Asia

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

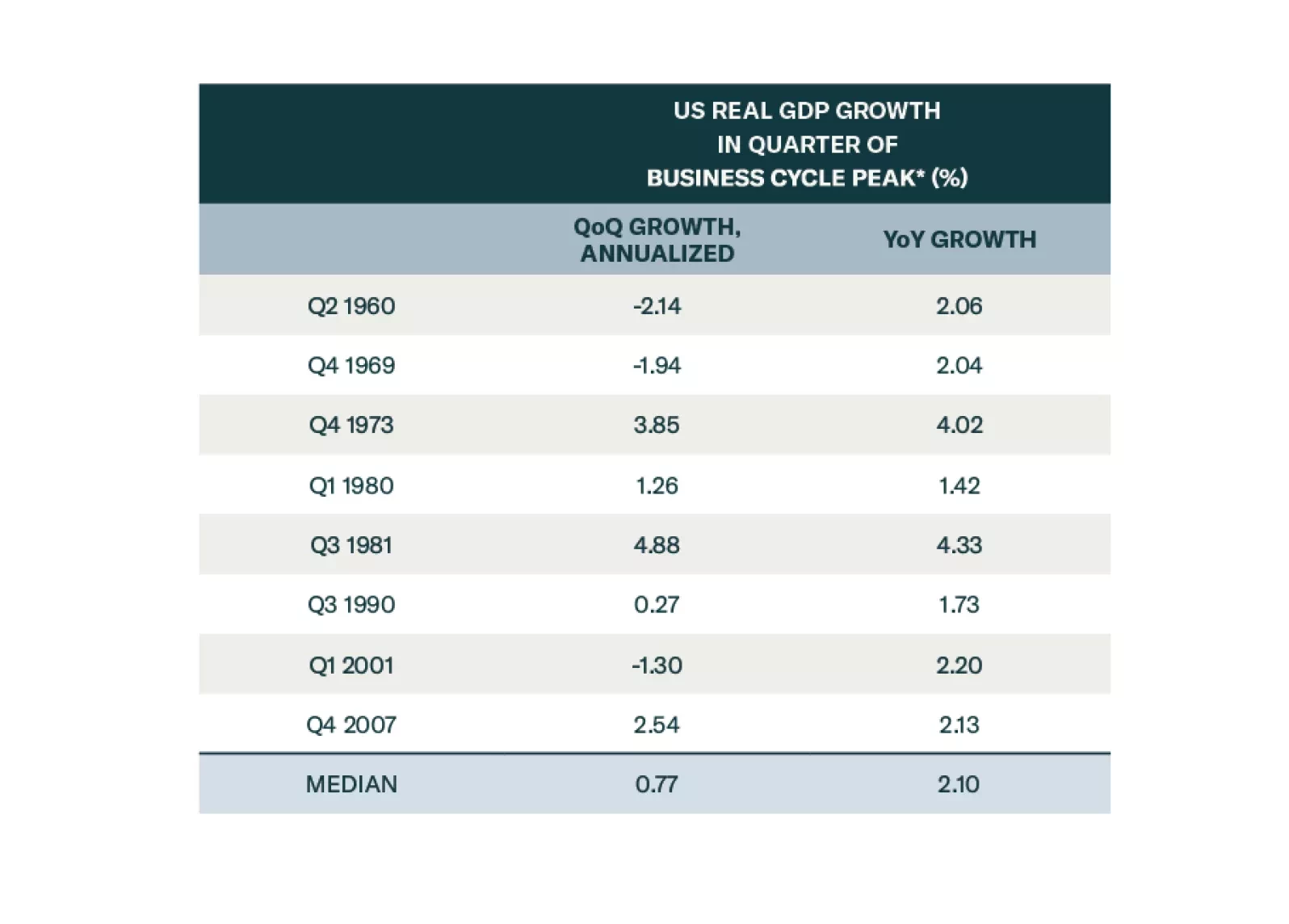

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

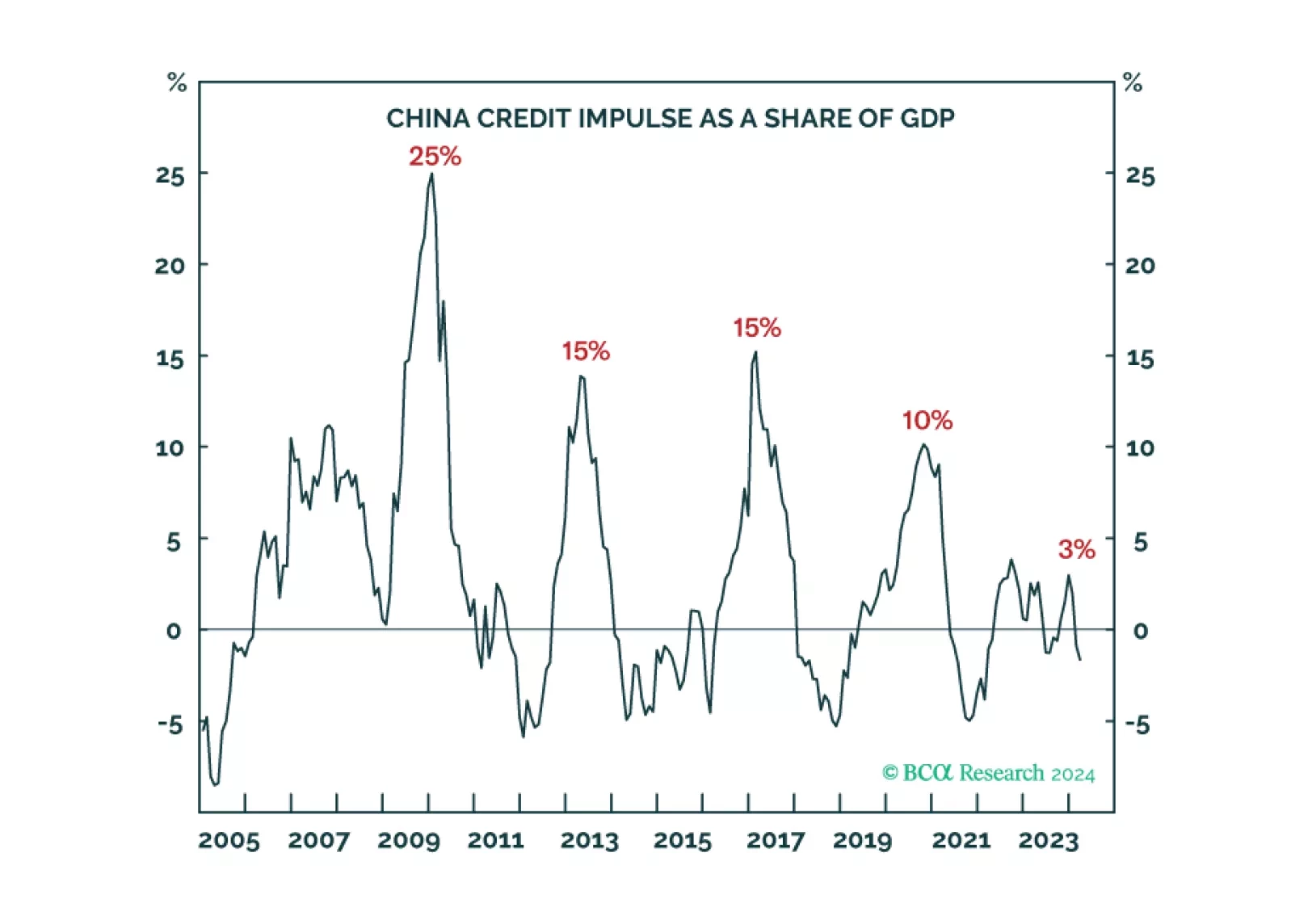

The end of China’s exponential credit growth will impede structural rallies in Chinese stocks and commodities, but US superstar stocks’ bubble-like valuations will impede them too. Leaving European stocks as the likely structural outperformer. Plus: copper is correcting, NVDA is consolidating.

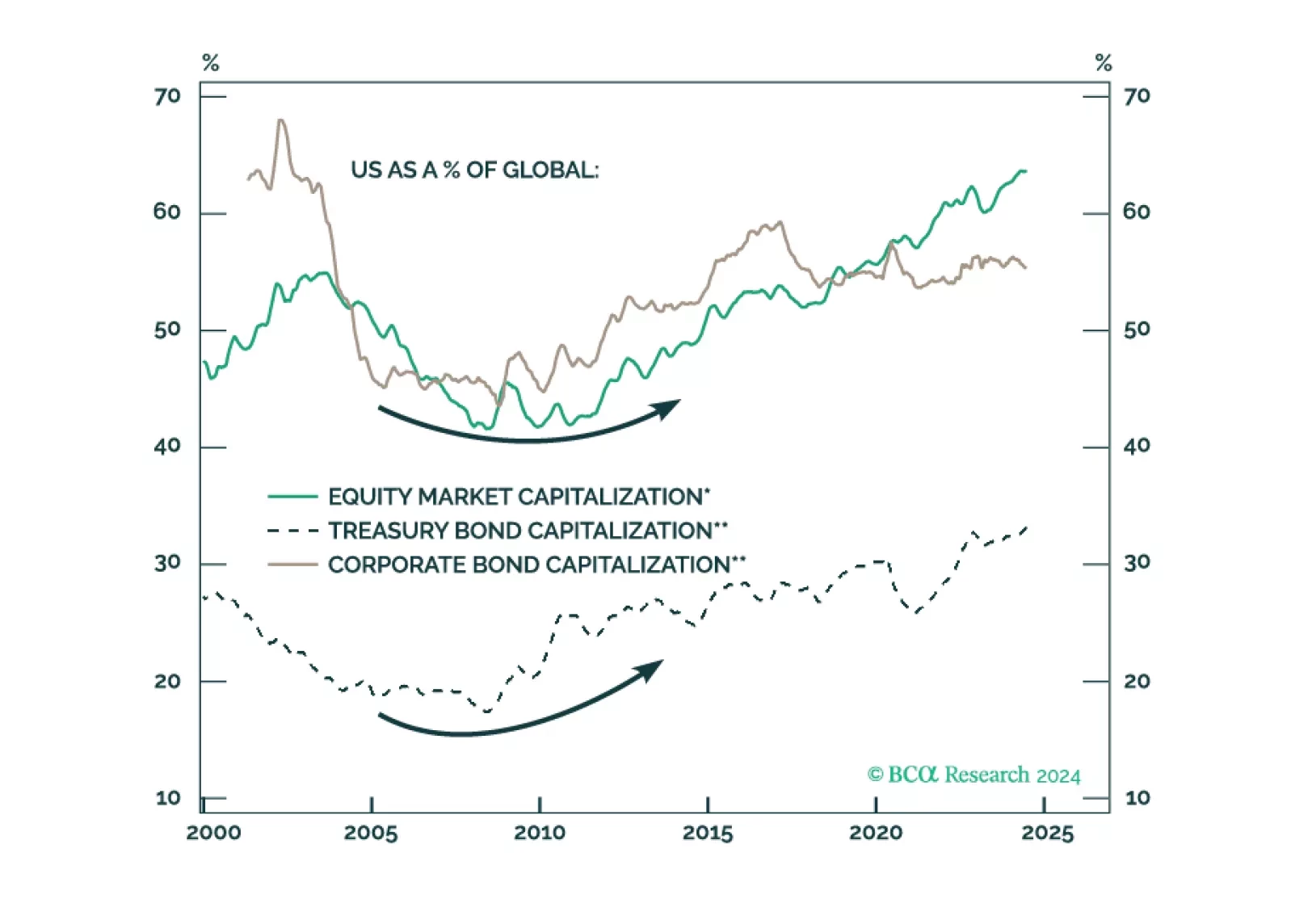

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

The EU's import tariff increases on Chinese EVs are expected to have a minimal impact on China's overall exports. We anticipate that most Western-brand EV shipments from China will be less affected by the EU import tax hike. Beijing will likely pursue continued negotiations with the EU rather than resort to harsh retaliatory measures.