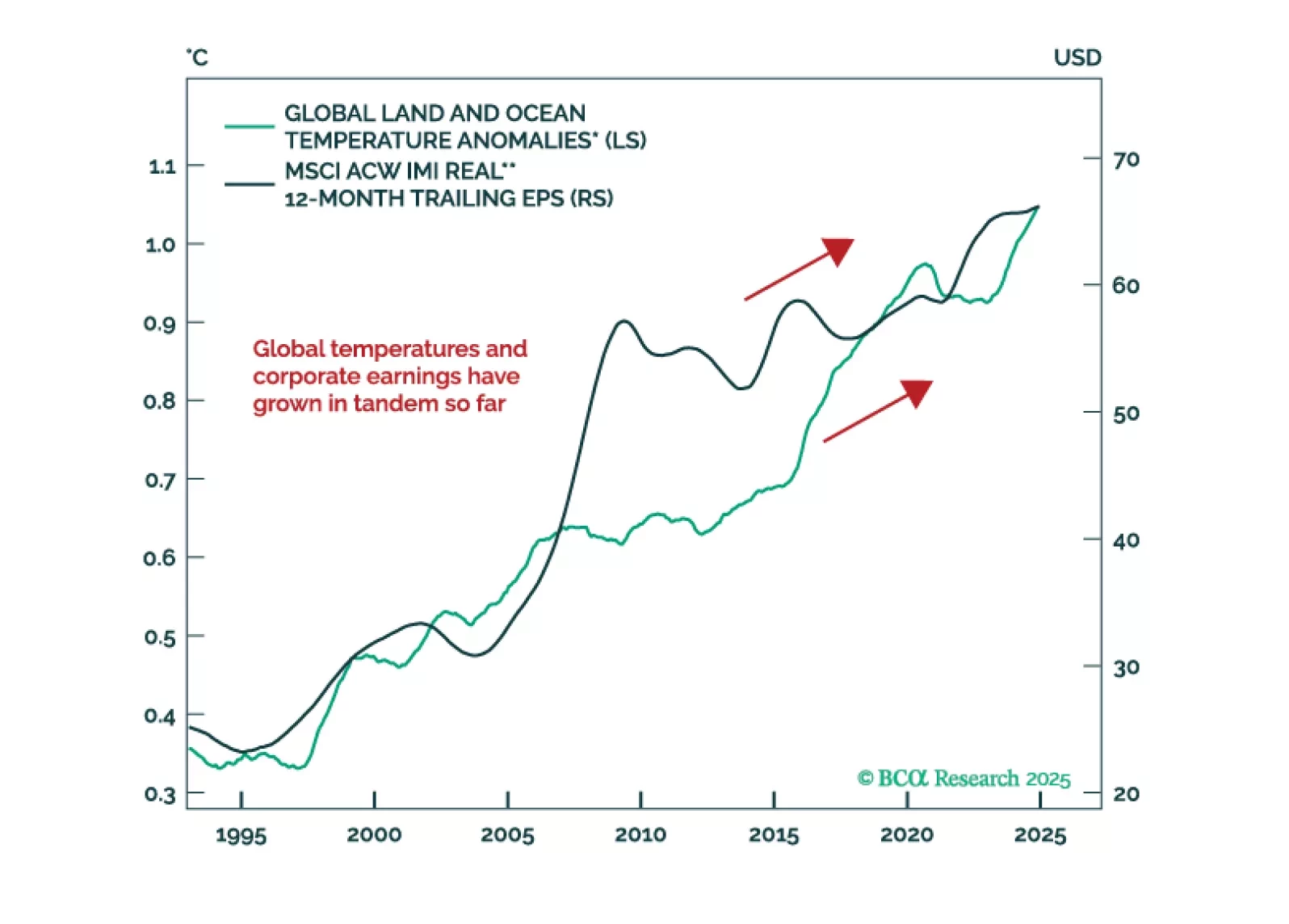

In our Beta report, we take a break from US politics and focus on the investment implications of climate change. Our colleague Ritika Mankar, of BCA’s Global Investment Strategy, makes a case for long-term investors to actually completely ignore climate change in their strategic asset allocation. Global warming will simply not make any difference, macroeconomically speaking, over the next five to ten years. Over a longer time horizon, climate change may even spur more economic growth, although with higher inflation as well.

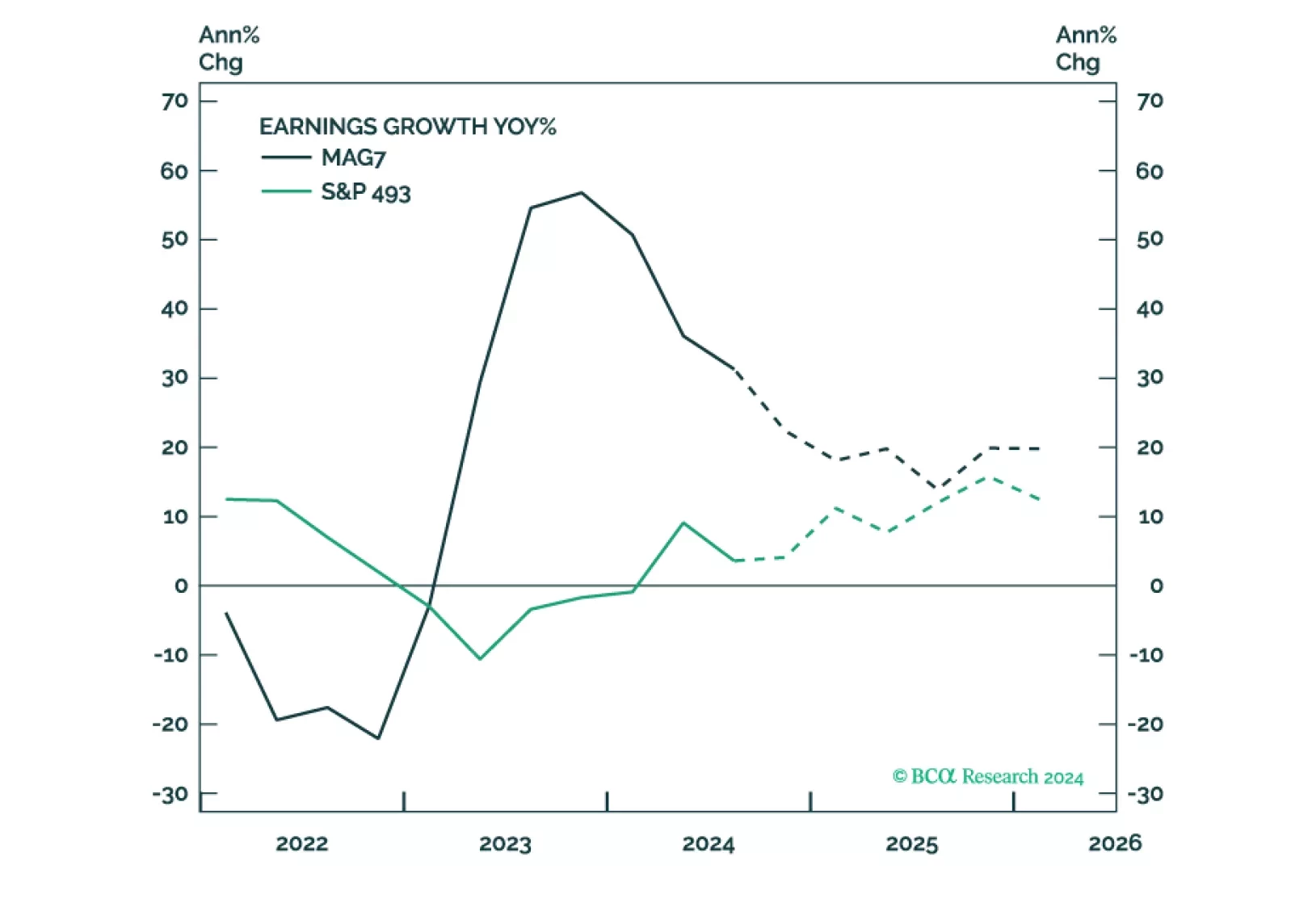

Trump's policies aim to support domestic producers and will be pro-growth and inflationary, at least initially. This environment is supportive of equities. Earnings will likely be strong, but elevated valuations make equities prone to a correction. Earnings growth broadening will translate into performance broadening – the S&P 493, Cyclicals, Value, Small and Mid are likely to outperform.

The prospect of a new trade war more than offsets the other pro-business parts of Trump’s agenda. With the labor market already weakening going into the election, we are raising our 12-month US recession probability from 65% to 75%.