Policy

The next six-to-nine months hold a crucial test of whether the equity market will ratify the soft landing and the Biden administration or not. If so, then markets will rally on policy continuity and likely gridlock. If not, then markets will struggle until the election is over and again in 2025-26.

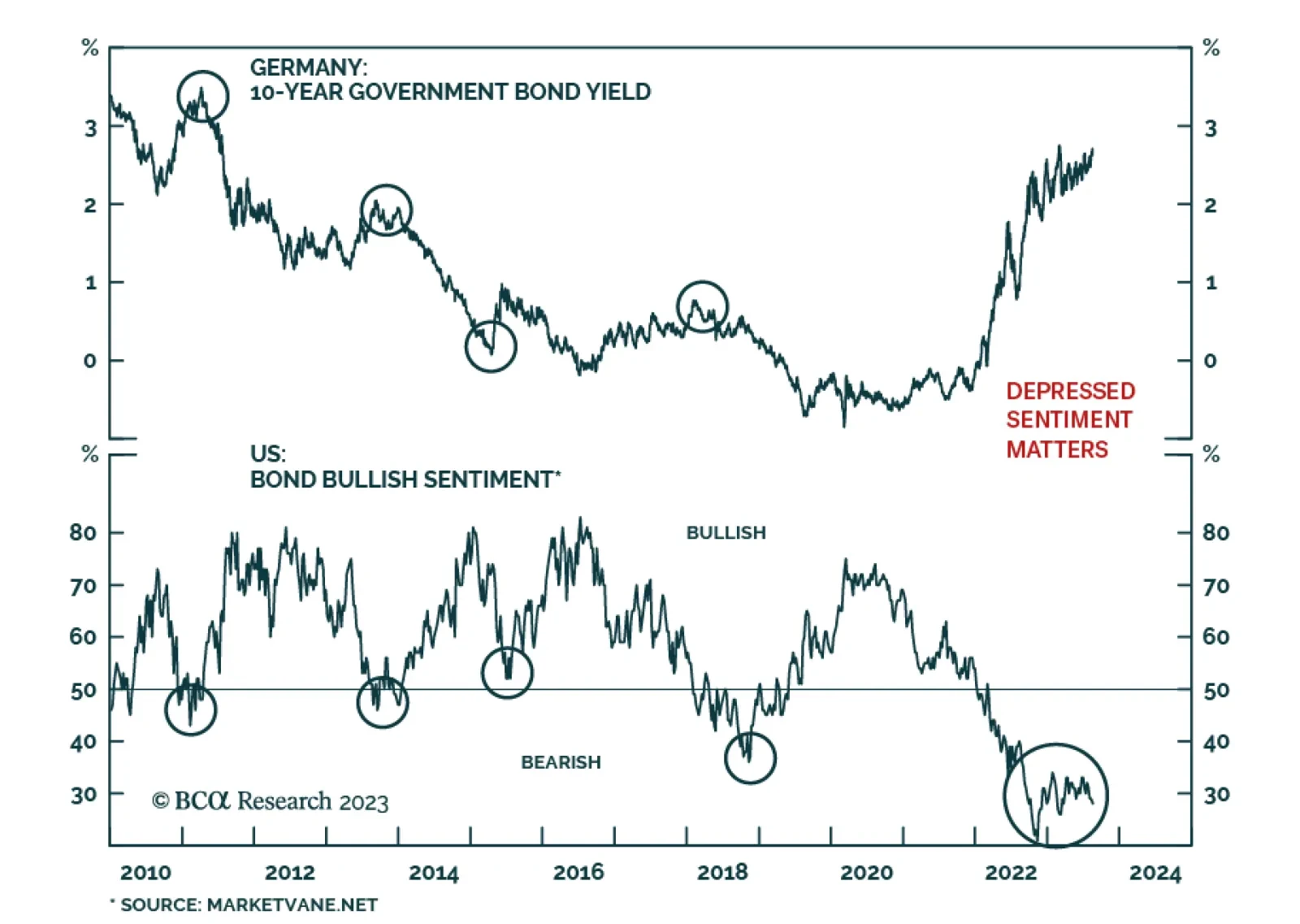

While the bearish bond trade currently has a lot of momentum, we continue to think that Treasury yields are close to a cyclical peak and will be lower on a 6-12 month horizon.

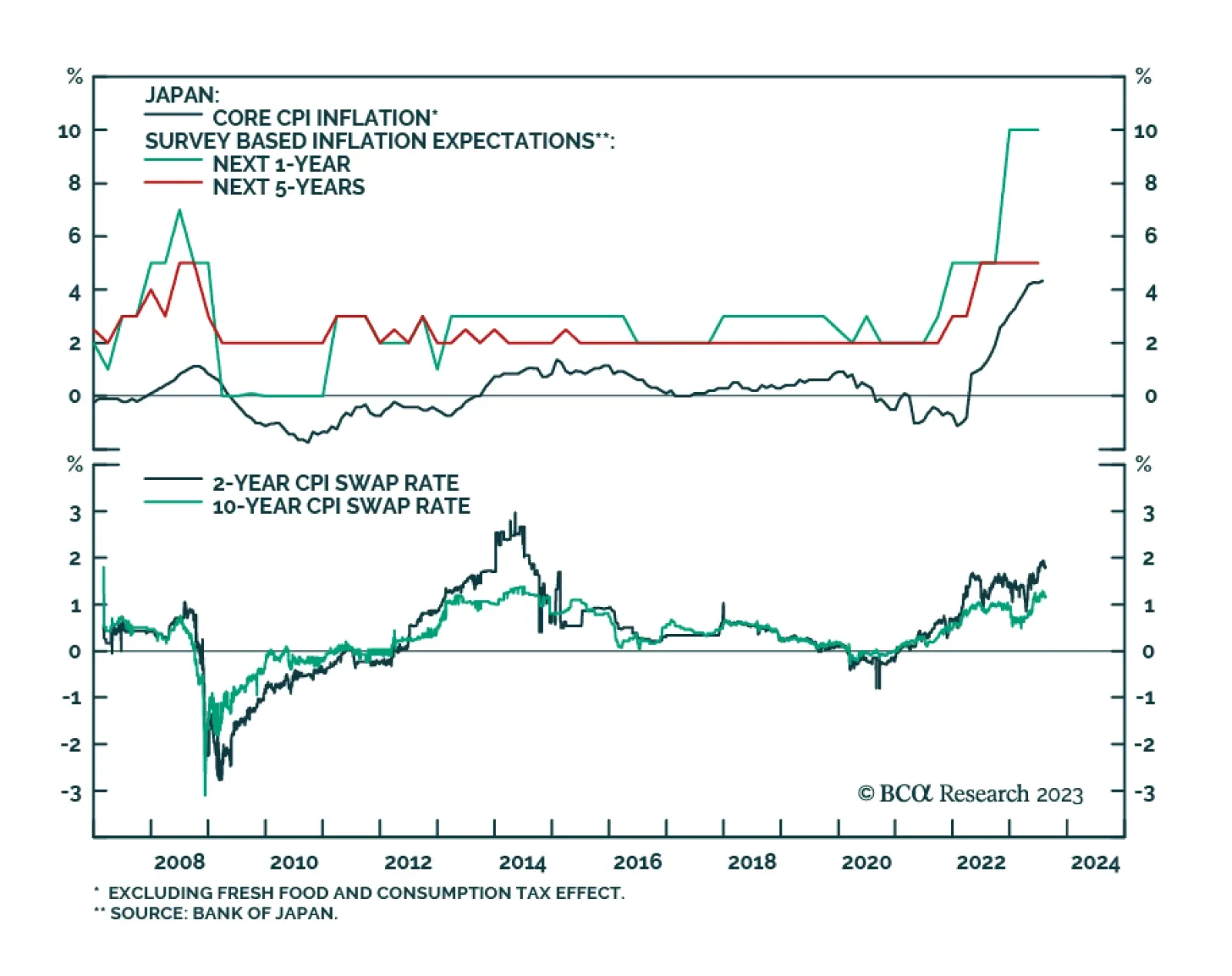

In this special report, we discuss whether the economic conditions necessary for a stronger yen (and higher JGB yields) will materialize over the next 12-to-18 months.

The next six-to-nine months hold a crucial test of whether the equity market will ratify the soft landing and the Biden administration or not. If so, then markets will rally on policy continuity and likely gridlock. If not, then markets will struggle until the election is over and again in 2025-26.