United States

Our Portfolio Allocation Summary for March 2025.

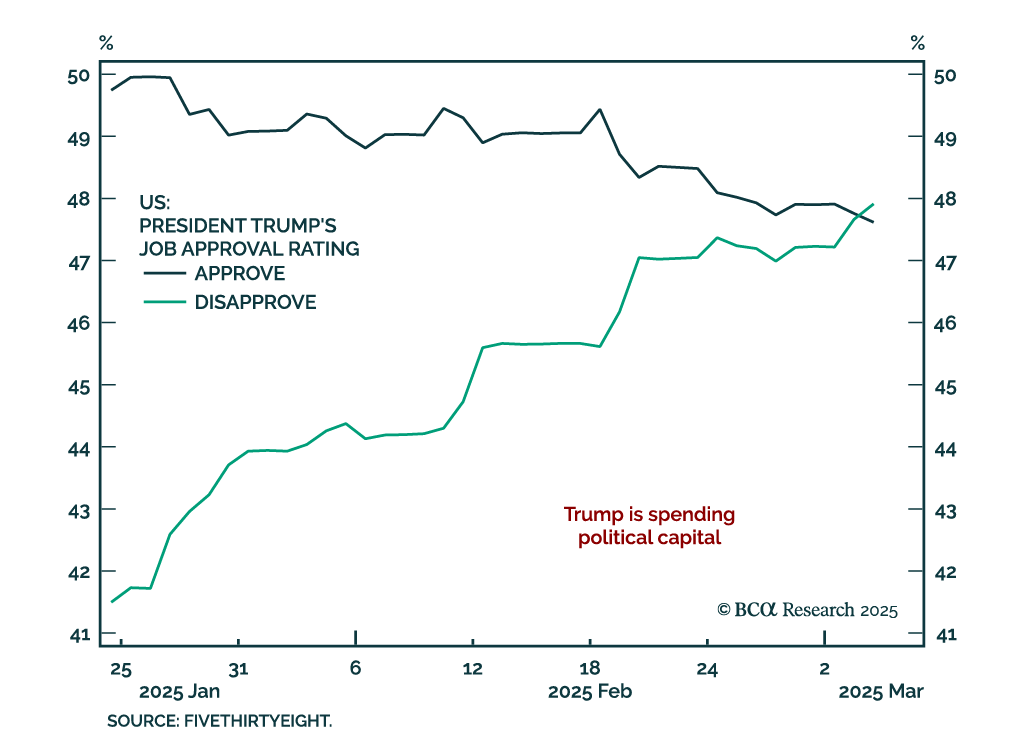

In light of President Trump’s address to Congress and the ebb-and-flow of tariff announcements, our Geopolitical strategists assessed the constraints on the administration’s disruptive agenda. Trump’s ability to implement his agenda is strongest in early…

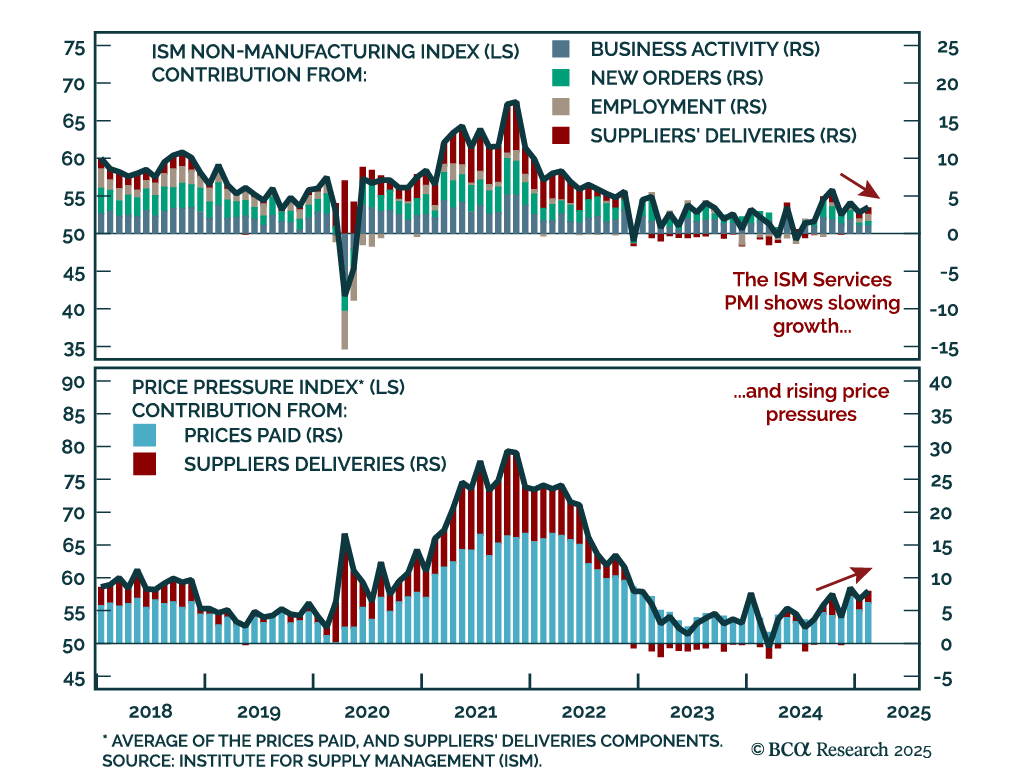

The February ISM Services beat estimates, rebounding to 53.5 from 52.8. All activity subcomponents increased, with new orders and employment ticking up. Price pressures however also increased, as prices paid went up and suppliers’ delivery times…

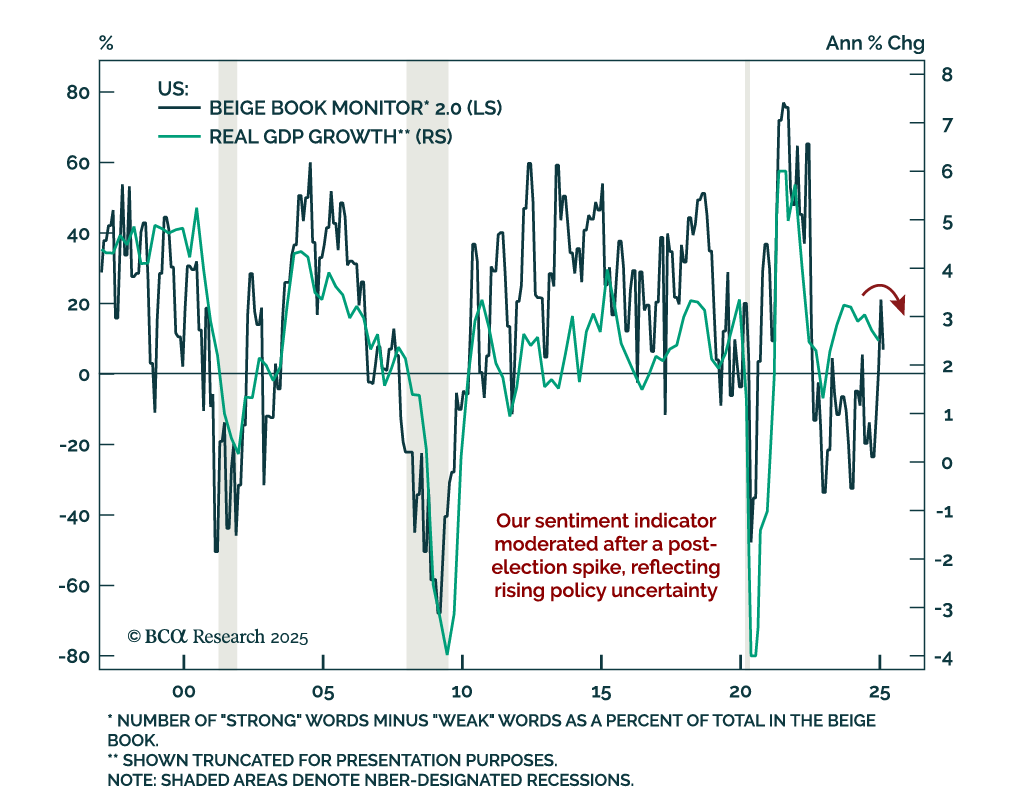

The Federal Reserve’s Beige Book shows a slowing economy, a moderating labor market, and rising price pressures. The latest Beige Book is in line with other sentiment indicators showing slower growth and decreased confidence following the post-election…

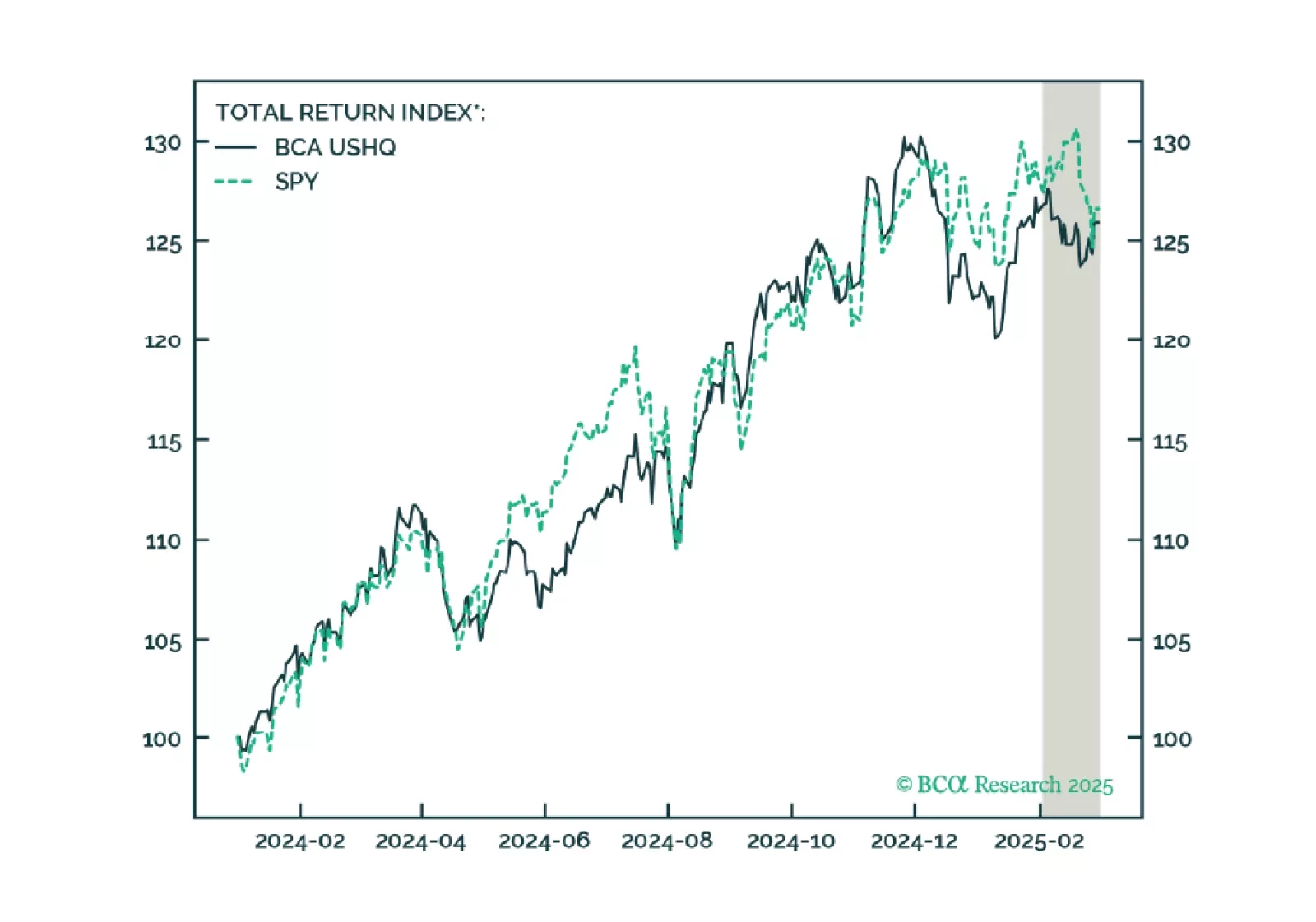

The US High Quality (USHQ) portfolio slightly underperformed in February, returning -0.7%, whilst its SPY benchmark returned -0.6%. While we continue to monitor the portfolio monthly, over a quarter-on-quarter basis, USHQ posted meaningful outperformance vs. benchmark, generating +130bps of excess return, while also exhibiting lower volatility and drawdown.

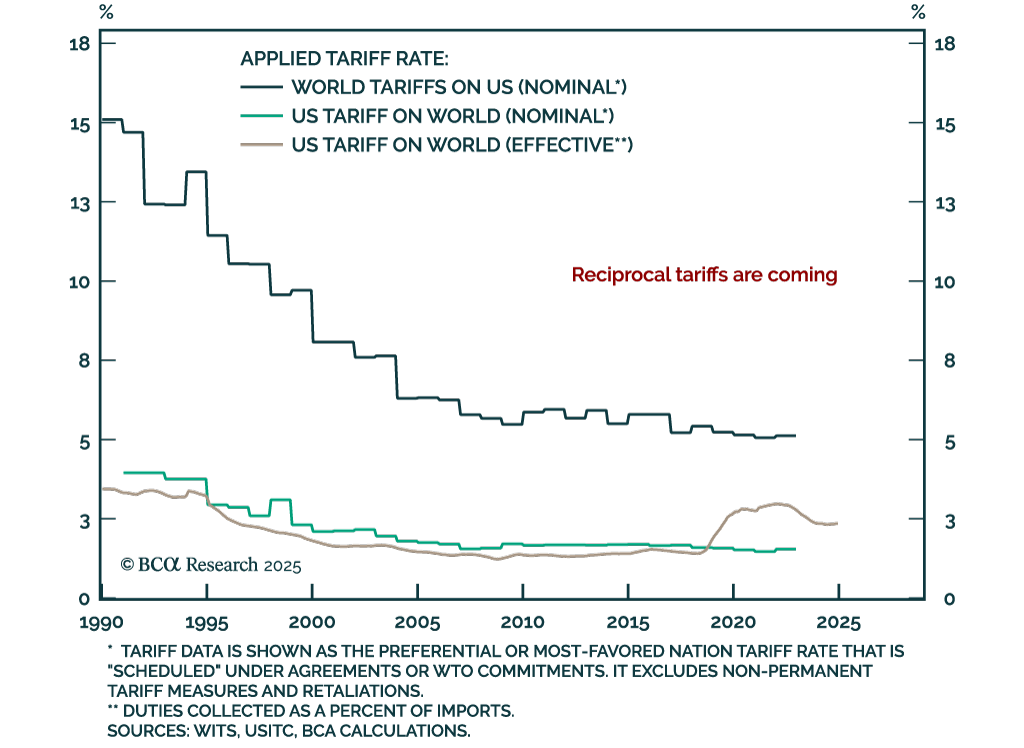

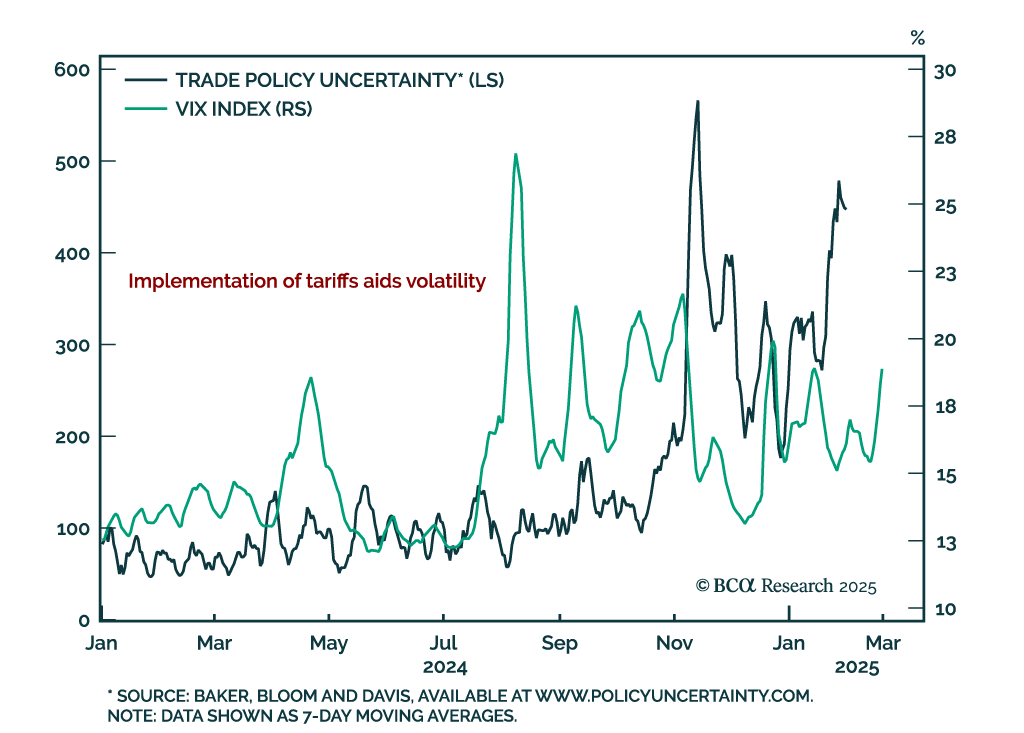

The Trump administration launched its biggest trade action on Tuesday, levying 25% tariffs on Canadian and Mexican goods, and an additional 10% to current tariffs on Chinese imports. Given its crucial role in US supply chains, Canadian energy only sees a 10%…

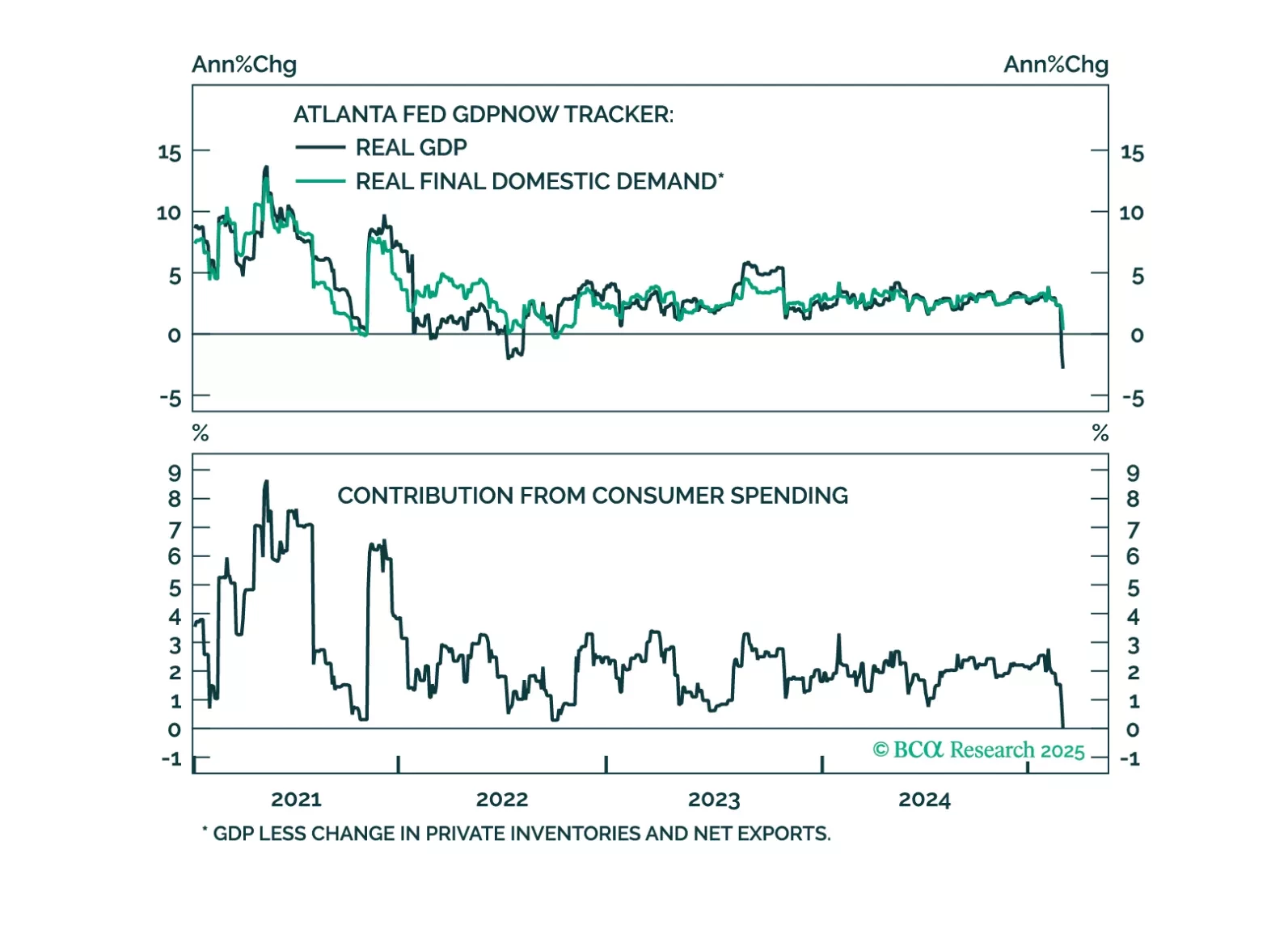

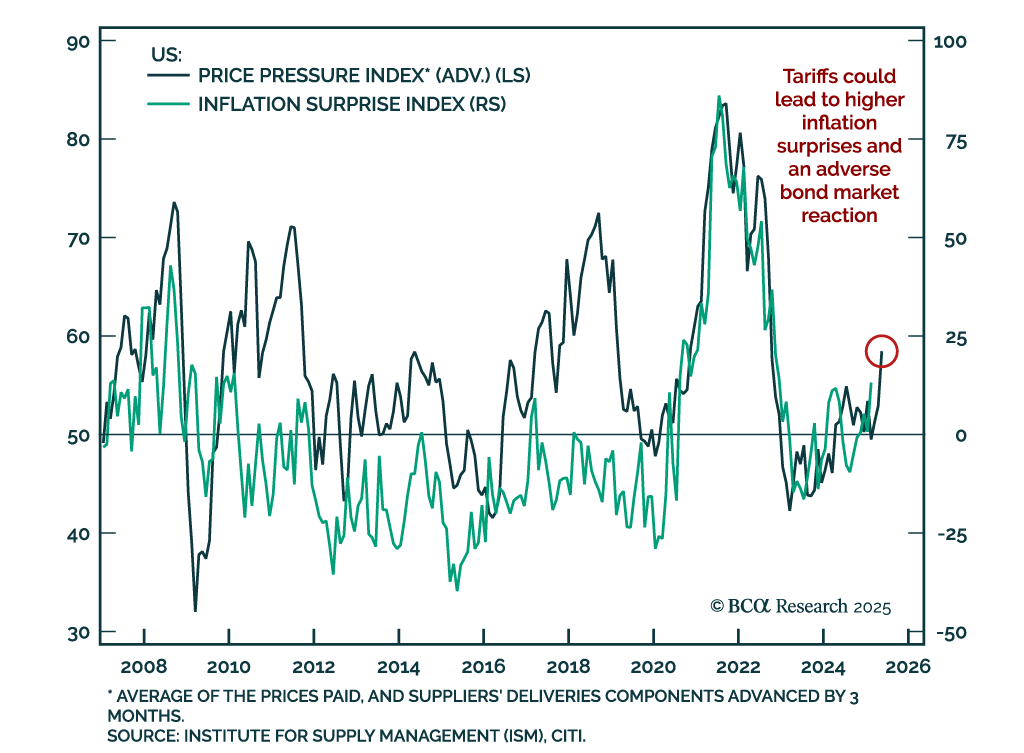

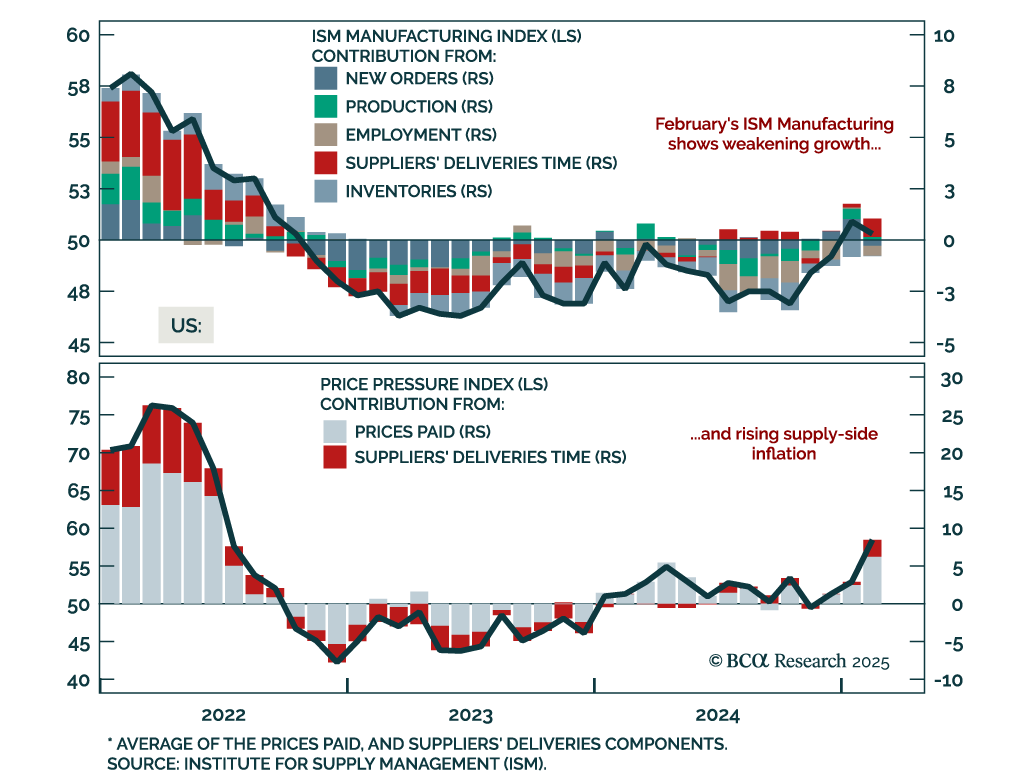

Leading US growth indicators have slowed, with economic surprises now in negative territory. However, Monday’s ISM Manufacturing showed that while activity is slowing due to tariffs uncertainty, supply-side price pressures are increasing. Our Price…

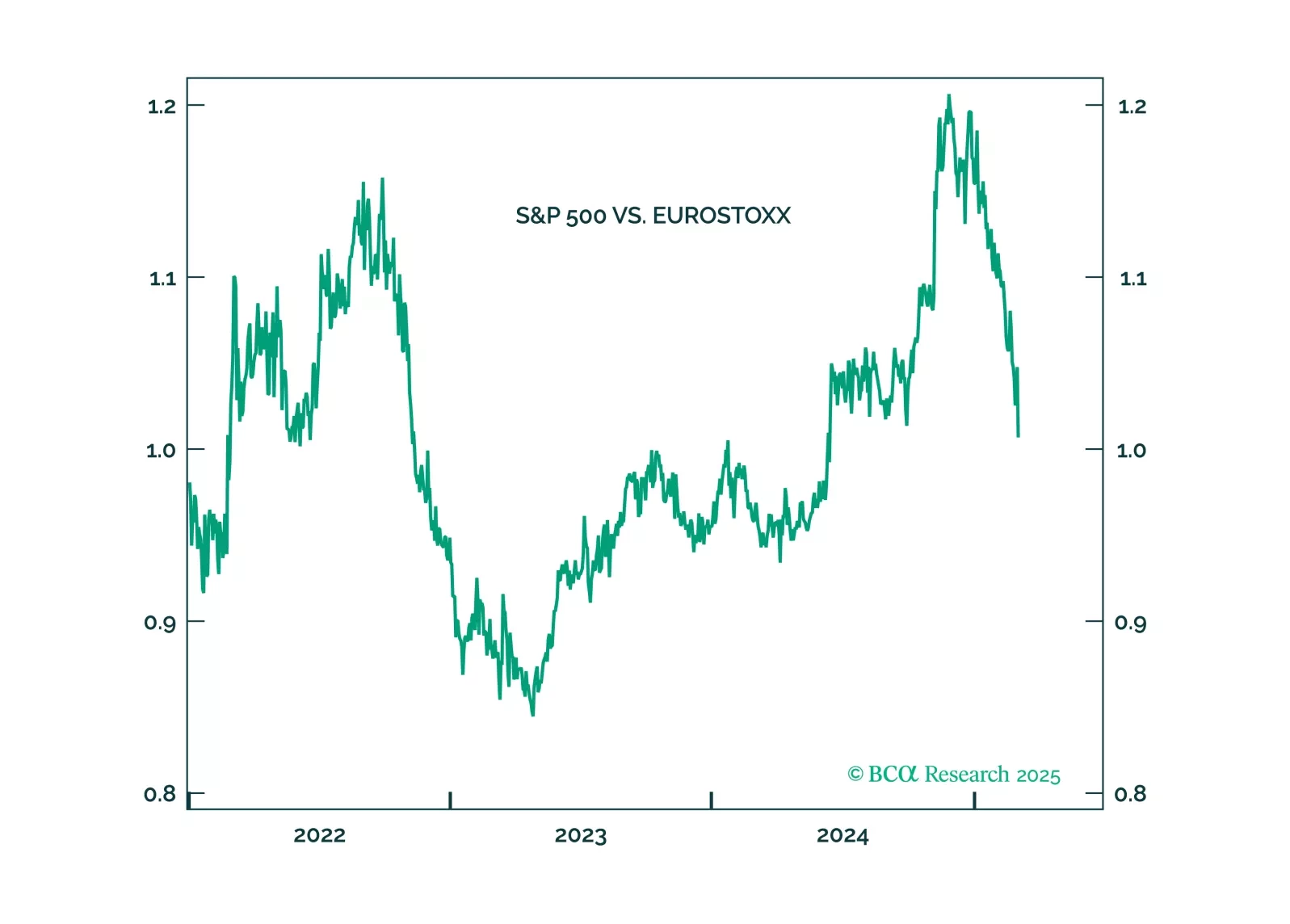

Trump will pull back from the trade war when stocks approach bear market territory. He will not withdraw from NATO. Favor European stocks on fiscal policy.

The February ISM Manufacturing index was weaker than expected, declining to 50.3 from 50.9. New orders plunged to 48.6 from 55.1, with employment also contracting. Price pressures however increased. Prices paid and suppliers’ delivery times jumped to their…

Our Geopolitical strategists received a lot of client questions following rapid US political developments, and addressed them in their latest report. US policy uncertainty is spiking, driving global uncertainty higher. Tariff implementation in March and…