United States

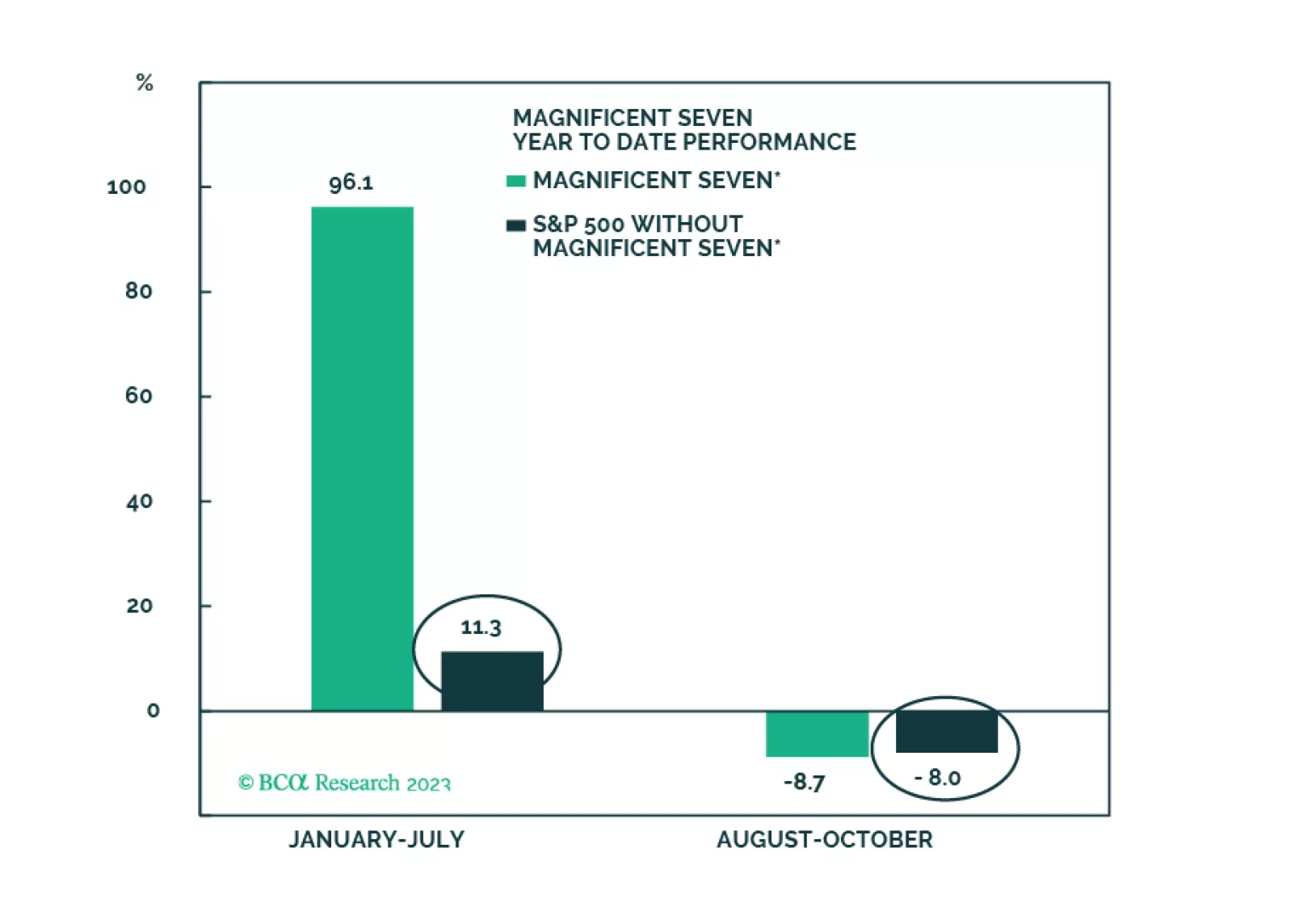

The Vicious Troika remains a long-term threat, but over the short term, rates will likely have another leg down on growth concerns, offering support to equities, which are now fairly valued and are no longer overbought. Longer-term outlook remains negative. The Magnificent Seven will likely lead a tactical rebound. Overweight Growth vs Value and FSemis.

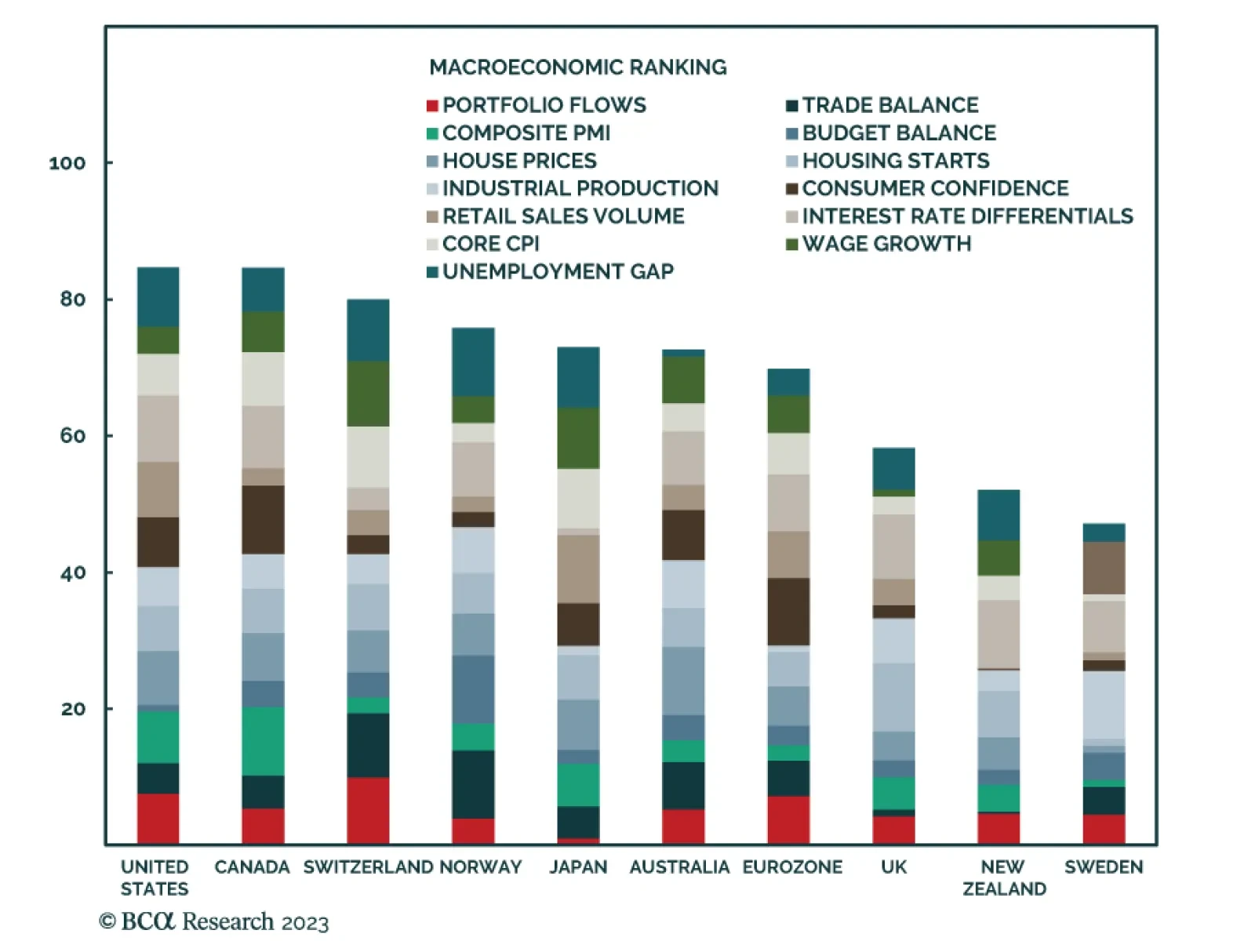

Our Portfolio Allocation Summary for November 2023.

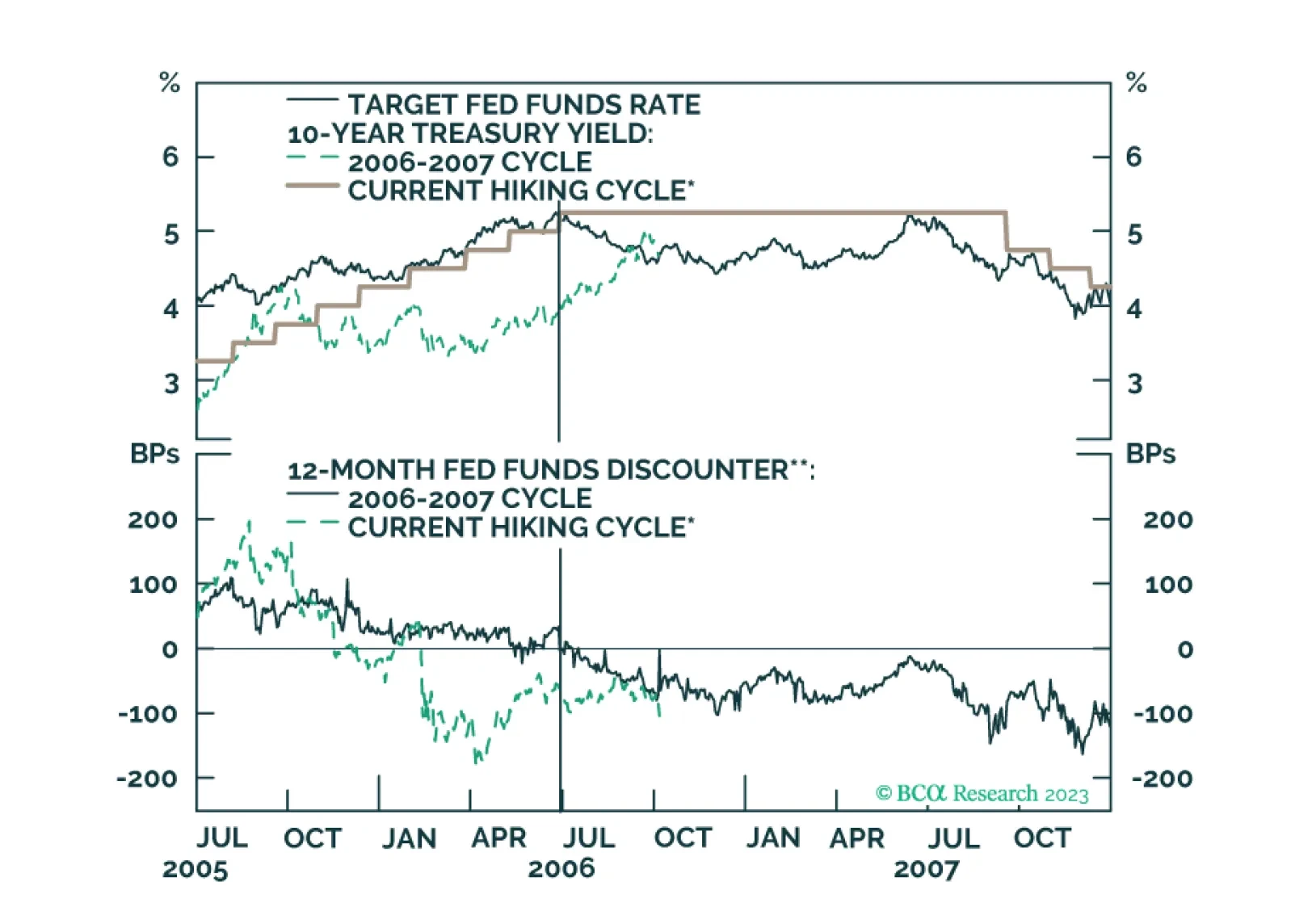

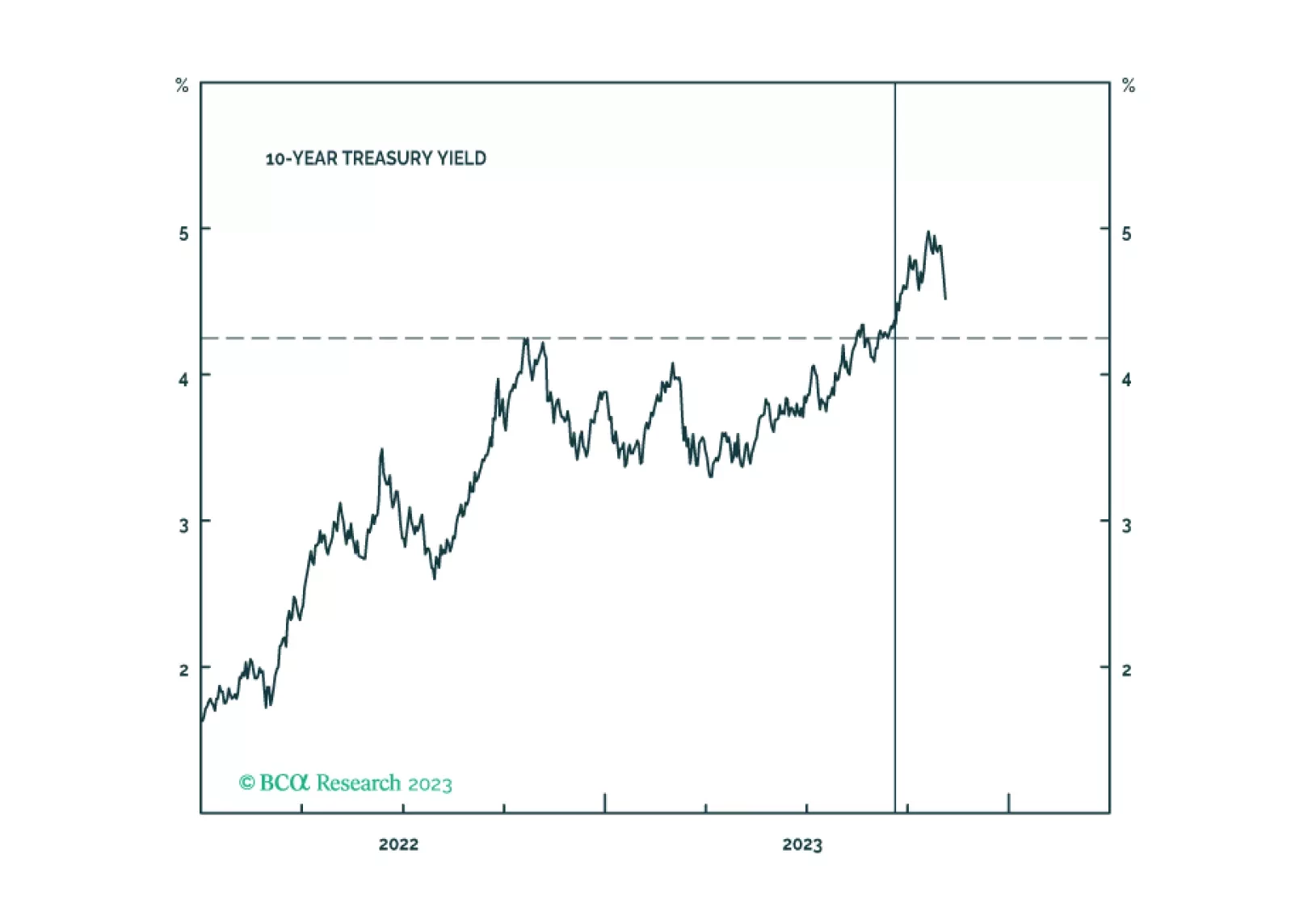

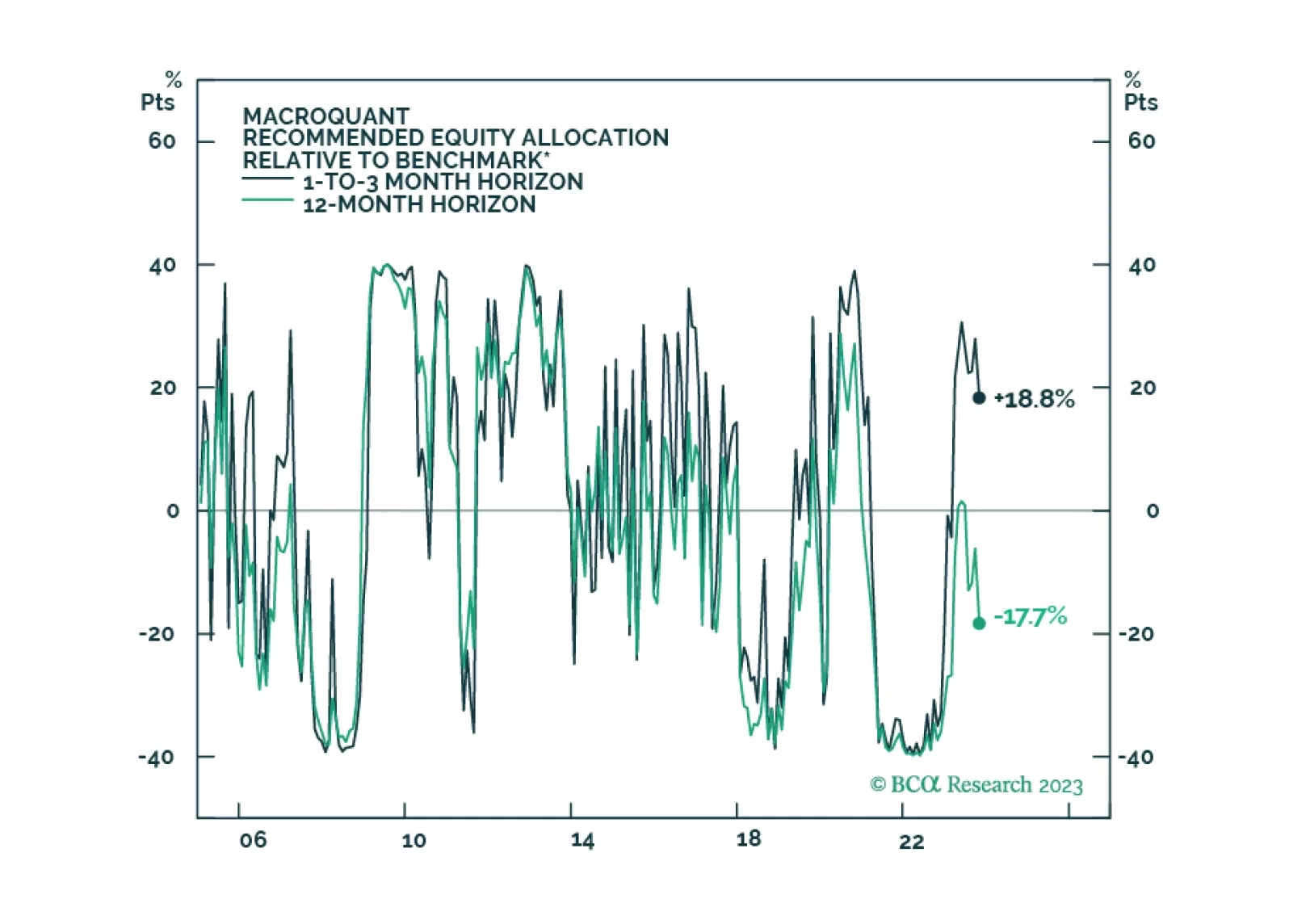

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

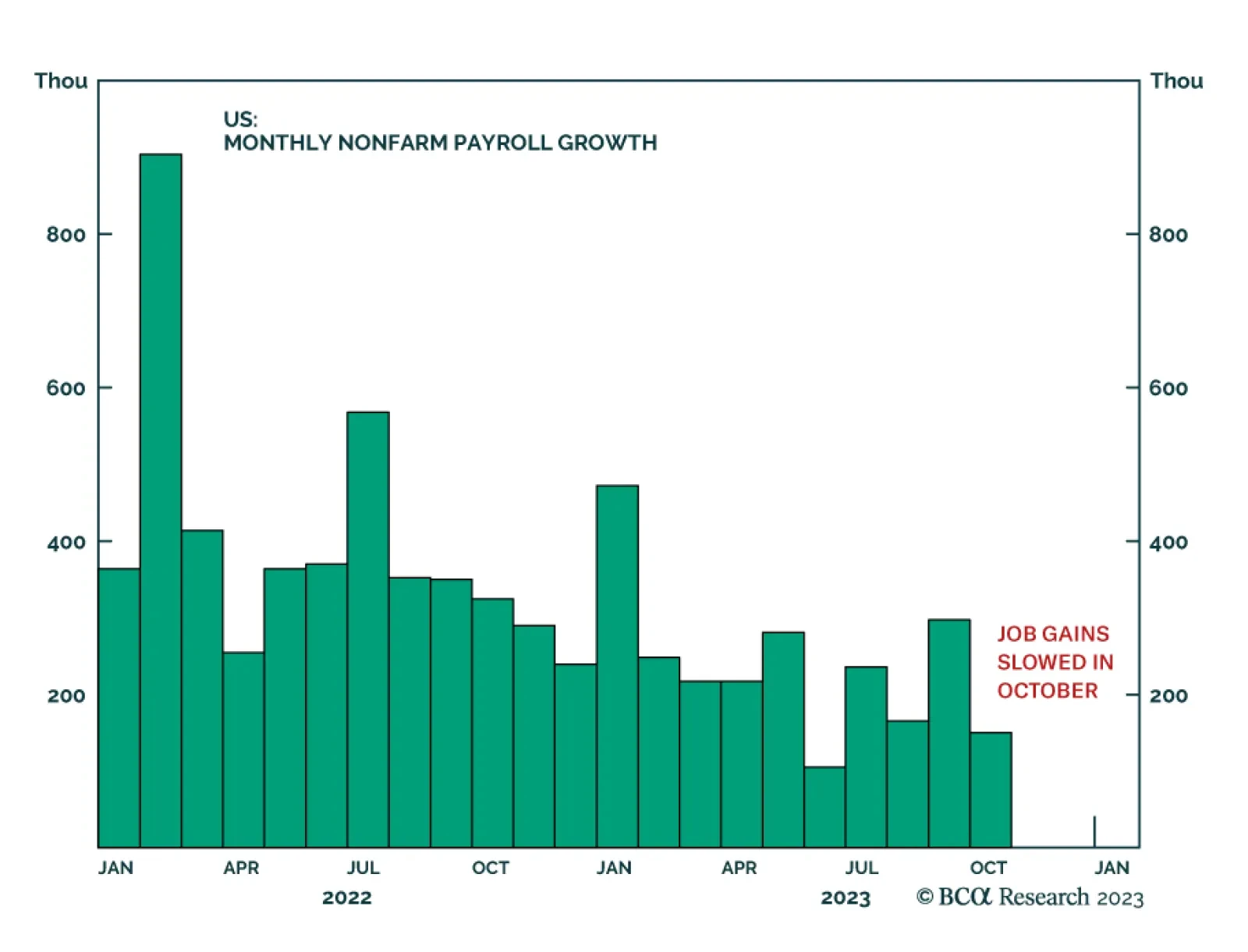

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.