Policy

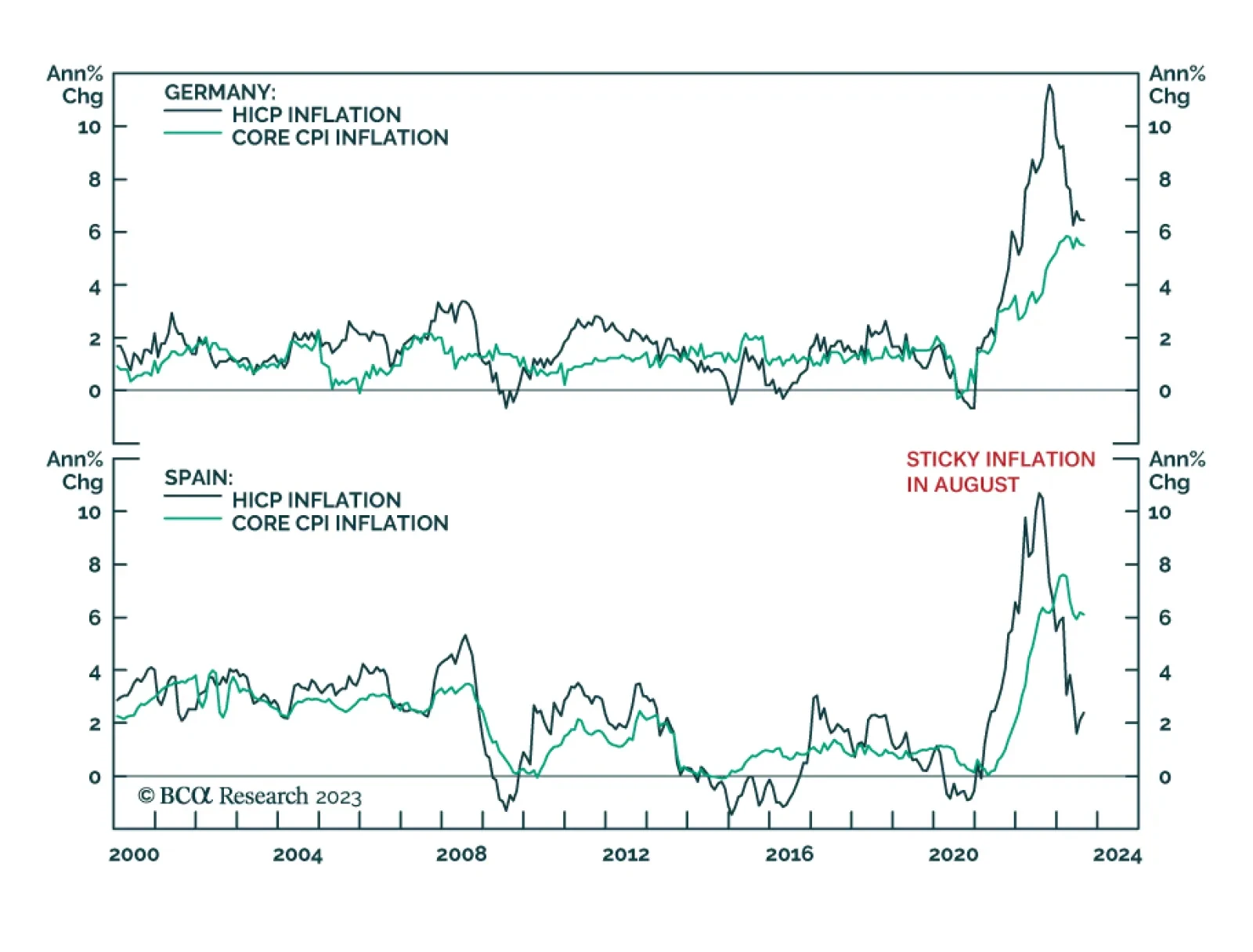

Euro Area inflation data surprised to the upside on Wednesday. According to preliminary data, although Germany’s harmonized headline CPI inflation rate fell from 6.5% y/y to 6.4% y/y in August, it nevertheless came in above consensus estimates calling for…

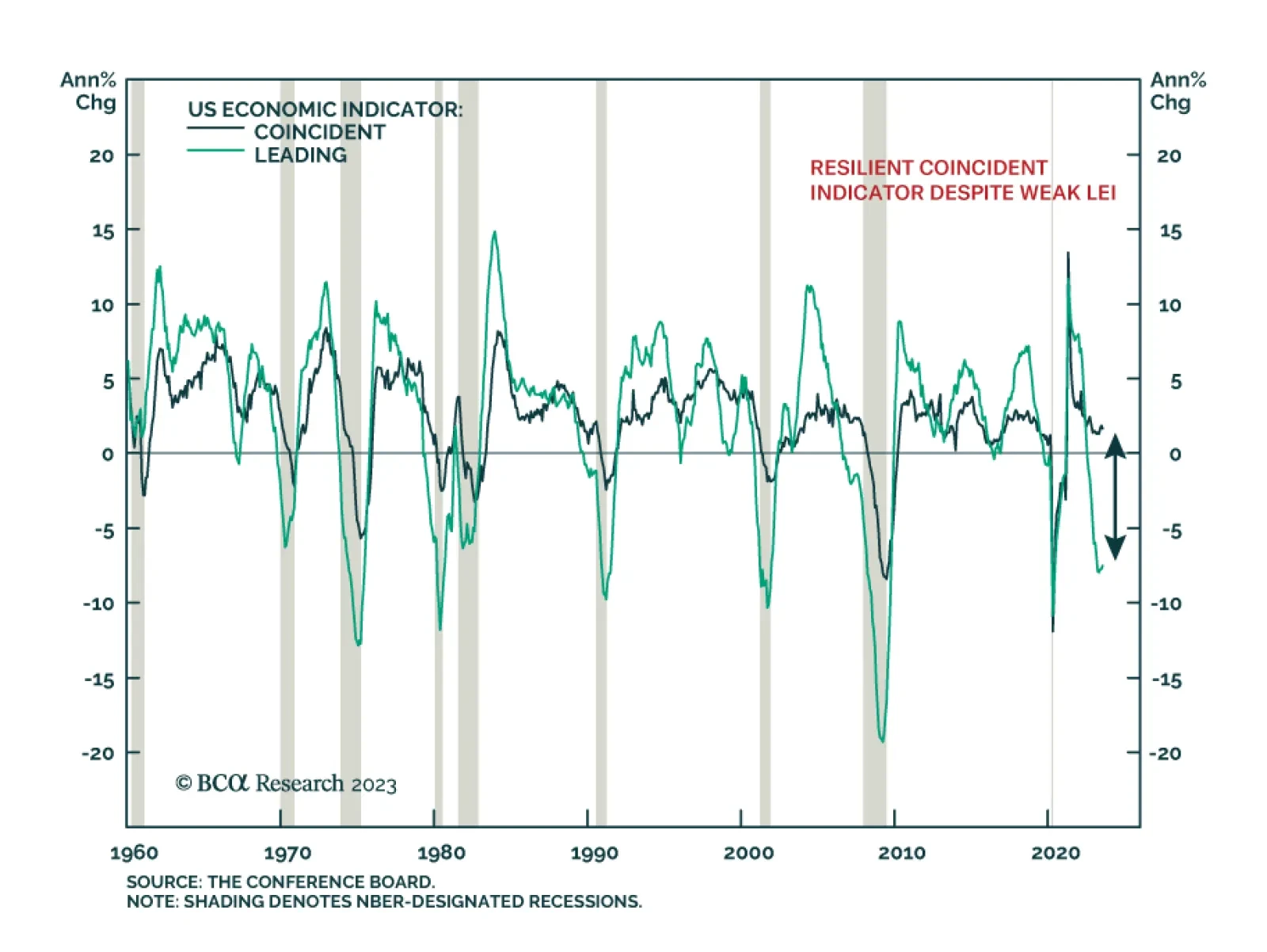

Consensus expectations for the US economy were bleak at the start of the year. In hindsight, this pessimism was excessive: real GDP expanded in the first two quarters of the year (see Country Focus). Similarly, the US Conference Board’s Coincident Economic…

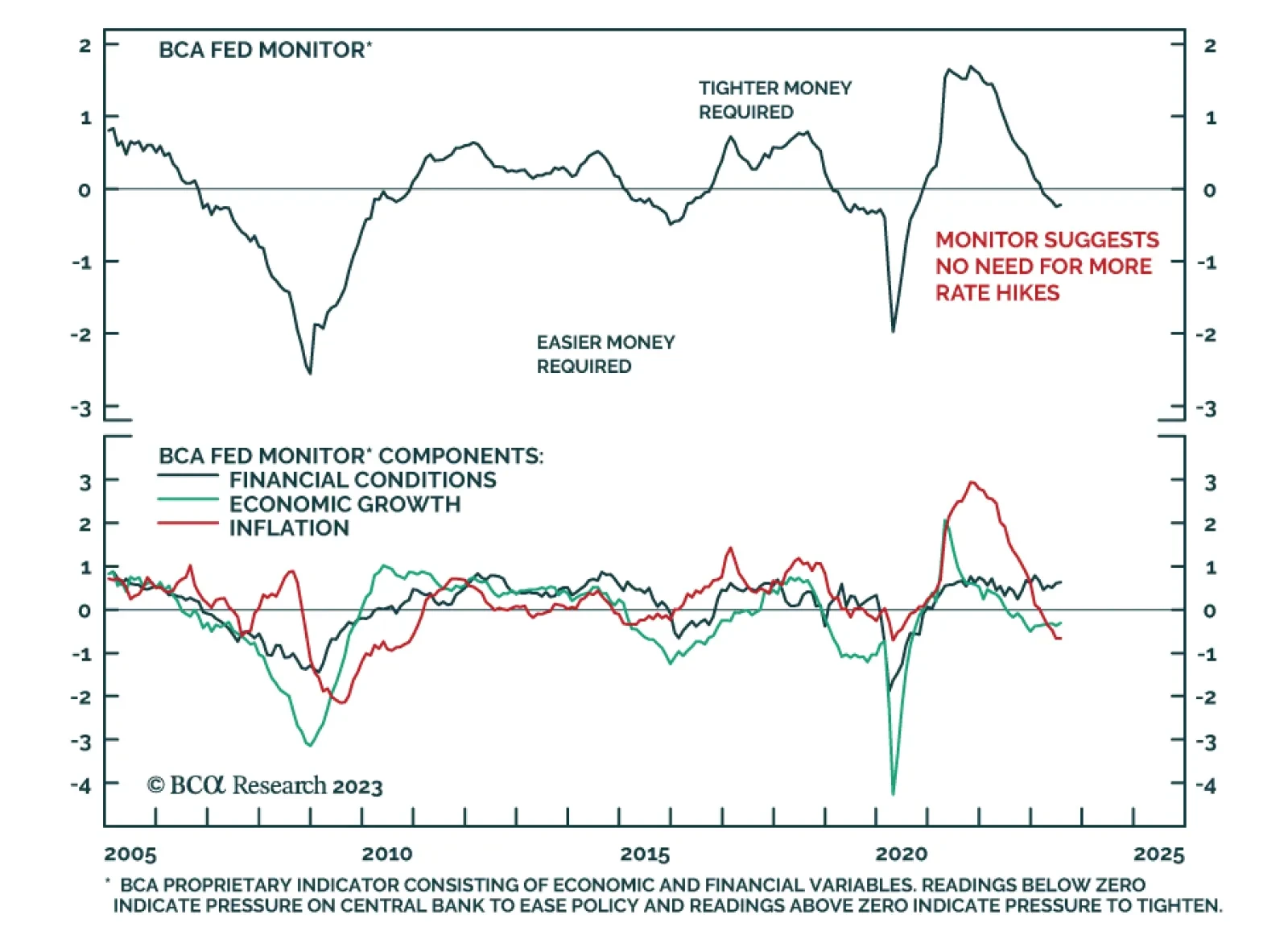

We comment on Jay Powell’s Jackson Hole speech and recommend shifting to a barbelled allocation along the Treasury curve.

The US and China agreed to hold trade talks more regularly on August 28, even as they fell short of establishing a strategic détente or general reduction of tensions. US Commerce Secretary Gina Raimondo visited Beijing and met with Chinese Premier Li Qiang…

Investors should underweight global equities and risk assets; overweight US stocks relative to global; and overweight defensive sectors versus cyclicals.

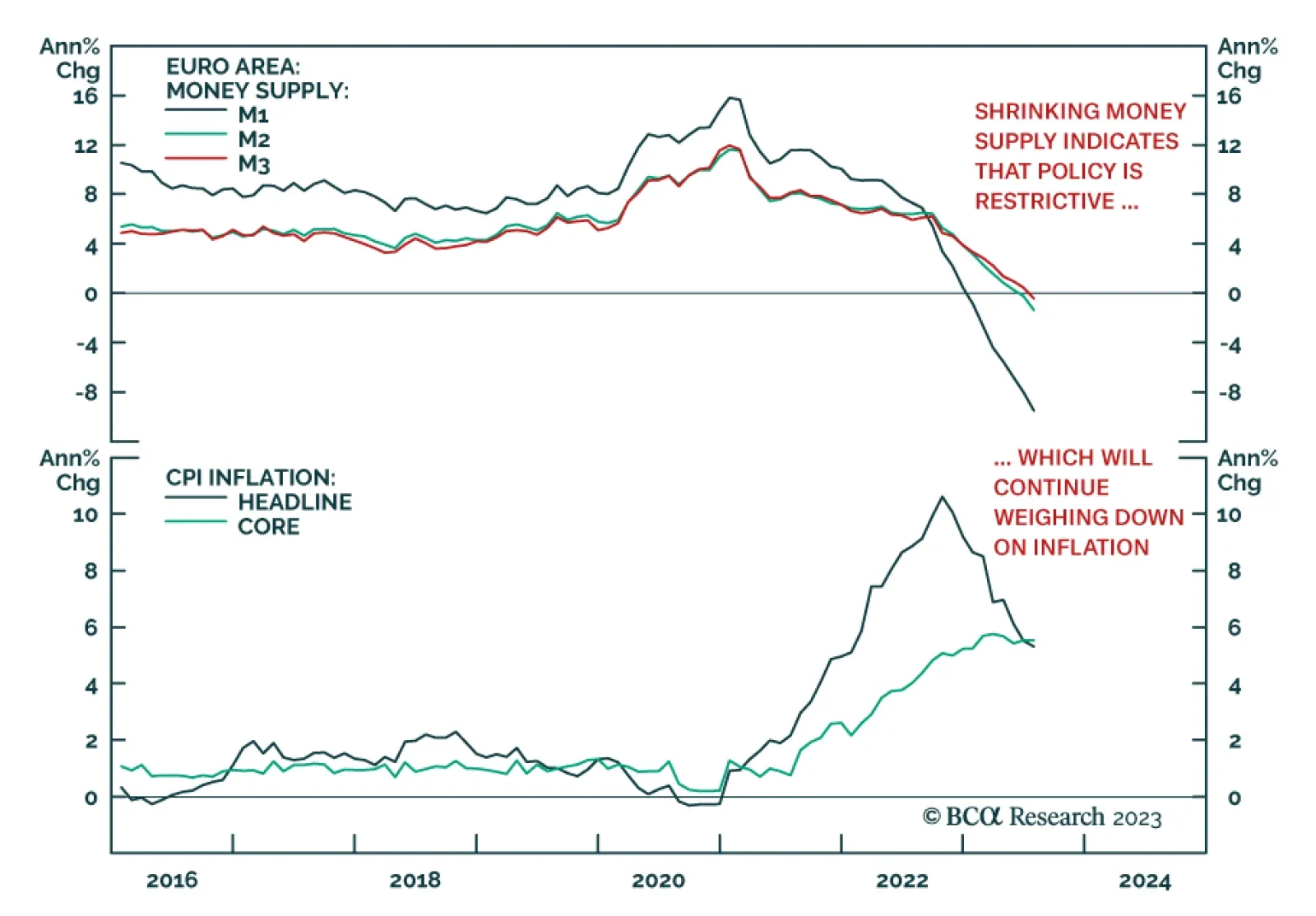

Eurozone money supply data reflect the impact of the ECB’s aggressive tightening campaign on the region’s economy. Data released on Monday showed the July M3 measure of broad money (the sum of M2, repurchase agreements, money market fund shares/units and…

Today’s Strategy Report chartbook presents the data underpinning our view that both inflation and growth are slowing, likely pointing to a recession beginning sometime in the first half of next year. We are tactically equal weight across asset classes after being stopped out of our equity overweight on August 17th and expect our next move will be to underweight equities and overweight fixed income, in line with our twelve-month view.

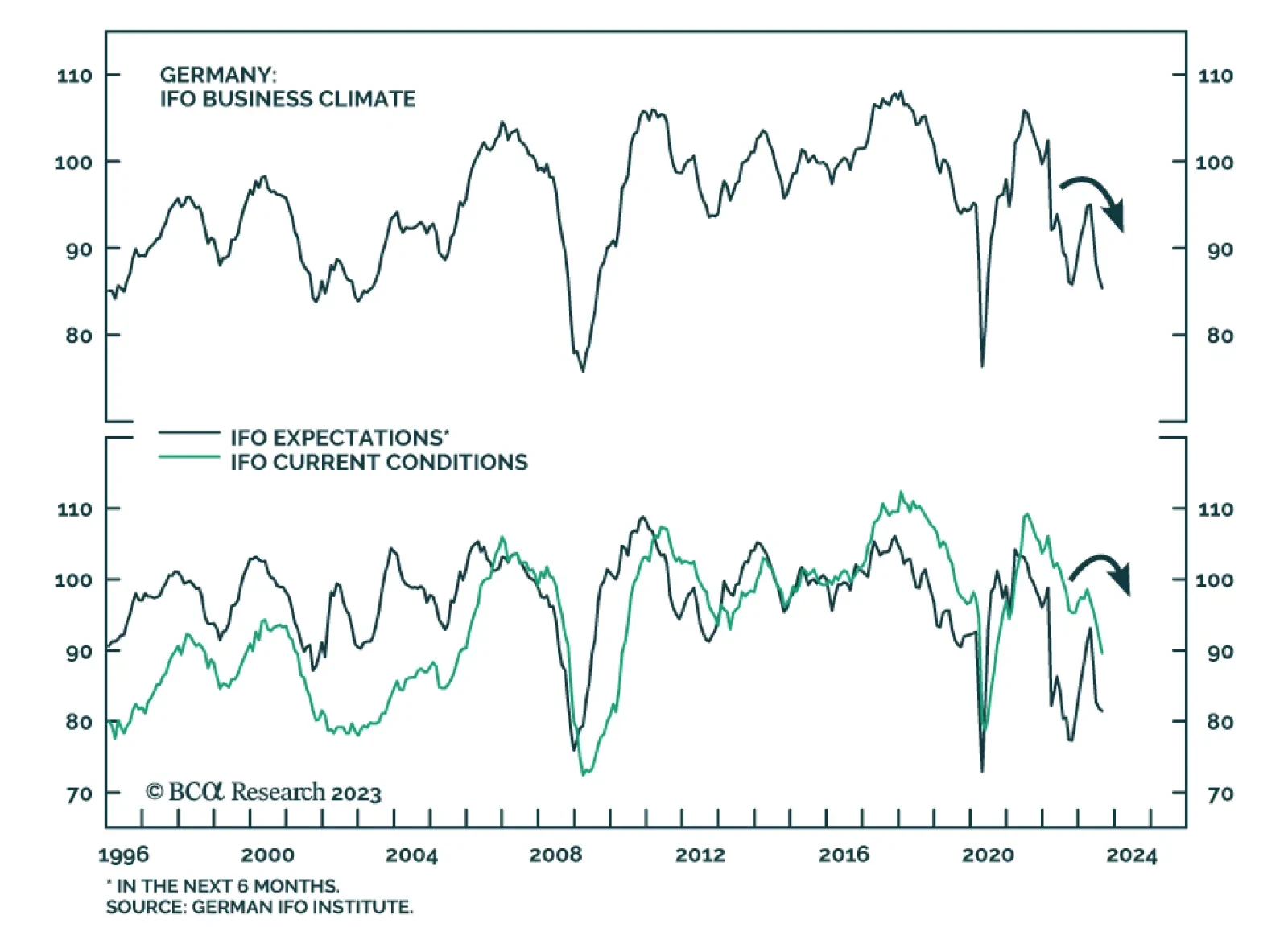

Germany’s IFO survey sent a downbeat message on Friday. The headline Business Climate Index fell by 1.7 points to 85.7, below expectations of 86.8 and near the 85.2 level at which it bottomed in October. A 2.4-point decline in the Current Assessment…

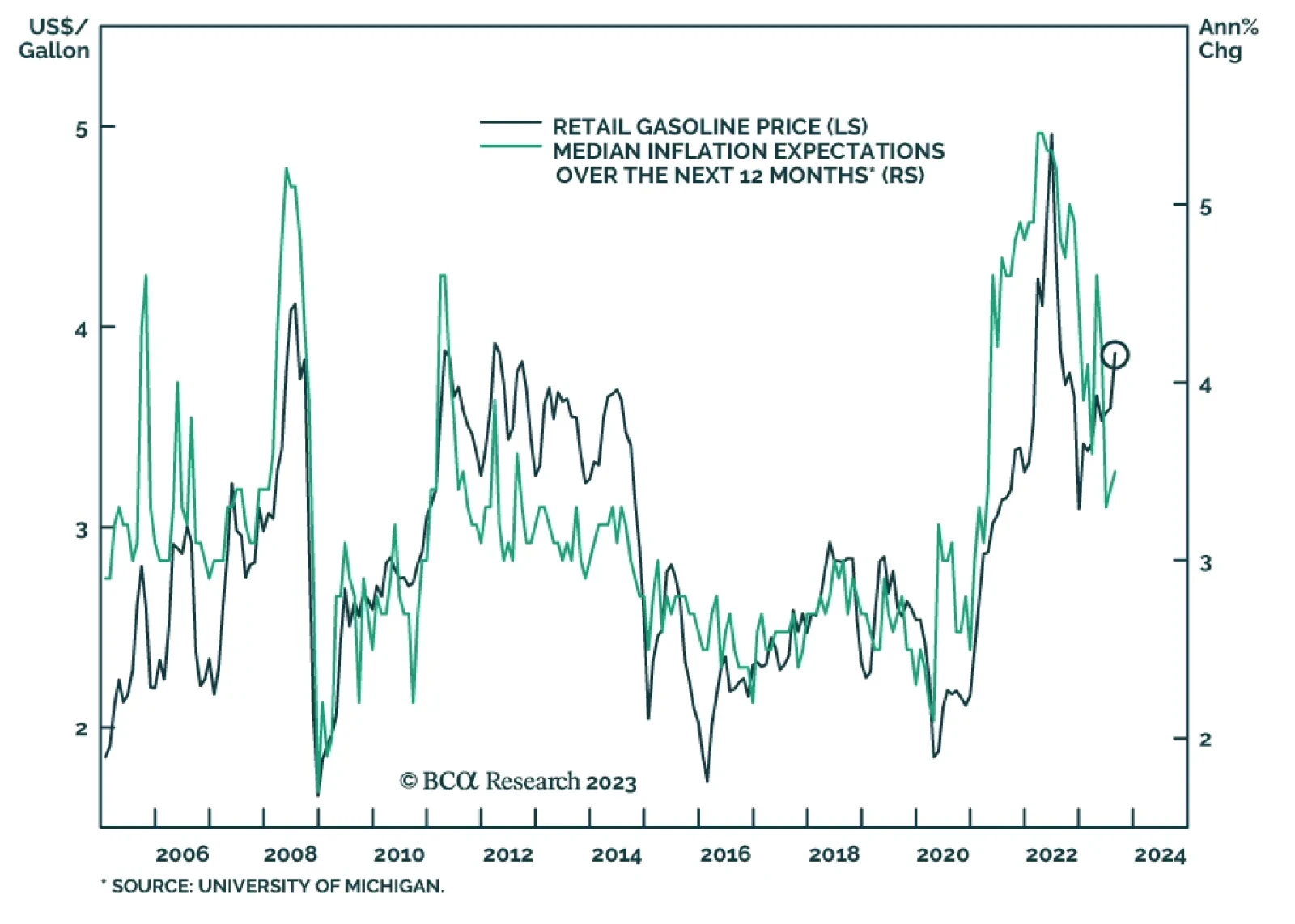

The final release of the University of Michigan’s gauge of US consumer inflation expectations unexpectedly rose in August. It shows 1-year ahead inflation expectations increased by a tenth of a percentage point to 3.5% (an upwards revision from the…

The Treasury market’s reaction to Fed Chair Jermone Powell’s Jackson Hole speech was relatively tame on Friday. Although there was some volatility during the speech, the 10-year yield ended the day broadly unchanged. Meanwhile, the 2-year yield rose by 5.5…