Oil

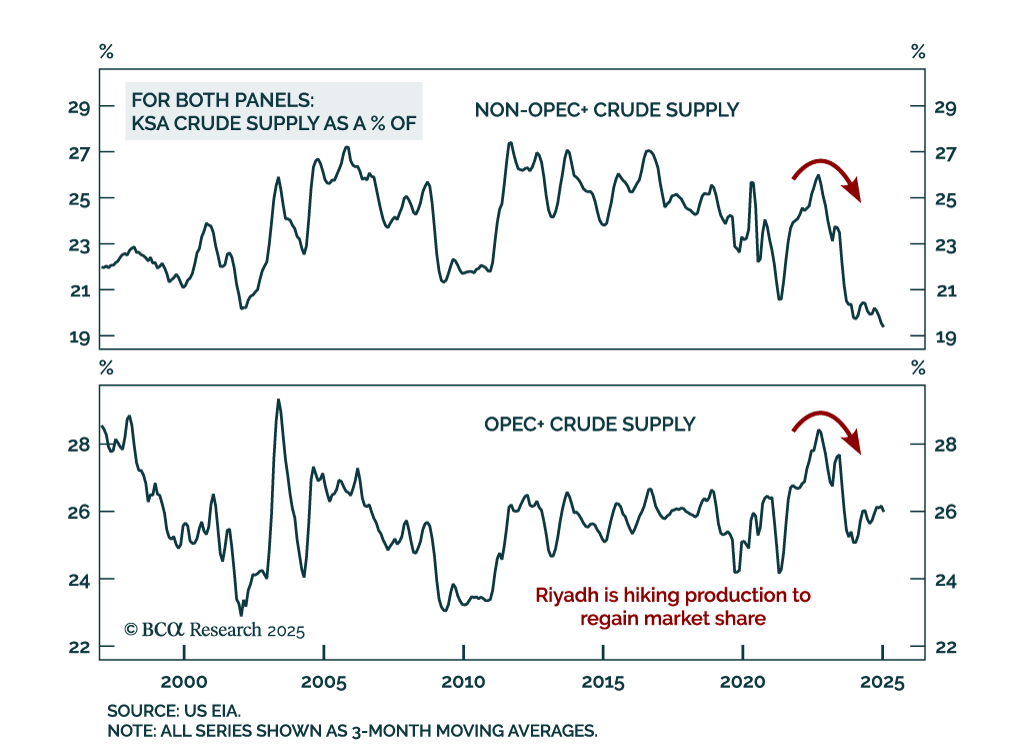

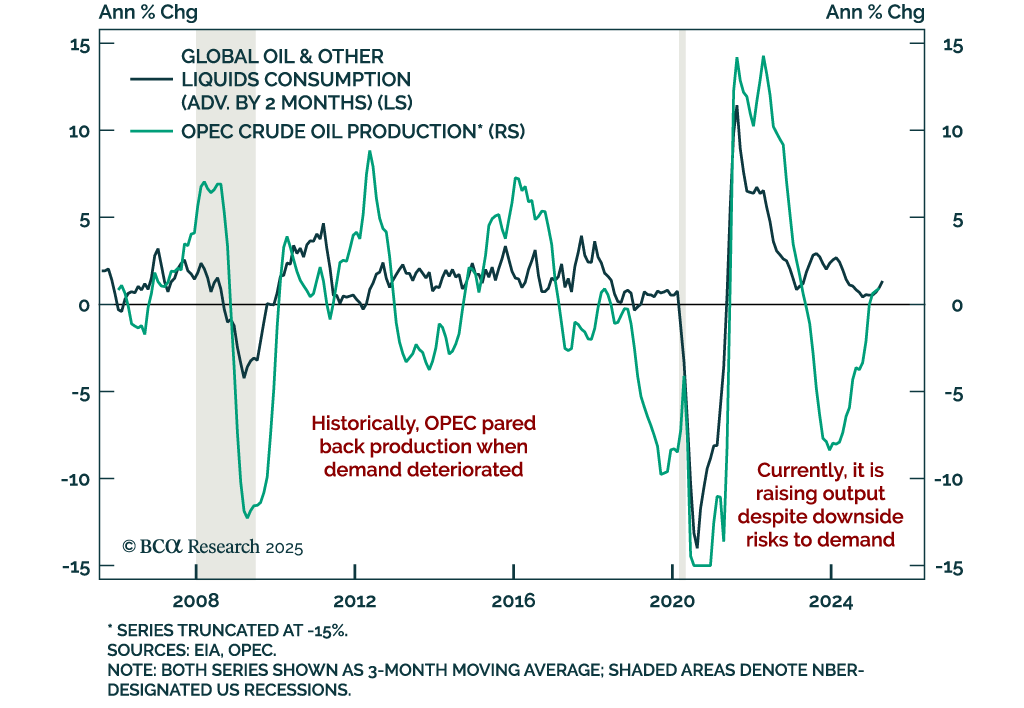

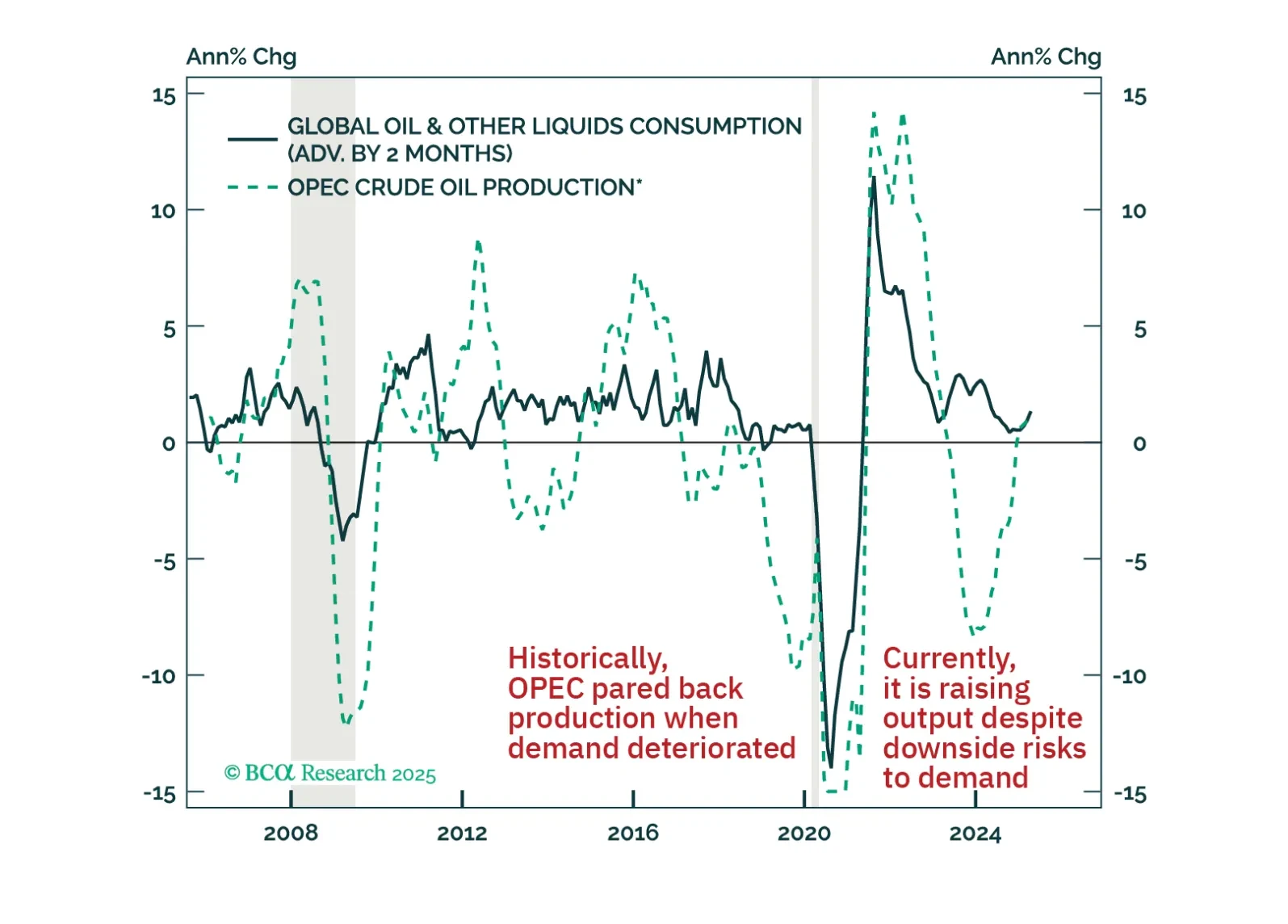

OPEC+ recently announced another outsized oil production hike, tripling its planned June output increase to 411k b/d for the second consecutive month. Our take on why KSA is boosting crude output at a time of heightened downside demand risks is that it is pursuing an oil price war lite. President Trump is not only blessing this strategy but also depending on it.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

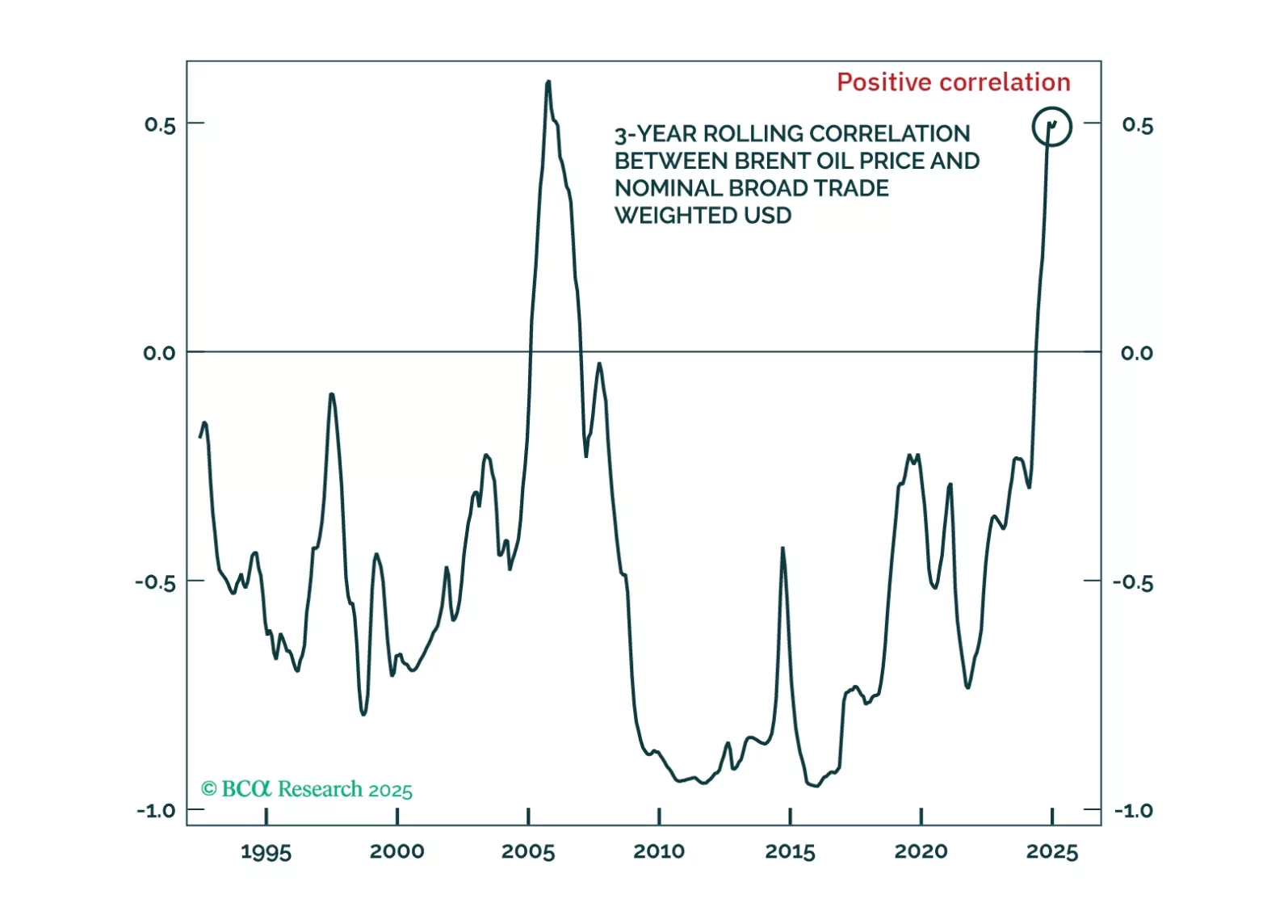

Oil has borne the brunt of the year-to-date deterioration in cyclically sensitive financial assets. It is a key underperformer both within the commodity space and among global risk assets. This underperformance underscores that in addition to the trade war-induced headwind to demand, bearish supply-side developments are also weighing down on crude prices. As we discuss in this report, these dynamics will likely continue exerting downside pressure on oil prices over the coming weeks and months.

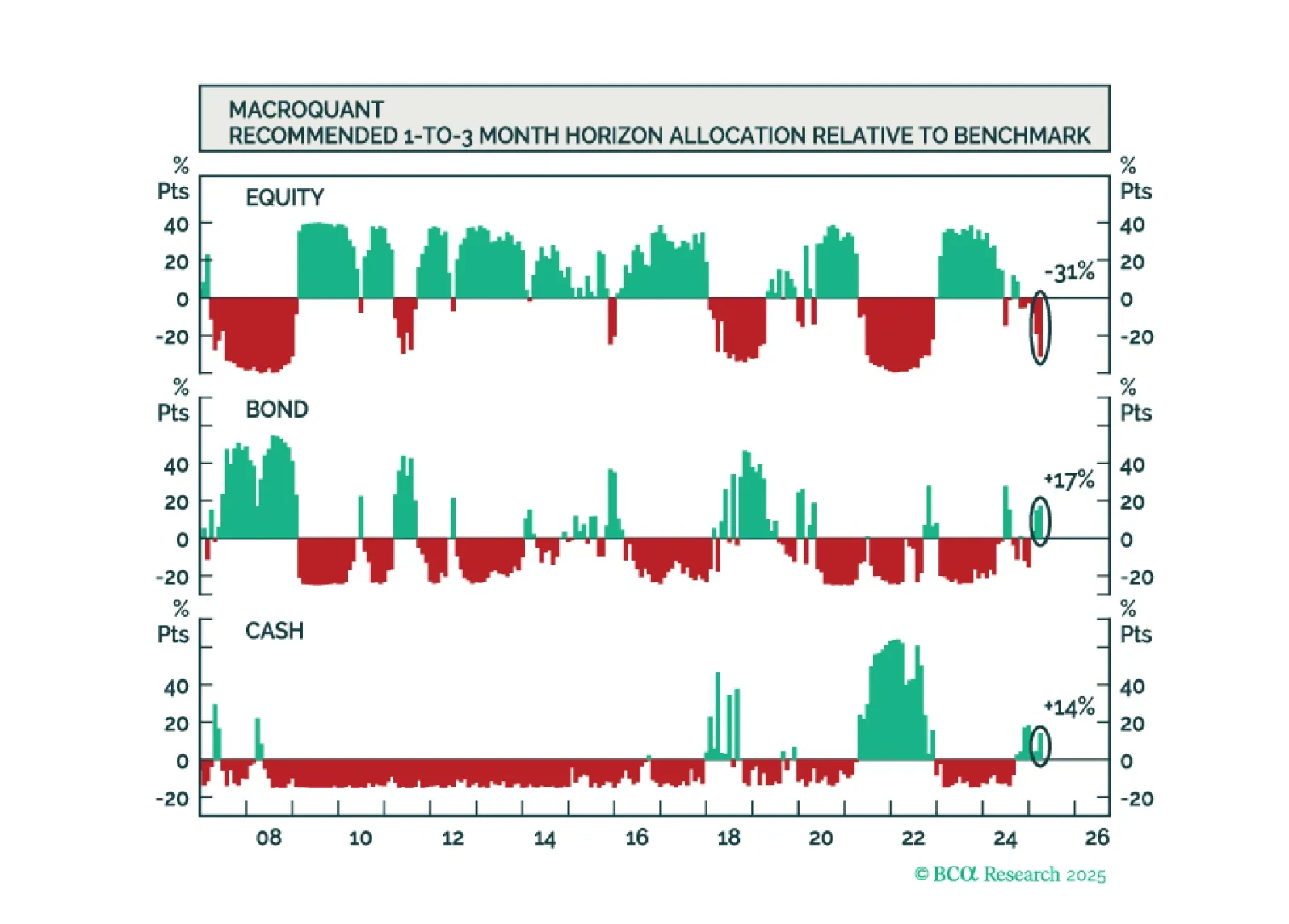

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

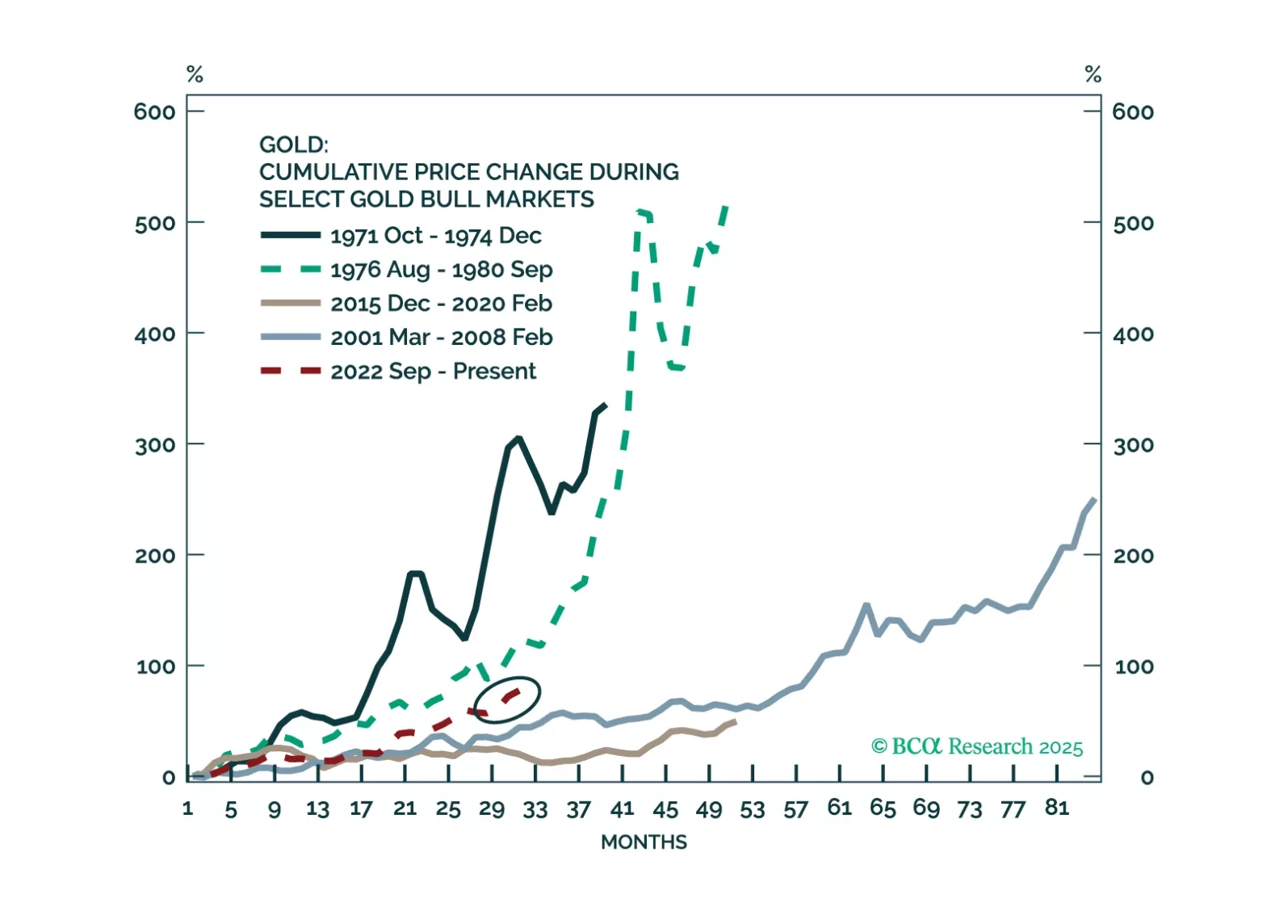

Commodities have not been spared the wrath of the post-"Liberation Day" selloff. However, in the sea of red, gold continues to shine bright, climbing to a fresh record high. How much further does the recent price action have left to run? We explore technical indicators to gauge the likely price outlook for gold, oil, and copper over the coming months.

Commodity prices are succumbing to the risk-off environment triggered by President Trump’s reciprocal tariff announcement. The latest events and market moves raise several important questions about the outlook for commodity markets.

In this Strategy Report we address some of the most pressing questions raised during our recent discussions.

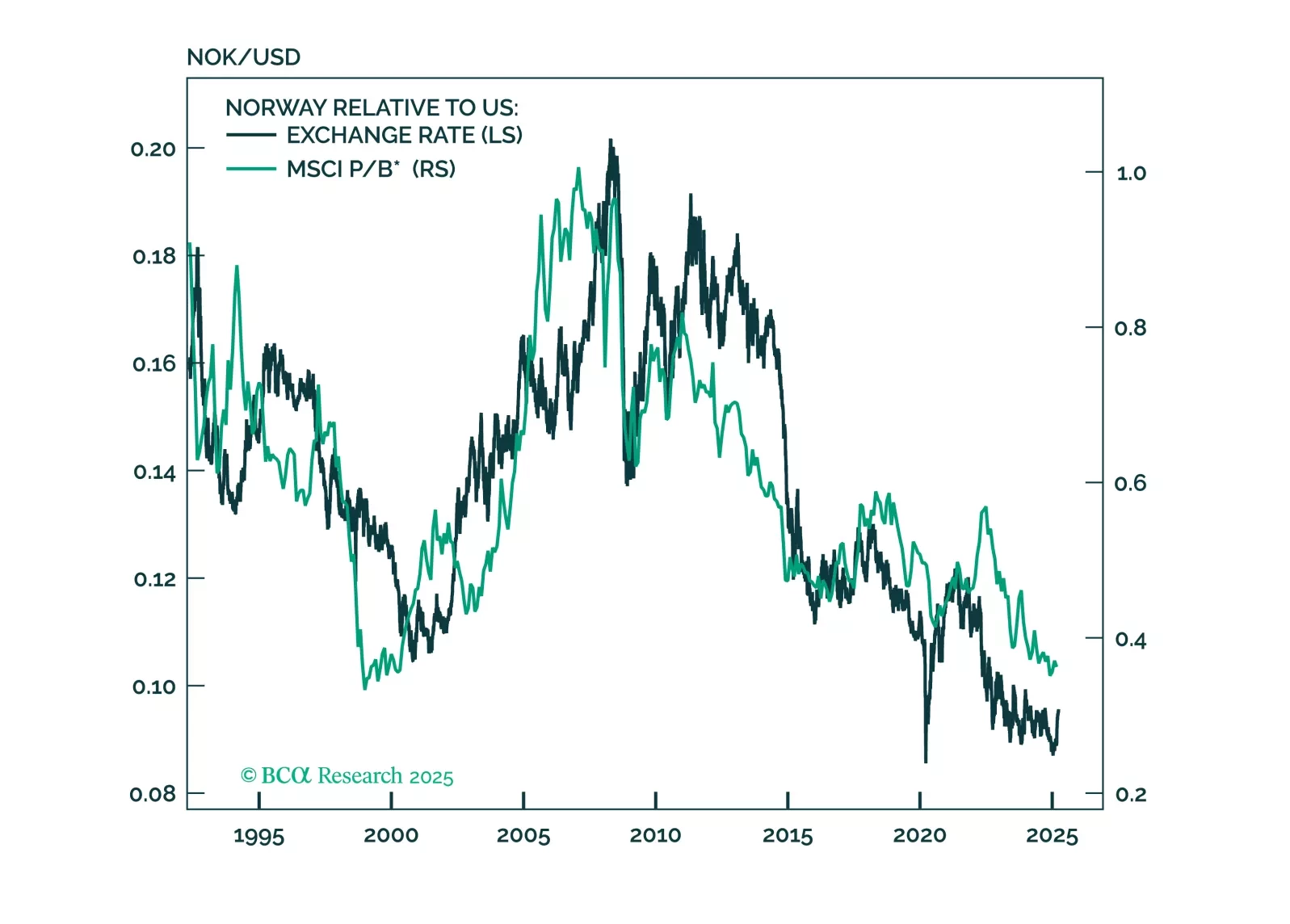

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.