Alternative Investments

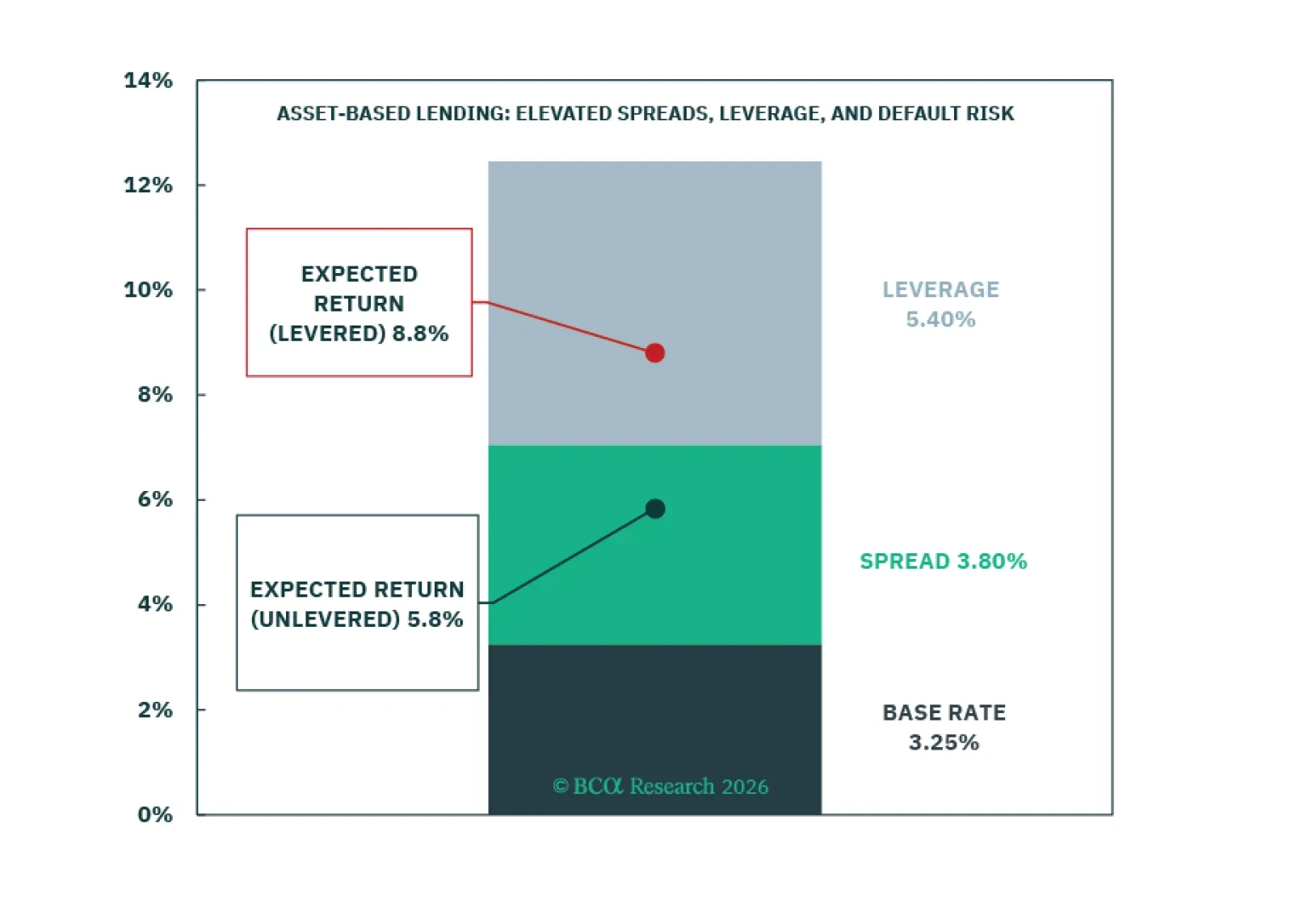

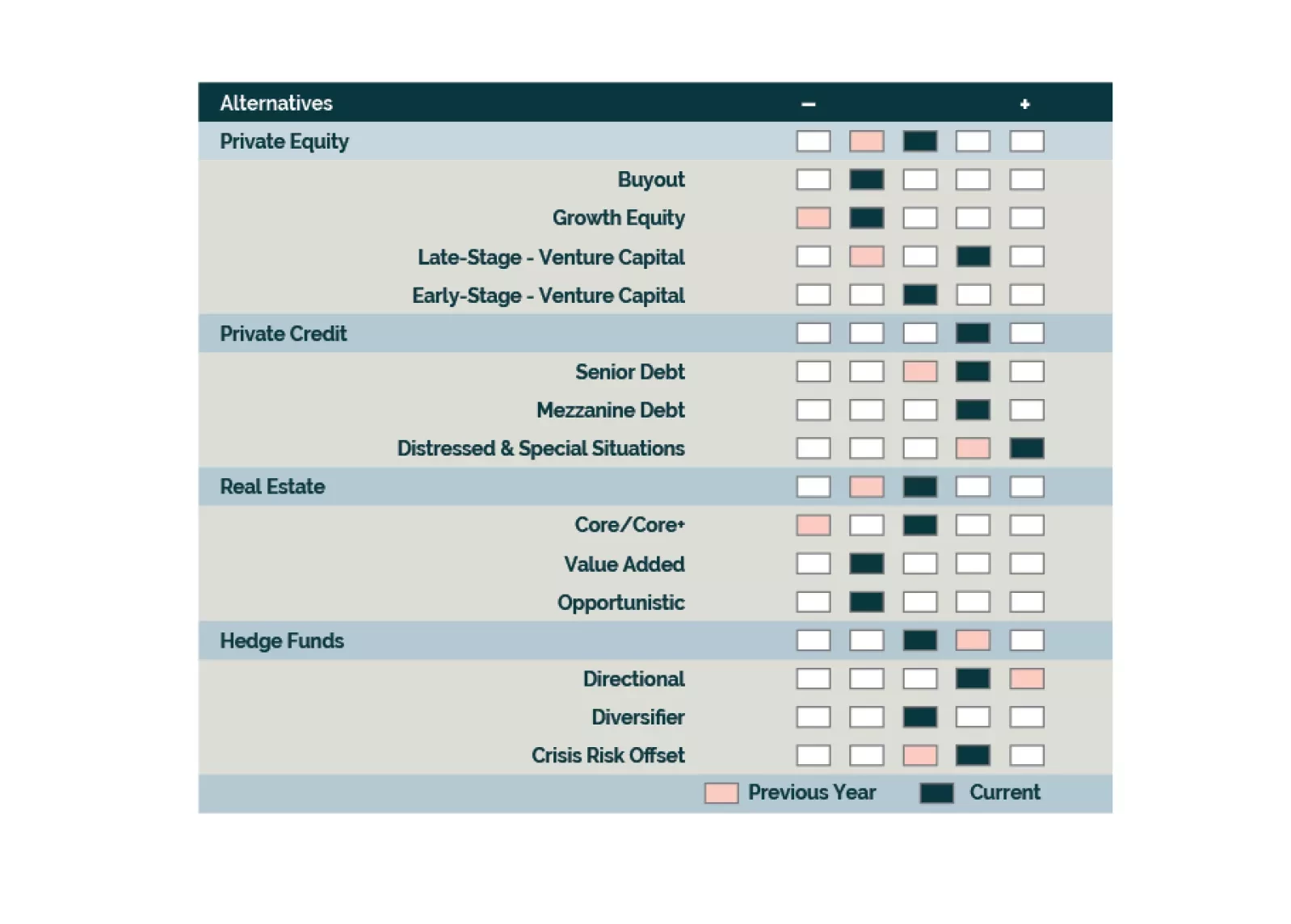

Our new Private Credit taxonomy adds granularity to the opaque lending universe and introduces Asset-Based Lending—attractive entry points, elevated risks. Private Real Estate delivers the largest upgrades from 2025, while Public REITs and Public Infrastructure present compelling opportunities that investors should not overlook.

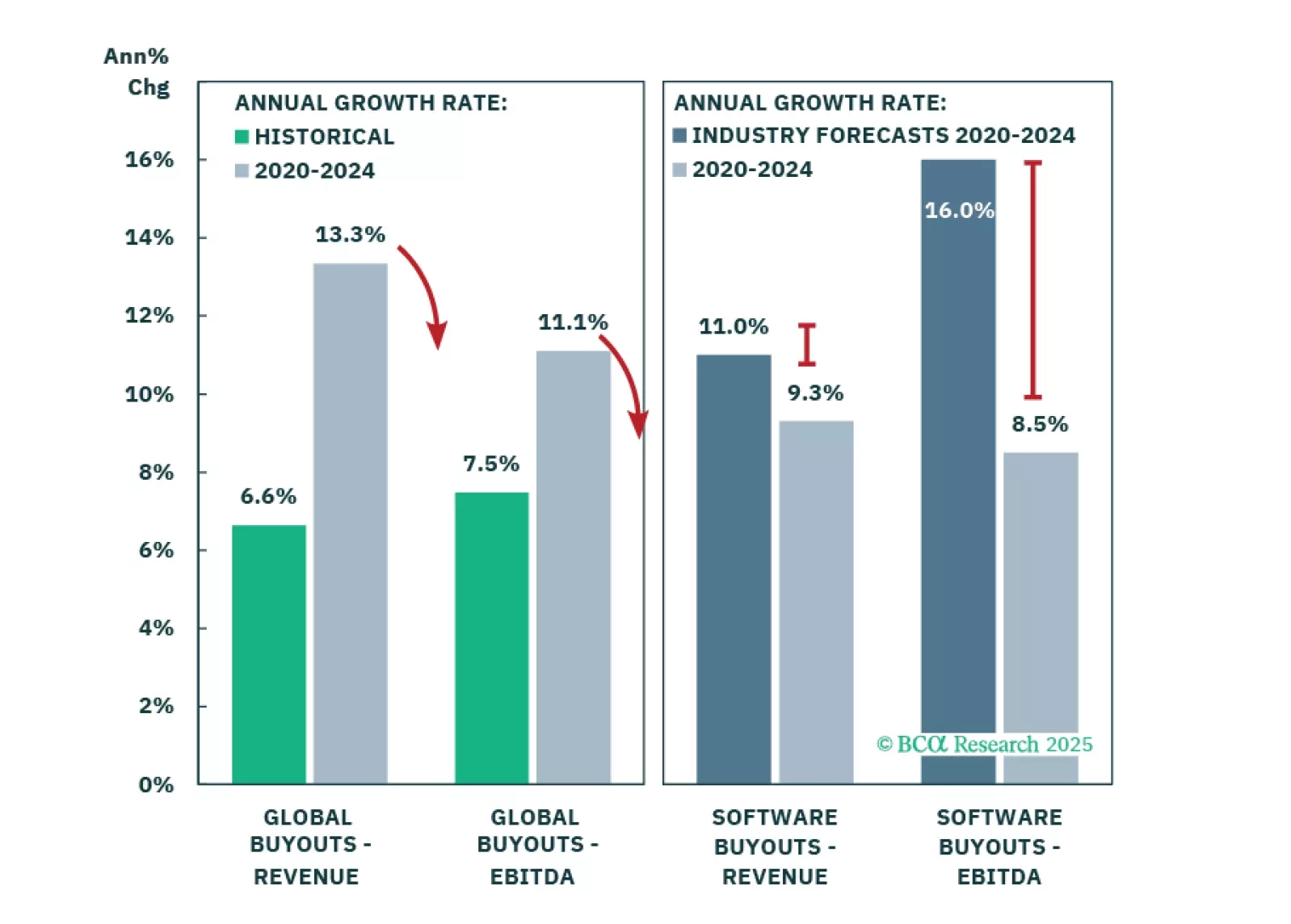

Tariffs may trigger the recession, but the economy was already vulnerable from unsustainable growth and inflated expectations. Private Equity is most exposed, though this situation neither emerged suddenly nor will it unfold overnight. Our recommendations remain largely unchanged as market conditions increasingly align with our outlook.

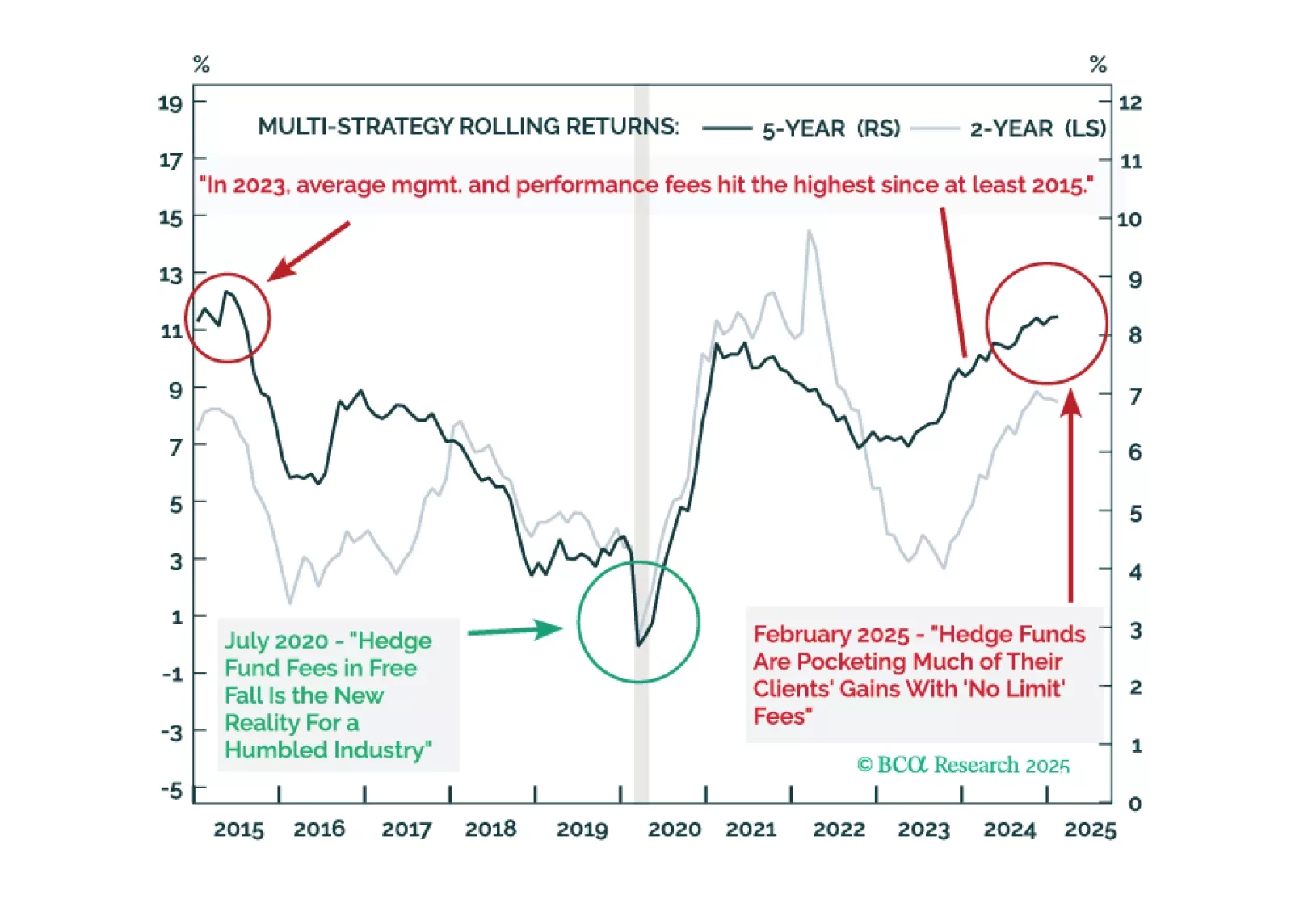

It is easy to hate Multi-Strategy Hedge Funds—they are no underdogs. The truth is they have been cheap, not expensive. Going forward, they come at a higher cost not just in the form of fees. The biggest risk is not to financial markets but to investors. We remain underweight cyclically, long structurally.

Asset class expectations show mixed shifts from 2024, with Real Estate seeing substantial upgrades and Private Equity benefiting from Venture Capital improvements. Private Credit return expectations decline from 2024 but remain relatively attractive. Infrastructure shows varied dynamics across sub-strategies, with Value-Add offering strong return potential. Within Hedge Funds, Long-Short Equity shows higher tactical returns while Multi-Strategy leads strategic projections.

We are growing positive on Growth assets with recession expectations increasing our optimism on entry points. Equities are led by APAC Private Equity, North America Venture Capital, and Europe Buyouts. Our outlook continues to improve on CRE within the Inflation & Diversification bucket while we are underweight Multi-Strategy amongst Hedge Funds. We maintain an overweight to Senior Direct Lending for Income with a preference for North America.

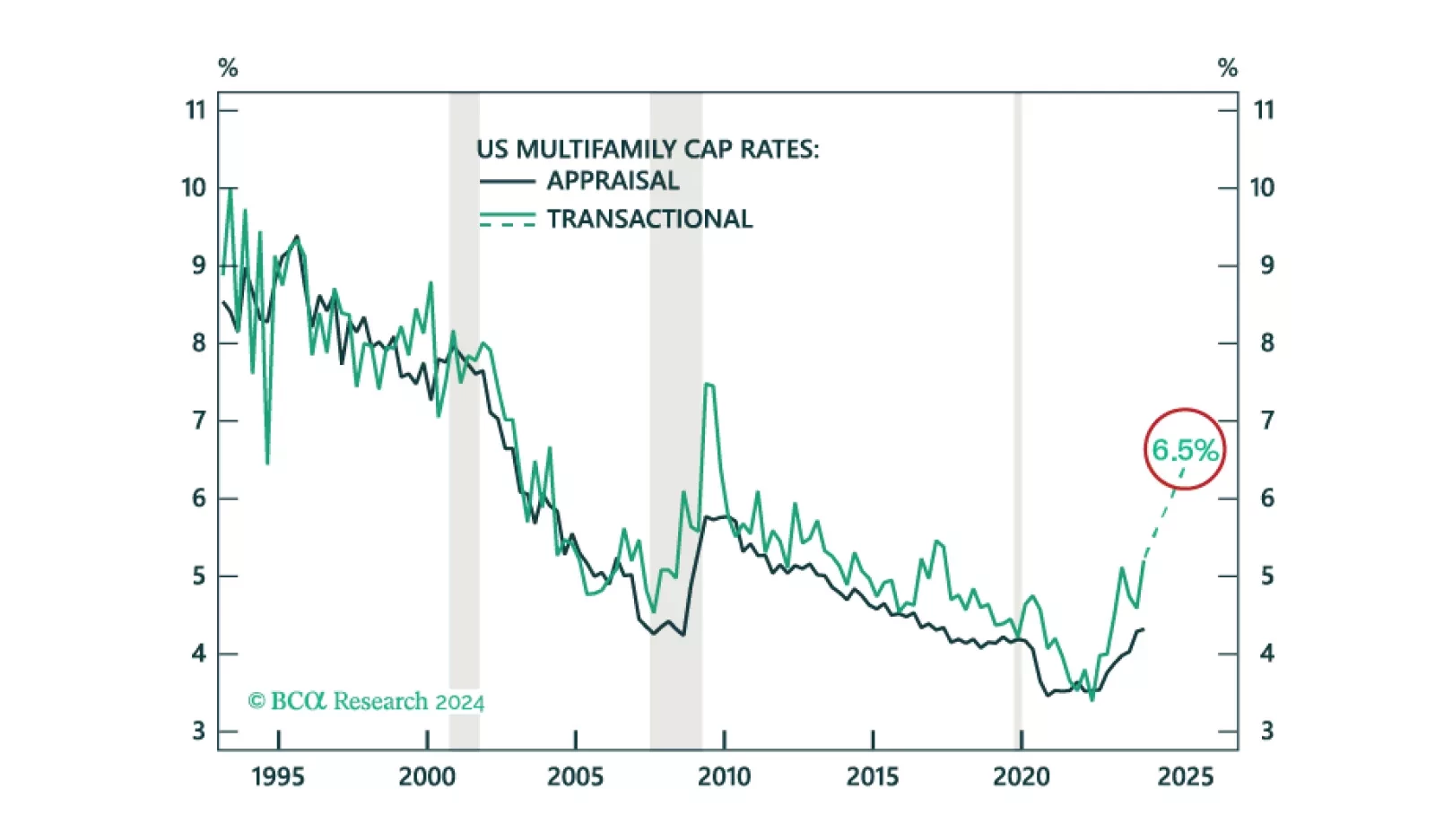

We project US Multifamily cap rates to increase from 5.2% to 6.5%. While we find an unfavorable risk-adjusted return on the asset, especially relative to other opportunities in CRE, cap rates are moving closer to peak.

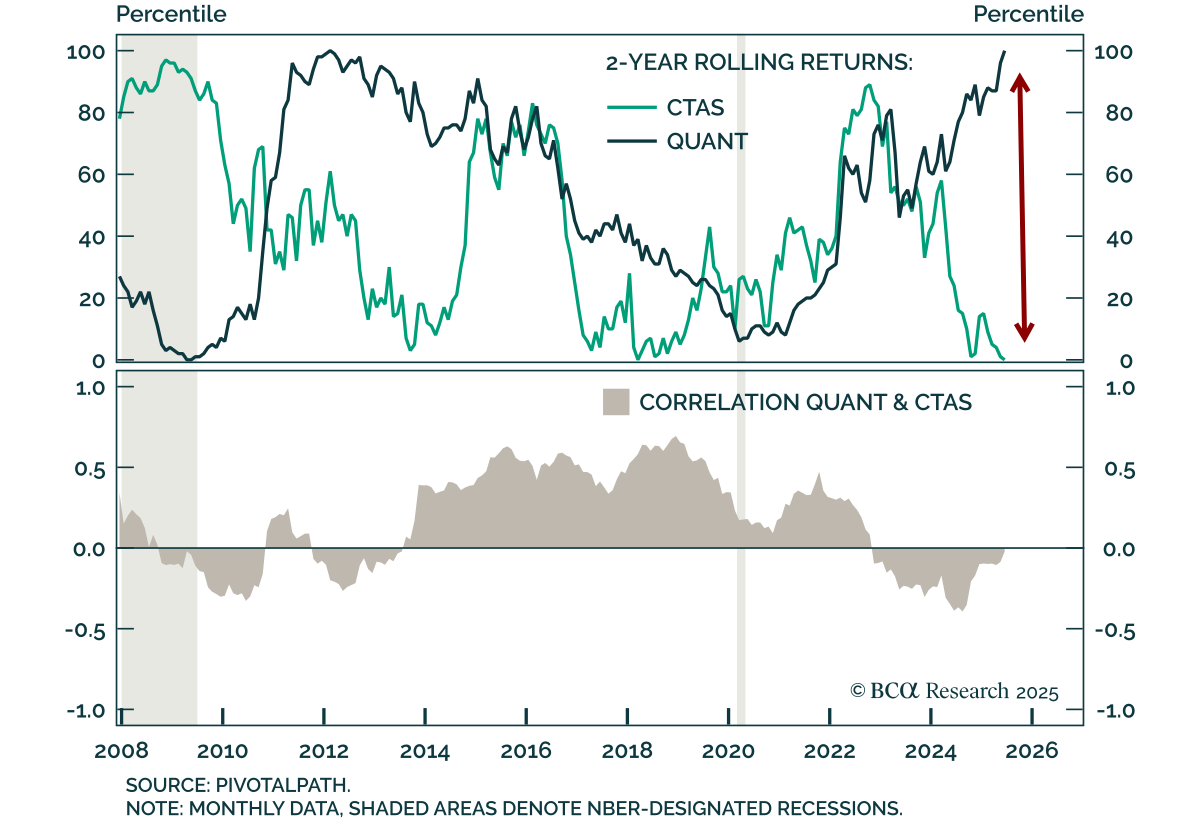

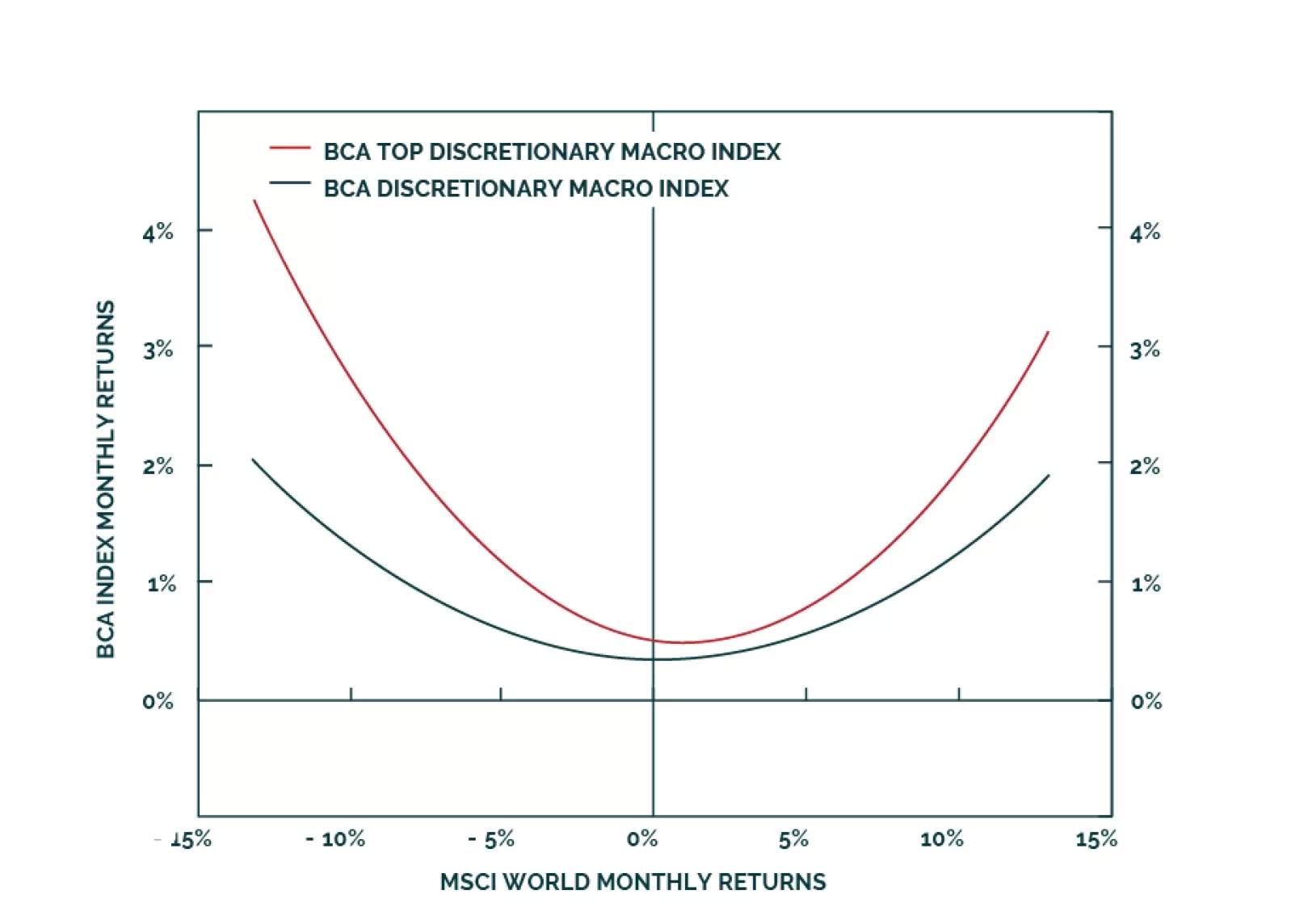

Investors often misjudge Global Macro managers. We outline key manager evaluation criteria and highlight the power of combining Macro Hedge Funds and Private Equity. Even for those who are not Macro Traders nor invest in Hedge Funds, this report may change the way you assess potential employees, partners, and even yourself—the most critical elements of any investment strategy.

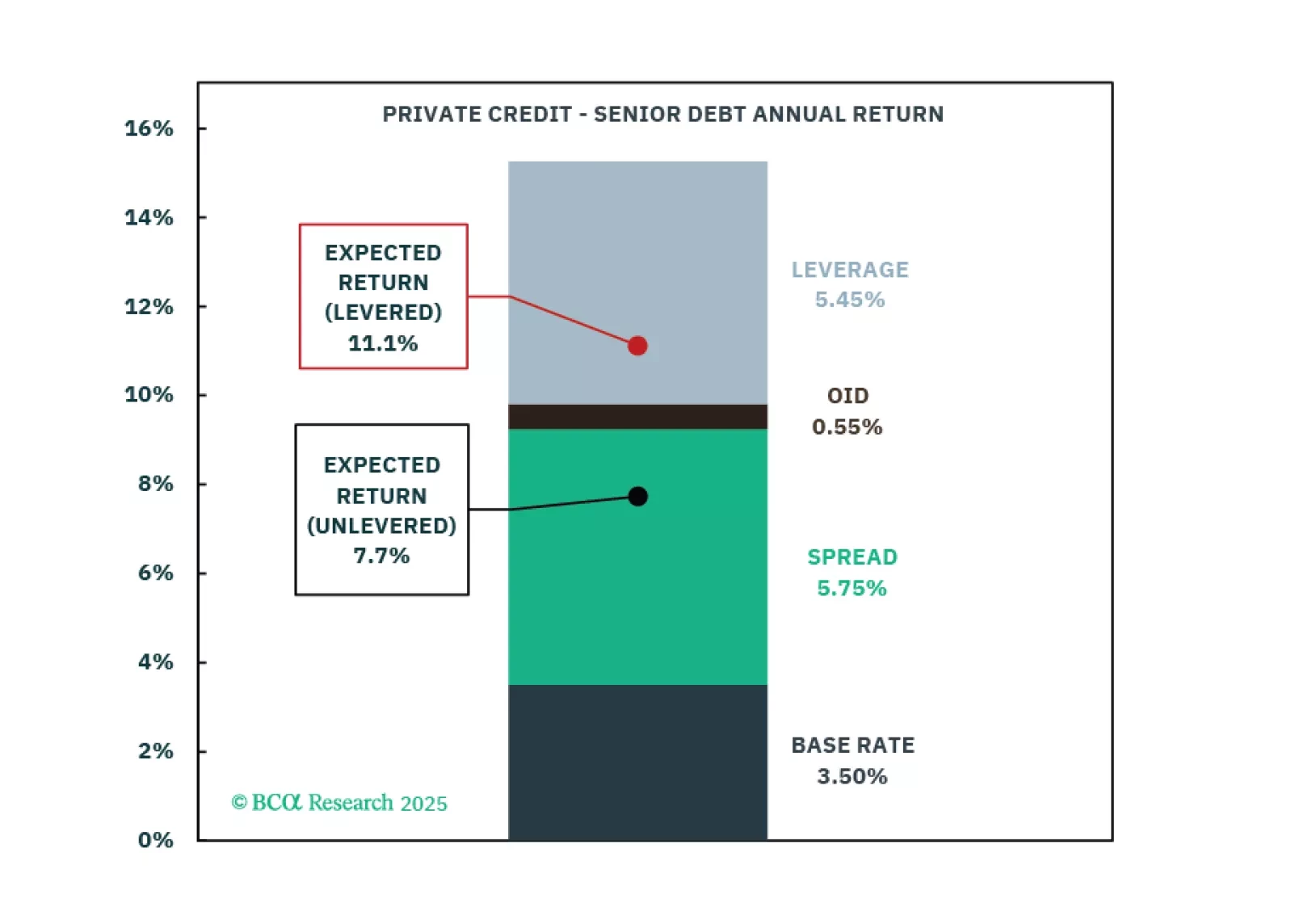

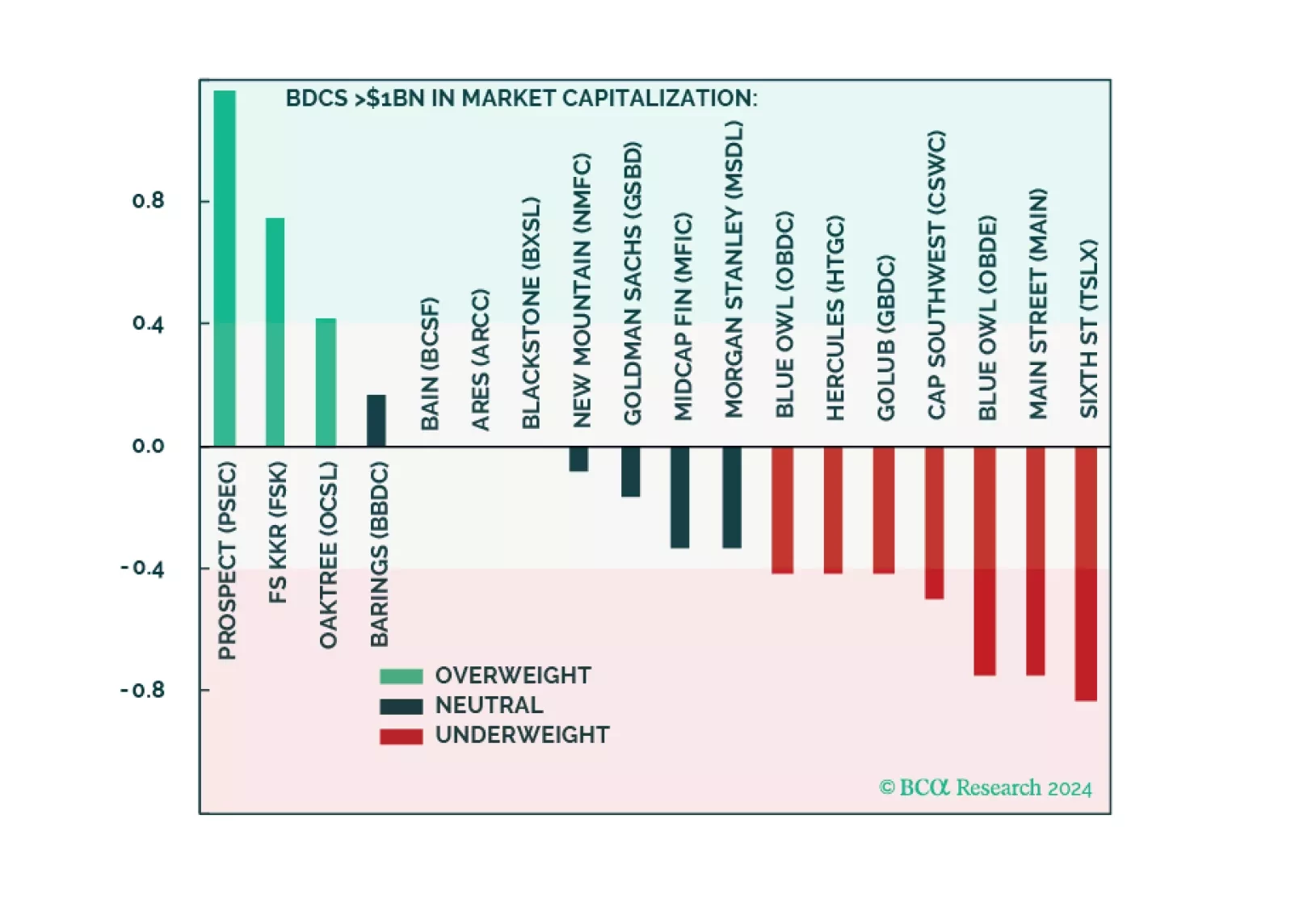

We are positive Private Credit but currently underweight Public BDCs. Today’s market pricing and sentiment in BDCs are excessively optimistic. Long-term investors should await a better entry point. Traders may find an attractive short. This report also peels back the Public BDC onion and presents over/underweights across individual BDCs via our filtering methodology.

Also included at the end of this report is an updated presentation titled 'Private Credit: Drivers Of The Boom And Understanding Risks On The Horizon,' recently presented at GII’s Private Credit Roundtable in Australia. It features updated charts and additional analysis.

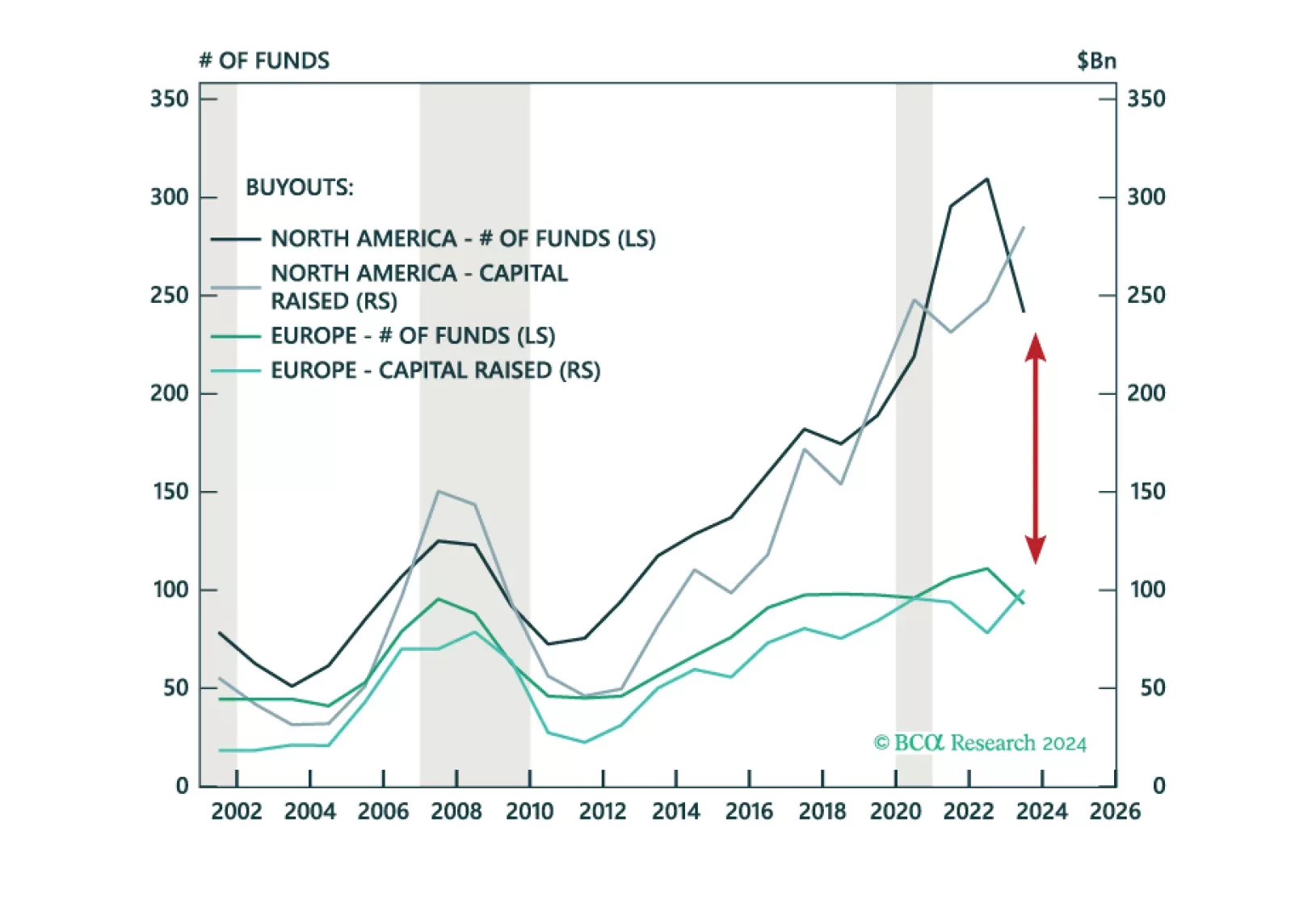

We go overweight Late-Stage Venture Capital and APAC Private Equity but remain underweight North America Buyouts. We maintain our neutral outlook towards Hedge Funds and are positive on Long-Short Equity, Event Driven, and CRO strategies. We are cooling towards Direct Lending strategies as competition and relative opportunities increase. CRE’s downturn continues to unfold; we are starting to be buyers.